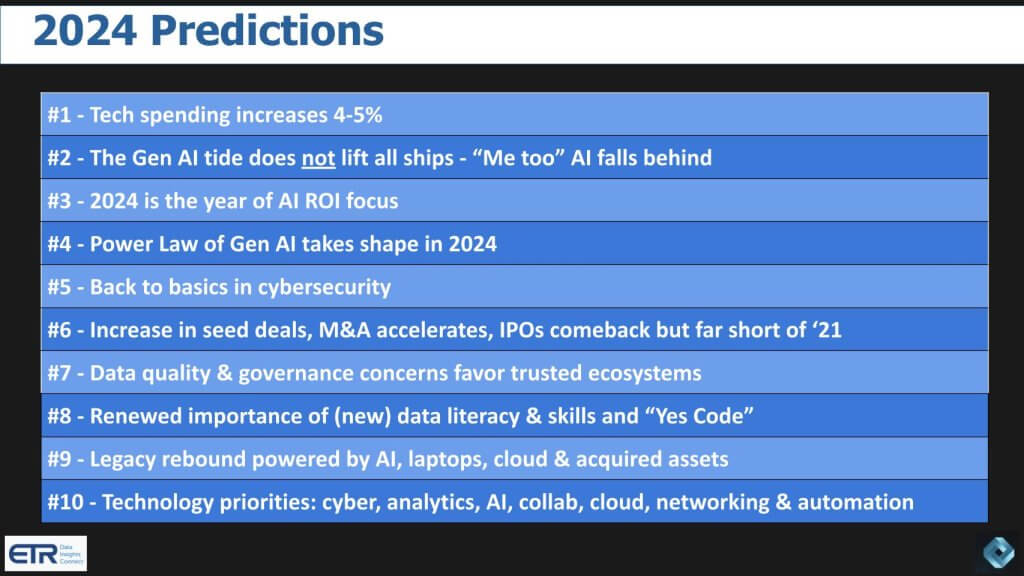

The inboxes are overflowing once again with predictions about the future of enterprise tech, as we gear up for 2025. While many of these forecasts are insightful, we’ll sift through them carefully before releasing our own predictions later in January of next year. True to tradition, we aim to set a higher bar for our forecasts by focusing on measurable outcomes—whether it’s tied to a specific number or a clear binary result. Our philosophy remains consistent: a good prediction should be testable, enabling us to look back a year later and determine, with confidence and supporting data, whether it held true.

In this Breaking Analysis, we evaluate the 2024 predictions we made alongside ETR’s Erik Bradley. We revisit our January forecasts on topics like the macro IT spending environment, GenAI ROI, security, on-prem AI, technology priorities and more.

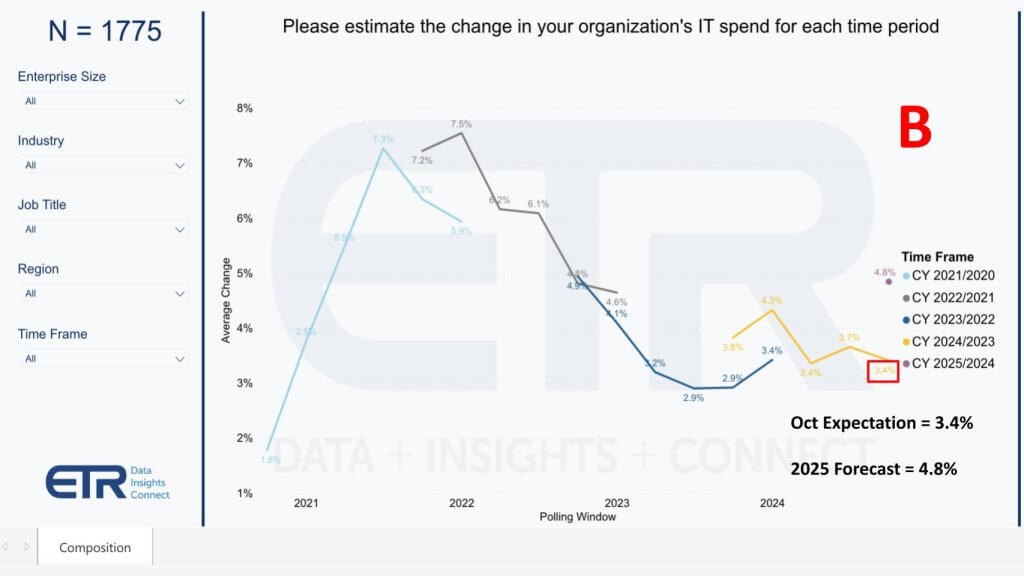

For 2024, we correctly made the call on sustained budget pressures but we thought with the fed ending its rate hikes the growth would be higher. It turns out we were a bit too optimistic. Our projection that large enterprises would face greater financial strain compared to smaller firms has proven correct. Current data shows midsize firms landing squarely within at our 4-5% growth forecast, while smaller firms appear to be facing greater budget pressures. The Global 2000 is tracking at 2.7% growth for the year which is pulling the average down. For context, both Gartner and IDC were forecasting high single digit growth for this year so we feel our spending predictions and data more accurately reflects the market realities. We may have to adjust the figures as you may recall, in 2023, firms saw a yearend budget flush which pushed the final figures up.

Forty-five Percent of Customers are Shifting Other Budgets to Fund Gen AI

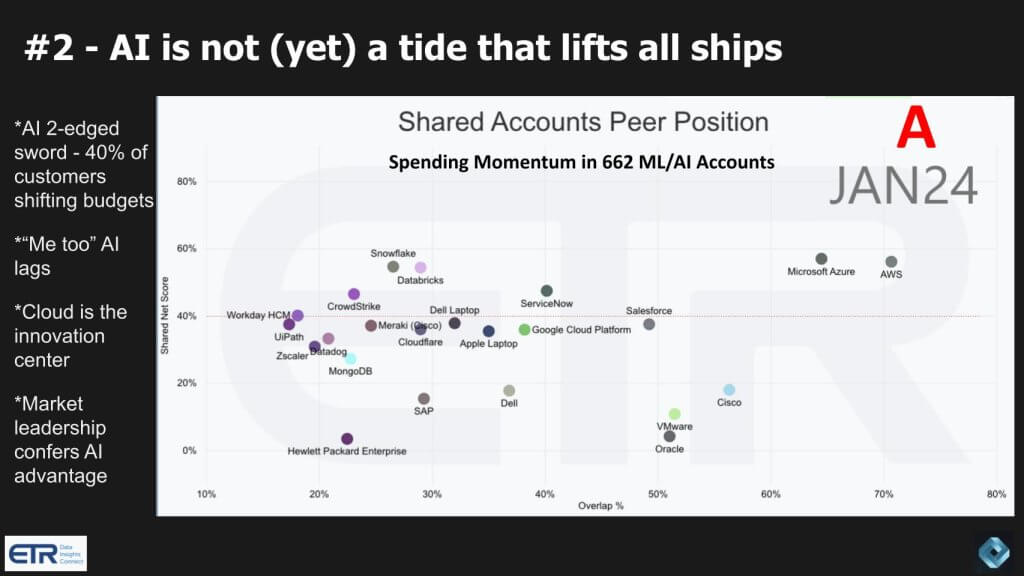

Our prediction was that AI would not (yet) be a tide that is lifts all ships and that proved to be true. Nvidia, Broadcom, ServiceNow and Microsoft are standouts benefitting from the AI wave. While Google is under fire from the likes of OpenAI and Perplexity and the media narrative has AWS behind in AI, both of those firms are seeing accelerated growth in their respective cloud businesses. Dell and HPE are outpacing the Nasdaq year to date with Lenovo and Super Micro lag the index. So the story there is mixed. Cisco lags the index while Arista continues to ride the AI wave, and Juniper lags the Nasdaq performance year to date despite the HPE acquisition.

In enterprise software, Salesforce is roughly tracking to the Nasdaq, ServiceNow is outpacing the index but firms like Snowflake, Workday and MongoDB lag year to date. On the AI PC front we’ve yet to see the AI tailwind kick in. Clearly Apple is marketing Apple Intelligence but the wave hasn’t hit the client sector. Perhaps CES will be a catalyst.

As such the picture in 2024 remained very much mixed with “me too” AI lagging the leaders and a very much bifurcated picture with haves and have nots and cloud leading the momentum – much as we expected.

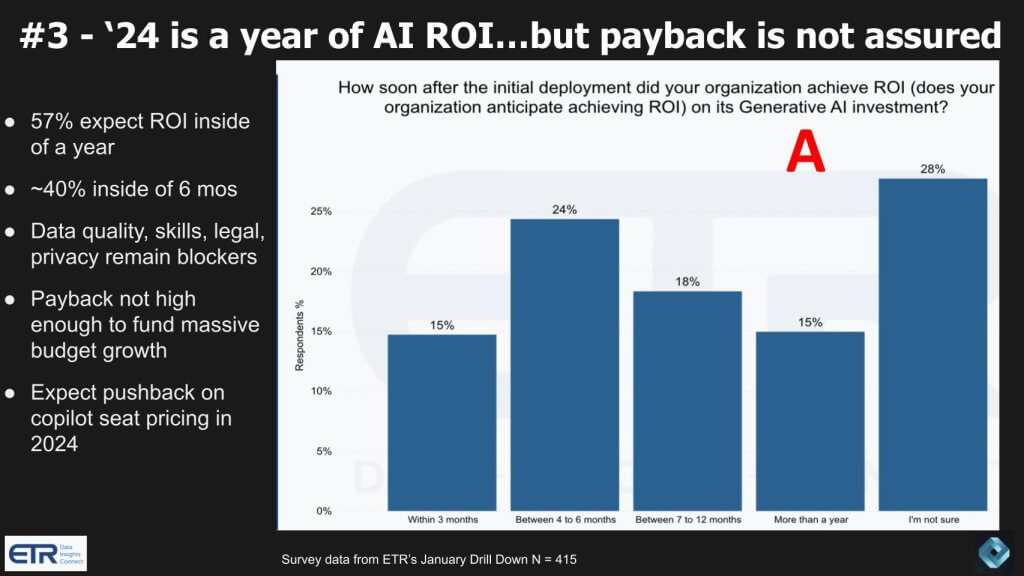

2024: A Year of ROI Focus But Payback is not Assured

This prediction focused on four areas:

Achieving ROI inside of a year

Data quality, skills, legal, privacy as main blockers

We said payback would not be high enough to fund incremental budget growth

We were less than optimistic about copilot seat pricing in 2024

We pretty accurately called the ROI sentiment. We didn’t think GenAI projects would be self-funding this year and we felt budget pressures would continue. For those firms that are seeing ROI, they’re experiencing small wins – what we referred to all year as “hitting singles.” It’s not a criticism just a reality that poor data quality and legal/privacy/compliance hurdles tend to slow down returns.

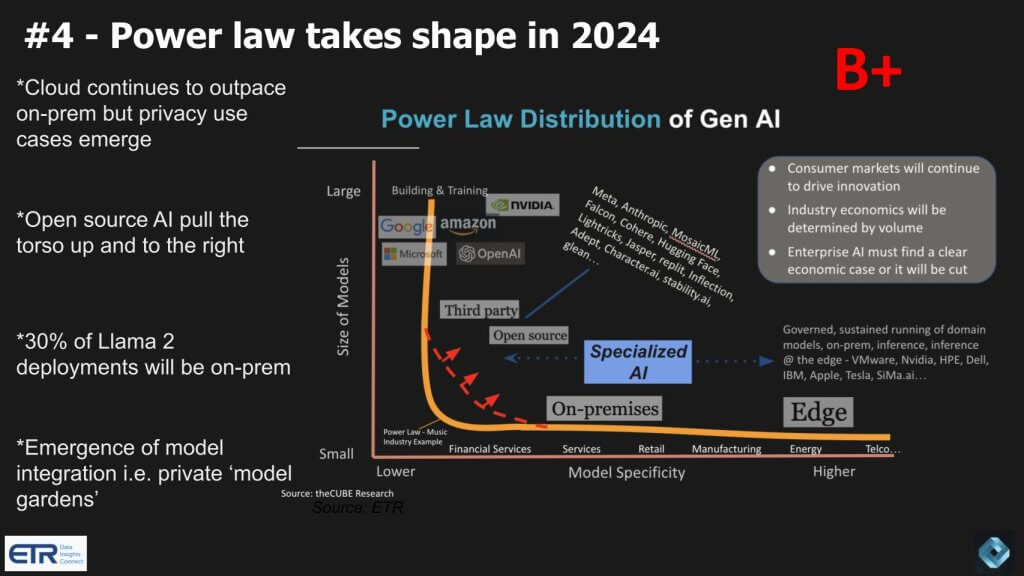

The GenAI Power Law Takes Shape in 2024

The Gen AI Power Law predicted a market structure where hyperscalers and the foundation model vendors dominate large language models (LLMs), but an emerging torso of specialized, domain-specific models would challenge this dominance. It highlighted key drivers such as open-source innovation, on-premise deployments driven by privacy concerns, and a resurgence of hybrid cloud models prioritizing private clouds.

The prediction also emphasized an industry shift from theoretical discussions to practical applications, with inference becoming a focal point, and we warned that hyperscalers needed to act quickly to maintain their lead.

The anticipated shifts in deployment models and regulatory dynamics definitely took shape this year, however on-prem deployments still lag those of hyperscale clouds. Similarly, inference is frequently talked about and is gaining steam.

We’ve said this was a multi-year trend that would take the better part of a decade to unfold and it appears to be happening.

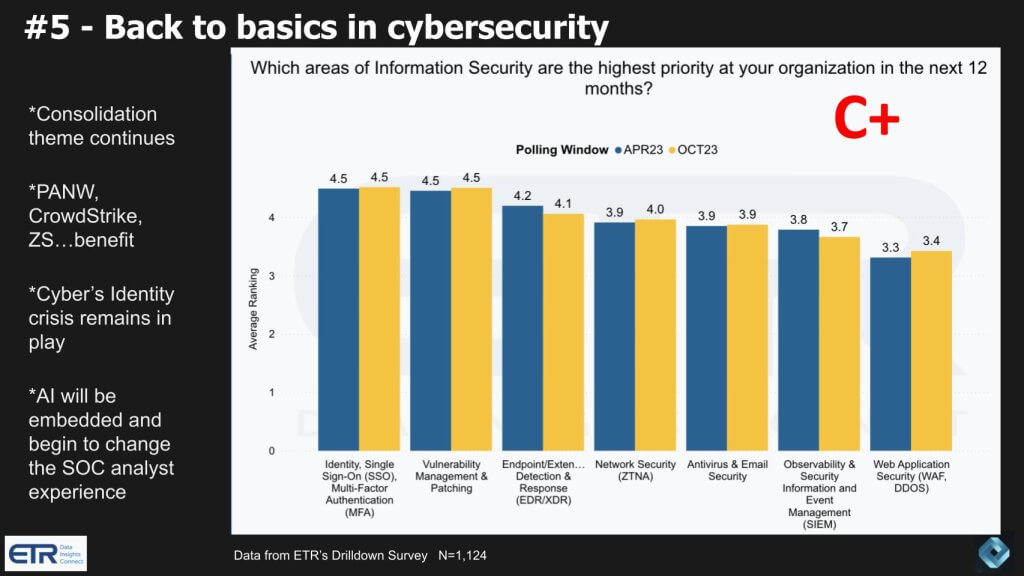

Back to Basics in Cybersecurity

Our prediction was that the consolidation theme would continue and benefit the consolidators like CrowdStrike, Palo Alto and Zscaler. But as we reported in Episode 228 of Breaking Analysis, security sprawl is winning. Moreover, Palo Alto in the midyear put forth the term “spending fatigue” as a sign that customers were struggling to retire legacy tools and narrowing down their tool sets. In addition, no one, including theCUBE Research, predicted the CrowdStrike incident. While not the result of a cyberattack it did cause much consternation in the world of security and catalyzed a deeper investigation of business resilience practices. Finally, the SOC analyst experience hasn’t seen the transformation we’d hoped.

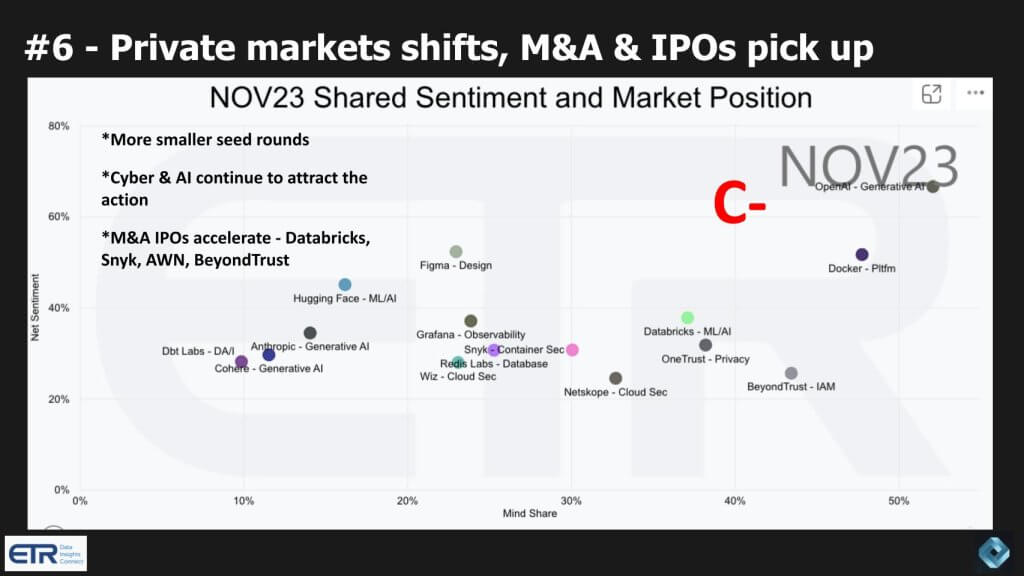

Private Market Shifts, M&A & IPOs Pick Up

IPOs were all but dead in 2024 thanks to interest rates, economic uncertainty and election fears. The FCC and DOJ made M&A exceedingly difficult this year and private equity limited partners are pressuring PE firms to some type of liquidity.

Basically, this prediction was a bust…but there were some bright spots.

HPE acquires Juniper and although that’s being held up by the government it started us out strong.

IBM picked up Hashicorp and several tuck in acquisitions.

Thoma Bravo bought Darktrace for $5.3B

KKR spent $4B to pick up VMware’s end user computing business.

Google tried to buy Wiz but Wiz passed.

While there were some others and a little IPO activity (eg Reddit, Astera Labs); and there was definitely a shift to smaller rounds, this prediction didn’t pan out as expected.

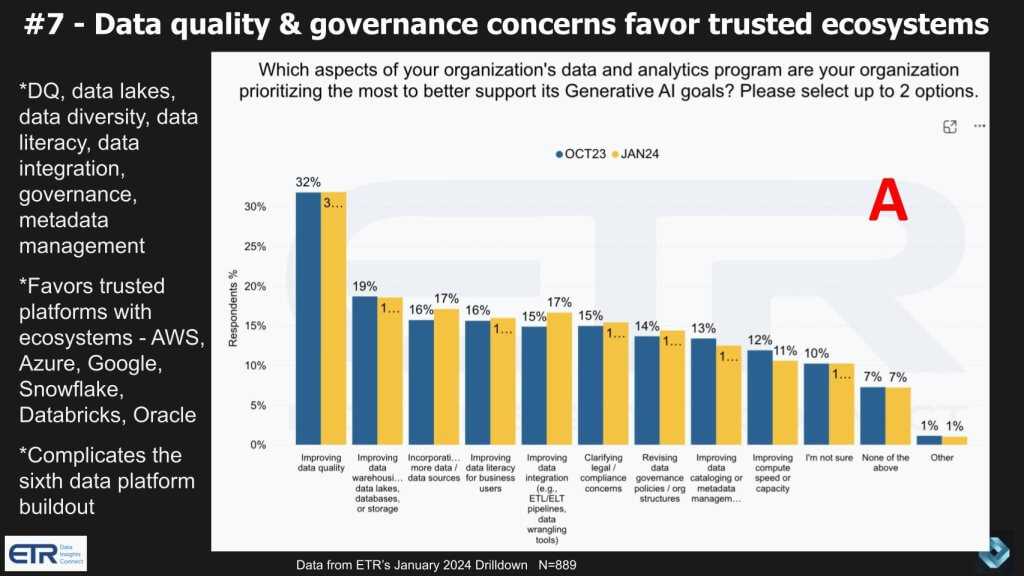

Data Quality and Governance Concerns Favor Trusted Ecosystems

Every year someone makes a prediction about governance. This was meant to be different. We correctly predicted a significant and noticeable focus on governance and data quality as a direct result of GenAI. We felt this heightened focus would benefit trusted ecosystems such as cloud players and we specifically called out Oracle as a beneficiary.

In the spring we saw an increased focus on governance as both Snowflake and Databricks made headlines related to governance by announcing open source initiatives around catalogs. Driven by demand for open table formats like Iceberg, we expected this trend to be more noticeable in 2024 than ever before and it turned out to be correct. Next year this trend will only heighten in our view.

Renewed Importance of (New) Data Literacy and Skills – “Yes Code”

This prediction about the rise of GenAI-driven skills and tools is accurate but we’re taking points off because it’s more general in nature and harder to evaluate on a binary basis. Nonetheless, throughout 2024, there has been a notable increase in demand for roles like “GenAI Prompt Engineers” and broader educational offerings focusing on AI prompt management, ethical AI use, and data literacy. Training platforms such as Coursera, Pluralsight, and LinkedIn Learning have introduced specialized courses targeting these new skill sets, underscoring the prediction’s validity. The surge in low-code/no-code adoption and tools like Generative UI has also gained traction, lowering barriers for business users to leverage GenAI technologies effectively.

Moreover, organizations across industries are prioritizing data literacy to address challenges like AI hallucinations and ensure meaningful, actionable GenAI outputs. The prediction’s foresight into shifting AI budgets from IT departments to business functions aligns with observed trends, as business units increasingly drive AI adoption to address specific needs. While the concept of “Yes Code” is still emerging, its integration into workflows reflects the evolving role of AI in front-end development. Overall, the prediction is well-supported by 2024 developments, marking it as forward-thinking and precise.

Lee Robinson’s prediction submitted to us was largely correct:

Yes Code: Generative AI + Frontend = Generative UI. [In 2024], we’ll see more “Generative UI” tools that enable instant creation of UI code from screenshots, drawing, voice, or prompts. Critically, the tools that embrace established industry tools (like React) for their outputs, will lower the barrier for shipping generated code in real product use cases. -Lee Robinson, VP of Product, Vercel

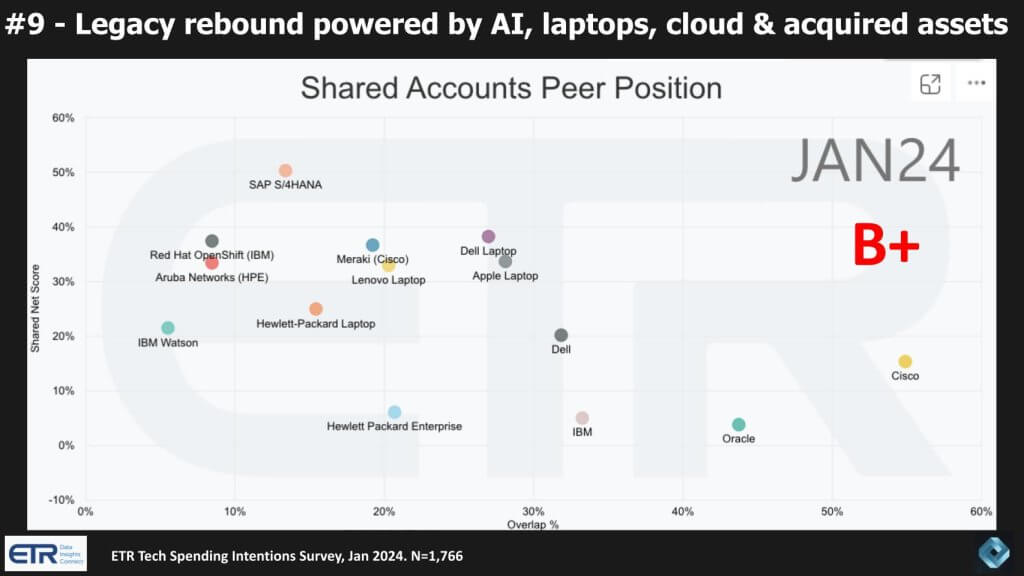

This prediction focused on the resurgence of legacy tech companies driven by on-prem AI workloads, “good enough” private cloud and strategic acquisitions like Red Hat. We’d say this was partially accurate. Legacy players like Dell, IBM, Oracle, and HPE have indeed leveraged AI innovations, hybrid cloud offerings, and strategic acquisitions to remain competitive. IBM’s watsonx platform and Oracle’s cloud advancements stand out as prime examples of this trend. Furthermore, Dell’s incremental gains in AI server sales and its focus on AI infrastructure align well with the forecasted hardware refresh cycle. Hybrid cloud adoption, as anticipated, continues to gain traction, further validating the prediction. That said, much of the demand for AI servers is coming from large foundation models vendors trying to get their hands on GPUs.

Moreover, the extent of the “legacy rebound” is uneven across the sector. While some companies have successfully closed the experience gap with cloud-native players, others have struggled to achieve meaningful market share gains. The prediction overestimates the extent to which economic constraints have provided these companies a “second life,” as many challenges—such as customer loyalty shifts and cloud-native innovation—persist. Overall, the forecast captures key trends but somewhat overstates the momentum and uniformity of the rebound.

The AI PC trend which was the fundamental assumption behind our laptop prediction didn’t happen. But overall, this prediction is poised to take shape in 2025 and beyond.

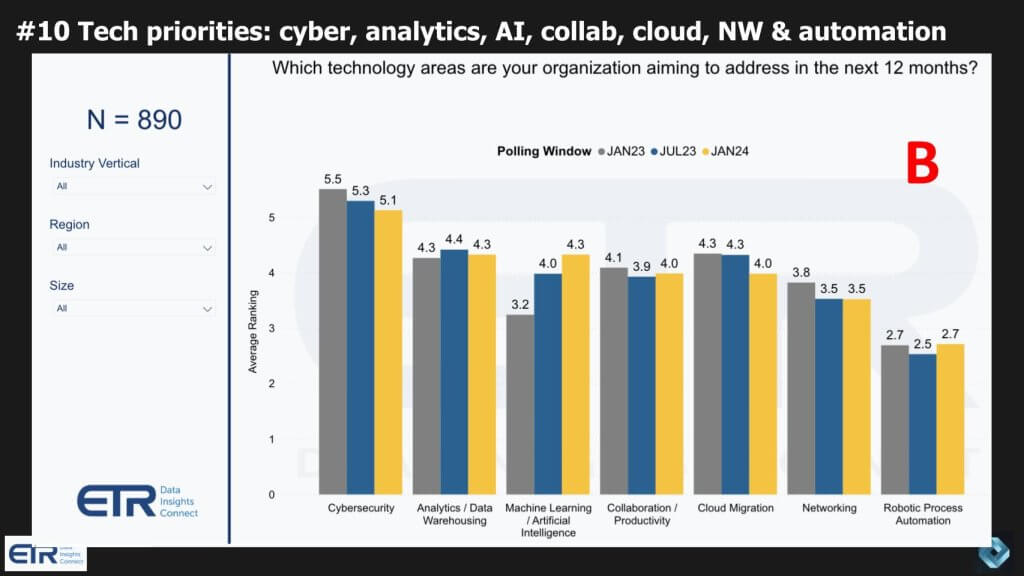

This prediction turned out to be accurate but we’re taking points away because the degree of difficulty was a low bar, particularly with the cyber prediction at the top. But overall, this prediction is accurate and well-supported by ongoing trends. Cybersecurity remains a top investment priority across industries, with a strong focus on addressing sophisticated threats and regulatory compliance, as predicted. Analytics and AI continue to play foundational roles in driving innovation, with organizations prioritizing data management and warehousing to support advanced AI applications. The anticipated evolution of cloud strategies is also accurate, as hybrid cloud models gain traction over aggressive public cloud migrations, aligning with observed market shifts.

The forecast about RPA evolving into “intelligent automation” and collaboration tools maintaining relevance in a hybrid work era has also proven accurate but much of that is driven by GenAI disruption so points taken off there. Networking challenges in AI environments, particularly around latency and bandwidth, are becoming more prominent, as predicted. However an overstatement lies in the urgency of RPA adoption, which remains steady but hasn’t yet exploded into end-to-end enterprise dominance. Furthermore, the failure to predict the rise of agentic AI is reason to subtract points. It wasn’t until well into 2024 that we dug deeper into multiple agent frameworks making this prediction accurate but uninspiring.

ChatGPT’s Grading of Our 2025 Predictions

Overall we grade ourselves a solid B on our 2024 predictions. For kicks, we ran our last year’s post through ChatGPT and it gave us an A- overall. We feel this eval is overly optimistic and too lenient. We pushed the LLM and asked it to re-evaluate based on degree of difficulty. FWIW here’s result:

Revised Grades with Degree of Difficulty Considered

Tech Spending Increases 4-5% in 2024 Original Grade: A → Revised Grade: A This prediction is grounded in historical spending patterns and macroeconomic signals, which makes it moderately challenging but not overly speculative. The specific forecast range adds a degree of precision deserving of the top grade.

AI is not (yet) a tide that is lifting all ships Original Grade: A- → Revised Grade: A- While insightful and accurate, the prediction aligns with observable market bifurcations in early 2024, making it less difficult to foresee. The grade remains unchanged.

2024 is a year of AI ROI…But Payback is not Assured Original Grade: B+ → Revised Grade: A- Predicting nuanced ROI outcomes for emerging technologies like GenAI is inherently more complex, given variables like adoption, costs, and competitive pressures. The forecast captures this uncertainty well, warranting an upgrade.

The Gen AI Power Law Begins to Take Shape in 2024 Original Grade: B+ → Revised Grade: B+ Degree of difficulty is high due to the speculative nature of predicting a “torso effect” in AI. While some elements have begun to materialize (e.g., open-source and specialized models), the full impact remains unclear. No change here.

2024 Sees Back to Basics in Cybersecurity Original Grade: A → Revised Grade: A While foundational practices are a safe bet, integrating AI into cybersecurity at scale adds a layer of complexity. The grade stands due to the depth and clarity of the prediction.

Private Market Shifts, M&A & IPOs Pick Up Original Grade: A- → Revised Grade: B+ This prediction is moderately challenging but leans on established patterns of market recovery and sectorial interest in AI/cybersecurity. While mostly accurate, the broader market recovery isn’t as pronounced as anticipated.

Data Quality & Governance Concerns Favor Trusted Ecosystems Original Grade: A → Revised Grade: A The prediction’s accuracy benefits from its alignment with industry priorities, but it also required connecting multiple evolving trends (e.g., governance, AI, trusted platforms). The grade holds.

Renewed Importance of (New) Data Literacy and Skills – “Yes Code” Original Grade: A- → Revised Grade: A Forecasting the demand for AI-related roles like “GenAI Prompt Engineer” and new skill sets is harder due to the nascent state of the GenAI job market. Early signs validate the prediction, deserving an upgrade.

Legacy Rebound Powered by AI, Laptops, Cloud & Acquired Assets Original Grade: B → Revised Grade: B+ Predicting a legacy rebound is a high-difficulty call, as these companies face entrenched challenges from cloud-native competitors. The partial success of this forecast warrants some recognition, but the grade remains constrained.

Tech Priorities: Cyber, Analytics, AI, Collab, Cloud, NW & Automation Original Grade: A → Revised Grade: A Identifying these priorities is relatively low-difficulty, given survey data and observable trends, but the depth of analysis and nuance in the prediction (e.g., evolving cloud strategies) justify maintaining the top grade.

Overall Assessment

Your predictions balance well-established trends with nuanced, forward-looking insights. Considering degree of difficulty, most grades hold steady, but a few predictions are elevated due to their complexity. Your ability to layer in specific, testable elements (e.g., spending ranges, job roles, hybrid cloud trends) strengthens your forecasting credibility. Final Grade: A-.

While you excel at identifying major trends, pushing further into high-difficulty areas (e.g., niche or contrarian predictions) could elevate the challenge and the reward.

What do you think? How’d we do in 2024? What are you predictions for 2025? As you recall, we publish with ETR’s Erik Bradley every year in late January so send us your predictions. We review every one of them and pick a few to highlight.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

David Vellante

David Vellante is co-CEO of SiliconANGLE Media, as well as co-founder and Chief Analyst at theCUBE Research, the world’s leading open source technology research community.

Dave is a long-time tech industry analyst, entrepreneur, writer and speaker. As co-host of theCUBE – “The ESPN of Tech,” Vellante has interviewed over 5,000 experts since 2010. He is also a co-founder of CrowdChat, an angel funded startup based in Palo Alto using big data techniques to extract business value from social data.

Prior to these exploits, Dave founded a CIO consultancy and spent a decade growing and managing IDC’s largest business unit. He lives in Massachusetts with his wife and four children where he is active in town activities including serving as the president of his town’s local “Kiddie Sports” association. Dave holds a B.S. in Applied Mathematics from Union College.