Snowflake’s IPO has eyes popping and the industry buzzing. We’ve had several dozen inbound PR from firms trying to hook us, offering perspectives on the Snowflake IPO so they can pitch us on their product. People are pumped up…and why not? An event like this doesn’t happen that often.

In week’s Wikibon CUBE Insights, Powered by ETR, we’ll give you our take on the Snowflake IPO and address the many questions we’ve been getting on the topic. We’ll also try to address what happens now.

The Hottest IPO in Software History – What Now?

First we want to congratulate the many people at Snowflake. The big hitters are all in the news: Slootman, Muglia, Speiser, Buffet, Benioff, Scarpelli. Interestingly you don’t hear much about the founders. Very humble. We’ll talk about them in future episodes. They created Snowflake. They had the vision and the smarts to bring in operators that could get to this point. So awesome for them. But we’re especially happy for the rank and file and many Snowflake employees where an event like this can be life changing. Fantastic for you.

Let’s get into the madness. As you know by now Snowflake IPO’d at a price of $120. Unless you knew a guy, you paid around $245 at the open…that’s if you got in. Otherwise, if you bought at a higher price. You just held your nose and made the trade.

Snowflake’s value went from $33B to more than $80B in a matter of minutes.

Now there’s a lot of talk and finger pointing that this issue was underpriced and Snowflake left $4B on the table. That’s just crazy talk to us. Snowflake’s balance sheet is in good shape thanks to this offering and we’re not sure jamming later stage investors even more would have been the right thing to do. This was a small float so you would expect a sharp uptick on day 1. We had predicted a doubling to a $66B valuation and it ended the day at around $70B.

The big question now: Is this a fair valuation? And can Snowflake grow into its valuation. We’ll address this in more detail but the short answer is, yes, Snowflake is overvalued right now in our view, but can grow into it’s valuation. But of course there will be challenges.

The other comment we get is “but the company is losing tons of money.” Yes. That’s is correct. But we’d point out that is a symptom of the street’s valuation. We’ve been saying for years that investors reward growth right now because they understand that to compete in software you need massive scale. So we’re not worried in the least about Snowflake’s bottom line at this point. Eventually we will pay closer attention to operating cash flow but right now we want to see Snowflake grow into its valuation.

The other common question is should I buy? When should I buy? What are the risks? And can Snowflake compete with the biggest cloud vendors?

We’ll say this before we get into it. As we’ve said many times, it’s very rare that you won’t get better buying opportunities than day 1 of an IPO. And we think you will here too. Back in 2015, in the first calendar quarter of the year, ServiceNow missed its earnings and the stock got hit. We had the opportunity to interview Frank Slootman right after that and it’s instructive to hear what he said:

Subsequently, we saw that stock drop to as low as $50 and today it’s a $450 stock so the point is that Snowflake, like ServiceNow will be priced to perfection and there will be bumps in the road. Possibly macro factors or other. And if you’re a believer you’ll have opportunities to get in. So be patient. Don’t let FOMO guide your investment decisions, rather let your research inform your strategy.

For context, the weighted average price that insiders paid for Snowflake came out to around $5-$6. So on day 1 of the IPO the insiders made a an average of 50X return on their investment. If you bought on day 1 you even or maybe losing money. But there are some ground floor opportunities that exist, which may be risky. But if you’re young and motivated or older and have some time to research you may be interested in what we have to say later on in this post.

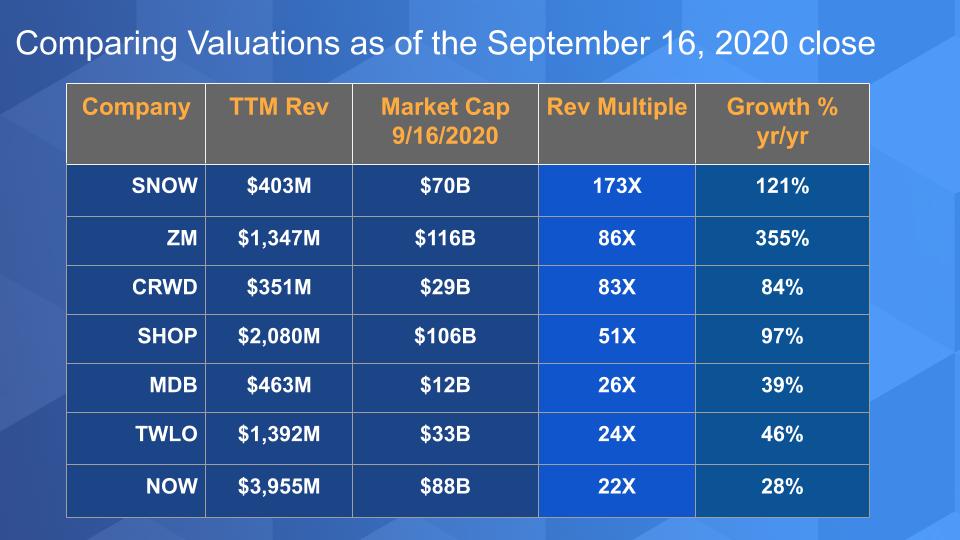

Comparing Snowflake to other High Fliers

This chart shows some other hot companies as compared to Snowflake. We show the company, the trailing twelve month revenue, market cap at the close of September 16th, day 1 of Snowflake’s IPO. Then we calculate and sort the data on the revenue multiple from the TTM. And the last column is the year on year growth rate from the latest quarterly report. We use TTM because it’s simple and easy to understand. And it makes the revenue multiple bigger so it’s more dramatic. Many prefer to use forward revenue based on consensus projections but that’s why the growth rate is there – you can pick your projected growth rate and do the revenue projection yourself.

So let’s start with Snowflake. $400M+ in TTM revenue and that’s based on a newish pricing model of consumption, not a SaaS subscription for a year or two. We love this model and have talked about it so we won’t dwell on it here. But you can see the TTM revenue multiple is massive and the growth rate of 120% – very impressive.

We put Zoom in the chart because the growth rate is so tremendous. Who knows how that correlates to the revenue multiple – but as you can see, Snowflake tops the frothiness of even Zoom. Maybe Zoom is undervalued? Hard to fathom.

We think Crowdstrike is an interesting compare and is a company that we’ve been following closely. In our last security update Crowdstrike had a 65X TTM revenue multiple and you see how that’s jumped since they reported and beat expectations. But similar size as Snowflake with a slower growth rate and lower revenue multiple. So there is some correlation to growth. The higher the growth rate, the higher the revenue multiple, Zoom notwithstanding.

Now Snowflake pulled back on day 2 of its trading and it was down again early Friday as you would expect with both the market being off and profit taking but it ended up for the day. If you got an allocation at $120, why not take some profits and play with house money? That Snowflake came back after being off suggests there’s still pent up demand for the stock. Again the small float will have that effect. Snowflake’s value right now is hovering at $67.4B, $1.4B higher than our projection for day 1.

If you project 100% TTM growth for next year and the stock trades in a reasonable range – which it very well could – you could see Snowflake coming down to Crowdstrike-like revenue multiples in twelve months. It will depend on Snowflake’s earnings reports, which will likely hit or beat estimates for the next several quarters…and if it’s growing faster than these others it should command a relative premium. The absolute value will of course depends on where the market prices all these companies in a year.

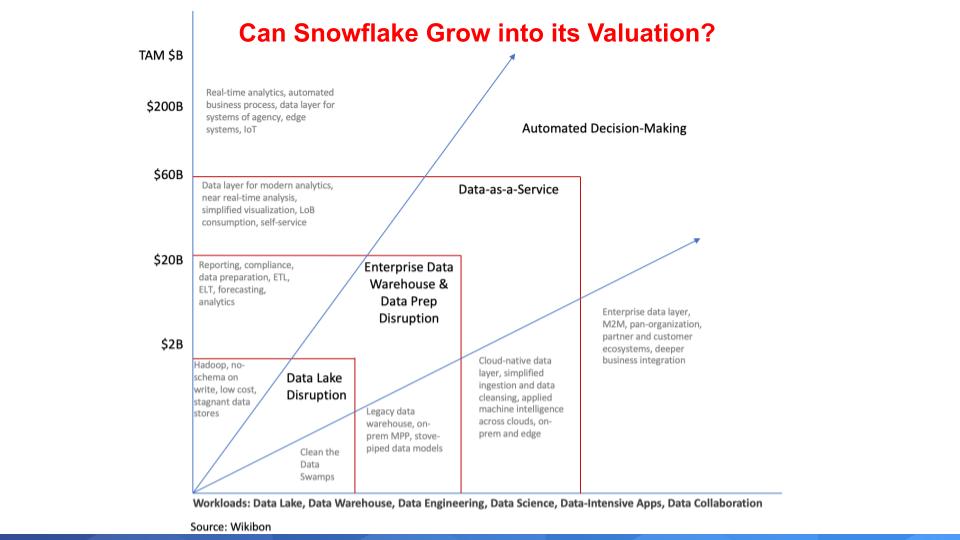

Can Snowflake Grow into its Elevated Valuation?

We shared the chart below with you in one of our earlier segments on Snowflake. And it talks to Snowflake’s TAM expansion opportunity. This is something we saw Slootman execute at ServiceNow when everyone underestimated its value. And we’ll briefly explain here.

Snowflake is disrupting the traditional data lake and enterprise data warehouse (EDW) markets (layers 1 and 2 above). Data lake spending is relatively small – under $2B. But data lakes are inexpensive. We often joked that the ROI of Hadoop stood for “Reduction of Investment.” While data lakes were less expensive, they never materialized as a full data warehouse replacement. The EDW market however is quite large.

Traditional enterprise data warehouses are big, slow, cumbersome, expensive and complicated. But they’ve been operationalized and are critical for companies’ reporting requirements and basic analytics. But they’ve failed to live up to their promise of 360 degrees of view of customers and real time analytics. One customer told us “my data warehouse is like a snake swallowing a basketball.” He gave an example where a change in regulation would occur and force a change in the data model and they would have to ingest all this new data and the warehouse choked. And so every time Intel came out with a new processor they would rush out to throw more compute at the problem. He called it “chasing the chips.” This is symptomatic of the cumbersome nature of traditional EDWs that Snowflake is disrupting.

My data warehouse is like a snake swallowing a basketball…

What Snowflake did was to envision a cloud-native world where you could bring compute to massive data volumes on an elastic basis and only pay for what you use. Sounds so simple but technically, Snowflake’s founders’ innovation of separating compute from storage to leverage the flexibility of the cloud was profound. And clearly was the right call. We’ll come back to this in a bit.

Where we think Snowflake is going is to build a data cloud (layer 3 above). Where your data can be ingested and accessed to perform near real-time analytics with machine learning and AI. And Snowflake’s advantage as we’ve discussed is of course its simplicity, but also the fact that it runs on any cloud and can ingest data from a variety of sources. Now there are some challenges here and we are not saying that Snowflake is going to participate in all use cases – however with its resources we expect Snowflake to create new capabilities and do tuck in acquisitions that will allow it to attack many more use cases.

And so you look at this chart above, and if the third layer is a $60B market, it means Snowflake needs to extend into the fourth layer which we call automated decision making– because it’s unlikely to secure 100% of the opportunity. Layer 4 is where real time analytics and systems are making decisions for humans and acting in real time. Clearly data will be a critical part of this equation. At this point it’s unclear that Snowflake has the capability to go after this space as much of the data in this area will live at the edge. But Snowflake is betting on its becoming a data layer across clouds and presumably at the edge and this market is enormous. So there’s no lack of TAM in our view for Snowflake.

Which Brings us to the Competition – Can Snowflake Continue to Win?

Much of the investment thesis behind Snowflake is Slootman and his army, including CFO Mike Scarpelli and what they did at ServiceNow is an indicator of what will happen with Snowflake. Scarpelli is an operational guru and keeps the engine running with very tight controls. They both are well respected by Wall Street, customers and employees. So betting on management is a pretty good bet. That said Snowflake’s competition is much more capable than what ServiceNow faced in its early days.

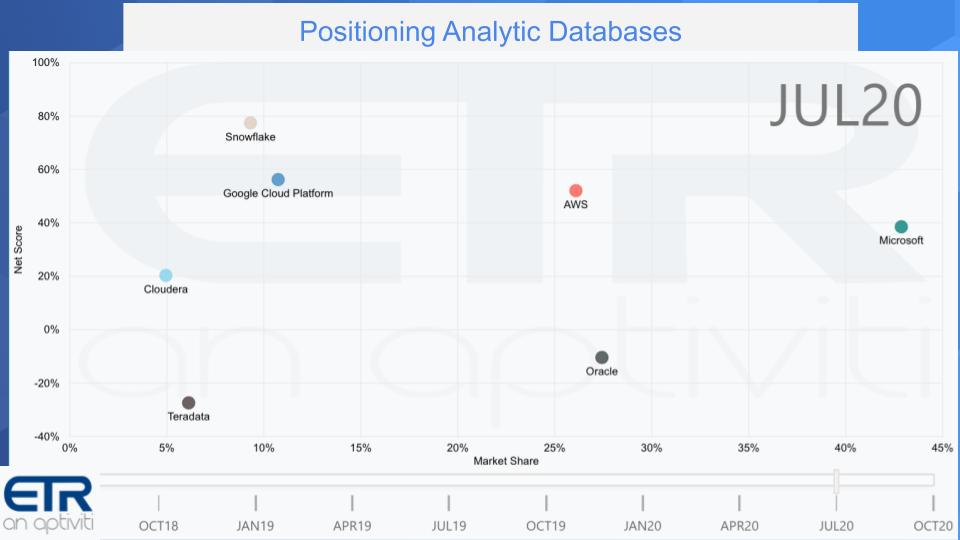

Here’s a picture of some of the key competitors. On the vertical axis is Net Score or spending velocity based on ETRs quarterly surveys. We’re showing July’s survey results – October is currently in the field. On the horizontal axis is Market Share or pervasiveness in the data set. So it’s a proxy for share but it’s based on mentions not dollars. And that’s why Microsoft is so far to the right because they’re huge and everywhere.

The more relevant data to us is the position of Snowflake. It remains one of the highest Net Scores in the entire survey base – not just database. AWS is its biggest competitor because most of Snowflake’s business runs on AWS. But Google BigQuery is technically the most capable because it’s a true cloud native database built from the ground up, whereas AWS took a database that was built for on-prem and brilliantly made it work in the cloud by re-architecting many pieces. But it still has certain legacy parts to it.

Oracle is huge and slow growth overall. And is making investments to hold on to its customers. Oracle is all about a single database for multiple use cases. Oracle’s R&D focuses on making Oracle Database the best database for mission critical workloads, while at the same time adding things like JSON to support document workloads. As well as analytics.

And you can see Teradata and Cloudera on the chart. Cloudera is a proxy for the data lakes which are lower cost platforms. And Cloudera which acquired Hortonworks is credited with the commercialization of the whole big data movement. And then Teradata as well which has been around since the 1980’s with a large base of customers.

There are a zillion other database players but these are the ones we wanted to focus on today. The bottom line is we expect Snowflake’s vertical axis spending momentum (Net Score) to remain elevated and it will continue to steadily move to the right.

Let’s Drill into the Snowflake Data a Bit More

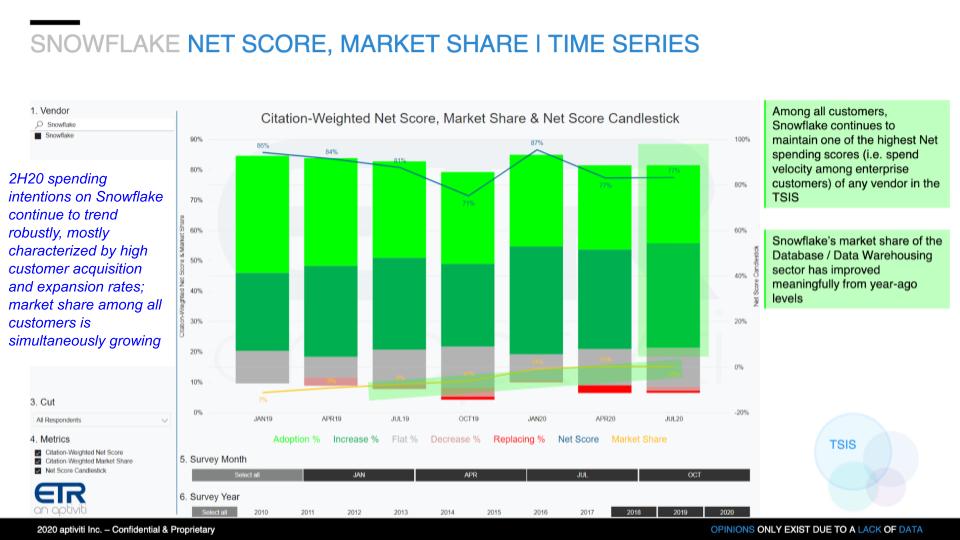

Below we show the components of Net Score for Snowflake over time. Remember, lime green is new adoptions, forrest green is spending up more than 6%, gray is flat spending, pink is spending 6% less and bright red is leaving the platform. The line up top is Net Score, which subtracts the red from the green, and is an indicator of spending velocity. The yellow line at the bottom is Market Share or pervasiveness in the survey.

Note the blue – is ETR’s top takeaway:

2H20 spending intentions on Snowflake continue to trend robustly, mostly characterized by high customer acquisition and expansion rates; market share among all customers is simultaneously growing. -ETR’s Top Snowflake Takeaway

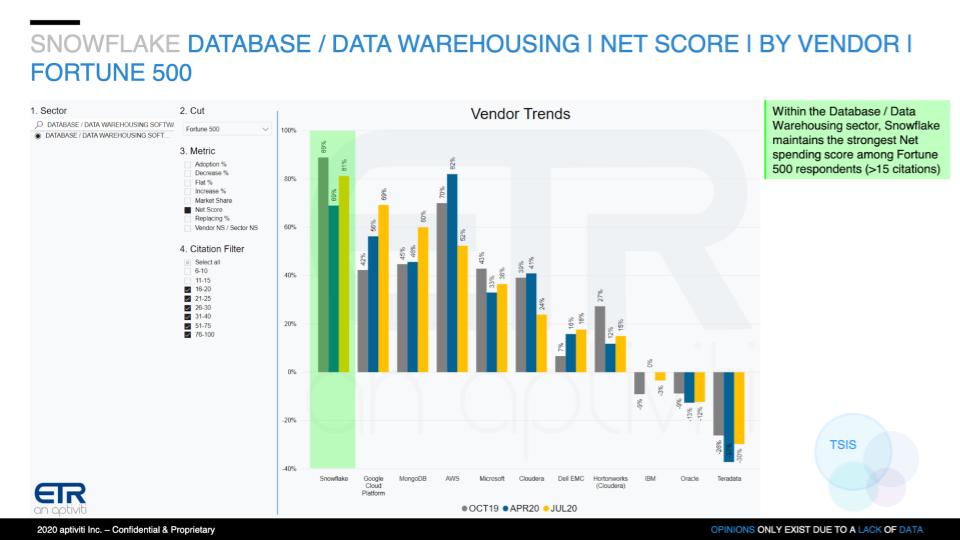

Snowflake Against the Competition in Fortune 500 Accounts

Below we show Net Score or spending momentum over time for some key competitors. And you can see Snowflake’s Net score has actually increased since the April survey, which was taken at the height of the U.S. lockdown. And its Net Score is actually higher in the Fortune 500 than it is overall, which is a proxy for spend, because bigger accounts tend to have higher average spend levels. Google, MongoDB & Microsoft also show meaningful momentum growth since the April survey. Notably, AWS has come off its elevated levels from last October and April. Still strong but something to watch.

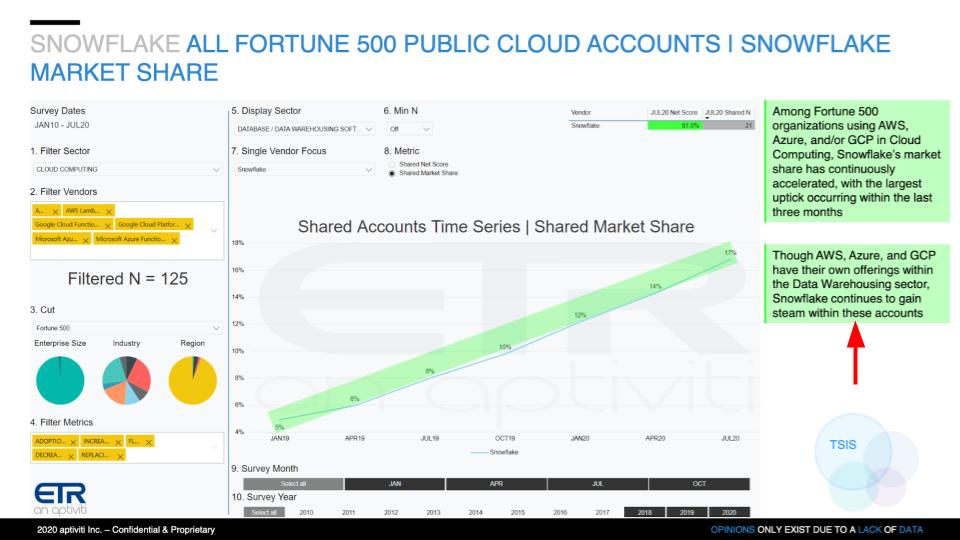

Snowflake’s Market Presence within Big 3 Cloud Accounts

Below is another cut on the Fortune 500 data but this time we show Market Share within Amazon, Google and Azure cloud accounts. You can see there are 125 respondents within the Big 3 clouds and 21 Snowflake respondents within that base of 125. And you see the steady and consistent growth of its share. Not huge Ns but enough to give some confidence in the data. Note the ETR call out that this trend is occurring despite the fact that each of the Big 3 cloud vendors has its own competitive offering.

But this is not a Layup for Snowflake

As we’ve said before, not ServiceNow part 2 – it’s a different situation.

The competition here is not BMC, which was ServiceNow’s target. As much as we love our friends at at BMC, we’re talking about AWS, Microsoft and Google. Amazon with RedShift is dialed into this. We’ve said often that AWS has borrowed many Snowflake innovations and last fall at re:Invent we heard them make a big deal about separating compute from storage. Andy Jassy took a swipe at Snowflake without mentioning them, specifically. But let’s listen to what he said and come back to discuss the nuances:

Ok so first of all – Jassy is awesome. He stands up at re:Invent for 2+ hours and connects trends and business to technology and he has a deep understanding of the tech, amazing. We are in awe of his presentation skills and knowledge.

However, we have to call attention to his statements here. Our interpretation of what AWS has done to separate compute and storage is good but it’s not as elegant architecturally as Snowflake. AWS essentially has tiered the colder storage off the cluster to lower the overall cost by placing it on cheaper S3 storage. And it uses high speed pipes to move it back to the compute when necessary. But our understanding is you can’t turn off the compute completely. You still need to store the “hot” data on the compute nodes. Yes it lowers costs for customers, which is goodness. But with Snowflake they’ve truly separated compute and storage. And the issue RedShift faces is, we believe it had to do a workaround because it’s essentially built on an architecture that was not designed as cloud native from the ground up.

So when Jassy talks about moving the data to the compute – what he’s really saying is our architecture is such that we had to do this clever workaround. But his whole narrative about the prevailing ways to separate compute and storage (by prevailing we believe he’s talking about Snowflake) and moving the datas [sic] to the compute, we feel, doesn’t completely apply to Snowflake. Because Snowflake, we believe, uses a metadata architecture that is purpose-built for its workloads. And Snowflake can more efficiently minimize data movement and where possible bring the compute to the data. Thank you Hadoop for that profound concept. We are confirming this is the case but that’s our current thinking on the issue.

Does this Mean Snowflake will have Cakewalk over RedShift & Others?

No. Not at all. AWS will continue to innovate. What matters in the end is customer outcomes and many customers are hopping on RA3 instances so Snowflake had better keep moving fast– multi cloud, new workloads, TAM expansion to adjacent markets, etc.

Microsoft is huge but as usual there’s not much to say other than they are everywhere. They put out 1.0 products that eventually they get right and because of their heft they get mulligans that they turn into pars or birdies. But we think Snowflake will bring some innovations to Azure that will get good traction.

Now Google BigQuery is interesting. By all accounts it gets high technical marks. Google is playing the long game and we would expect that Snowflake will have a harder time competing in Google Cloud than in AWS. But we’ll see.

Database Workload Convergence. The penultimate point on the above slide is many are talking about the convergence of analytic, operational and transaction databases. And the thinking is this doesn’t necessarily bode well for a specialist like Snowflake. We would make a couple points here:

- One is that while it’s definitely true, you’re not seeing Snowflake positioned today as responding at the point of transaction to influence an order in real time, for example. And this may have implications at the edge. But we have learned there are many ways to skin a cat and we see integration layers and innovative approaches emerging in the cloud that could address this gap and present opportunities for Snowflake.

- The other thing we’d say is maybe that thinking misses something altogether where this idea of Snowflake in that third data layer we showed, data-as-a-service or the data cloud, which is maybe a giant opportunity that they are uniquely positioned to address because they are cloud agnostic, have the technology and the vision.

Nonetheless, the final point is we will see the battle continue between integrated suites and best of breed players. We talk about it all the time and there is no one single answer.

How can the Little Guy get an Insider’s Return?

Let’s take a tangent here and talk about this. Now we have to caution you – and this is a bit tongue in cheek – but this is buyer beware. But as we wrote earlier, the insiders on Snowflake had a 50X return on day 1. You probably didn’t.

We want to talk about the confluence of software engineering, cryptography and game theory…powered by the underlying appeal of blockchain technology.

And we’re talking about innovations around a new Internet. And a distributed Web or dWeb where many distributed computers come together to form one computer that guarantees trust between two or more users for a variety of use cases. Not just a financial store like Bitcoin…but that too. And the motivation behind this is the fact that 5-6 companies today control the Internet and have essentially taken control of the major protocols like TCP/IP, HTTP, SMTP, etc. These are the protocols on which the Internet was built. And you had no way to invest in them until Cisco, Google, Amazon, Facebook and some others went public.

The people we’re showing below are working on new innovations. Essentially building out a new Internet. Olaf Carlson-Wee started Polychain Capital to invest in core infrastructure around these new computing paradigms. And Mark Nadal is someone who is working on new dApps as is Tim Berners-Lee with his Solid project at MIT, emphasizing data ownership and privacy. Of course Satoshi got it all started when she invented Bitcoin and created the notion of fractional shares. And the folks at Andreesen Horowitz are actively making bets in the space.

Here’s the premise. If you’re a little guy and wanted to invest in Snowflake – you couldn’t until late in the game. If you wanted to invest in the LAMP stack directly in the late 90’s there was no way to do that. You had to wait for Red Hat to go public to get a piece of the Linux action. But in this world there are opportunities that are not mainstream and often based on cryptocurrencies.

Again – it’s dangerous – there are scams and losers but if you do your homework there are actually vehicles for you to get in on the ground floor of some of these new innovations and you could get a 50 or 100 bagger too. But you have to do your research and there’s no guarantee that these innovations will be able to take on the Internet giants.

But the point is that there are people – really smart technologists and software engineers – that are young, mission driven and are forming a collective voice against what they see as a dystopian future. Because they want to level the Internet playing field. And this may be a disruptive force to challenge the Internet giants. And if you’re game we would take a look at the space and see if it’s worth a small investment.

Ok a little off Snowflake but we wanted to put that out there.

Snowflake…Wow!

The issue closes its first trading week as a company worth $66B. Roughly the same value as Goldman Sachs. Worth more than VMware. The list goes on. As Slootman will no doubt stress to his troops, this is the beginning, not the end.

There’s not much more can we say other than we’re excited to watch what unfolds and report what we see and believe.

And…

Remember these episodes are all available as podcasts – please subscribe. We publish weekly on Wikibon.com and Siliconangle so check that out and please do comment on the LinkedIn posts we publish. Don’t forget to check out ETR for all the survey action. Get in touch on twitter @dvellante or email david.vellante@siliconangle.com. And don’t forget, Breaking Analysis posts, videos and podcasts are all available at the top link on the Wikibon.com home page.

Thanks everyone, be well and we will see you next time.

Watch the full video analysis: