The stablecoin market is rapidly maturing into one of the most consequential sectors of the digital asset economy. After years of uncertainty, regulatory friction, and media skepticism, stablecoins are no longer a speculative curiosity, rather they are foundational to the next chapter of programmable finance. Our research suggests that the convergence of policy shifts, institutional adoption, and new economic use cases has thrust stablecoins into the spotlight. In short: crypto’s ChatGPT moment has arrived, and its name is stablecoin.

In this Breaking Analysis we answer your questions about stablecoins. We’ll cover what stablecoins are and why they’re relevant. We’ll also dig into where they fit in the crypto value chain and what the public policy shifts mean to the industry. Specifically, we’ll look at the genius act and what it portends for crypto and what’s next with the Clarity Act. We’ll also dig into what this all means for US Treasuries and finally what the risks are to this whole movement.

Now to help frame this we’re going to draw on an interview from our NYSE CUBE studio that John Furrier did with Tom Lee as part of our CUBE + NYSE Wired Crypto Trailblazer series. Tom Lee is a Managing Partner and the Head of Research at Fundstrat Global Advisors. He is by far my favorite guest from TV programs like CNBC and provides next level analysis on markets and financial trends. For a long stint he was J.P. Morgan’s Chief Equity Strategist and is the chairman of Bitmine Immersion Technologies which is a blockchain tech and digital asset management firm. So we’ll insert commentary from that interview throughout this episode.

https://www.youtube.com/watch?v=gf_qOVHpDlo&t=1s

Here’s the TL;DR on these questions:

- What are stablecoins?

Digital assets pegged to fiat (typically USD), enabling low-volatility, safe transactions in the crypto ecosystem. - Why are they relevant?

Think of stablecoins as the financial rails of crypto – they power payments, trading, and yield, which drive real revenue and subsequently adoption. - Where do they fit in the crypto value chain?

At the intersection of decentralized finance (DeFi), institutional finance, and programmable money – especially on Ethereum which we’ll talk about more. - Policy divergence: Biden vs. Trump/Sacks; Gensler vs. Paul Atkins

Biden/Gensler pushed aggressive SEC oversight and frankly opacity. Crypto industry executives complained that when they’d visit Gensler at the SEC and shared their information, the next week they’d get a C&D or they got de-banked. The Trump administration led by Crypto and AI Czar David Sacks are far more crypto-friendly and pro-innovation; supporting new laws that bring clarity to the table. This has created a huge shift in sentiment. - Massive regulatory shift – What’s changed?

Growing clarity (and bipartisan support) is driving institutional participation and reducing the stigma that crypto is a scam – it legitimizes crypto. - What is The Genius Act

It standardizes stablecoin rules across issuers and focuses on reserve transparency and interoperability. - The Clarity for Payment Stablecoins Act – What is the Clarity Act?

Legislation that has passed committee with bipartisan backing and provides legal routes for banks and fintechs to issue stablecoins. This is huge because mainstream traditional institutions are getting in on the act. Remember when Jamie Dimon threw cold water on crypto and then flip flopped on that issue? Well this will take crypto into hyperdrive. - How are stablecoins backed?

Most major stablecoins are backed by short-term U.S. Treasuries that earn yield without passing it to holders – 4-5% yield. - What are the Implications for treasuries?

Stablecoin demand is now a meaningful new source of U.S. Treasury buying – this expands the global reach of the USD and makes treasuries more attractive because they are the major asset backing stablecoins. There are other real world assets (RWAs) like securities, art, physical assets and even real estate. Real estate in particular is more complicated primarily because it’s less liquid. But the tokenization of RWAs is real. Remember the NFT craze when Beeple got $69M for his digital art? Well the idea of tokenizing real world assets is back in vogue and this promises much less friction in asset sales. - Risks and critiques

Regulators are rightly concerned about protections for consumers, inadequate oversight, especially of international stablecoin providers, runs on stablecoins, regulatory arbitrage – especially around state-level loopholes, reserve quality, systemic risk from concentration, too-big-to-fail dynamics.

Despite all the enthusiasm, which is awesome, we’ve seen this before where the regulatory pendulum swings toward less oversight which invariably leads to bad behavior and often market meltdowns.

Ok so let’s dig in a little more to each of these questions.

What Are Stablecoins?

Stablecoins are digital assets pegged to the value of fiat currencies – most commonly the U.S. dollar. Unlike cryptocurrencies such as Bitcoin or Ethereum or Solona, which are highly volatile, stablecoins maintain a steady price by being backed with reserves, either in fiat, other cryptocurrencies, or algorithmic mechanisms. Think of stablecoins as the grease in the wheels of crypto markets, enabling real-time trading, payments, and increasingly, on-chain financial services.

According to Tom Lee, stablecoins and the recent change in attitude of from public policy has created the “ChatGPT moment for crypto” and has become a catalyst for broader institutional acceptance – and a growing revenue engine for banks and platforms alike.

[Watch Tom Lee explain his point of view on the ChatGPT moment for stablecoins].

The stablecoin business has become the ChatGPT moment for crypto. It’s widely been adopted by consumers and merchants. And now banks want to offer stablecoins. Most of that’s taking place on Ethereum. – Tom Lee on theCUBE + NYSE Wired

Why Ethereum?

For those not familiar with the premise behind Ethereum let’s explain briefly. Bitcoin is often referred to as a store of value or digital gold. You buy it and hold it. But it doesn’t really have much utility in terms of enabling new technologies or supporting the development of nascent markets like decentralized apps (dApps) or supporting the exchange of goods and services via smart contracts. Bitcoin is not programmable. Ether is. The primary programming language for developing smart contracts on the Ethereum blockchain is called Solidity. It’s an object-oriented language, purpose-built for creating smart contracts that run on the Ethereum Virtual Machine (EVM). Its syntax is much like C++, Python, and JavaScript, which makes it relatively easy for developers who are familiar with these languages.

Of course GenAI will make programming Ethereum even easier. So Ether’s founders like Vitalik Buterin and Anthony Di Iorio (a CUBE alum by the way), had the vision of creating a blockchain platform that was programmable and could execute smart contracts to build decentralized applications. And this is all gaining new momentum in the market.

Why Are Stablecoins Relevant?

Stablecoins represent a bridge between the traditional financial system and the decentralized future. Their relevance stems from four factors as shown below:

But let’s dive in a bit deeper:

- Financial Infrastructure Modernization – Stablecoins are useful because they reduce friction in cross-border payments. This has been a dream in finance forever – i.e. enabling 24/7/365 settlement with low fees.

- Dollarization and Monetary Policy – As Tom Lee noted, this is a “dollarization story”. Stablecoins have become a global flashpoint for U.S. dollar influence.

- Programmable Yield and Treasury Replacement – Ethereum-based staking and yield generation now offer viable alternatives to traditional fixed-income strategies. Ethereum staking is where you lock up your ETH to help secure the Ethereum network and earn rewards in return. It’s a core part of the Proof-of-Stake (PoS) consensus mechanism that Ethereum uses. By staking your ETH, you become a validator, responsible for verifying transactions and adding new blocks to the blockchain. And simply by holding the asset you earn returns that are typically better than fixed-income instruments.

- Institutional Entry Point – Banks and asset managers are entering the space through regulated stablecoin products. And this is a game-changer because it’s flipping the script on the safety and stability of crypto.

[Watch Tom Lee explain the economics behind stablecoins and staking].

Stablecoins are a hugely profitable business. Circle is showing it, because they don’t pay interest and they’re earning 4% on their reserves… Coinbase is very profitable… Ethereum treasury companies are very profitable.” – Tom Lee

Where Do Stablecoins Fit in the Crypto World?

Stablecoins operate as the foundational layer of liquidity in the crypto ecosystem. They are integral to decentralized finance (DeFi), centralized exchange (CEX) operations, and emerging use cases like tokenized real estate and equities. Although we’re less bullish on real estate as an asset backer for stablecoins because of it’s inherent lack of liquidity. But over time that will perhaps evolve. In Lee’s words, Ethereum has become “the biggest macro trade for the next 10 years,” in part because it is the dominant substrate for stablecoin deployment and smart contract innovation.

Ethereum is programmable. It is really robust… Wall Street is coming in and saying, ‘I want to tokenize a dollar.’ That’s the stablecoin. – Tom Lee

Public Policy and the change From Enforcement to Engagement: Trump, Sacks and Atkins Shift the Regulatory Posture

The transition from the Biden-Gensler regime to the Trump-Sacks-Atkins leadership marks a clear and deliberate pivot in U.S. crypto policy – from an enforcement-first posture to a market- and crypto-friendly framework aimed at better clarity and sparking innovation.

Under President Biden, former SEC Chair Gary Gensler – as you’ve heard us complain many times on theCUBE Pod, pursued an aggressive enforcement agenda, asserting that most digital assets qualified as securities under existing law. His tenure was marked by high-profile lawsuits, regulatory ambiguity, and a chilling effect on U.S.-based crypto innovation. The Gensler era framed the industry largely through the lens of investor protection and systemic risk. That’s not all bad by the wa,. but they had zero focus in our opinion on innovation, U.S. competitiveness and absolutely no vision of the future.

By contrast, the Trump administration’s appointments of David Sacks as the AI and Crypto Czar and Paul Atkins, who was confirmed as SEC Chair in April 2025, has introduced a dramatic shift in tone, substance and vision. Sacks is an entrepreneur and innovator while Atkins is a known proponent of light-touch regulation and market-driven oversight. Under this regime we expect the following:

The new administration is:

- Prioritizing the development of clear regulatory definitions for digital assets. This is critical as it distinguishes between commodities, securities, and stablecoins – something Gensler refused to address during the Biden administration.

- This can encourage stablecoin innovation, including public-private models for compliance and creating transparency in reserves. Previous administration policies forced stablecoin providers to leave the US and domicile in places that didn’t require as much transparency. This was bad policy in our view.

- This administration is reducing the role of regulation-by-enforcement, instead favoring clear rulemaking and guidance to foster responsible growth.

- Finally – there’s closer coordination between financial agencies like the commodity futures trading commission and the US Treasury such that these agencies can align to a unified digital asset strategy.

In our view, this leadership transition signals a green light for financial institutions, fintechs, and crypto-native firms seeking to operate within clear, predictable rules. It also aligns the U.S. more closely with jurisdictions like the U.K., UAE, and Singapore, which have already implemented forward-leaning crypto frameworks. But importantly, because stablecoins will be backed by the world’s reserve currency, it creates a virtuous dynamic cycle for the USD and treasuries.

This is why Tom Lee calls stablecoins and the recent legislation the “ChatGPT moment for crypto.”

As we enter the second half of 2025, we believe the regulatory bottleneck that once constrained U.S. crypto leadership is finally breaking loose. And our view is this will usher in a new era of digital asset legitimacy, capital formation, and competitive positioning for the dollar.

The Regulatory Evolution: How It’s Shaped Attitudes

Attitudes toward crypto have shifted dramatically. What was once considered fringe is now mainstream. Wall Street is not only buying crypto assets but building infrastructure around them.

The legitimization is not only regulatory – it’s cultural. The listing of crypto firms like Bitmine (BMNR) on the NYSE, as Lee noted, sends a powerful signal that traditional finance sees crypto as credible.

[Here’s Tom Lee’s take on the credibility of crypto and why the NYSE].

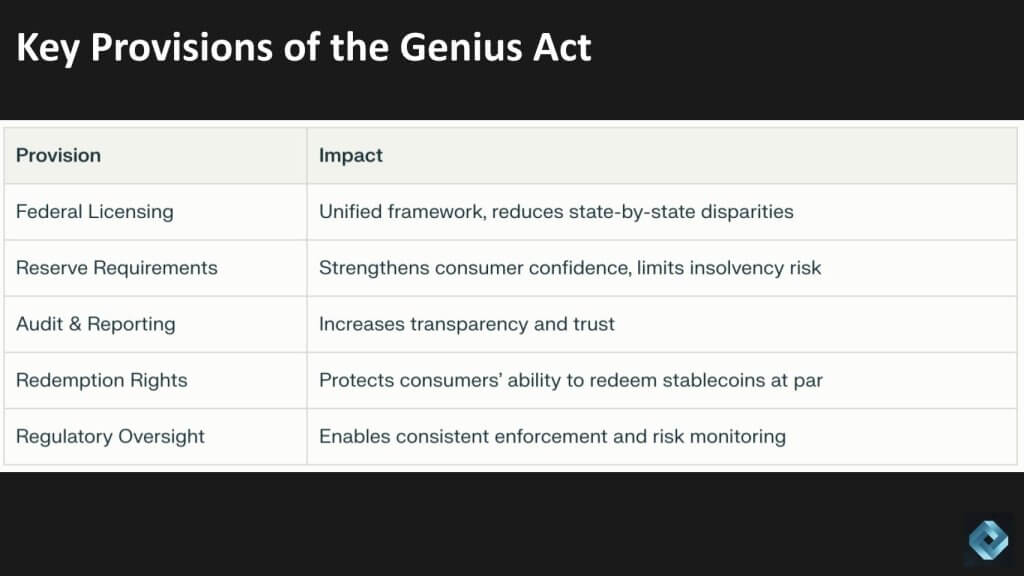

What Is the Genius Act?

The GENIUS Act, which stands for the Guiding and Establishing National Innovation for U.S. Stablecoins Act, is a U.S. law establishing the first comprehensive regulatory framework for stablecoins. It aims to provide clarity and consumer protections within the stablecoin market, fostering innovation and potentially strengthening the U.S. dollar’s position as a reserve currency. The bill was signed into law on July 18, 2025, by President Trump.

Why Is the GENIUS Act Important and what are the key provisions in the act?

This is the First Comprehensive Federal Stablecoin Regulation – The U.S. has operated without a unified national law specifically governing stablecoins, leading to a patchwork of inconsistent state rules. The GENIUS Act aims to provide clarity and uniformity, reducing regulatory uncertainty for issuers, financial institutions, and consumers.

Consumer & Financial System Protections – By imposing reserve requirements and explicit rules for redemptions, the Act ostensibly reduces risks such as issuer insolvency, bank runs, and consumer losses that have been major concerns in the rapidly growing stablecoin market.

Encouraging Responsible Innovation – The Act allows both banks and qualified nonbanks (including technology firms) to issue stablecoins, potentially fostering competition and innovation in digital finance. It seeks to balance growth in the stablecoin sector with safeguards for market integrity. this is somewhat controversial and we’ll address the risks later in this episode.

Addressing Systemic Risk & Market Integrity – Stablecoins are increasingly used in payment systems, remittances, and decentralized finance. The Act addresses systemic risks by ensuring that issuers are subject to ongoing supervision and that the underlying assets are transparent and secure.

What Is the Status of the Clarity Act?

The Clarity for Payment Stablecoins Act (aka the Clarity Act) recently passed out of the House Financial Services Committee with bipartisan support. It defines payment stablecoins and sets reserve requirements, audit standards, and registration routes. This bill is critical because it differentiates stablecoins from securities and provides a lawful on-ramp for banks and fintechs to issue them.

If passed, the Act will likely accelerate institutional adoption and reduce regulatory uncertainty, making it a foundational piece of the crypto policy framework.

The Genius Act and Clarity Acts are different.

GENIUS Act: Focuses narrowly on the regulation of payment stablecoins

CLARITY Act: Provides a broader market structure for digital assets that are not stablecoins (e.g. cryptocurrencies and tokens). The Act seeks to clarify the distinction, regulatory treatment, and supervisory roles for all digital assets that may be classified as commodities, securities, or fall under other regulatory categories.

How Are Stablecoins Backed?

Stablecoins like USDC (issued by Circle) are backed by short-term U.S. Treasuries and cash equivalents. The business model is simple but really powerful. The way it works is issuers collect deposits, invest them in T-bills yielding somewhere around 4-5%, and return none of that interest to holders.

As Tom Lee said in the earlier clip: “Circle doesn’t pay interest and they’re earning 4% on their reserves.”

This has created massive cash flow opportunities, making stablecoins functionally similar to money market funds, but with blockchain-native benefits – i.e. low friction movement of money, no trusted third party required, lower fees and immutability of the blockchain.

What Does This Mean for U.S. Treasuries?

Stablecoins are becoming significant marginal buyers of U.S. Treasuries. As adoption scales, so does demand for T-bills. This supports Treasury market liquidity and extends dollar influence globally, particularly in emerging markets where dollar-pegged stablecoins often outcompete local currencies.

[Listen to Tom Lee explain this dynamic using Bermudian dollars as an example].

In our view, this reinforces U.S. economic sovereignty through digital financial infrastructure and represents an underappreciated geopolitical tailwind.

In short, the passage of the GENIUS Act has major implications for the U.S. Treasury market, primarily because it requires permitted stablecoin issuers to fully back their tokens with high-quality, liquid assets – most notably U.S. Treasuries and cash equivalents. Two things we’d call out in terms of the impact on US Treasuries:

First – this creates Increased Demand for Treasuries:

Stablecoin issuers are now mandated to maintain reserves in cash or short-term U.S. Treasury securities. As the stablecoin market grows (potentially into the trillions of dollars), these issuers will become significant purchasers of Treasuries. JP Morgan analysts have projected that stablecoin issuers could soon be among the largest buyers of Treasury bills, ranking alongside major foreign holders like China and Japan.

Second – this Reinforces Dollar and Treasury Hegemony:

By establishing a robust regulatory framework and making U.S. dollar stablecoins more globally attractive, the law supports the continued centrality of U.S. Treasuries as a global safe asset. This could support the demand for dollars and Treasuries, especially for cross-border payments and international investors seeking regulatory certainty

ETR Data for FinTech

Now let’s tie this into some ETR data on the Fintech sector and we’ll do so with this two dimensional graphic that shows a number of FinTech platforms. Spending velocity on the platform is the Y axis and market penetration or Pervasion is on the X axis.

Let’s just focus in on Stripe’s leadership to make a point.

Stripe’s Strength Signals Institutional Validation for Crypto Rails

This ETR Peer Position chart from July 2025 shows Stripe with the highest Net Score (39.7%) and the broadest shared account footprint (11.5%) among FinTech vendors—well ahead of legacy platforms like Intuit, Fiserv, and Bill.com.

This positioning reinforces a key thesis in today’s Breaking Analysis: the crypto economy is rapidly merging with mainstream FinTech infrastructure, and firms like Stripe are emerging as a primary conduit.

- Stripe’s strong momentum reflects enterprise demand for programmable payments, embedded finance, and crypto-on/off ramps—all of which are foundational to stablecoin adoption and blockchain-based settlement rails.

- Its integration with stablecoin networks (e.g., USDC) aligns with the regulatory thawing and strategic focus we now see under the Trump/Sacks/Atkins regime.

- Stripe’s lead in this data set represents not just tech strength, but early-mover advantage in offering compliant crypto-native services to institutional clients.

In our view, this validates Tom Lee’s assertion that stablecoins are the “ChatGPT moment” for crypto, and that banks and fintechs are now racing to offer Ethereum-based stablecoin solutions – a narrative that Stripe is helping operationalize at scale.

There are Always Risks…So Investor Beware

Ok all that said…Let’s look at some of the risks and criticisms on the other side of this legistlation.

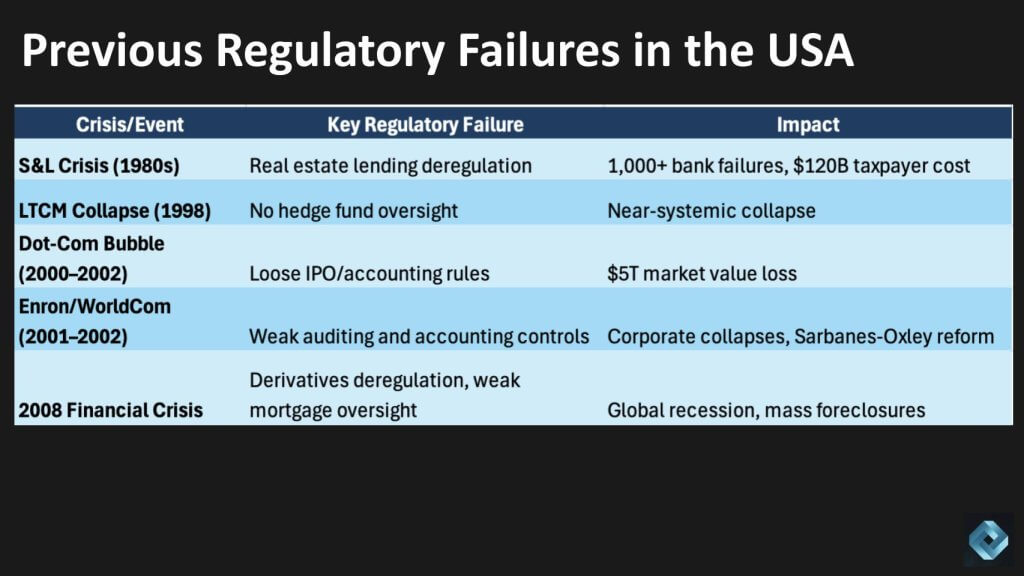

While we’re really bullish on the recent changes in public policy toward crypto, we don’t want to ignore the fact that often relaxed regulation leads to financial meltdowns. Here’s a quick look at some of the disasters or crises over the past 4-5 decades.

The S&L crisis in the 1980s stemmed from the relaxation of real estate lending regulations and put over one thousands banks out of business at a taxpayer cost well over $100B

The Long Term Capital Management collapse in 1998 can be traced back to the lack of hedge fund oversight and when LTCM went rogue the system nearly collapsed.

In order to do an IPO during the Dotcom era you had to have a Web domain and a prospectus – I’m over-simplifying but the accounting rules were lax leading to trillions in lost market value.

Enron and Worldcom essentially had fraudulent accounting and that led to Sarbox.

And the 2008 financial crisis can be traced to deregulation in packaging crappy assets i o derivatives, easy money lending policies that were overlooked by regulators leading to a prolonged global recession.

For what it’s worth, the S&L crisis was pushed by republicans under the Reagan administration. The lack of regulation that led to the Long Term Capital Management and Dotcom meltdowns were bipartisan as was the derivatives deregulation that led to the 2008 financial crisis – approved by republicans in congress and signed by President Clinton – and the weak accounting controls that led to the Enron and Worldcom fraudulent reporting was a W Bush era initiative.

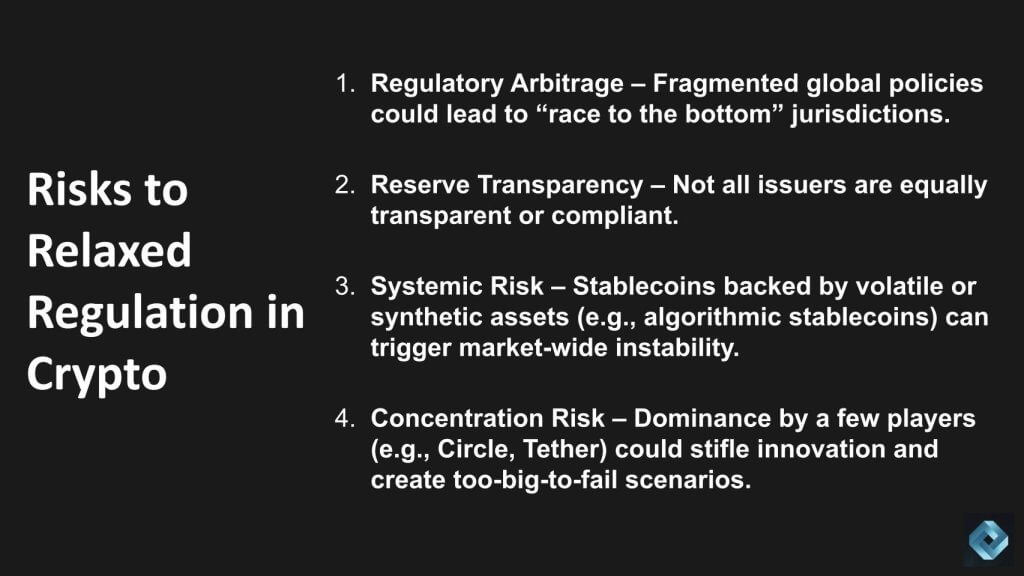

At any rate – Despite the wonderful tailwinds, many feel the stablecoin ecosystem faces substantial risks:

Below we highlight four:

- Regulatory Arbitrage – Fragmented global policies could lead to “race to the bottom” jurisdictions. Regulatory arbitrage happens when companies or investors move their business to countries with the weakest rules, just to avoid stricter oversight elsewhere. Since different countries have different crypto laws, some may offer looser regulations or lower taxes to attract business. This can create a “race to the bottom”, where countries compete by weakening their laws, which can lead to less transparency, more fraud, and higher risks for everyone – uninformed consumers.

- Reserve Transparency – Not all issuers are equally transparent or compliant. There will invariably be bad actors trying to game the system for short term gain that could create domino effects in the economy.

- This is what people mean by Systemic Risk – Stablecoins backed by volatile or synthetic assets (e.g., algorithmic stablecoins) can trigger market-wide instability. Systemic risk means that one failure can cause everything to start breaking down, like dominoes falling. In the case of stablecoins, some are backed by risky or made-up assets, instead of real dollars or safe government bonds. For example, algorithmic stablecoins try to stay stable using computer code and trading tricks – but if those systems fail, the stablecoin can suddenly lose its value. If that happens, it can shake confidence across the entire crypto market, causing prices to crash and other companies to fail—just like how one bad bank can trigger a financial crisis. Remember the Jenga blocks in the movie “The Big Short?” It’s like building the foundation of a skyscraper out of Jenga blocks. It might look stable for a while—but if one piece shifts, the whole building can collapse.

- Then there’s Concentration Risk – If there’s dominance by a few players (e.g., Circle, Tether, JP Morgan) it could stifle innovation and create too-big-to-fail scenarios where taxpayers must bail out the system.

As Tom Lee explained, clear backing is essential. He said to John Furrier:

“As long as people are backing the reserves, there’s no risk… That’s what the model is.” – Tom Lee

As he also noted the irony is that many existing fiat-pegged currencies (like the Bermudian dollar) operate with far less transparency or backing than modern stablecoins. Hence these stablecoins are more stable than many existing currencies.

Closing Thoughts

Despite the risks, in our opinion, stablecoins are no longer the speculative playground of crypto insiders. They are becoming mainstream instruments of economic policy, institutional strategy, and programmable finance. The regulatory fog is lifting and clarity is emerging. As lawmakers, investors, and financial giants converge around stablecoins, we believe this is not merely a trend, it’s an inflection point.

Crypto has had many “moments.” This one feels different. In a tip of the cap to Tom Lee – This one has a yield.