Azure cloud is the linchpin of Microsoft’s go forward innovation strategy.

As we reported last week, we believe that in the next decade, changes in public policy will restrict the way in which big Internet companies are able to appropriate user data. Big tech came under fire again this week with the CEOs of Facebook, Twitter and Google going toe to toe with several U.S. Senators. Microsoft CEO Satya Nadella, however, was not one of those CEOs in the firing line. Unlike Google, Microsoft does not heavily rely on ad revenues. Rather the company’s momentum is steadily building around Azure cloud which by my estimates is now 19% of Microsoft’s overall revenues, surpassing $7B for the first time.

In this Breaking Analysis we will respond to the many requests we’ve had to dig into the business of Microsoft and provide a snapshot of how the company is faring in the ETR data set.

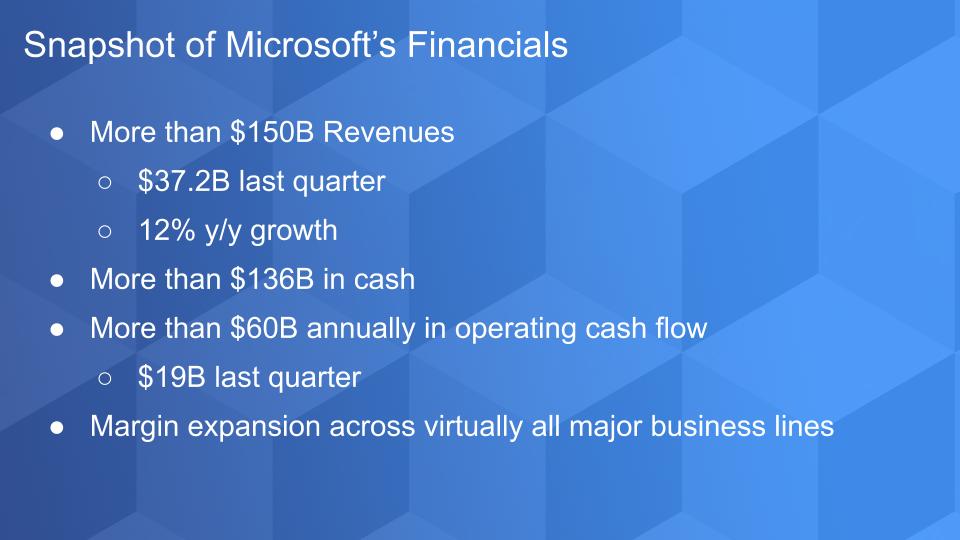

A Snapshot of Microsoft’s Financials

The scope of Microsoft’s business is mind boggling. The company has roughly $150B in revenue and grew its top line 12% last quarter. It has more than $136B in cash on the balance sheet. It generates more than $60B annually in operating cash and last quarter alone threw off more than $19B in operating cash flow. Its gross margins are expanding across all of its major business lines.

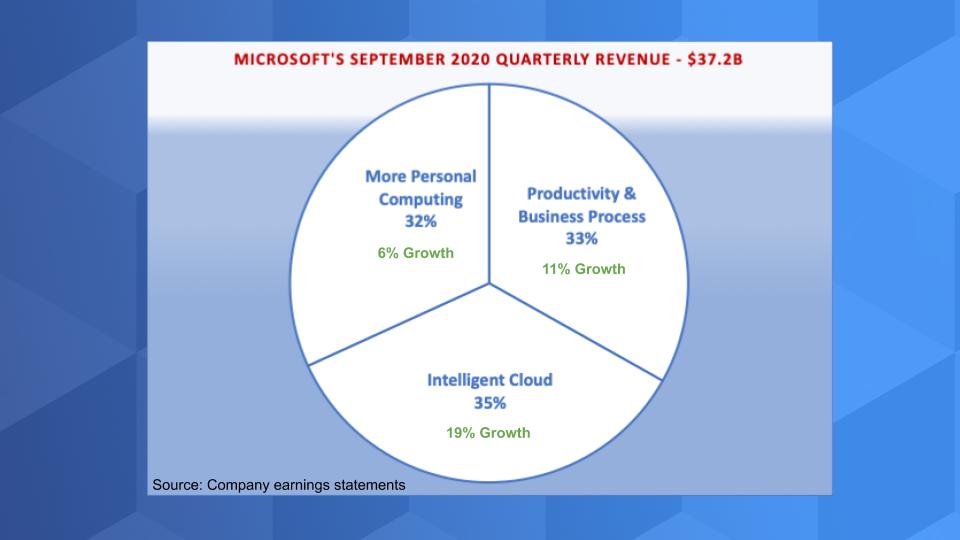

Microsoft’s Big Three Segments

Microsoft doesn’t suffer from the nagging problem that many older tech companies face. Companies like IBM, Dell, Cisco, Oracle and SAP struggle with growth because their growth businesses are not yet large enough to offset the declines in their traditional on-premises segments.

At the highest level Microsoft breaks its business into three broad categories and they’re all growing quite nicely.

Productivity and Business Process

LinkedIn, which is growing at 16%, is in this category as is Office. This business is shifting from on-prem licenses to the cloud in the form of SaaS with Office 365 which is growing at a 20% clip in commercial markets. Even the consumer side of Office 365 is growing in the double digits. Dynamics, Microsoft’s ERP and CRM business falls in this slice of the pie and is growing at 18%. The newer Dynamics 365 is growing at 37%. So as you can see, Microsoft is easily able to show growth despite the transitions from its legacy businesses.

Intelligent Cloud

Intelligent Cloud is what we call Microsoft’s cloud “kitchen sink” category – meaning there’s stuff in there that’s includes a bit of cloud washing.

But Microsoft is not nearly as egregious as IBM in the liberties that it takes with its cloud categorization. This is a $13B quarterly business for Microsoft and it’s growing at 19% as we show in the pie chart. Azure cloud is an increasingly large portion of this segment. Azure is the most direct comparison with AWS and our estimates are that this past quarter, Azure accounted for around 50% of the Intelligent Cloud segment…approaching $7B per quarter. Azure cloud revenue grew at 47% annually this quarter, the same growth rate as last quarter.

Ironically, both AWS and Google Cloud grew at the same year over year rate this quarter as last quarter. AWS 29% and GCP in the high 50’s by our preliminary estimates. AWS revenue was $11.6B this past quarter and we have GCP still well under $2B per quarter. We’ll be updating our cloud numbers and digging deeper next week so consider these estimates preliminary for Azure cloud and GCP, which the respective companies don’t break out explicitly for the street.

Back to Microsoft’s Intelligent Cloud business. It also includes on-prem server software which is a managed decline business for Microsoft and is one of the reasons we refer to this category as somewhat cloud washing. Microsoft also includes enterprise services in this category so as you can see it’s not a clean cloud number for comparison purposes.

More Personal Computing (MPC)

Yes, we think this is kind of a dorky name. But nonetheless it’s a nearly $12B business that’s growing at 6% annually. The Windows OEM business is in here as is Windows 10 and some security offerings. Surface is in this category as well and that popular line of laptops/tablets is growing in the mid 30’s. Search revenue is in here as well and it’s declining per our earlier statements that it’s not a main piece Microsoft’s business.

Gaming

Gaming is also in MPC and is one of the most interesting areas of this sector. Microsoft’s gaming business is growing at 21% and the company just acquired ZeniMax Media for $7.5B.

The gamers at theCUBE are really excited about Microsoft’s Xbox content services, which grew at 30% this past quarter. Game Pass is basically Microsoft’s Netflix or Spotify. You can get in for $5 per month and pay up to as much as $15/month and get access to a huge catalog of games that you can download. In November of last year Microsoft launched its xCloud beta which allows users to download to a PC or a game box. Now eventually, with 5G, the box goes away. All you’ll need is a screen and a controller – no download. In fact, this is how it works today for Android.

Similar to what happened with Epic Games, Apple is blocking Microsoft and some others (e.g. Google’s Stadia) saying it doesn’t allow streaming game apps like Microsoft’s xCloud service because these services don’t follow Apple’s guidelines.

What Apple is not telling you is that its adjacent offering, Apple Arcade, is considered subpar by many hardcore gamers, although Apple does have a loyal following. But while Apple allows the streaming of movies and music from any service on iPhone, it doesn’t currently allow streaming games from competitors.

Developers, Developers, Developers

Last thing we want to stress about Microsoft is its leverage point around developers. Developers is a big one. We all remember a sweaty and semi-maniacal Steve Ballmer running around the stage like a mad man screaming “developers developers developers,” cajoling the audience to synchronize with his clapping. Well, despite his obsession with Windows he sure got that one right. The GitHub acquisition was Microsoft’s way of buying more developer love. It concentrates power with a tech giant but if it wasn’t Microsoft it would have been Facebook or Amazon or Google. Despite some angst in the developer community, GitHub is a lever for Microsoft to more tightly integrate GitHub with its tool set.

Despite its Size, Microsoft’s Spending Momentum Impresses

We said last week that Google needed to look to the cloud and edge and get its head out of its Ads. Well Microsoft recovered from its Windows myopia after Satya Nadella took over in 2014 and by all accounts from the ETR survey data, Microsoft is killing it across the board.

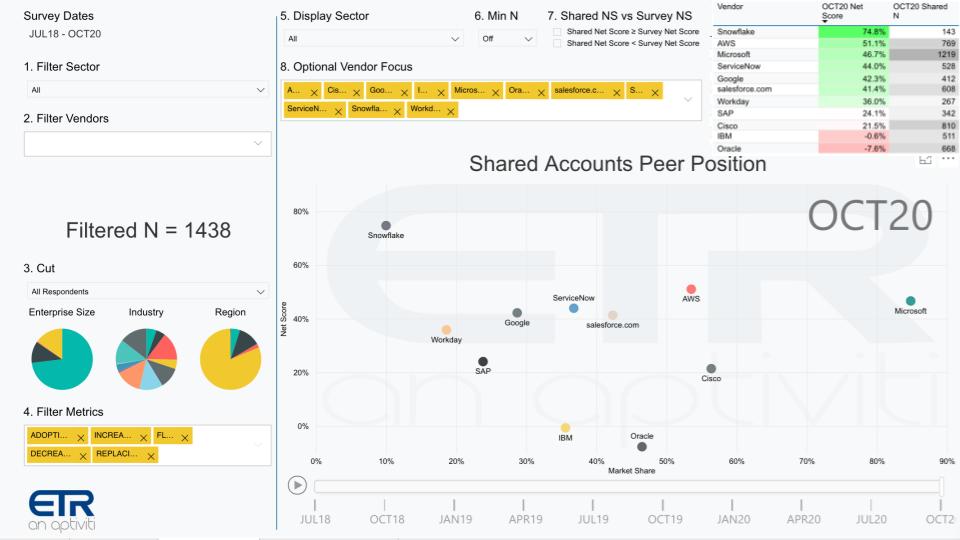

The chart above puts Microsoft in context with some of the most prominent companies that both compete and partner with Microsoft.

This XY graph shows Net Score on the vertical axis, which is a measure of spending momentum, and the horizontal axis shows Market Share, which is a measure of pervasiveness in the survey. In the upper right table you can see the data for each company. This is an ETR survey taken in October with more than 1,400 completes.

Three points stand out:

- Microsoft is by far the most pervasive.

- And yet its Net Score or spending velocity is right there with AWS, ServiceNow, Salesforce, Workday and Google.

- Only Snowflake, which we included for context because of its strong Net Score, shows a meaningfully higher Net Score – but from a much smaller base.

What makes this so impressive is it represents a pan-Microsoft view across its entire portfolio. And you can see where companies like IBM and Oracle struggle from a momentum standpoint compared to Microsoft, a much larger company. It’s that problem we referred to earlier regarding the smaller size of their respective growth businesses.

We’d also call out Cisco and SAP, which despite some earnings challenges recently, are able to maintain Net Scores that, while not in the green, aren’t in the red either. Green essentially means your overall installed base is expanding. Red indicates a contraction.

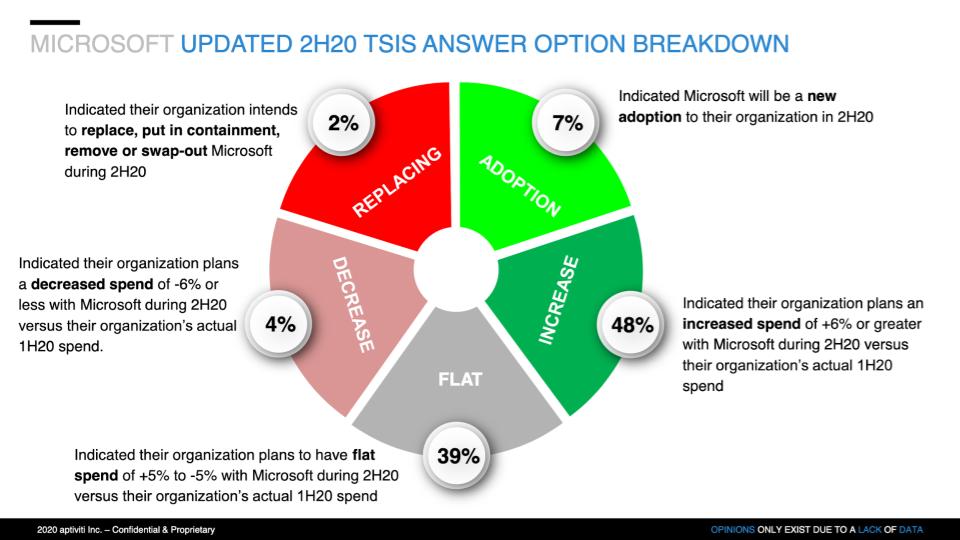

Microsoft Customers are Spending More with Microsoft

The chart below shows the granularity of ETR’s Net Score for Microsoft. The green represents increased spend and the red decreased spending. What’s impressive is that Microsoft’s red zone is negligible at 6% in total. Its customers are all spending more or the same and very few are leaving the platform.

Having spent the past 18 months digging into the ETR data set, we can tell you that for a company of Microsoft’s size and maturity, this is not only uncommon, it’s absolutely unique. Microsoft stands alone in the ETR data as the one very large company that demonstrates aggregate spending momentum equal to focused specialists of much smaller size.

Microsoft Azure Cloud is the Linchpin its Performance

Microsoft has made the transition to a cloud first business. Most other large on-premises players struggle and focus on three primary strategies:

- Hang on for dear life to on-premises workloads, arguing security, governance, latency and legal edicts.

- Lean in hard to hybrid cloud strategies that consistently loop back to #1.

- Lay out a vision of multi-cloud, which today generally means;

- Partnering (sometimes reluctantly) out of necessity with the Big 3 cloud players.

These are all reasonable strategies but as we’ve pointed out many times, Amazon launched S3 in 2006 to usher in the cloud era. In 2007, IBM spent far more on R&D than Amazon and Google and similar amounts to Microsoft. But over the next several years, Microsoft directed its research, development and capital resources in a way to compete directly with AWS and become a leader in cloud.

This successful leadership decision created Azure cloud, which powers all of the company’s software and services. Importantly, it allows Microsoft to not only migrate its existing customers to a world class cloud, but also attract troves of new logos to its platform. And all the while it gives Microsoft tremendous operating leverage with steadily improving marginal economics.

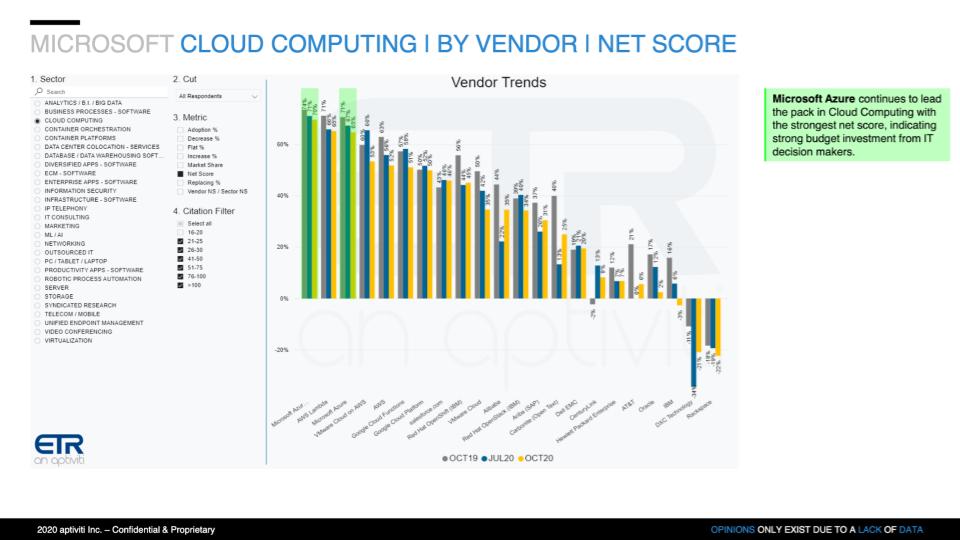

Sizing up the Cloud Vendors

The graphic above shows Microsoft’s position within cloud computing in terms of Net Score. Microsoft Azure functions (#1 on this chart) and Azure cloud overall (#3) shows momentum as strong as any cloud category, including AWS Lambda (#2 from the left). Five over from the left you can see AWS overall and while its levels are elevated, Azure Cloud overall (#3 from the left) has meaningfully more momentum with a 65% Net Score versus 52% for AWS overall.

Reasonable people can debate the quality of these clouds and argue over feature sets and regions and datacenters and the like…and fairly point out Azure’s struggles with outages, but it’s hard to argue against Microsoft’s “good enough” approach. It’s working and has been for decades.

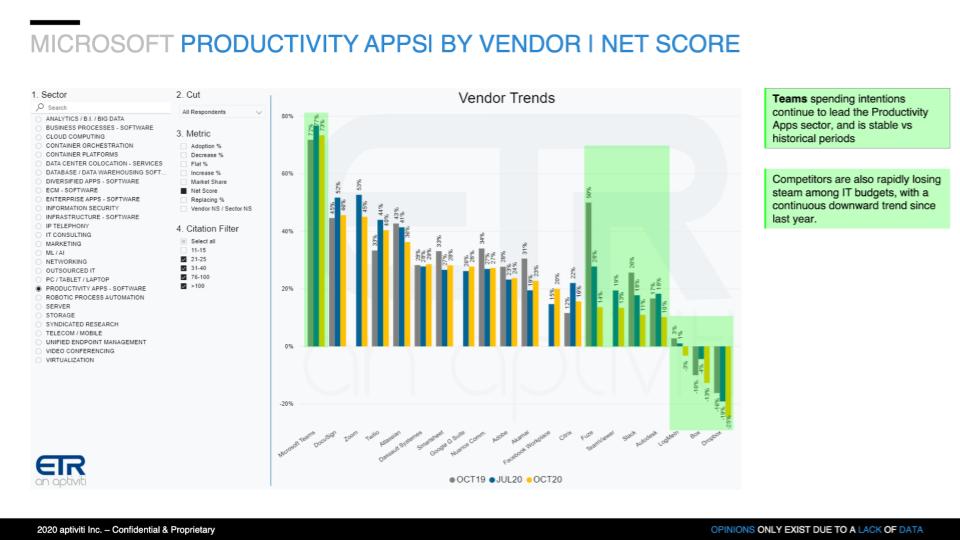

Teams – Another Example of Copy, Bundle, Integrate & Dominate

In the late 1980’s, we saw Microsoft first deploy this strategy with Office and it’s continued in a number of areas. The latest example is Microsoft Teams. Teams combines features like meetings, phone, chat, collaboration, as well as business process workflows leveraging tools like SharePoint and PowerPoint. It’s a killer strategy borrowing from Zoom, Slack and other leaders. But it bundles capabilities, integrates them into Microsoft’s vast estate and it all runs on the Azure cloud.

You can see the results in this chart below.

The graphic compares Net Scores from the year ago October survey, the July survey and the most recent October survey with 1400 respondents. Look at the lead Teams has relative to the competition with a 73% Net Score compared to 45% for Zoom and 11% for Slack. Teams is dominating.

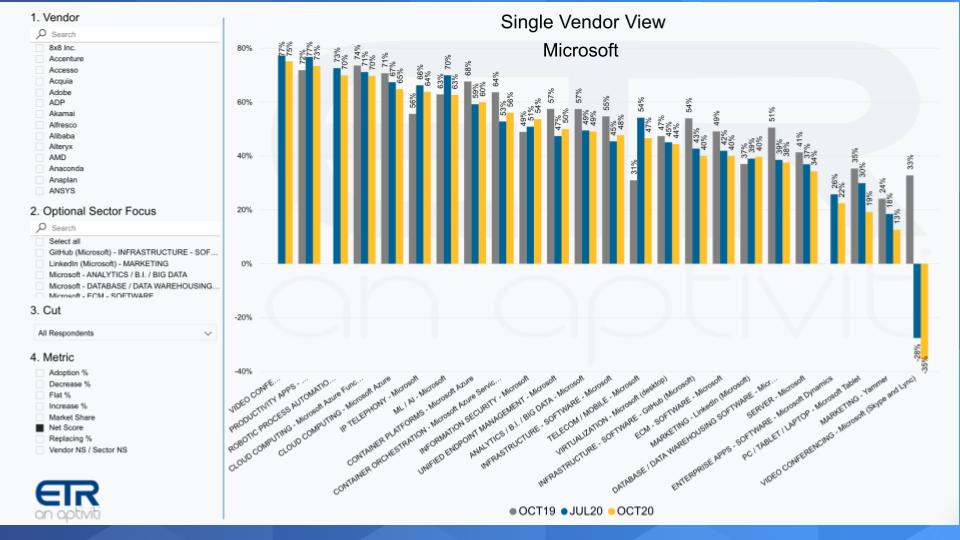

Nearly all of Microsoft’s Categories are Winning

The chart below shows Microsoft’s products across the ETR taxonomy. Video conferencing with Teams, productivity apps, RPA, cloud and cloud functions, MI/AI, containers, security, endpoint, analytics, mobile, database. All of these categories show Net Scores over 40% (with the exception of database/data warehouse, which still is in the high 30’s). These are extremely impressive signs of spending momentum for a company of Microsoft’s size.

The only signs of softness are seen in the company’s legacy businesses like Skype or its on-prem license businesses. And while PCs and Tablets are weaker than the others but it’s what you’d expect for such a mature and low growth business.

Again the premise in this post is that by pivoting to the cloud and going all in competing with infrastructure-as-a-service, Microsoft has created a platform for innovation for its business. Its developer chops are credible, it is evolving its installed base to the cloud, it has a solid hybrid and multi-cloud story with Microsoft Arc; which eventually it can take to the edge; although we think that Microsoft has some work to do there (more on that in future posts).

Importantly, the company has a huge partner ecosystem – it even partners with Oracle. As well it’s using Azure cloud to enter new markets, including vertical clouds like healthcare. We see this ecosystem play as the next wave of Microsoft’s innovation engine. Going from products–>platforms–>ecosystems is a powerful lever for the next ten years. Because there will be so much data living in Azure, its ecosystem partners will be able to more easily collaborate within Azure Cloud and create new capabilities for customers, especially as the edge evolves.

It’s the holy grail of cloud and edge and is a multi-trillion dollar market opportunity.

Critical Analysis

There’s really not much on which you can criticize Microsoft. Sure Microsoft has had some high profile failures, like the Nokia acquisition, Windows Phone, Zune, Mixer. Bing – is Bing a fail? Not really. Maybe the fail is what we discussed last week with antitrust. Microsoft was distracted by the DoJ and maybe that caused it to miss search and give it to Google. In that sense it was a failure but overall a pretty good track record. And really, who wants to be under the social media and advertising microscope today anyway?

Maybe you can say Microsoft is a copycat. Windows copied the graphical user interface of the Mac, but even Steve Jobs got that idea from Xerox PARC. Surface? The cloud? Yes these were not inventions of Microsoft per se. So what – ideas are plentiful. Execution is the key.

No matter how you slice it, the data doesn’t lie. Microsoft’s financial performance, its pivot to the cloud and the success of adjacent businesses make it one of the most remarkable re-births in the history of the technology industry. We wouldn’t say turnaround because the company was really never in trouble. It just became largely irrelevant.

Today – Microsoft is far from immaterial.

Remember these episodes are all available as podcasts wherever you listen.

Ways to get in touch: Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Featured Image Credit: Alexey Novikov