CIOs and IT execs report strong RPA adoption plans in a post-pandemic environment.

We’ve been reporting that the COVID pandemic has created a bifurcated IT spending outlook. Legacy on-prem infrastructure and traditional software licensing models are giving way to approaches that enable more flexibility and business agility. Automation initiatives that reduce human labor that is not value add has been gaining traction for the past 18 months. The pandemic has accelerated the focus on such efforts and robotic process automation (RPA) along with machine intelligence have been beneficiaries relative to other segments of the IT stack.

In this Breaking Analysis we’ll update you on the latest demand picture for the red hot RPA sector. We want to focus on two main areas:

- We’ll briefly review the basics of the RPA space for those that may not be as familiar with the market.

- Next we’ll share the spending data and outlook in the RPA space. We’ll dig into the COVID impact on the space and the competitive outlook with particular attention to the leaders in the space.

RPA 101

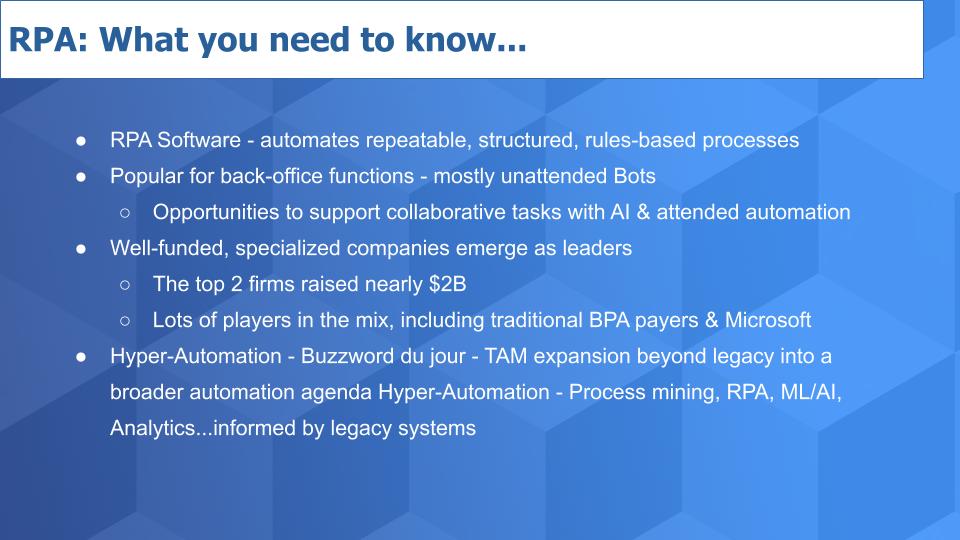

Here’s what you need to know about RPA. It gained traction by taking software robots and pointing them at existing applications to mimic human / keyboard interactions and automate repeatable and well understood processes. A challenge with early RPA implementations is that most customers chose to point these bots at legacy back office systems to open emails and fill in forms and the like…which digitizes processes around legacy systems–great.

But the problem is that these bots interact with the user interface of the application and many of these apps have no API. So any change in data or the interface causes the automation to break down. More recently automations are interacting to apps through APIs which makes them less brittle but of course the quality of the APIs will vary.

Enter Machine Intelligence

There’s been lots of discussion around the intersection of RPA and AI. And that’s allowed organizations to automate more processes and do so in a way that takes an augmentation approach – using natural language processing, speech recognition and machine learning to iterate and improve automations. This trend holds much promise, particularly in the form of trying to understand which processes to automate and where the best ROI can be achieved. But it’s still early days.

Nonetheless – investors have piled into this space as we’ve been reporting for some time now. UiPath and Automation Anywhere have raised close to $2B dollars and have both been growing rapidly. Existing players like Blue Prism have benefited from the automation trend and legacy business process players like Pegasystems, who started in the early 80’s, has added RPA to its platform. As have many others, including Microsoft, who has been trying to crack into this market for a while.

In fact Microsoft just bought a small company called Softomotive to try and up its game. But in our view Microsoft is far behind the leaders and it will take years for them to get to where the leaders are today. But it’s Microsoft so we know not to ignore them.

Hyper-Buzz

The big buzzword du jour is hyper-automation. UiPath has picked up on it big time and so has Automation Anywhere, each with their own hyper-automation Web page. Those companies are in hyper growth so it plays well. More established companies – for example Pegasystems – look at the term differently. Not surprisingly, RPA is only a small piece of its vision. More established firms want to incorporate their business process automations built over decades into a system view of the organization using existing platforms. The upstarts of course want to build from their platforms.

What’s happening, like in most polarized market situations, is a hybrid emergence. We saw this in mainframes coexisting with client/server, traditional data warehouses fitting into Big Data initiatives and we’re seeing it play out in cloud with multi- and hybrid-cloud. Most companies don’t throw away the investments they’ve made in legacy systems – they’re stable and are operationalized. Rather they overlay the more modern technologies and create abstraction layers for their business that incorporate both old and new.

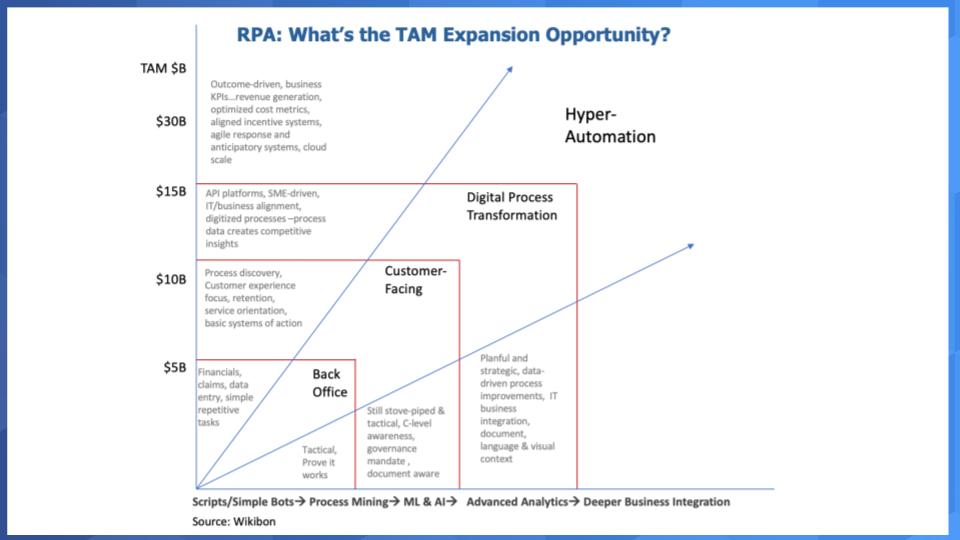

But the growth is much much higher in new and that leads us to the total available market (TAM) conversation.

The RPA Market Potential

We think the TAM expansion opportunity for RPA is substantial. We put together the chart below that underscores the progression of RPA from simple bots automating back office functions to infusing automations and AI in all applications. If you expand the definition beyond RPA software into the broader automation opportunities, this market could be much larger than depicted here – perhaps well over $100B opportunity as AI powered automation becomes a fundamental part of of every organization’s operating model.

It’s a big opportunity and the data suggests that it’s growing rapidly.

So let’s look at the spending action and bring ETR survey data into the mix.

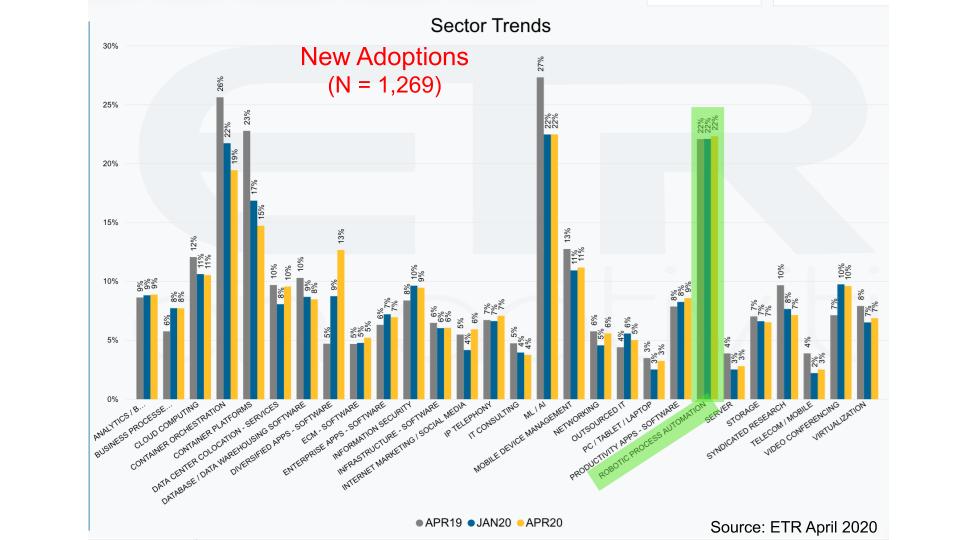

Which Technologies Show new Adoptions?

On balance, the tech sector has done quite well despite this pandemic. At the time of this post, the Nasdaq composite is up about 1.5% year-to-date. And we know from previous surveys that heading into 2020, there was a pullback and narrowing of new technology adoptions as organizations began to operationalize their digital initiatives.

The chart above shows the new adoptions across three survey dates – the gray is April last year, the blue is January 2020 (pre- pandemic) and the yellow is the latest survey of more than 1,200 IT buyers. Remember this survey took place at the height of the COVID-19 lockdown. And you can see RPA with 22% new adoptions – meaning 22% of customers planning RPA spend are newly adopting RPA. That’s a figure as high as machine learning and AI. And of course as we’ve said these two technologies are increasingly playing together.

The data show RPA adoptions higher than containers, greater than video conferencing (despite the work from home trend), more than cloud and more than mobile device management.

New Entrants are Creating Market Momentum

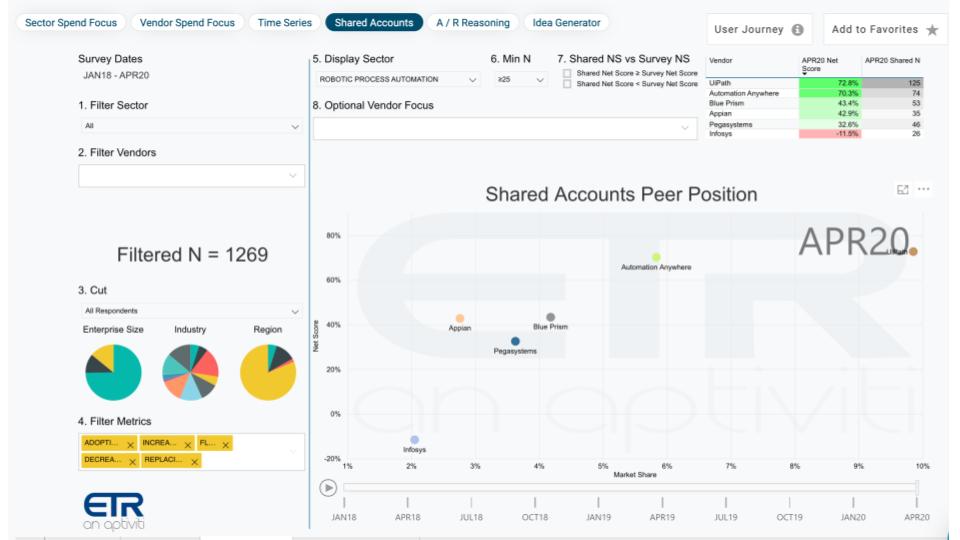

The chart below uses the two primary ETR metrics that we’ve been sharing over the past year. Net Score or spending momentum is on the Y Axis and Market Share – which is a measure of pervasiveness in the survey on the X Axis.

The chart plots the RPA players in the ETR data set and you can see UiPath in the far upper right in the brown dot and Automation Anywhere in the green. They are the two market leaders and both show strong spending momentum and market awareness. Then you see Blue Prism and Pega and the rest of the pack. We will say this about Pegasystems – after speaking recently with company CEO Alan Trefler, an amazing, self made billionaire with a great business. Pegasystems is not an RPA play. RPA is only a part of their story. But they show up in the ETR data set and certainly are automation related, so we think it’s worth showing. However, it’s a bit of an oranges and tangerines dynamic.

In the upper right of this chart you can see the Net Scores in the mostly green shaded area. Remember Net Score is a simple metric like net promoter score (NPS). It essentially subtracts customers spending less from those spending more and nets the difference. You can see the very strong Net Scores for both UiPath and Automation Anywhere, which we discuss below in detail.

The point is there’s lots of green on the chart and even Pega who is not considered an RPA specialist has a solid Net Score.

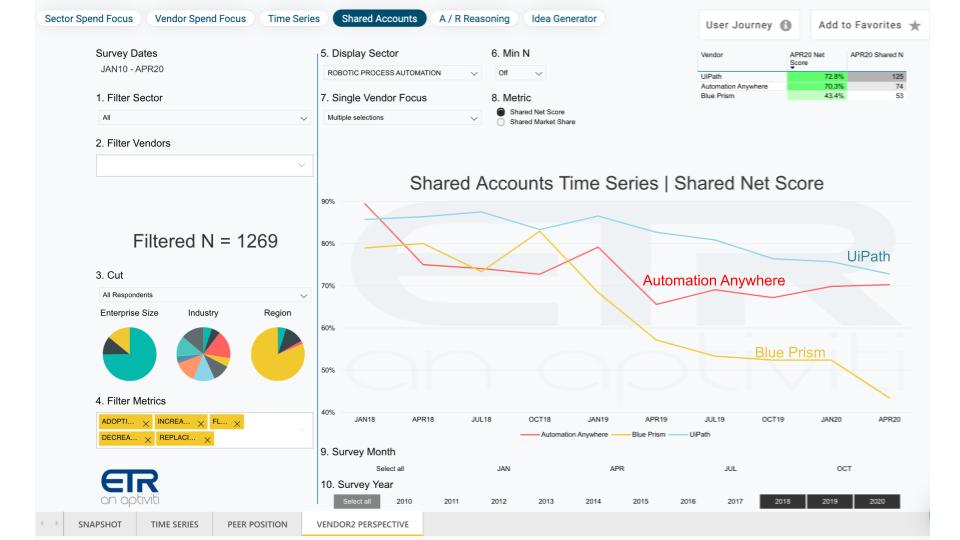

Spending Momentum has Been Steady over Time

This chart takes the three leaders, UiPath, Automation Anywhere and Blue Prism and plots their Net Scores over time – back to the Jan 2018 survey.

There are three points of relevance, including the following:

- UiPath and Automation Anywhere, at a 70%+ Net Score each, is very impressive and amongst the highest in the data set across all sectors. There is some loss of momentum in the UiPath line and a convergence with Automation Anywhere but they’re both very strong. And in the upper right you can also see the Shared N – which is an indicator of the presence of the company in the data set.

- You might be thinking– but UiPath had layoffs last fall and Automation Anywhere more recently how can they show such strength? First, fast growing companies that have raised nearly a billion dollars each have investors they serve and they will course correct when they need to – to us, it’s not a sign of fundamental trouble. Second – both of these companies will continue to invest heavily on research and development. UiPath has 60 openings on its Web site, most in engineering. Automation Anywhere has only 9 openings but we would expect both companies to up their engineering hiring given the Microsoft acquisition today.

- Finally, remember this is not an indicator of amount of spend in absolute dollars, rather it looks at spend momentum of all respondents. As well if you were to cut the data by larger companies – say the F1000 where the average contract values are higher, you would see UiPath’s Net Score jump to 77% and AA would drop into the 60s and Blue Prism would stay about level.

We know UiPath report annual recurring revenue of $360M last year and we also know the company continues to grow. We suspect somewhat faster than Automation Anywhere but the company does not share its ARR data publicly. In February we published estimates for the RPA vendors and pegged Automation Anywhere at $250M.

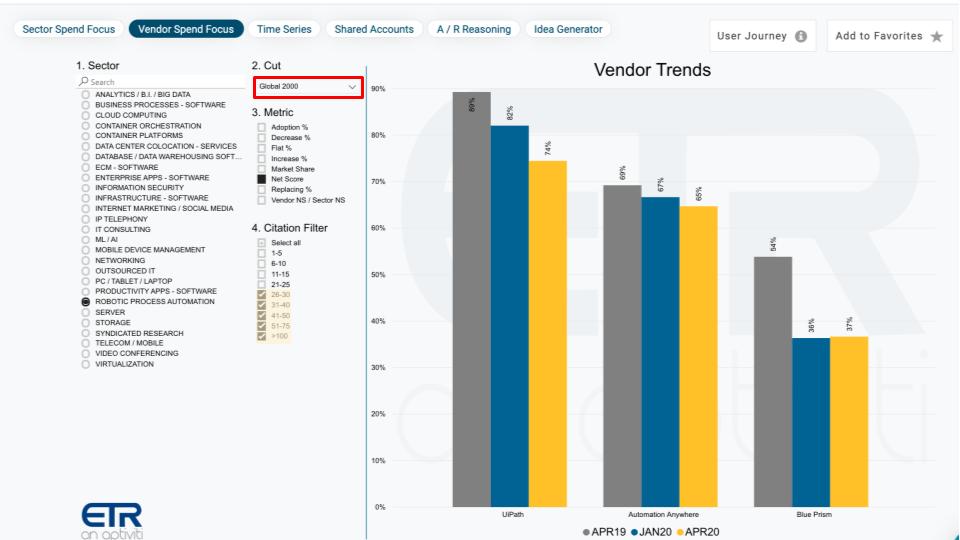

Spending Momentum in the Global 2000

If we expand the data slice from F1000 to G2000 where the N is larger, you see the picture changes somewhat from the overall data sample.

The chart above shows Net Scores in the Global 2000 where Ns are greater than 25 responses across all three companies. The gray bar is last April, blue is the January survey and Yellow is April 2020. And you can see the year-on-year decline and the modest step down in the COVID lockdown survey in April. But the Net Score levels are still elevated to 65% and 74% respectively for UiPath and Automation Anywhere. And Blue Prism at 37% is still. The point is COVID has not crushed the RPA market. If anything, as witnessed by new adoptions, its better off than most sectors in IT.

Comparing UiPath and Automation Anywhere

Net Score is a very important metric and we want to spend a moment explaining how it can be most effectively utilized.

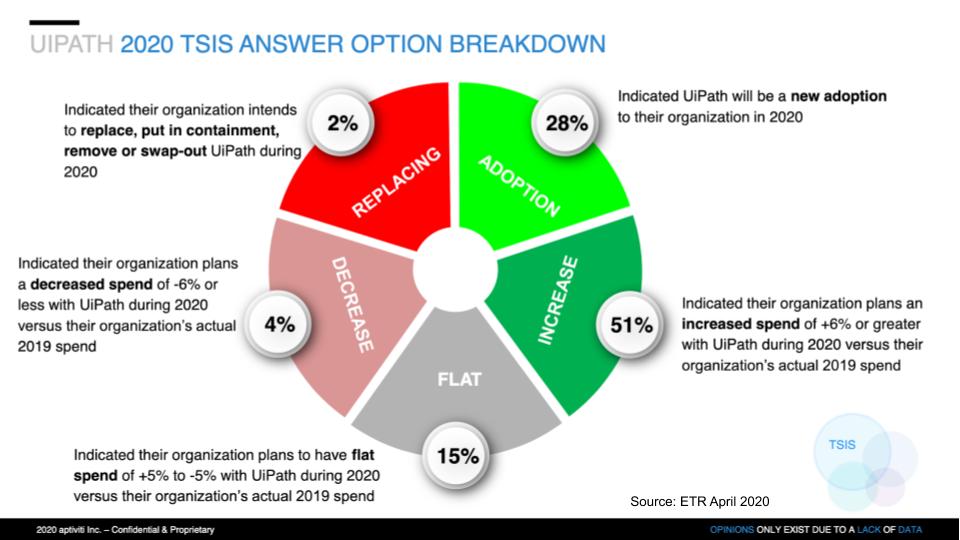

The “wheel chart” below shows the Net Score method applied to UiPath from the April Survey.

Net Score works by asking buyers – relative to last year – are you adopting new (28%), increasing spend by 6 percent or more (51%), expecting flat spending (i.e. within +/- 5% – that’s 15% in the UiPath sample), planning to decrease spending by 6% or more (4% above); or are you replacing the vendor (2%).

You can see for UiPath, 79% of respondents (sum of the green) expect to increase spending in 2020 relative to 2019. Remember this survey was taken at the height of the COVID lockdown.

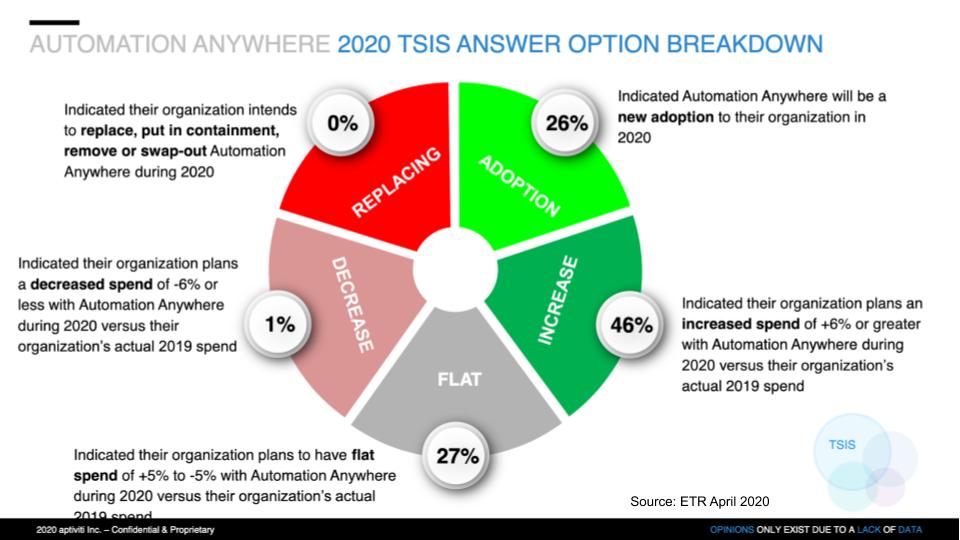

Spending Profile for Automation Anywhere

Now let’s look at the data for Automation Anywhere.

Using the same methodology as described earlier, you can see that 72% of Automation Anywhere customers plan to spend more in 2020 relative to last year. Only 1% plan to spend less with zero replacements. So we see very strong fundamentals as it relates to spending momentum for both UiPath and Automation Anywhere.

How is Pervasiveness – AKA Market Share” Changing?

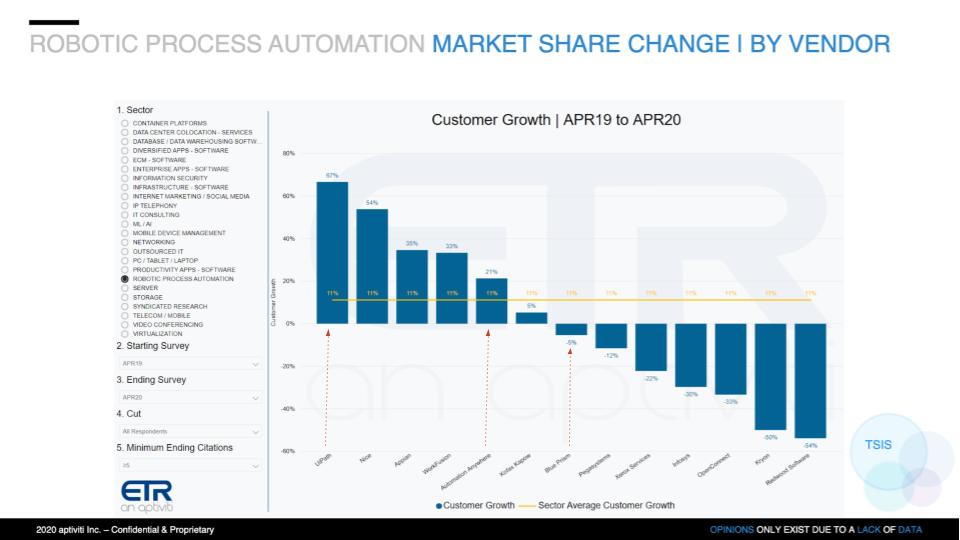

The last data point we will show relates to the metric of Market Share. Again, this is a measure of pervasiveness in the data set. It is calculated by dividing the number of mentions of a vendor in a sector by the total mentions of the sector – in this case RPA.

The chart above shows the year-on-year change in customer growth comparing Market Share from the April ’20 survey with the April ’19 data. The yellow line at 11% is the RPA sector average. UiPath has had the fastest share growth at 67%, Automation Anywhere is growing faster than the market at 21% and Blue Prism is below the average, at -5% share growth.

Now remember, this looks back to last year and it will be interesting to see how this picture changes with the next survey based on the earlier Net Scores we analyzed.

RPA on the Positive Side of Bifurcation

We’re seeing that the bifurcated market highlights automation as a trend that is real, and the RPA sector specifically shows us an example in action.

We think that had COVID not hit, the RPA numbers would actually be higher by as much as 10 percent. But in the near-to-mid-term we would expect a pretty fast return to a “normal” pattern of demand for RPA. In fact while we don’t expect a V-Shaped recovery across the board, RPA is one area where we may see such a rebound. The pandemic underscores the need to accelerate digital transformations. RPA we think will be a central player in that movie along with AI and cloud.

Stay in Touch

Remember these episodes are all available as podcasts wherever you listen. – just search Breaking Analysis Podcast and please subscribe to the series. Check out ETR’s Web site. We also publish a full report every week here and on SiliconANGLE.

Ways to get in touch: Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Stay safe and we’ll see you next time.

Watch this week’s full video analysis: