Last week’s AWS re:Invent underscored the degree to which cloud computing generally and AWS specifically have impacted the technology landscape. From making infrastructure deployment simpler, to accelerating the pace of innovation, to the formation of the world’s most active and vibrant technology ecosystem; it’s clear that AWS has been the number one force for industry change in the last decade. Going forward we see three high level contributors from AWS that will drive the next 10 years of innovation, including: 1) the degree to which data will play a defining role in determining winners and losers; 2) the knowledge assimilation effect of AWS’ cultural processes such as two pizza teams, customer obsession and working backwards; and 3) the rise of superclouds– that is clouds built on top of hyperscale infrastructure that focus not only on IT transformation, but deeper business integration and digital transformation of entire industries.

In this Breaking Analysis we’ll review some of the takeaways from the 10th annual AWS re:Invent conference and focus on how we see the rise of superclouds impacting the future of virtually all industries.

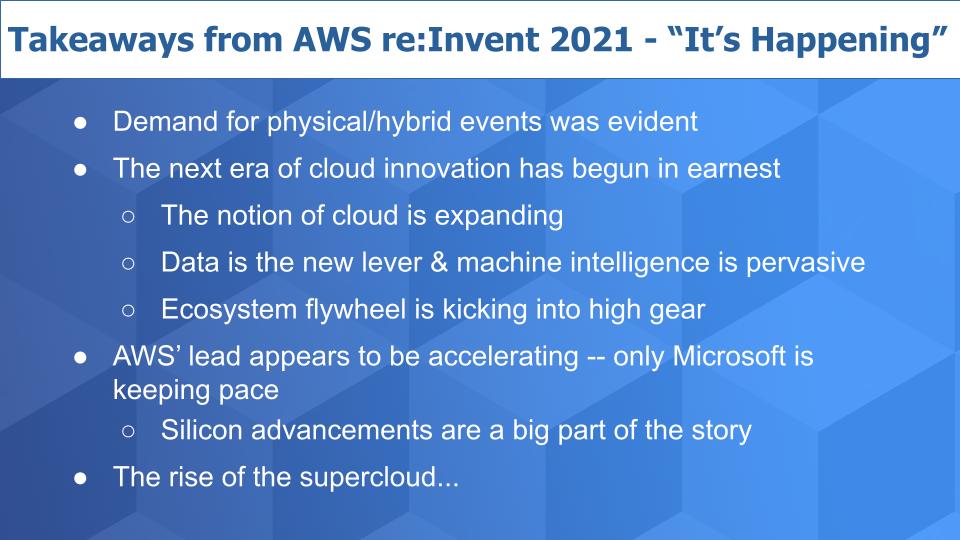

It’s Happening

AWS re:Invent 2021 was the most important hybrid tech event of the year. No one really knew what the crowd would be like but well over 20,000 people came to re:Invent; and probably another 5,000 – 10,000 folks came without badges to have meetings and do networking off then expo floor. So somewhere well north of 25,000 people physically attended the event with another 200,000 plus online. Huge for this year.

One of the most telling moments at re:Invent was a conversation with Steve Mullaney, CEO of networking company Aviatrix. Just before we went on theCUBE, Nick Sturiale, one of Aviatrix’ VCs looked at Steve and said – “It’s Happening…”

What Sturiale meant by ‘it’s happening’ is that the next era of cloud innovation is here and is beginning in earnest. The cloud is expanding out to the edge – AWS is bringing its operating model, APIs, primitives and services to more and more locations. And companies like Aviatrix, and many others, are building capabilities on top of the cloud that don’t exist from the cloud providers today. And their strategy is to move fast in their respective domains to stay ahead and add value.

Yes, data and machine learning are critical – we talk about that all the time but the ecosystem flywheel was so evident at this year’s re:Invent. Partners were charged up – there wasn’t nearly as much chatter about AWS competing with them…rather there was much more excitement around the value these partners are creating on top of AWS’ massive platform.

Despite aggressive marketing from competitive hyperscalers, other cloud providers and as-a-service on-prem / hybrid offerings, AWS’ lead appears to be accelerating. A notable example is AWS’ efforts around custom silicon. Far more companies, especially ISVs are tapping into AWS’ silicon advancements. We saw the announcement of Graviton3 and new chips for training and inference. As we’ve reported extensively, AWS is on a curve that will outpace x86 vis a vis performance, price/performance, cost, power consumption and speed of innovation. And its Nitro platform is giving AWS and its partners the greatest degree of optionality in the industry – from CPUs, GPUs, Intel, AMD, Nvidia and very importantly, Arm-based custom silicon springing from AWS’ acquisition of Annapurna.

AWS started its custom silicon journey in 2008 and has invested massive resources into this effort. Other hypersalers, which have the scale economics to justify such efforts, are just recently announcing initiatives in this regard. Others who don’t have the scale will be relying on third party silicon providers– a perfectly reasonable strategy. But because AWS has control of the entire software and hardware stack, we believe it has a strategic advantage in this respect. Silicon especially is a domain where – to quote Andy Jassy – there is no compression algorithm for experience. Being on the curve matters. A lot.

[Listen to AWS’ Dave Brown talk about the company’s custom silicon journey].

And the biggest trend in our view this past week was the clear emergence of superclouds.

Rise of the Supercloud

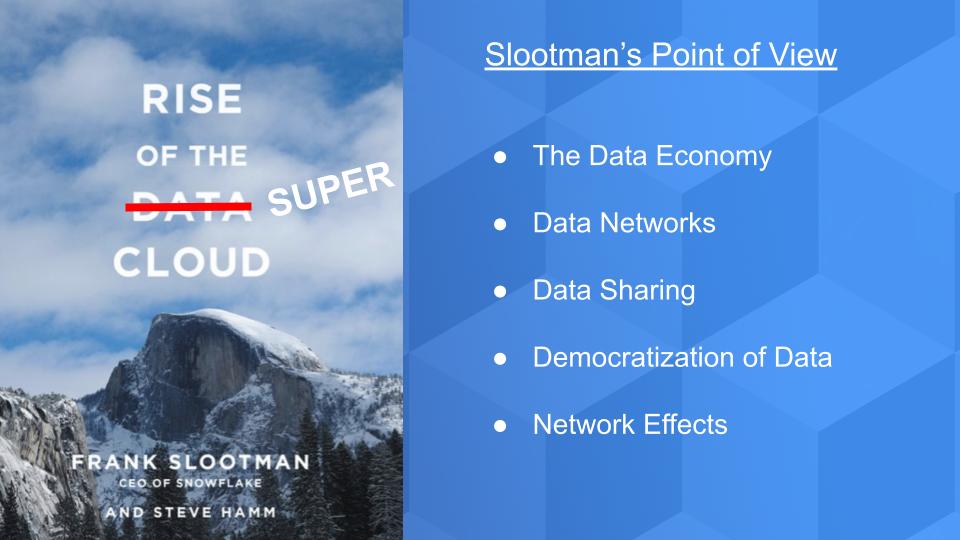

In his 2020 book with Steve Hamm, Frank Slootman laid out the premise for the emergence of data cloud, a title which we’ve conveniently stolen for this Breaking Analysis. Rise of the Supercloud – thank you Frank Slootman. In his book, Slootman made a case for companies to put data at the center of their organizations– rather than organizing just around people, for example. The idea is to create data networks. While people are of course critical, organizing around data and enabling people to access and share data will lead to the democratization of data and network effects will kick in– kicking off a renaissance in business productivity.

Essentially this is Metcalfe’s Law for data. Bob Metcalfe, inventor of Ethernet, put forth the premise when we both worked for Pat McGovern at IDG. It states that the value of a network is proportional to the square of the number of its users on the network. Thought of another way – the first connection isn’t so valuable but the billionth is really valuable.

Slootman’s Law – if you will – says the more people that have access to the data (governed of course) and the more data connections that can be shared, the more value will be realized from that data. Exponential value in fact.

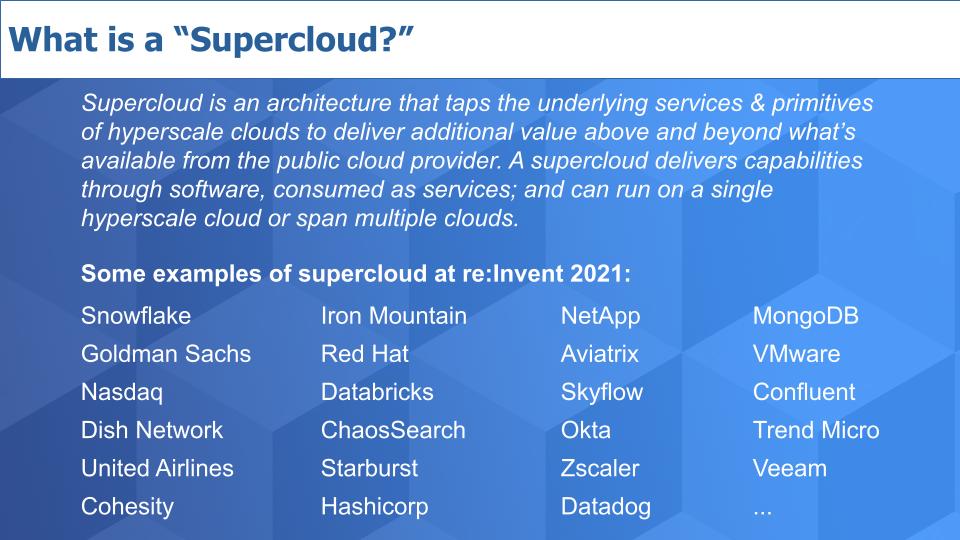

What is a Supercloud?

Supercloud is a term we first referenced in the post led by John Furrier prior to re:Invent. Supercloud describes an architecture, which taps the underlying services & primitives of hyperscale clouds to deliver additional value above and beyond what’s available from public cloud providers. A supercloud delivers capabilities through software, consumed as services; and can run on a single hyperscale cloud or span multiple clouds.

In fact, to the degree that a supercloud can span multiple clouds — and on premises workloads — and hide the underlying complexity of the infrastructure supporting this work, the more adoption and value will be realized.

We’ve listed some examples above of what we consider to be superclouds in the making. Snowflake is one of our favorite to cite and we use it frequently. Snowflake is building a data cloud that spans multiple clouds and supports distributed data, but governs that data centrally– somewhat consistent with the data mesh approach.

[Listen to how Snowflake’s co-founder, Benoit Dageville, thinks about data mesh.]

Goldman Sachs announced at re:Invent this year a new data management cloud — the “Goldman Sachs Financial Cloud for Data with AWS.” We’ll come back to that later in more detail but it’s a prime example of an industry supercloud.

Nasdaq CEO Adena Friedman spoke at the day 1 keynote and talked about the supercloud they’re building. Dish Networks is building a supercloud to power 5G wireless networks. United Airlines is, at this time, focused on porting applications to AWS as part of its digital transformation, but eventually we predict it will start building out a supercloud travel platform. What was most significant about the United effort is the best practices they’re borrowing from AWS like small teams and moving fast. AWS is teaching customers how to build a culture to support the buildout of superclouds.

But many others that we’ve listed above are on a supercloud journey. Just some of the folks we talked to at re:Invent that are building clouds on top of clouds are shown. Cohesity building out a data management supercloud focused on data protection and governance. Hashicorp announced its IPO at a $13B valuation– building an IT automation supercloud. Databricks, ChaosSearch, Zscaler, which is building a security supercloud, and many others that we spoke with at the event.

Castles in the Cloud

We want to take a moment to talk about “Castles in the Cloud.” It’s a premise put forth by Jerry Chen and the team at Greylock. It’s a really important piece of work that is building out a dataset and categorizing the various cloud services to better understand where the cloud giants are investing, where startups can participate. How companies can play in the castles built by the hyperscalers…how they can cross the moats that have been built and where the innovation opportunities exist.

Superclouds are strong examples of companies leveraging the castles and crossing the moats built by hyperscalers.

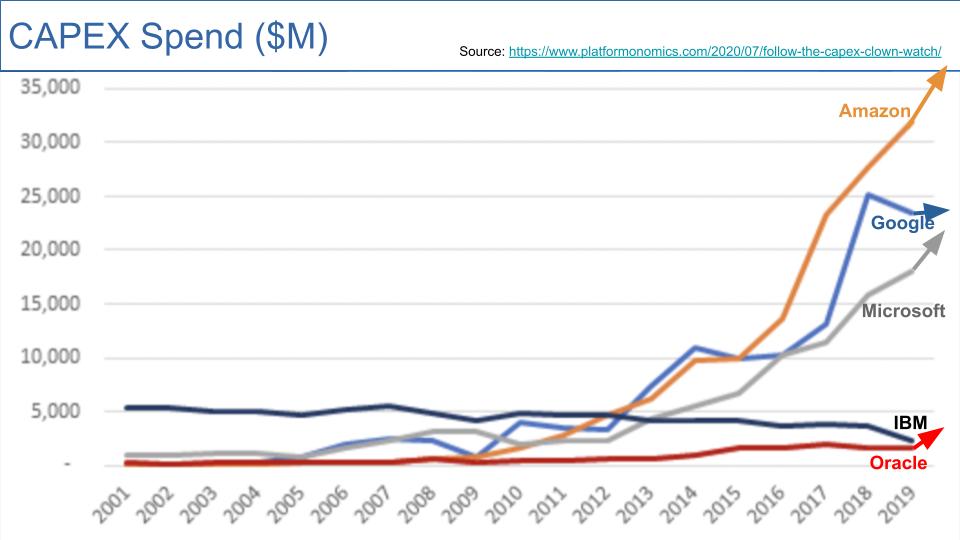

Only Four Players Have Built Hyperscale Castles

Frequently, we’re challenged about our statements that there are only four hyperscalers – AWS, Microsoft, Google and Alibaba. While we recognize that certain companies, Oracle in particular, have done a good job of improving and building out their clouds, we don’t consider companies like IBM and other smaller managed service providers as hyperscalers. And one of the main data points we use to defend our thinking is CAPEX investment. There are many other KPIs like size of ecosystem, partner acceleration and enablement, feature sets, etc. but CAPEX investment is a big factor in our thinking.

Above is a chart from Platformonomics – a firm that’s obsessed with CAPEX – showing annual CAPEX spend for five cloud companies – Amazon, Google, Microsoft, IBM and Oracle. This data runs through 2019 and we’ve superimposed the direction each company is headed. Amazon spent more than $40B on CAPEX in 2020 and will spend more than $50B this year. Sure there are warehouses and other capital expenses in those numbers but the vast majority is spent on building out its cloud infrastructure. Same with Google and Microsoft. Oracle is at least increasing its CAPEX spend to $4B…but it’s de minimis compared to the cloud giants. IBM is headed in the other direction – choosing to invest $34B in acquiring Red Hat instead of putting its capital into cloud infrastructure. A reasonable strategy but it underscores the gap and to us strongly supports the premise.

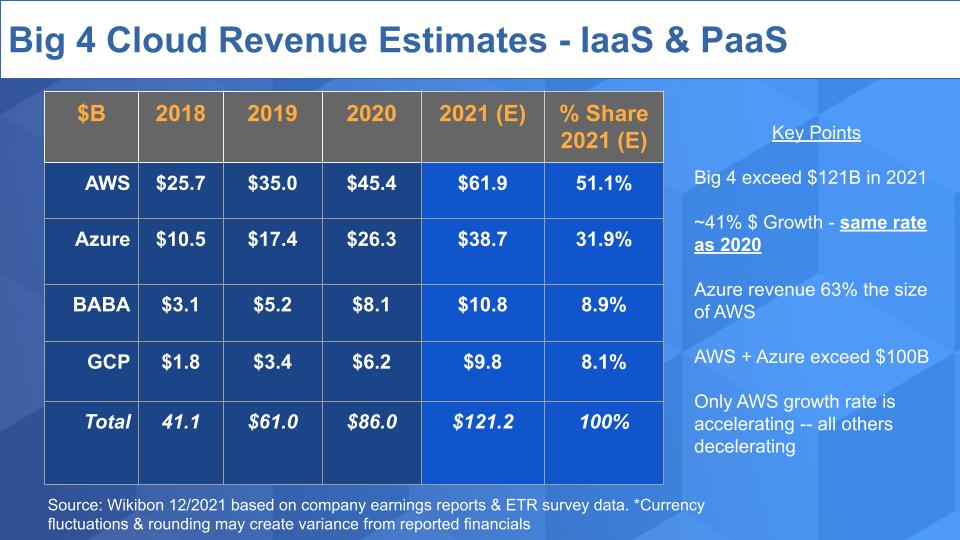

IaaS Revenue as an Indicator

Another key metric we track is IaaS revenue.

Above is an updated chart from the one we showed last month, which at the time excluded Alibaba’s most recent quarter. The change was not material but the four hyperscalers, which invested more than $100B in CAPEX last year, will together generate more than $120B in revenue this year. And they’re growing at 41% collectively. That is remarkable for such a large base of revenue. And for AWS the rate of revenue growth is accelerating.

The point is, if you’re going to build a supercloud, why wouldn’t you start by building on top of these platforms (notwithstanding concerns about China with respect to Alibaba)?

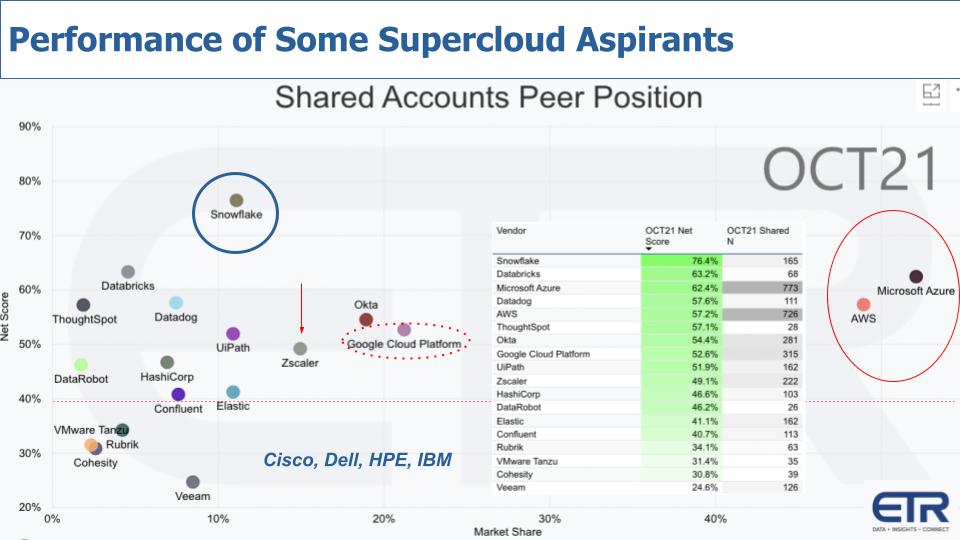

How Some Early Superclouds are Performing

Supercloud is not a category within the ETR taxonomy. But we can evaluate some of the companies we’ve been following that we see as building superclouds by looking at ETR survey data. The chart above plots Net Score or spending momentum on the vertical axis and Market Share or presence in the ETR data set on the horizontal axis. Most every name on the chart is building a supercloud of some sorts.

Let’s start by calling out AWS and Azure. They stand alone as the cloud leaders. You can debate what’s included in Azure and our previous chart on revenue attempts to strip out the Microsoft SaaS business but this is a customer view. Customers see Microsoft as a cloud leader – which it is – so that’s why it’s presence is larger than AWS even though its IaaS revenue is significantly smaller. But they both have strong momentum on the vertical axis as shown by that red horizontal line. Remember, anything above that is considered elevated.

Google cloud, as you see, is well behind those two leaders.

Snowflake’s Data Cloud as Supercloud

Look at Snowflake. We realize we repeat this often but Snowflake continues to hold a Net Score in the mid-to-high 70’s and, at 165 mentions – which you can see in the inserted table – continues to expand its market presence.

Of all the technology companies we track, we feel Snowflake’s vision and execution on its data cloud strategy is the most prominent example of a supercloud. Truly, every tech company should be paying attention to Snowflake’s moves and carving out unique value propositions for their customers by standing on the shoulders of cloud giants (as ChaosSerach CEO Ed Walsh likes to say as his company contemplates its supercloud buildout).

On-prem Dependency Creates a Wide Range of Supercloud Maturity

In general, the more cloud native the firm’s offering, the further along they’ll be toward building a supercloud. And the greater the momentum. But typically these firms are coming from a smaller installed base and have foreclosed on the on-premises opportunity (for now).

On the left hand side of the chart above, you can see a number of companies we spoke with that are in various stages of building out their superclouds. Databricks, Thoughspot, DataRobot, Zscaler, HashiCorp, Elastic, Confluent – all above the 40% line. And somewhat below that line but still respectable, are those with a significant on-prem presence – VMware with Tanzu, Cohesity, Rubrik and Veeam. And many others that we didn’t necessarily talk to at re:Invent and/or they don’t show up in the ETR data set.

Cisco, Dell, HPE & IBM

We’ve called out Cisco, Dell, HPE and IBM on the chart because they all have large on-premises installed bases and different points of view. To varying degrees they are each building superclouds. But to be frank, these large companies are first protecting their respective on-prem turf. You can’t blame them. They are all adding as-a-service offerings, which is cloud-like. They will rightly fight hard and compete on their respective portfolios, channels and vastly improved simplicity. But when speaking to customers at re:Invent – and these are not just startups we talk to…we’re talking about customers of enterprise tech companies like these – the customers want to build on AWS. They will fully admit they can’t or won’t move everything out of their data centers but the vast majority of customers we spoke with have much more momentum around moving toward AWS.

Yes, of course there’s some recency bias because we just got back from re:Invent and it’s a conference full of Amazon customers, but the pace of play, the business savvy and the transformative mindset of these customers is obvious. And the numbers we shared earlier simply don’t lie. These customers are among the firms consuming technology and transforming their business at the most rapid pace.

Regarding these four players, they are starting to move in the supercloud direction — but they are late to the party. Nonetheless, a big strategic advantage is they have more credibility around multi-cloud than the hyperscalers. But on balance, AWS’ overall lead is accelerating in our opinion, the gap imo is not closing.

A New Breed of Tech Companies is Emerging

In and around 2010 and 2011 we collaborated with two individuals who shaped our thinking in the big data space. Peter Goldmacher at the time was a sell side analyst at Cowan and Abhi Mehta was with BofA, transforming the bank’s data operations. Peter said at the time that it was the buyers of big data technologies – and those that applied it to their operations who would create the most value. He posited that they would create far more value than Cloudera or Hortonworks, for example, and a collection of other big data players. Clearly he was right.

Abhi Mehta was a shining example of that premise and he posited on theCUBE that ecosystems would evolve within vertical industries around data. And the confluence of data and technology and machine intelligence would power the next generation of value creation.

Fast forward and apply this thinking to 2021….

Superclouds Form Around Industries & Data

Just after the first re:Invent, we published a post on Wikibon about the making of a new Gorilla – AWS. And we said the way to compete would be to take an industry focus and become best-of-breed within your industry. We aligned with Abhi Mehta’s view that industry ecosystems would evolve around data and offer opportunities for non-hyperscalers to add value. What we didn’t predict at the time – but are seeing clearly emerge – is that these superclouds will be built on top of AWS and other clouds.

Goldman’s Financial Cloud for data is taking a page out of Amazon’s retail business. Pointing its proprietary data, algorithms, tools and processes at its clients and making these assets available as a service on top of the AWS cloud. A supercloud for financial services. They are relying on AWS for infrastructure, compute, storage, networking, security, and services around machine learning to power their supercloud.

Nasdaq and Dish are similarly bringing forth their unique value. As we said earlier, United Airlines will in our view eventually evolve from migrating its apps to the cloud to building out a supercloud for travel.

This trend is taking shape in virtually every industry and geography and will establish a new breed of disruptive winners. Incumbents that move fast and capitalize on this trend will thrive in our view.

What about your logo? What is your supercloud strategy? We’re sure you’ve been thinking about it. Or perhaps you’re already well down the road. We’d love to hear how you’re doing it and if you see the trends the same or differently as we do.

Keep in Touch

Remember we publish each week on this site and siliconangle.com. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon/SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.