In 1987, Nobel Prize-winning economist Bob Solow famously observed, “You can see the computer age everywhere but in the productivity statistics.” This proclamation became known as the productivity paradox. Ironically, Solow’s statement preceded the greatest productivity boom since the dawn of the computer age which subsequently came to fruition in the 1990’s. It can be argued that a similar pattern is being seen today where AI is everywhere but generally not showing up in earnings numbers or productivity statistics…yet.

In this Breaking Analysis we squint through the latest earnings reports from Microsoft, Alphabet and Amazon to understand what’s happening in cloud, evaluate the impact or lack thereof of AI on cloud earnings momentum and explain how we think about the future impact of generative AI and cloud.

Investor Confusion

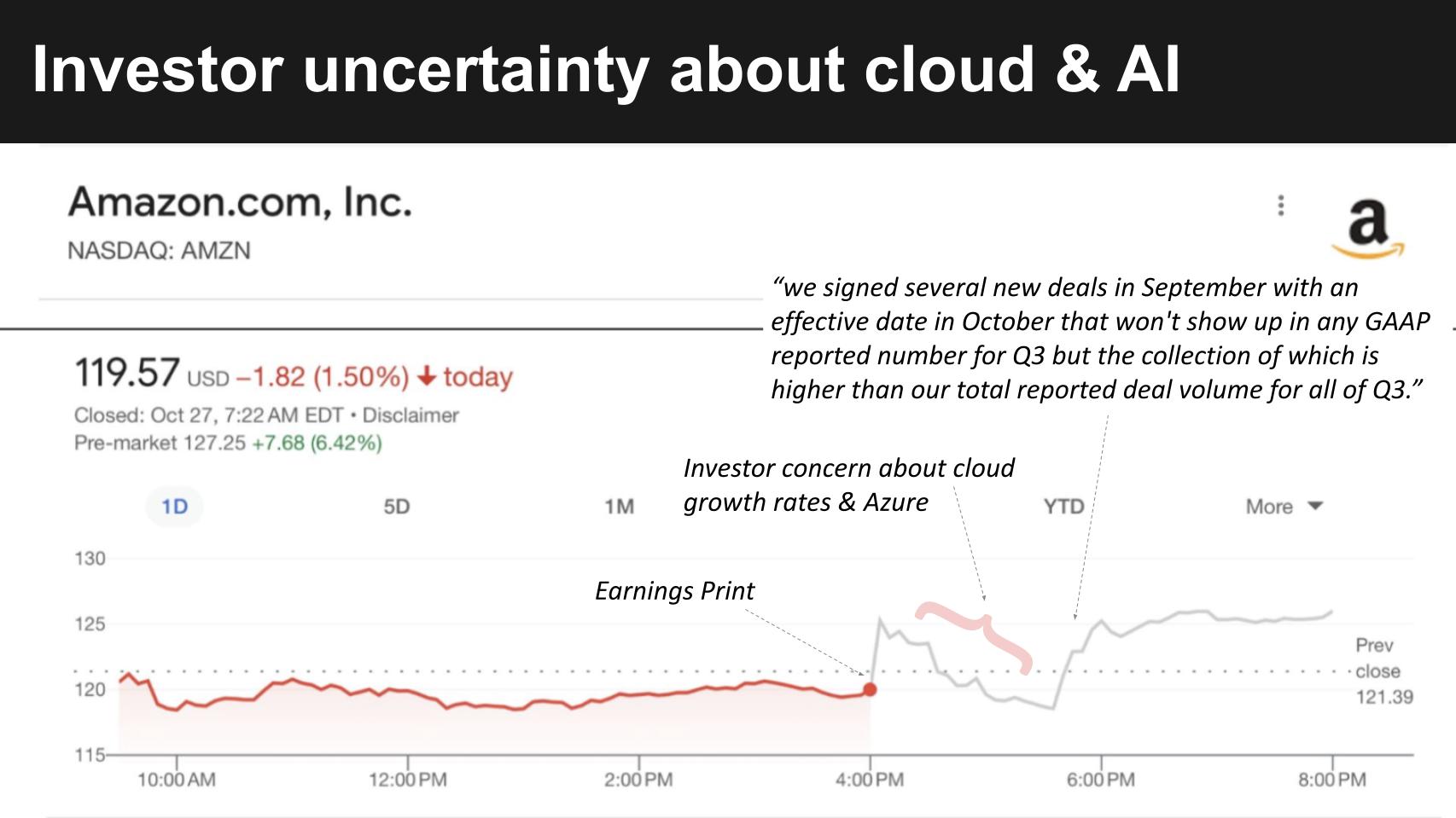

The above chart underscores the mixed reactions from investors. It shows Amazon’s stock price the day it announced after the close (Thursday). The red line is during trading hours prior to its earnings release and after hours is the gray line up through Friday morning before the open. The stock was down 1.5% during the day then Amazon announced earnings. After the print the stock shot up after hours because Amazon beat but then the talking head “experts” on the financial channels started to question the attractiveness of of Amazon as an investment. One analyst on CNBC cited the tepid growth rate of AWS compared to Azure as a negative. He said that he wouldn’t get excited again until AWS was growing in the high teens or even 20% range…and you can see above that narrative dampened enthusiasm after hours.

As an observer of AWS and tech markets this reaction is perplexing. Here’s AWS…a $90B company growing at 12% with 30% operating margins. That’s north of Cisco and, although south of Oracle it’s really fantastic. AWS basically came in on the number and its $7B of operating income only accounted for about ¼ of Amazon’s overall operating profit. Remember we’ve seen that percentage exceed 100% in the past. Not to mention that growth at Microsoft isn’t necessarily a negative for AWS; prompting the following Tweet while on a plane with CNBC in one ear and the earnings call on spotty wifi in the other:

Microsoft is unique with a massive software advantage built up over decades. AWS is nearly the size of Dell with a profit model north of Cisco’s and a bit south or Oracle’s – it’s an incredible business.

— Dave Vellante (@dvellante) October 26, 2023

Now Amazon’s guide for AWS was conservative ok – why wouldn’t it be? There’s no upside in being too aggressive in this market. Then Jassy says on the earnings call:

…we signed several new deals in September with an effective date in October that won’t show up in any GAAP reported number for Q3 but the collection of which is higher than our total reported deal volume for all of Q3.

The expert investor comes back on TV and basically says he may have to rethink his stance on Amazon. And you can see above how the stock reacted during the call shooting back up today and as of midday Friday the stock is up 7% while the Nasdaq is basically unchanged.

Takeaway: We’ve seen many waves over the years and what happens is when there’s a big disruptive trend that everyone knows is coming…it gets hyped up. But the reality is the size of the new is still so small that despite the momentum and growth, it’s just not nearly big enough to blow through any headwinds or other market friction. Of which there is a lot today.

AI Continue to Shift Budgets

Given all the market uncertainty, CEOs are not allocating huge incremental dollars to CIOs for AI. Rather they’re saying figure it out, show some ROI and we’ll invest more.

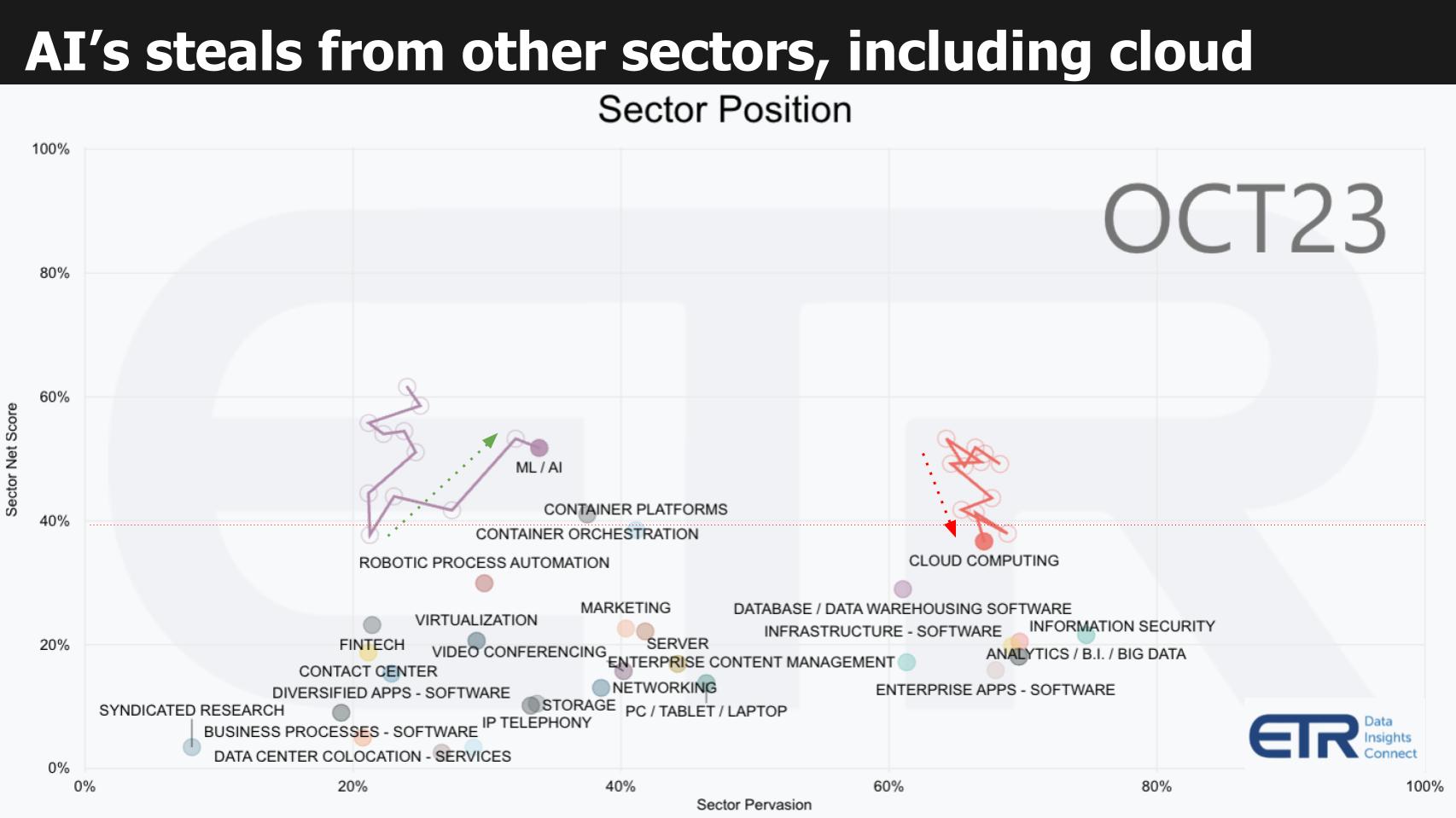

As we’ve said in previous research notes, AI is stealing from other sectors. The chart above from ETR’s latest spending intentions survey shows all the sectors the company tracks. The N in this study is over 1,700 IT decision makers (ITDMs). The Y axis is Net Score or spending velocity in a sector and the X axis is the pervasiveness of the sector in the data set. We show here via the squiggly lines that AI bounced off its low in October 2022, one month before ChatGPT was announced. You can also see the trajectory of cloud computing over the last 10 quarters or so. Shifting budgets plus other factors including cloud optimization and a rebalancing of hybrid portfolios has been taking place for over a year now. Notably, we see very few sectors over that red dotted line at a 40% Net Score– considered a highly elevated indicator of spend momentum.

Takeaway: AI is still experimental today. Showing lots of promise but most activity remains at the evaluation stage. Resources are being allocated but for the most part, they’re not incremental resources. Rather they’re stealing from other buckets.

We Still Live in a Cloud World

The cloud operating model continues to set the agenda for IT. Overall hyperscale cloud growth continues to outpace that of on-prem by 4-5x rate. So let’s take a look at what the market for hyperscale clouds looks like post earnings.

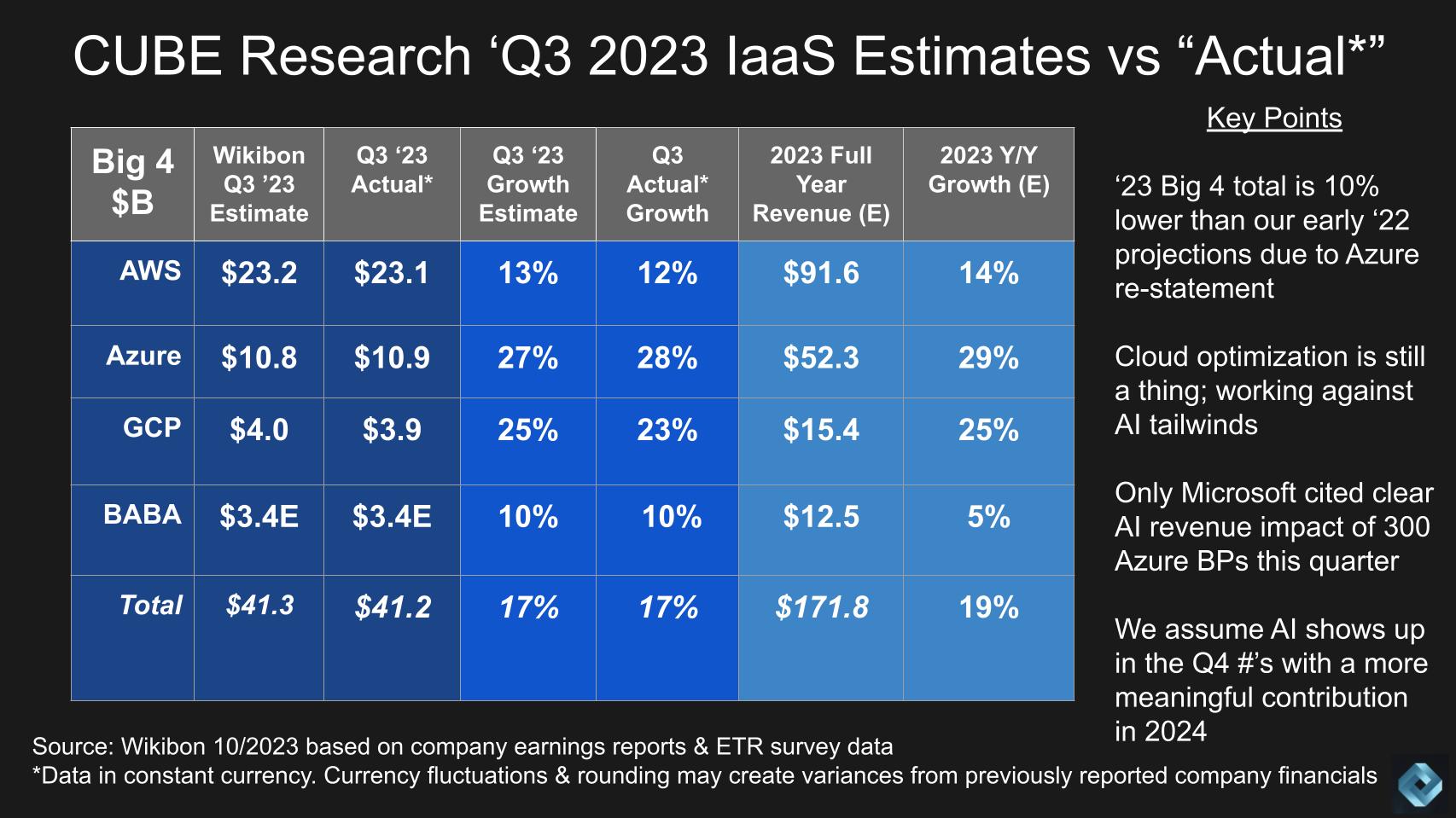

Above we show updated figures for our quarterly IaaS and PaaS forecasts. Remember this is meant to be apples-to-apples with AWS – i.e. we’re stripping out applications, collaboration software and things like Microsoft 365 and Google Workspaces. We consider the big four hyperscalers to be AWS, Azure, Google Cloud and Alibaba. And we’ve been tracking these four for years.

The second column shows our previous Q3 estimates compared to our new actuals based on the latest earnings reports. Alibaba has not reported yet. We then show the growth rates compared to our previous forecast and the latest full year revenue estimates and corresponding growth rates.

The following key points are notable:

- 2023 unfolding as expected. The numbers are pretty much in line with our expectations. However the total for the big 4 of $172B is about 10% lower than our early 2022 projections, due almost entirely to our restatement of Azure revenues based on the poorly redacted court documents during the Microsoft Activision hearings, which mistakenly leaked Azure data.

- Microsoft’s AI lead shows in the numbers. All three U.S. hyperscalers report optimization is still happening in the cloud. AI is not yet showing up on the income statement, except for Microsoft, which indicated about a 300 basis point tailwind for Azure as a result of AI.

- Expect Q4 to show AI acceleration. Our assumptions are that AWS and Google will join Microsoft in Q4 by disclosing a measurable revenue impact from AI. Microsoft will continue to lead and get a boost from its Ignite event. AWS will gain momentum coming out of re:Invent and Google in the spring from its Next conference, which should feature new AI announcements.

Let’s face it. Microsoft is making all the right moves with AI and elsewhere across its portfolio including collaboration, database, security and more. Its performance is remarkable. So it’s somewhat understandable why analysts might be negative on AWS but they’re missing the big picture in our view. Microsoft is a decades old company with a giant software estate, which serves as a captive market for Azure. In other words, because Microsoft runs its own software on Azure it has a unique fly wheel effect that AWS doesn’t possess. AWS competes on the merits of its IaaS and PaaS and the fact that it has the best cloud services. But the point is there’s plenty of room for both so don’t assume Azure’s success is necessarily a negative for AWS.

Having said that, the performance of Azure is astoundingly good. We have it growing nearly 30% this year to AWS’ 14%. The real concern we have is Google. It can be argued that Google has the best tech, the best AI and the resources to invest. But at $4B per quarter in IaaS, its growth rate should be at least double that rate in our opinion. Both AWS and Azure at this same size were growing at rates of 60% plus. Accounting for the fact that Google was late to enterprise cloud and is ramping up in times of much greater uncertainty, they still should be growing faster.

The last point on the chart above is we fully expect accelerated growth in Q4 as a direct result of AI. We have the overall year over year growth rate of 17% this past September quarter accelerating to 21% in the December quarter. With AWS, Azure and GCP growing at 17%, 30% and 25% respectively.

While Azure and GCP are growing faster than AWS, AWS remains the largest IaaS/PaaS player in our models through the next 24 months at least. And we expect to see a re-acceleration of AWS growth.

Which Gen AI are Buyers Deploying?

Microsoft & Google lead, an IBM surprise, AWS & Oracle poised and plenty of “other”

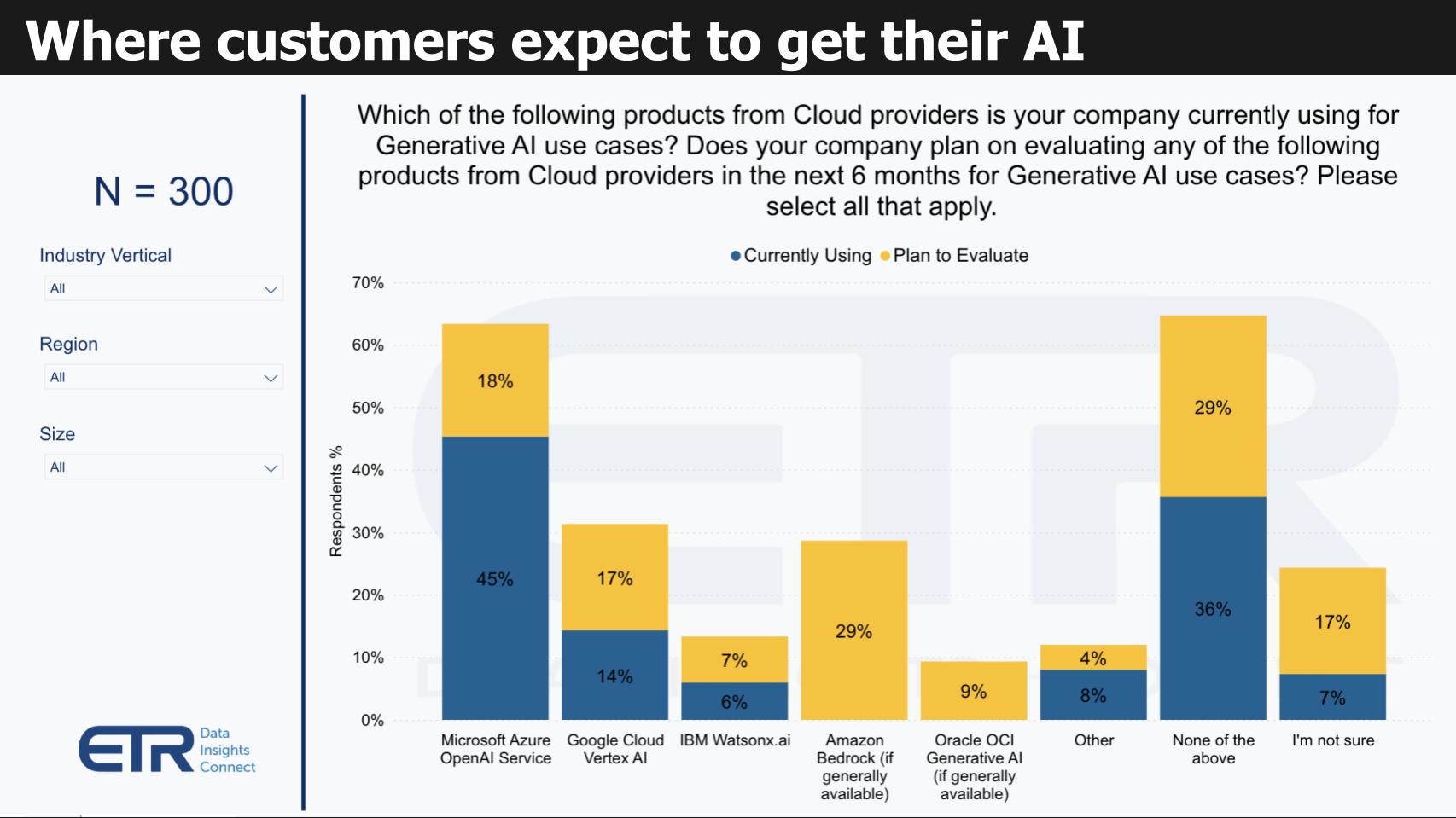

For the first time in the cloud era, AWS is playing catch up. The company is messaging “it’s early days in generative AI.” But AWS has spotted the opponents a lead.

Above is a chart of 300 respondents from a recent ETR drilldown that asks which products from the cloud providers are currently in use (the blue bars) and are planned for evaluation (the yellow). Microsoft is winning right now, there’s little question. Google with VertexAI combined with BigQuery has a very strong data story – despite the fact that it’s not showing up in the numbers yet. And interest in Amazon is quite high. Note the parenthetical (if generally available). Amazon Bedrock went GA this month and with re:Invent around the corner, one would have to believe that AWS will have the last word this year on Gen AI and it will be a strong one.

Several points stand out:

- Amazon trips at the start. Amazon is not used to playing from behind. They’ve always led in cloud and for the first time, they’re giving a head start to the opposition. Everyone was caught off guard with the GPT heard ‘round the world – the uptake surprised even Microsoft and OpenAI. AWS has always had ML/AI momentum with SageMaker. But it was caught flat footed this time so let’s see how they play from behind.

- Google’s response was swift. Google called a “code red” and quickly responded as a recognized AI leader; notwithstanding it hasn’t yet helped its cloud business in a measurable way.

- IBM shows promise; Oracle in the game. The other call-out on the chart is IBM watsonx. Both IBM and Oracle are in the game and IBM seems to be further along based on customer input.

- “Other” presents third party & open-source options. There are plenty of other open-source and third-party options also in the race, including OpenAI itself, Anthropic, Meta, Cohere, Falcon, Jasper and many others.

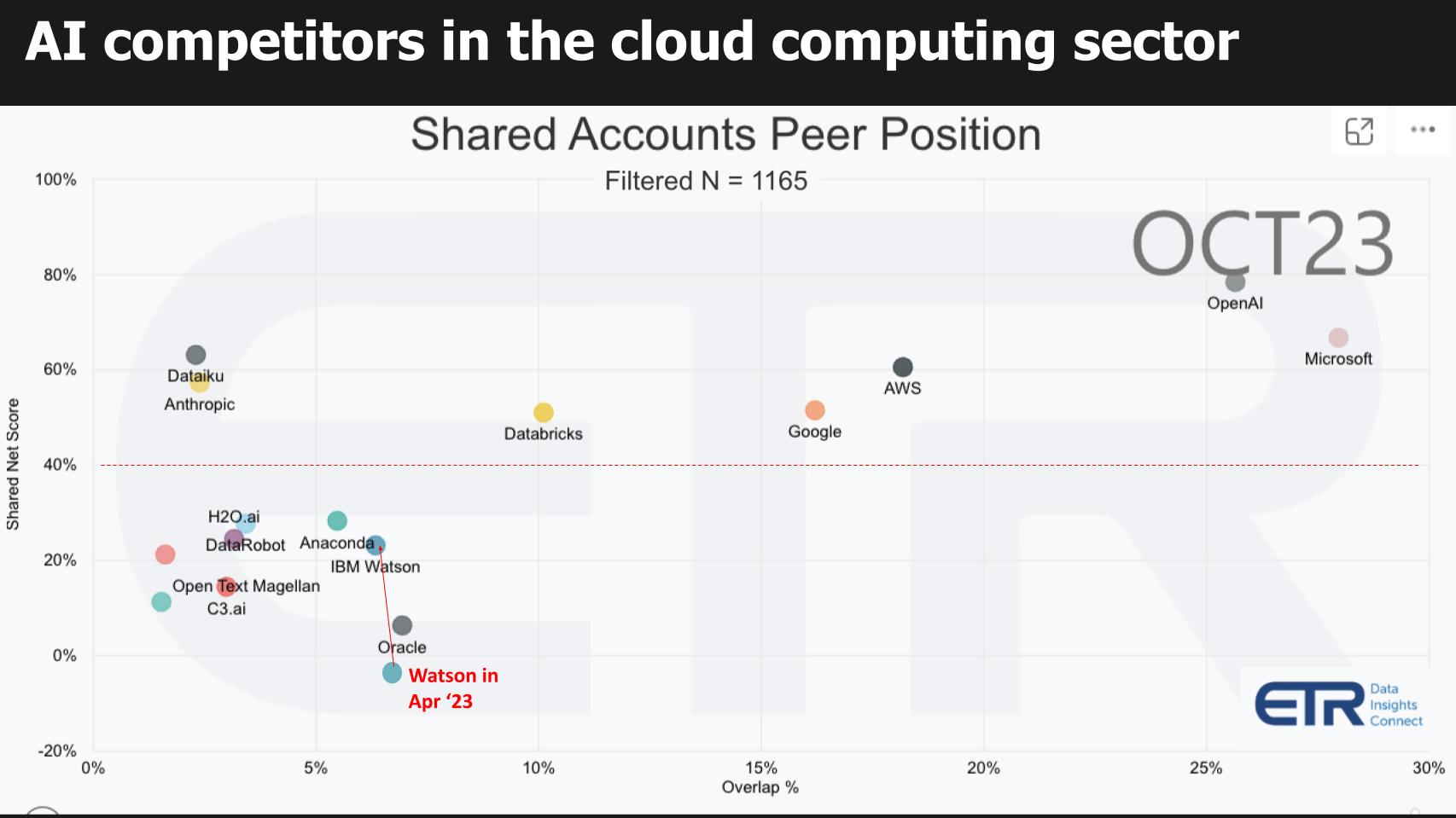

Cloud Leaders Poised for AI Growth

IBM shows promise with watsonx

The YX graphic below shows Net Score or spending velocity on the vertical axis and presence in the sector on the X axis. This data filters on 1,165 cloud computing accounts in the ETR data set. It then cuts the data by ML/AI platforms that buyers are deploying. The red dotted line at 40% indicates a highly elevated spending velocity on a platform.

OpenAI has shot to the lead and Microsoft’s bold strategy have put these two firms in a prominent position. They’re crushing it relative to the rest of the crowd. It’s notable how AWS and Google have come more closely aligned when you cut the data on cloud and AI. Normally AWS would be much closer to Microsoft than to Google but not when the data is filtered on AI. Now as a caution, remember Microsoft is so large and ubiquitous it skews the data to their favor because of the massive software estate it has. But nonetheless AWS clearly has some work to do despite the fact that it’s well above the 40% Net Score mark.

Our strong bet is that AWS will see accelerated momentum coming out of re:Invent. Just as Google saw coming off Next and IBM off Think. AWS could be sitting pretty next year.

We also want to point out Anthropic which is not as prominent on the X axis but clearly is showing market momentum. Everyone seems to be working with Anthropic, including Google’s recent announcement to invest and partner with the company. And you may recall in the previous chart the “other” category of AI players being adopted or evaluated was meaningful. So as we’ve been saying with our Gen AI Power Law research the tail in AI will be long.

IBM’s reset with watsonx & an unfair consulting advantage

IBM for years was marketing Watson hard with unimpressive results. But watsonx from a product standpoint is looking good. Watsonx supports open data formats and has strong metadata management. It supports many data types, multiple database and query engines and has a decent data sharing story.

Look at IBM Watson in the above chart. While it’s still well below the magic 40% red line, look at where it was in ETR’s April survey of this year. IBM announced watsonx in May at its Think conference and is showing momentum. Arvind Krishna’s hybrid cloud narrative has expanded to include generative AI and IBM has an unfair advantage with its consulting business.

What do we mean by this? When IBM bought Red Hat we said this was really a consulting and services play. Or at least that was why the deal made economic sense because IBM’s services business de-risked the acquisition. Why? Because IBM’s strong consulting business allows it to have a captive market for its software and other products. Provided that watsonx is competitive – and by our initial assessment it appears to be so – it should do well in market. After years of torturing us with Watson mumbo jumbo bolstered by great advertising – IBM, we believe, got it right this time around.

Cloud Meets AI and the Promise of Productivity

Cloud optimization continues but it is a feature not a bug. It drives lifetime customer value, it increases net revenue retention rates and minimizes churn. This in turn keeps customer acquisition costs management and can drive attractive LTV/CAC ratios above 4X.

Cloud growth is playing out as expected from our early ‘23 forecast. With the exception of the re-statement of Azure, we’ve been pretty much dead on. Certainly at the total market level – perhaps a bit too optimistic with Google. But Microsoft has made up for that.

Cloud growth continues to dramatically outpace overall IT spending rates. 19% growth on a $170B market is pretty impressive while on-prem growth hovers in the mid single digits. How generative AI will affect these growth rates remains to be seen but in general we see a rising tide lifting most ships.

Foundation models like GPT shift the economic equation and drive cloud demand: Silicon→LLM APIs→Apps which drive compute, storage and other infrastructure. Importantly, it must also drive productivity and address rising labor costs or enterprises will become more cautious in our view.

But on balance, we expect an acceleration in Q4 cloud growth, driven by Gen AI and into 2024 with the obvious macro caveats that we’ll be watching.

Keep in Touch

Thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.