With George Gilbert and Rob Strechay

At Cloud Next, Google showcased its strong leadership position in data and AI. In our view, Google’s messaging, demos and tech-centric narrative have broad appeal for developers and next generation startups. As well, the company’s focus on solutions, contrasts its strategy to the typically disjointed services we’ve seen from AWS over the past decade. Google also showed off an expanded ecosystem of GSIs and smaller CSPs, encouraging the broad use of Google’s kit globally. While Google remains a distant third in the Iaas/PaaS race, with revenue one-fifth the size of AWS, it is playing the long game and betting the house on AI as a catalyst to its cloud future.

In this Breaking Analysis we unpack the key takeaways from Google Cloud Next with Rob Strechay and George Gilbert. We’ll share ETR data that positions Google’s AI relative to other leaders and we’ll contrast Google’s data-centric strategy with traditional architectural models.

Google’s Trifecta and Gen AI Impacts on the Tech Industry

The following points summarize our key takeaways from Google Cloud Next.

- Google’s Trifecta: Coming out of Next, John Furrier coined the phrase “Google trifecta” referencing Google’s focus on:

- Developers – Offering low code, no code and advanced coding solutions for greater developer accessibility. Furrier makes the point that today’s 20-something developers grew up without Microsoft Office. Rather they used Gmail, Google Docs and other Google tools and have a familiarity with and positive view of the Google brand.

- Solutions – Showcasing the rapid evolution of generative AI (Gen AI) co-pilots, which are integrated across products.

- Ecosystems – Google presented its advanced integrated data and AI platform, emphasizing a data-centric approach over traditional DBMS-centric architectures. As well, the company showcased a number of global system integrator partners and smaller CSPs that Google is encouraging to use its technologies globally.

- Acceleration in Compute: Google’s advancement in compute with its TPUs (Tensor Processing Unit) serves as partial answer to the current GPU shortages, further promoting Gen AI’s integration across all their products. The tradeoff is that users need to use Google tools. But it provides a path to developers who are GPU constrained.

- Security: Google emphasized on full development and operations security (DevSecOps) capabilities, a noteworthy mention especially in light of Microsoft’s recent security shortcomings; and Google’s 2022 acquisition of Mandiant.

From the Field (Rob’s Perspective):

- The energy and turnout at the show was impressive, with the Moscone event selling out to 20,000 attendees.

- Demonstrations, such as an AI-powered Wendy’s drive-through, showcased Google’s real-world applications of its technology, emphasizing developer centrality, open-source, and extensibility.

Remote Observations (George’s Insight):

- Gen AI: Perhaps the biggest accelerant the tech industry has ever seen. Gen AI is unique as it boosts both the demand for applications and the supply – i.e. the capability to develop them. Previous technological shifts enhanced demand, but Gen AI propels the creation of new apps.

- Infrastructure Bottlenecks: Despite Nvidia presenting some roadblocks in terms of supply, Google has anticipated the need for acceleration. With their infrastructure, especially their fifth-generation TPUs, Google can infuse Gen AI across all their offerings. In comparison, Microsoft faced internal challenges, having to ration access to GPUs.

Bottom Line: In our view, Google’s latest advancements, particularly in Gen AI, underscore its vision for the future of computing. By focusing on the developer experience, optimizing solutions, and expanding their ecosystem, Google is setting the pace in a new phase of the cloud market where rapid innovation based on AI is paramount. Their ability to anticipate and address infrastructure challenges is also commendable, positioning them ahead of competitors like Microsoft in this arena. The emphasis on security, especially given recent security breaches at other tech giants, further underscores Google’s comprehensive approach. We believe that Google’s strategic direction in AI and cloud will have significant ramifications for the broader tech industry as Google becomes a more viable cloud alternative for developers and industry participants.

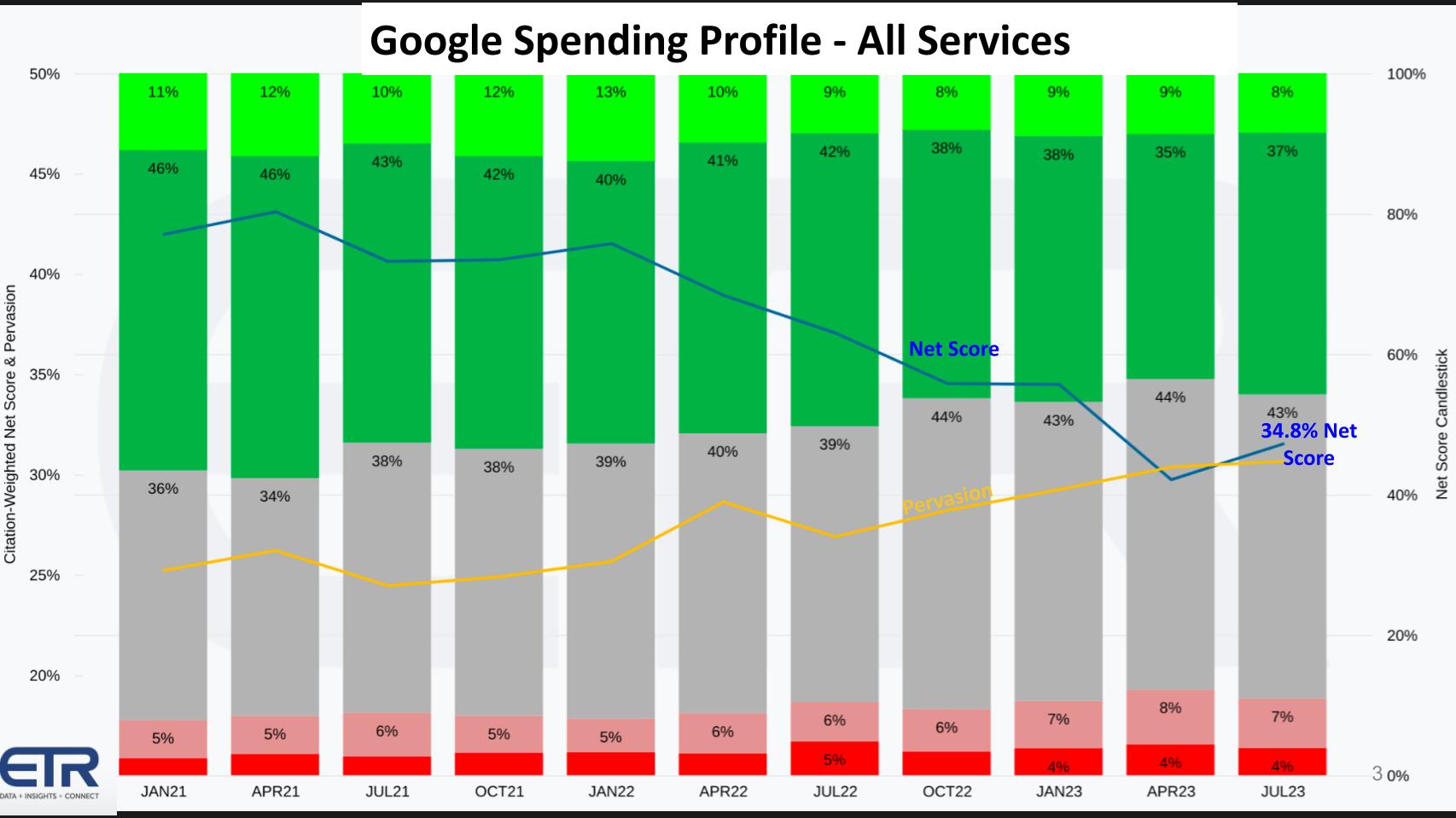

ETR Data Shows Overall Spending on Google’s Cloud Services Lags but is Improving

The following chart shows the overall Google spending profile across all Google Cloud services that ETR tracks.

This chart above shows the granularity of ETR’s proprietary Net Score methodology. Net score is a measure of spending momentum. The lime green boxes show new customer ads. You can see in the July survey, 8% of the customer surveyed were new to Google Cloud. The forest green, at 37% of Google customer respondents, represents customers spending 6% or more. The gray is flat spending. That’s a big chunk of Google’s profile as it is with most vendors these days. The pinkish area at 7% represents spending down 6% or worse. And the bright red at 4% is churn.

Subtract the reds from the greens and you get a net score of 34.8%, represented by the descending blue line that bottomed in the April survey and bounced back in the July measurements.

The yellow line is pervasiveness in the dataset. In other words, it takes the total N of Google customers divided by the total N of the entire survey, which is around 1700. This figure measures the share within the survey.

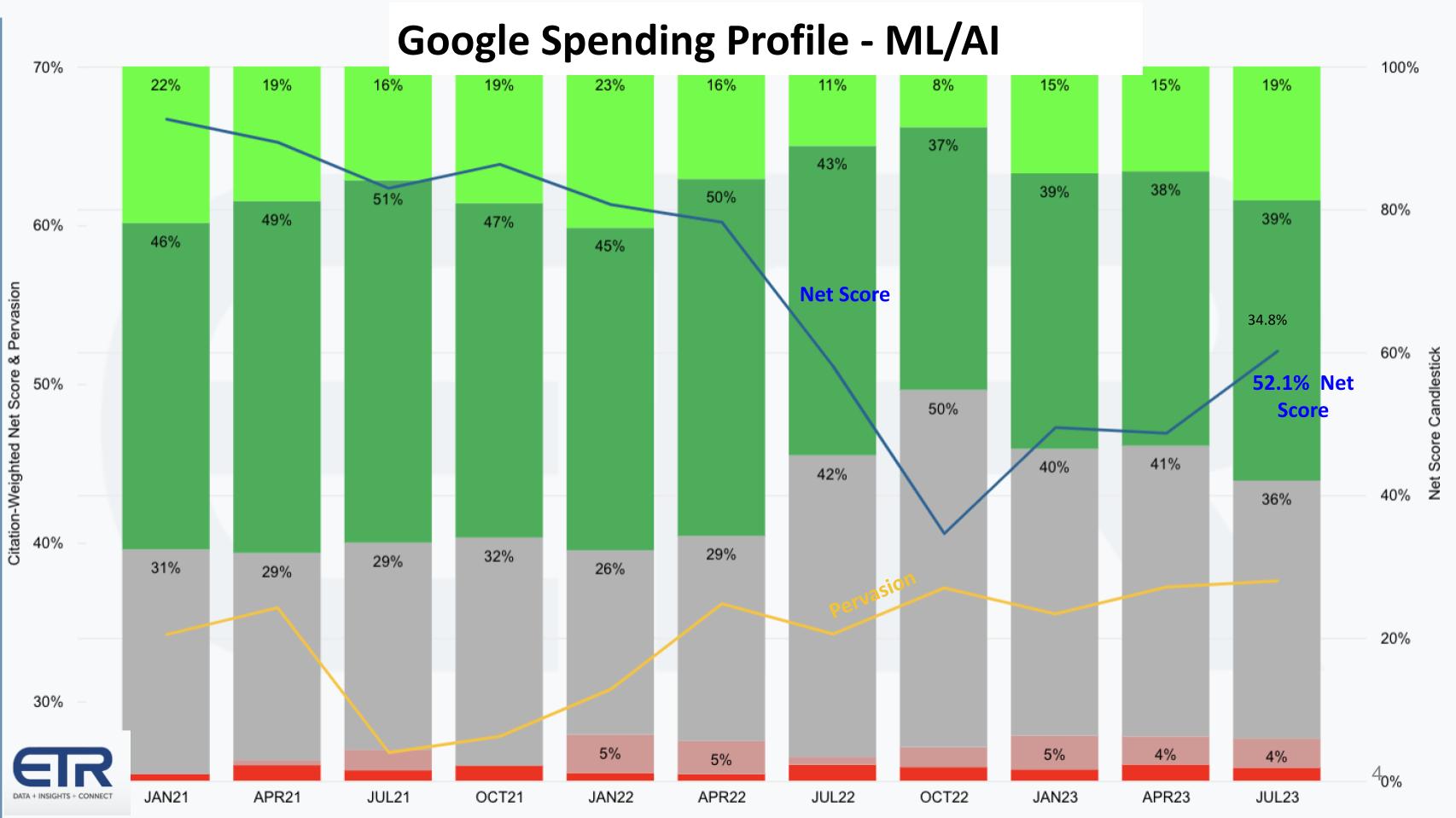

Google’s AI Performance Shows a Different Picture

Below we show what happens when we cut the data only on Google’s AI offerings.

You can see above, Net Score bottoms in October 2022, the month before ChatGPT is announced. We were seeing the slow deceleration of AI / ML spend post pandemic. And then Google responds with Bard other AI tooling at Google I/O earlier this year and you can see its next net score jumps to 52.1%. We should note that despite Google’s AI prowess, it still ranks lower than the other big cloud players, Microsoft and AWS and we’ll show you some comparison data in a moment. Nonetheless, Google’s momentum is headed in the right direction and based on what we saw at Google Next, they intend to make inroads.

Architectural Differences and Gen AI Impacts on Market Leaders

In addition we make the following observations:

- Google’s AI Integration Strategy:

- Google’s widespread AI integration is attributable to its unique architecture encompassing its compute layer, storage layer, and application solutions.

- By owning the entirety of these solutions and platforming them uniformly, Google can seamlessly infuse AI capabilities across its suite.

- This integration surpasses even Microsoft’s Office 365 with OpenAI due to Google’s cohesive platform design.

- AWS’s Unique Challenges:

- AWS’s product suite is akin to 300+ individual services, lacking the unified layer that Google and Microsoft possess.

- While AWS might introduce AI capabilities to its services, the inherent disjointed nature could slow down the AI implementation process across its platform.

- AWS’s AI Capabilities – A Mixed Perspective:

- While some argue AWS lags behind in AI, given recent articles and critiques (such as those from The Information and Charles Fitzgerald), it’s also essential to recognize AWS’s established historical presence in AI, notably via SageMaker. But from a public relations standpoint, Google and Microsoft have outgunned AWS thus far.

- It’s early in the AI game, and while AWS may seem behind, they’ve historically not settled for anything but the top spot and re:Invent will give AWS the last word of 2023.

- Infrastructure Mindset Differences:

- AWS, Google, and Microsoft approach infrastructure differently. AWS has a more hardware-centric platform mindset, focusing on providing a plethora of services to enhance its hardware capabilities.

- Google and Microsoft’s software-centric mindset allowed them to re-platform their services swiftly, leveraging Gen AI’s advantages.

- This fundamental difference explains AWS’s challenges: mindset misalignment, delays in core AI tooling, and infrastructure rationing.

- Market Perception – “The Boomer Cloud:”

- As mentioned above, John Furrier highlighted a generational shift in tech affinity, noting that developers in their twenties predominantly grew up using Google’s suite (Docs, Gmail), which may skew their loyalties towards Google.

- An intriguing remark at Next labeled AWS as the “Boomer Cloud,” implying its potential diminishing appeal among younger developers.

Bottom Line: In our view, Google is making inroads with developers (AWS’ historical stronghold) and solutions for enterprises (Microsoft’s strength). Google and Microsoft may have an edge due to their more cohesive software-centric platforms. AWS’s modular approach poses challenges in the rapid AI integration race. Despite AWS’s potential challenges, our research indicates that it would be unwise to underestimate them given their historical competitiveness. However, the broader tech landscape’s shifting generational perceptions, with younger developers leaning towards Google, could have lasting ramifications on market dominance in the coming years.

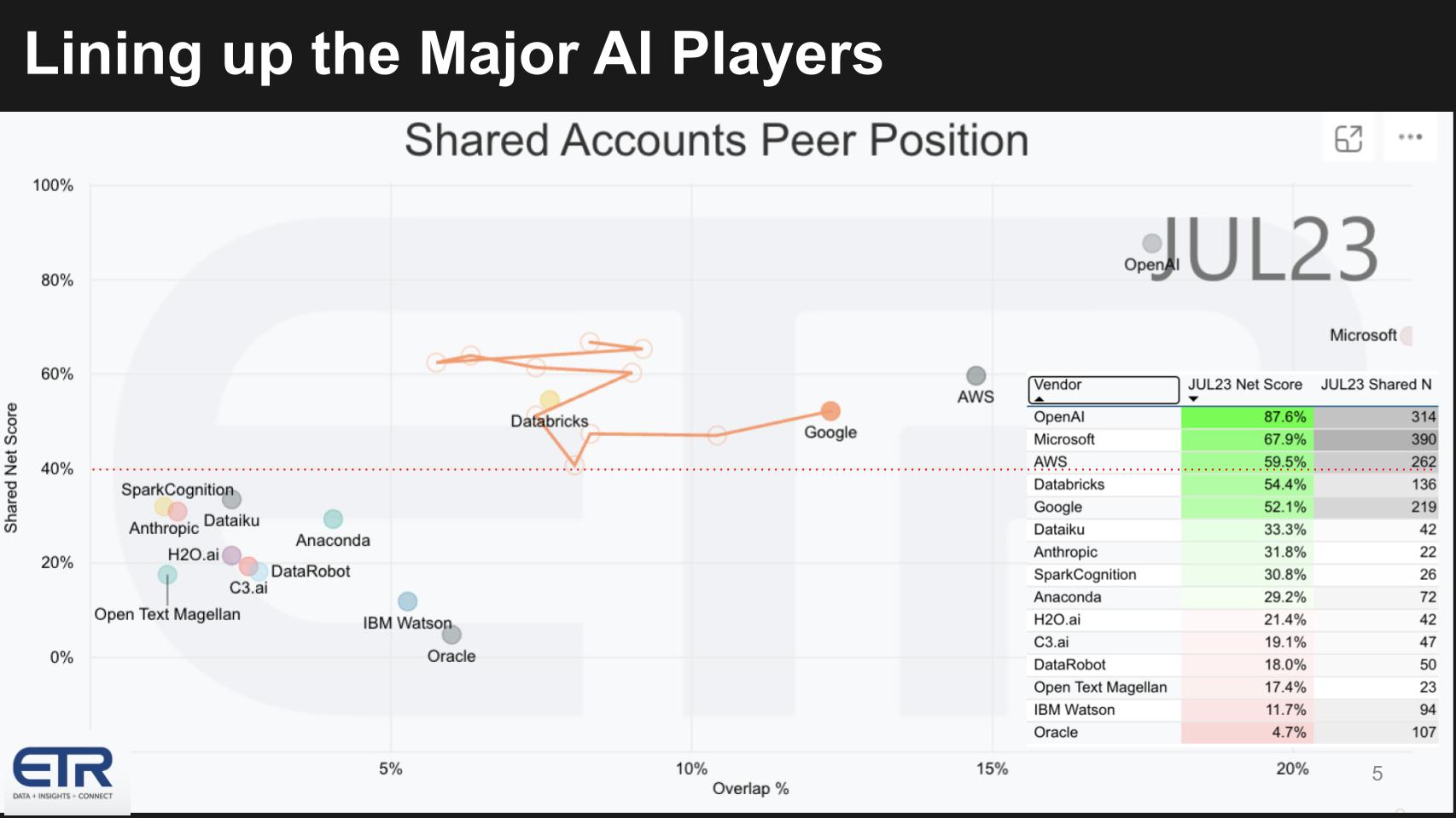

Google Still Lags Microsoft, OpenAI and AWS in AI Spend Momentum & Market Presence

Above we show the AI spending comparison the AI leaders found within the ETR data set. In the chart, Net Score or spending momentum is on the vertical axis and the penetration in the data set or overlap is shown on the X axis. The inserted chart on the right informs how the dots are plotted.

The key points are:

- OpenAI at an 88% Net Score with 314 citations, an N only second to the ubiquitous Microsoft. Microsoft has catapulted itself into a leadership position with the OpenAI relationship.

- AWS has always been a major player with Sagemaker and now with Bedrock, Titan, and other GenAI tooling it continues to show strong momentum.

- Databricks also shows strong spending momentum with a Net Score above the 40% red dotted line, an indication of highly elevated spending velocity.

- Google’s progress is shown with the squiggly orange line, an impressive move to the right. However relative to the moves AWS and Microsoft have made in terms of market presence in the survey, Google still has much work to do.

And you can see the pack with Spark Cognition, DataRobot, Dataiku, Anthropic, H2O.ai, C3, etc. along with IBM and Oracle by the way who are both in the mix. Lower on the momentum axis but they show up in the survey.

The point here is that while Google is strong, it still has a lot of work to do to catch up in market performance.

Next we want to address the question: Will Google’s strong technical position in AI change the game in cloud? If not why not? If so…when?

Google’s AI-First Strategy in Cloud

- Google’s Home Field Advantage – AI:

- Instead of merely competing on the IaaS (Infrastructure as a Service) and PaaS (Platform as a Service) front, which AWS predominantly set as the game’s terms and which Microsoft followed, Google is leveraging its unparalleled strength in AI.

- This shift to AI is strategic, positioning Google on its “home turf,” where its expertise and innovations can be genuinely groundbreaking.

- From Solutions to Momentum:

- Google’s recent emphasis on AI reflects a pivot from general cloud solutions to a more specialized approach, capitalizing on AI-driven offerings.

- Google’s “coming out party” paints them as the quintessential “AI cloud,” which could be a significant market differentiator.

- Comparative Analysis:

- Google’s entrance into LLMs (Language Model as a Service) – especially with their Vertex AI – is a clear indication of their intent to compete aggressively in this space.

- By providing LLMs as a service, Google is signaling its ambition to make AI models as accessible and scalable as other cloud services.

Bottom Line: In our view, Google’s strategic pivot to capitalize on its strengths in AI represents a significant shift in the cloud wars. While the broader market battles on IaaS and PaaS offerings, Google’s emphasis on AI-centric solutions, like Vertex AI, and Duet may not only enhance their cloud position but also potentially redefine how cloud services are conceptualized and delivered. This approach might establish Google as the go-to cloud provider for organizations prioritizing cutting-edge AI integrations.

Recapping Google’s Architectural Innovations at Next

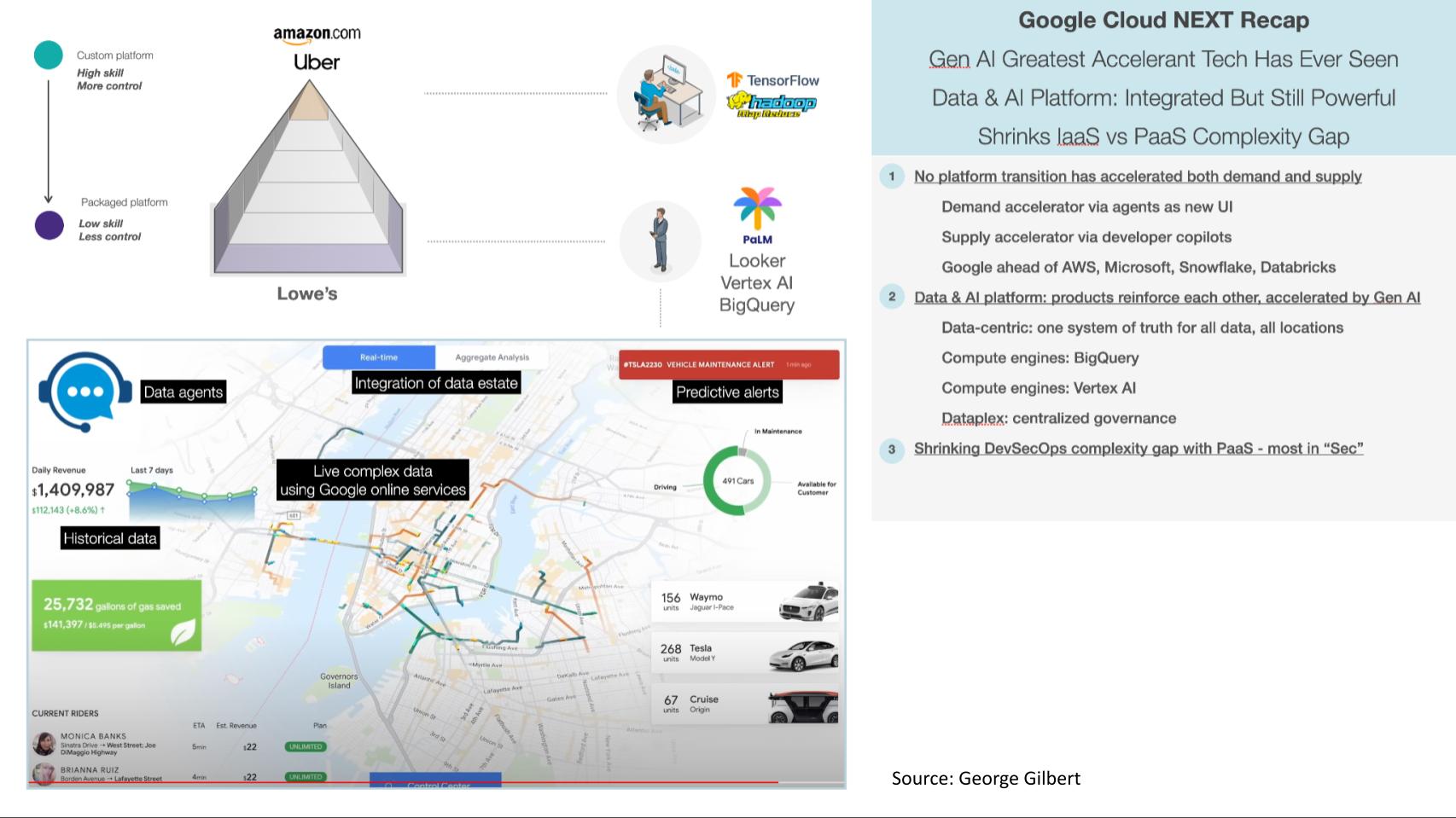

Let’s dig into some of the announcements and architectures Google showcased at Next. Above is a slide George created. The pyramid up top underscores the evolution of data apps. We’ve often used Uber and Amazon.com as leading examples of highly advanced companies with lots of engineers and deep technical expertise.

The following further summarizes the key points of George’s analysis:

Gen AI as the New Accelerant in Tech

- The Demand Side Dynamics:

- Gen AI’s capability to simplify user interfaces extends applications into uncharted territories, surpassing the reach of previous technology phases like GUI, the browser, mobile and cloud.

- Projections suggest the emergence of “agents” by year-end that can execute actions for users, akin to a more capable Siri, thus taking the concept of chat interfaces a notch much higher.

- Revolutionizing the Supply Side:

- Gen AI supercharges the software development process, presenting unprecedented rates of innovation and application deployment.

- Hyperscalers, with their expansive array of services, stand to benefit significantly. Their extensive service catalog allows Gen AI to weave together various components seamlessly, advancing platform engineering.

- The Multi-Vendor Stack Potential:

- There’s future potential for Gen AI to accelerate multi-vendor stacks using “generated glue code.” However, this progression requires market consensus on such a stack.

- Market Landscape Analysis:

- Players like Snowflake and Databricks have effectively acted as the AI and data layer on platforms like Amazon and Azure, given these cloud platforms’ underwhelming data and AI capabilities.

- AWS seems shackled by its infrastructural constraints and the nascent stage of its Gen AI development tools.

- Google, in comparison to Azure, boasts superior Gen AI development tools and security. While Microsoft’s Build conference emphasized the embedding of copilots in low code development tools and their Fabric data layer, Google’s implementation of Gen AI as a coding accelerator across all their services is more widespread. The reasons for Google’s lead could be infrastructural advantages or simply being more advanced in their development phase.

Bottom Line: In our view, Gen AI represents a transformative shift in the technological landscape. On both demand and supply sides, it promises to redefine user experience and the software development paradigm. While Google is emerging as a clear leader in this new era, given its advanced tools and widespread implementation, competitors need to innovate rapidly to stay relevant. The dynamic interplay between infrastructure, development tools, and user expectations will determine the next cloud champions.

BigQuery as the Linchpin of Google’s Data Strategy

Google’s strategic emphasis on BigQuery as its primary data platform is evident. This focus is a competitive response to the significant traction Snowflake has gained within AWS and Microsoft platforms. Google Next had less emphasis on database partnerships than, for example, re:Invent, indicating Google’s intent to prioritize its proprietary data platforms over third-party solutions.

On the topic of governance and other data platforms, our research suggests:

- Google’s governance ecosystem is robust. There is a substantial emphasis on data quality, governance, and security. This is supported by a vibrant ISV ecosystem.

- Despite Google’s proprietary advancements, Databricks and Snowflake maintain a modest presence in Google’s ecosystem.

- Databricks’ late integration with GCP, towards the end of the previous year, might be in response to market demand. We see a potential greater strategic partnership opportunity between Databricks and AWS, especially given AWS’s current position in the AI platform layer; and Snowflake with Microsoft given the renewal of Snowflake’s commitment to purchase Azure infrastructure at volume.

Bottom Line: Google is making deliberate efforts to bolster its data stack, emphasizing BigQuery combined with ecosystem governance tools. However, the dynamics with third-party solutions like Databricks and Snowflake could further strengthen existing cloud partnerships and integrations with AWS and Azure.

Drilling into Google’s Data & AI Platform and Strategy

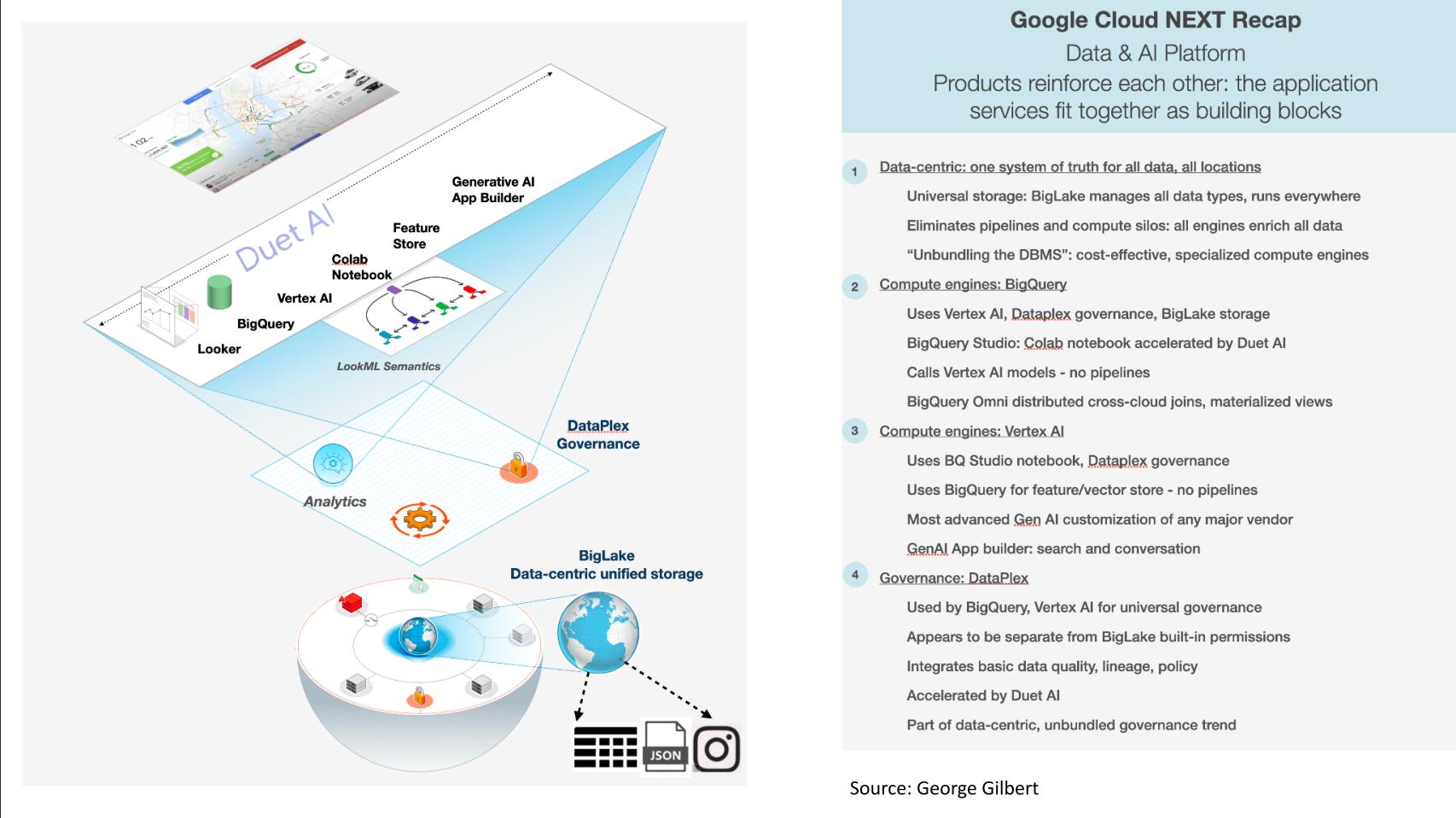

The graphic below represents a form of the Google fly wheel and speaks to how Google’s product portfolio across infrastructure, data and AI reinforce each other. In this next section we examine in more detail, the tools Google showcased at Next such as Vertex AI – the framework – and Duet, the solution-oriented chat capability and how they fit into Google’s broader portfolio.

Key Insights on Google’s Data & AI Platform:

- Shift to Data-Centric Architecture: There’s a transformation towards making data the central point in many platforms. This perhaps signals a move away from DBMS-centric platforms in the AI era. Instead of pipelines, numerous compute engines communicate with a single system of truth.

- Reason: Cost effectiveness. Utilizing one DBMS as a gatekeeper becomes expensive even if it offers transactional integrity.

- Universal Storage – Big Lake: It handles all data forms, structured and unstructured. This is significant because it reduces data silos and pipelines. Multiple engines, including BigQuery, Vertex, and third parties, can access this one system of truth.

- DBMS Shift: There’s a major change in the architecture. DBMS is no longer the gatekeeper, rather its a supporting element. Multiple compute engines now share a single storage engine. There’s a trade-off in transactional integrity, but it provides flexibility and cost efficiency.

- Duet AI and Chatbots: Google introduced Duet AI, a chatbot that seamlessly integrates with various tools, enhancing the user experience. It’s a solution for the general public and experts alike.

- Google’s Messaging: Google aims to portray itself as the platform for the next-gen tech-centric companies. The energy and approach signify they are trying to appeal to younger tech enthusiasts, positioning Amazon and Azure as legacy – AKA the ‘boomer clouds’.

- Looker and BigQuery with Duet: There’s still some ambiguity around whether Looker needs to be on top of BigQuery for the full advantages of Duet.

- Coherency of the Platform: The components of Google’s data and AI platform are tightly integrated. BigQuery and Vertex can interact without data moving through pipelines. This is a capability not yet shown by Amazon or Microsoft.

- Security: A significant emphasis was placed on security at Next, with the integration of Mandiant’s capabilities into Google’s platform, particularly with the rise of AI threats.

- Networking: Google highlighted their cross-cloud networking capabilities, emphasizing the importance of efficient data transfer.

- Google Distributed Cloud: A point that might have been overlooked by many but is significant. AlloyDB Omni’s capability to run disconnected not in the cloud on any docker container instance is a big move towards decentralization and edge support.

- Ecosystem: We also a bigger presence from the GSIs, PWC, Deloitte, Slalom, Cognizant, HTC, Wipro, Infosys, etc. investing heavily in the Google Cloud wave.

Bottom Line: Google is asserting its position in the market with a data-centric approach, integrating AI across its platform. The company’s emphasis on cost-effectiveness, universal storage, and coherent interplay between components shows its commitment to a unified experience. Our research indicates that Google is indeed making a compelling case for its Data and AI platform, differentiating from cloud competitors with a stronger data and AI play in specific areas.

Keep in Touch

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image: Sundry Photography

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.