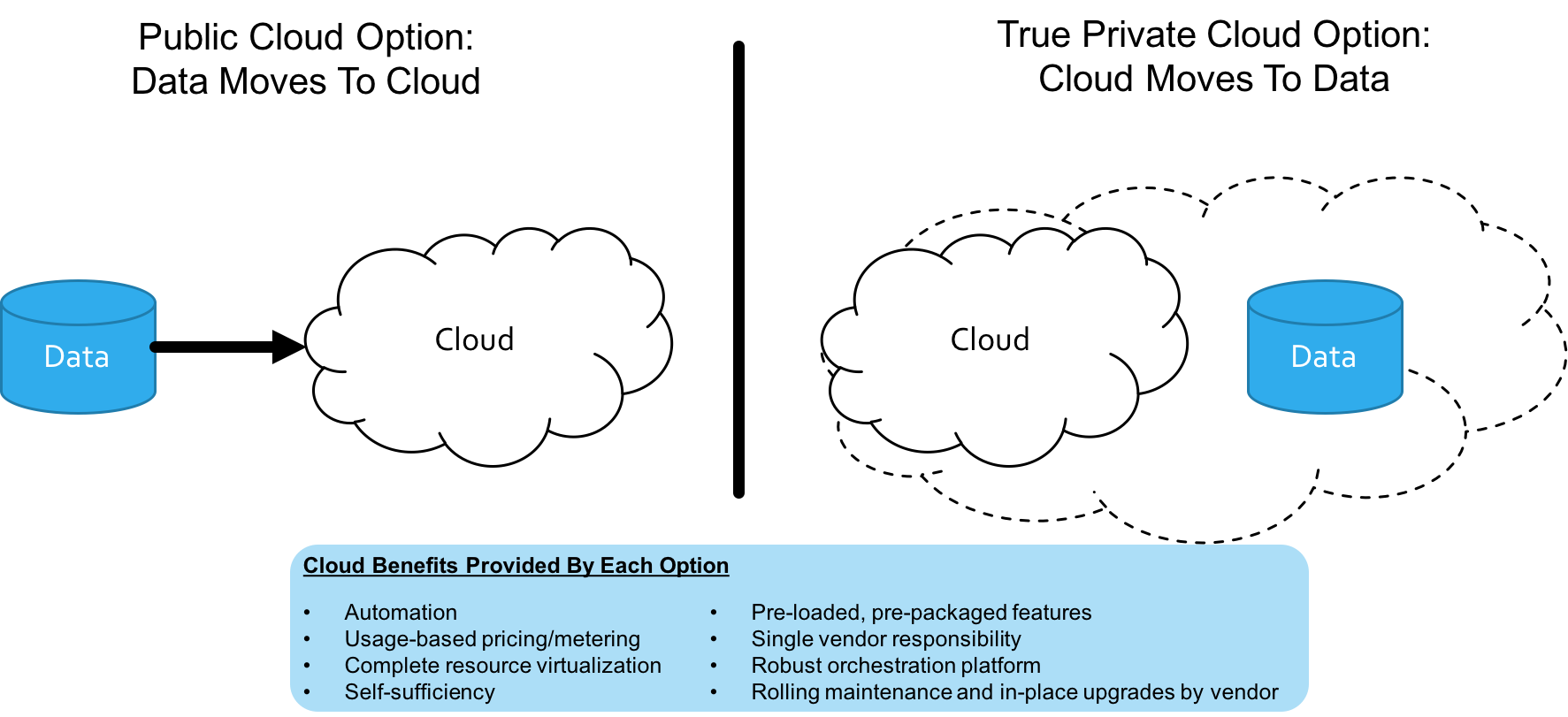

Cloud computing offers businesses infrastructure plasticity, faster change, lower administration costs, and superior matching between costs and utilization. A true private cloud (TPC) option provides cloud benefits on premises, for comparable costs of public cloud. As Wikibon predicted, these options are starting to enter the market, and are poised for significant growth.

With Stu Miniman, David Floyer, and Ralph Finos

Over the next few years, all application forms will benefit from the greater plasticity, lower administration costs, and superior matching between costs and utilization provided by cloud computing. However, not all applications are candidates for public cloud implementations. IoT edge applications cannot physically operate in public clouds (almost by definition); many legacy applications are prohibitively expensive to move to public cloud; and some high-value applications operate on data that businesses are reticent to place in public clouds (e.g., financial data).

For several years, server companies marketed “private cloud” products that used integrated virtualization to offer a subset of cloud benefits, but most users recognized these offerings for what they were: replacement products that fundamentally sustained installed footprints and server company business models.

In 2015, Wikibon predicted the emergence of a new class of system that offered the full range of cloud benefits for applications that didn’t satisfy the stringent physical, technological, or business constraints of public cloud. We called these systems “true private cloud” options because we foresaw that they would be packaged to offer the complete cloud benefit set in an on-premises setting.

And during 2016, true private cloud packaging did, in fact, emerge and expand from companies like Dell EMC, HPE, and Oracle. Moreover, public cloud suppliers took important steps toward delivering true private cloud options; although only Microsoft Azure offers a complete cloud packaging that can run locally.

This is our second year forecasting the TPC portion of the total cloud industry, and our research shows that TPC:

- Growth is strong. The TPC category nearly doubled in 2016, to $13B. While this is less than our 2015 forecast of $15B, it still reflects strong growth and is more than robust enough to encourage systems vendors to further invest in developing and delivering TPC alternatives.

- Leadership is shifting. Closing its acquisition of EMC vaulted Dell into the leadership position in TPC revenues, and the company shows no sign of letting go. A more focused cloud strategy also filled Oracle’s TPC “sales,” pushing it into a top 5 market position in 2016. TPC also fueled the growth of independent cloud service providers (CSPs), who marketed TPC options to customers requiring an alternative to the big cloud players.

- Future is bright. Although starting from a small base, the TPC category is poised to grow nearly 34% compound annual growth rate (CAGR) 2016 through 2026. By the end of 2026 forecast period, TPC will eclipse IaaS sales, as businesses increasingly employ SaaS/TPC combinations for their hybrid cloud strategies.

TPC Growth Is Strong

True Private Cloud (TPC) systems are distinguished from private cloud systems by the completeness of integration of all aspects of the offering, including performance characteristics such as price, agility, and service breadth. Equally important is the nature of the relationship with the TPC supplier, who is a single point of purchase, support, maintenance, and upgrades. The key benefit of TPC is that they provide solutions close to the cost and plasticity characteristics of public cloud in an on-premises or edge deployment when business, compliance, security, and latency requirements dictate. Today, the market for TPC includes systems that may not currently replicate public cloud services, but are on a committed path to that end, as well as hosted managed private cloud services. (See the Appendix for a complete discussion of our category definition.)

In 2016, the TPC category grew to $13B, a growth of 85% over 2015. Why? Because customers want the benefits of cloud for applications that don’t fit the public cloud mold. Therefore, a key architectural design assumption for enterprise infrastructure has flipped: After presuming data and applications would inexorably flow to the public cloud, the industry is now investing under an assumption that cloud services will extend into edge and on-premises locations, complementing public cloud (see Figure 1). Both segments represent large enough market opportunities to attract significant investment. AWS and Google, for example, will invest heavily to improve the performance, plasticity, security, and service portfolio for their public cloud options. So, too, will Dell EMC, HPE, Oracle, IBM, and newer players like Nutanix invest in TPC products that mirror cloud features.

TPC Leadership Is Shifting

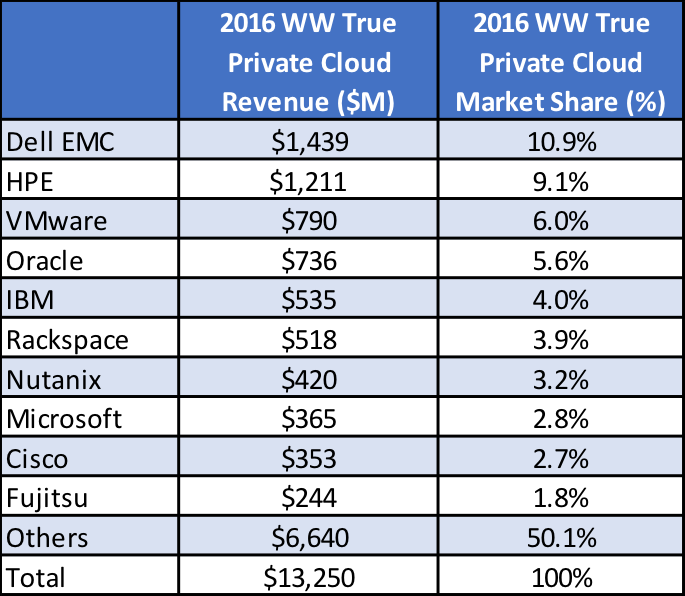

After years of competing with public cloud mainly by renaming existing offerings “private cloud,” all major systems vendors are now on a TPC vector with at least one product line. Start-ups like Nutanix catalyzed the change, but today Dell EMC, HPE and even Oracle are speeding down the TPC path. International players like Lenovo, Huawei, and Fujitsu are also bringing TPC options to global markets. Because most vendors are shifting TPC directions, year-to-year comparisons in the market are problematic, but our research shows that 2016 was a good TPC year, in particular, for Dell EMC, Oracle, Rackspace, and Nutanix.

The “Other” number in our market model is especially large. It includes most Managed Hosting Private Cloud players like CenturyLink and Expedient. However, it also demonstrates the lack of maturity in the category. Cloud computing is an incredibly complex set of technologies, only recently made simple through the remarkable technology and business engineering efforts of companies like AWS and Microsoft. Players like Dell EMC and HPE that choose to abandon their own cloud service efforts (to significant condemnation) are pivoting in part to TPC, but much engineering and business model work remains. Customer demand for TPC is high. Most CIOs we speak with presume that future system architectures will incorporate relatively integrated cloud models in both public and TPC modes.

Conspicuously absent from our list of TPC leaders are pure-play OpenStack solutions. While OpenStack technology provides a technically mature foundation for private (or public) cloud deployments, it has yet to see broad adoption. Huawei, Canonical, Cisco, and many other companies have a significant push in OpenStack, but other large players, like HPE, pulled back in 2016. Red Hat likely is the deployment leader, claiming 500 OpenStack production sites. Our expectation? OpenStack faces a make or break year in 2017, as Kubernetes and other initiatives mature and siphon off energy and revenue in the “open” TPC domain.

Table 1: True Private Cloud Market Shares, 2016

The TPC Future Is Bright

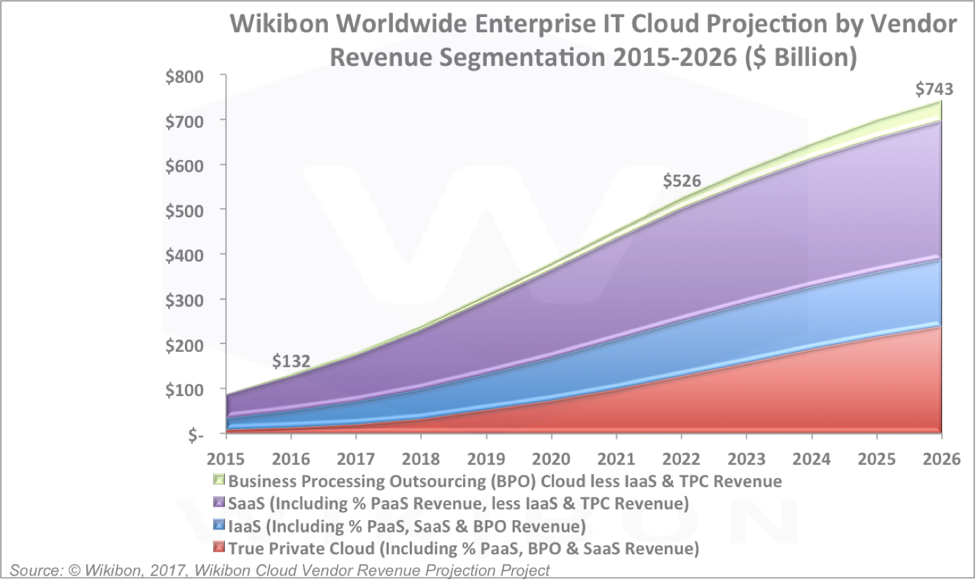

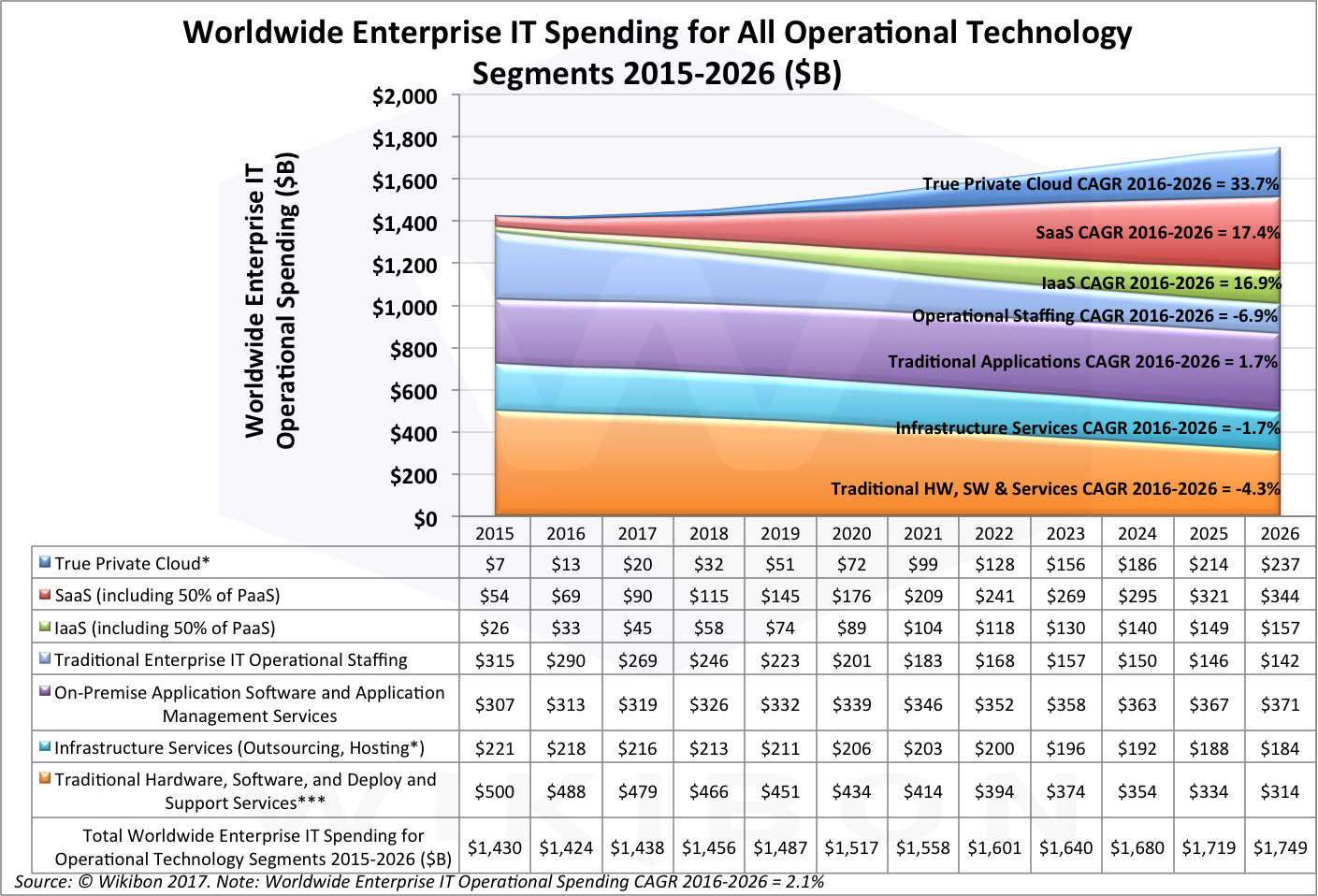

Through 2026, Wikibon projects that the TPC market will grow from $13B in 2016 to $237B worldwide by 2026, which is a robust 33.7% CAGR. By 2026, TPC will comprise 34% of the total $696B cloud market (see Figure 2). The adoption of TPC, however, will not lead to renewed spending on infrastructure services or traditional enterprise IT operations staffing; both will continue to fall over the next decade (2016 to 2026), by -1.7% CAGR and -6.8% CAGR, respectively (see Figure 3). This is a crucial point. The advent of TPC ensures that the systems will not evolve into a monopsony made up of AWS, Google, and Microsoft. While their market power will increase, TPC will sustain most large system vendors. However, the criteria are clear: TPC must be a true reflection of cloud benefits and not be a catalyst to sustaining traditional hardware-based IT and IT operations.

As enterprise IT groups divorce themselves from hardware-based practices, organizational structures, and sourcing relationships, workload will be the main determinant of public cloud and TPC choices (see Figure 4). Horizontal SaaS applications that don’t feature significant latency concerns, like most human-user, function-specific applications, will continue to grow in the public cloud, as will a range of big data and greenfield applications, so long as they don’t involve significant data movement costs. Industrial internet of things (IIoT), high-value legacy, and essential data (e.g., finance) applications will tend to move toward Edge TPC options. TPC also will attract greenfield applications that are likely to suffer onerous data communications costs unless sensible Edge data reduction policies are taken.

Our expectation is that virtually all enterprise IT will be conducted utilizing a hybrid cloud model that will be dominated by SaaS and TPC, with IaaS playing an important role in engagement applications and big data services. This will lead to a new dynamic in the cloud business: how best to traverse cloud boundaries as applications increasingly are composed from networks of cloud services operating in different clouds. Cloud gateways will be a fix, but the pressure to choose cloud alternatives that can support applications end-to-end will be extreme. Microsoft and Oracle are best positioned to offer end-to-end SaaS and TPC today, but eventually AWS, Google, and others will respond with TPC-like capabilities. Want evidence? Simply look at the VMware/AWS announcement of October 2016. While final details remain hidden, our expectation is that this will be one of many AWS moves to extend its footprint to local and edge computing instances.

Figure 3 can also be viewed as a modern vs. traditional IT comparison. The top three segments of Cloud Enterprise IT spending (True Private Cloud, SaaS and IaaS) are together growing at a 2016-2026 CAGR of about 20%. This growth together with the reduction in traditional IT is projected to reduce Operational Staffing Spend by a 2016-2026 CAGR of about -7%. The traditional IT spend is reducing by a 2016-2026 CAGR of about -2%. Overall this is good news for Enterprise IT, who should expect greater application value from applications in the modern segments, with significantly lower non-differentiated operational costs.

Source © Wikibon 2017

Action Item. True private cloud (TPC) is a practical response to real constraints on public cloud options. CIOs must begin building TPC into strategy plans and begin recasting key system vendor relationships now to ensure access the TPC options in the future, as those options mature and become more available.

Appendix

A “true private cloud” is distinguished from a “private cloud” by the completeness of the integration of all aspects of the offering, including performance characteristics such as price, agility, and service breadth. Equally important is the nature of the relationship with the cloud supplier – namely a single point of purchase, support, maintenance, and upgrades (often referred to as a “single hand to shake, and a single throat to choke”). The key benefit of true private cloud is that they provide solutions close to the cost and agility characteristics of public cloud in an on-premises deployment when business, security, and latency requirements dictate.

While aspects of the performance characteristics (i.e., virtualization) are broadly available today and characterized as “private cloud”, true private clouds are emerging as a distinct market sector – primarily from the hyperconverged infrastructure offerings (e.g., Cisco/NetApp Flexpod, Dell EMC Vblock & Vscale, HPE Synergy, Microsoft Partner ECI, Nutanix, Oracle Engineered Systems, HPE SimpliVity, etc).

While these products generally do not offer the totality of services today that we characterize as true private clouds, they are the vanguard of advanced building blocks along that path that Wikibon expects to rapidly evolve over the next few years.

Wikibon True Private Cloud Definition

As such, true private cloud should incorporate the following characteristics of public cloud:

- Significantly simplify the relationship between the user and the provider. That is, the user should have a relationship/transaction with a single provider, as is the case with public cloud. This can be realized in one or more ways:

- Through a foundation of hyperconverged systems (i.e., Nutanix, VMwre vSAN, Dell EMC VxRail, HPE SimpliVity, Pivot3, et alia) that are highly automated and managed as local pools of compute, storage, and network resources optimized to integrate the infrastructure as a single managed entity. We include cases where the system is converged but where Level 2 software support may reside with another provider.

- Hosted managed private cloud (CenturyLink Private Cloud, CSC BixCloud, Cisco Metapod, Expedient Private Cloud, IBM BlueBox, Rackspace Private Cloud, CenturyLink Private Cloud, et alia) would also be included in our definition. The chief characteristics of true private cloud in this case are it’s embrace of hyper-convergence as a service delivery vehicle and similar efficiencies for customers as provided by public clouds.

- Available on a self-service basis. Of course, the user can elect to pay for support from a provider if it useful, but there should be no requirement for permissions or provider intervention to use the service. Enterprises may impose rules of use of their own (say for access to hosted private cloud resources), but these would not affect how the user could interact with the true private cloud if they had license to.

- Allow users the flexibility to choose how IT resources are consumed – either “by the drink” or in a longer-term commitment. Whichever method they chose to pay their bills, the per-transaction cost of true private cloud should be transparent to the user.

- Designed to accommodate hybrid cloud application use cases. We believe that effective hybrid clouds will require much greater commonality and convergence of hardware and software within the hybrid on-premises and cloud components. As a result, a significant portion of the enterprise public cloud and on-premises true private cloud will be part of an integrated hybrid cloud. The most effective and highest function hybrid clouds will share common storage as well as hyperscale server and orchestration/automation layers between public clouds and true private clouds. See the recent Wikibon report https://wikibon.com/hyperconverged-infrastructure-as-a-stepping-stone-to-true-hybrid-cloud/ for a more complete exploration of this emerging requirement.

In terms of levels of convergence to qualify as true private cloud, Wikibon would expect to see automation and orchestration including:

- Cluster management

- Network automation and management

- VM/container automation and management

- Storage automation and management

- Application templates and deployment tooling

- Operations dashboard

- Workload analytics

- Capacity optimization

- Log management

- Root cause analysis

- Remediation tools

- Configuration monitoring and dynamic changing

- Proactive alerts

- Backup and replication services on premises or hybrid to other cloud services

- Snapshot management & catalog services

Managed/Hosted True Private Cloud

Managed/hosted true private cloud includes offerings such as Cisco MetaCloud, Verizon Private Cloud, Rackspace Private Cloud, CenturyLink Cloud Managed Services, IBM Softlayer Private Cloud, IBM BlueBox, Internap Dedicated Private Cloud, Dell Managed Cloud Services, Platform9, et alia. These offerings, as far as the user is concerned, look and behave like a public cloud services except that under the covers, the resources are not shared across enterprises.

What Our Definition Does Not Include

Wikibon is taking a long term, disruptive perspective on the optimal end state that true private clouds should be reaching in the next decade to realize the full value of “cloud” if they elect to own their own cloud in their data center or via providers. As such the following are not included in our sizing or forecast of true private cloud.

- Converged systems with limited orchestration and automation, i.e. not meeting the true private cloud criteria above.

- Self-integrated private cloud or convergence involving numerous vendors. For example, Wikibon would regard the installation of VMware vSphere (or Microsoft HyperV) on new Dell EMC or HP servers and storage, and Cisco networking along with packaged orchestration and automation as “virtualization” but not true private cloud. Virtualization is a useful step, but ultimately falls short in terms of costs and supportability to the quantum gains that true private cloud can deliver. This extends to situations where users deploy VMware tools such as vSphere, vCloud Suite, etc. or Microsoft Cloud Platform System – but not as part of a single entity managed converged solution. VMware, Microsoft, and other software providers, of course, participate in this market significantly as OEM providers to hosters of private clouds who take full responsibility for a true private cloud converged systems with infrastructure management and automation.

- Spending by service providers (AWS, Azure, Softlayer etc.) for their public cloud infrastructure whether self-built or acquired via a converged system. While these are advanced deployments and there is considerable activity in the Service Provider sector to build their own clouds to offer as a public cloud service, Wikibon’s perspective for this report is on what enterprises should be doing to duplicate Public Cloud experience, costs and efficiencies. We cover this architecture in the report “Server SAN Readies for Enterprise and Cloud Domination“.

- Spending for cloud consulting, support and deployment, general data center outsourcing, co-location, and similar services – unless the service is to maintain and manage a private cloud for an enterprise.

- Virtual private cloud (Amazon VPC, Azure Virtual Network, CSC Virtual Private Cloud et alia). These revenues are included in our public cloud figures now.