The big three US cloud players all announced earnings this past week and, as expected, cloud growth is slowing. But don’t kid yourselves. Hyperscale clouds remain the epicenter of innovation in tech and foundation models like GPT will only serve to harden this fundamental fact. Our data suggests the deceleration in cloud spend is a function of two related factors: 1) Cautious consumption patterns; and 2) Aggressive cloud optimization, which is being promoted by the big three cloud vendors in an attempt to lock in customers to longer term commitments. There is still no clear evidence in the numbers that repatriation is a factor. Rather, the ability to quickly dial down spending and pause projects is an attractive feature of cloud computing and one that, until now, has never really been seen on a broad market basis.

In this Breaking Analysis we try to explain the implications of this seemingly simple but nuanced dynamic. We’ll review the latest hyperscale cloud data for the big three players, share our analysis of certain comments made by cloud executives and show you the latest ETR data on spending and market presence in the cloud.

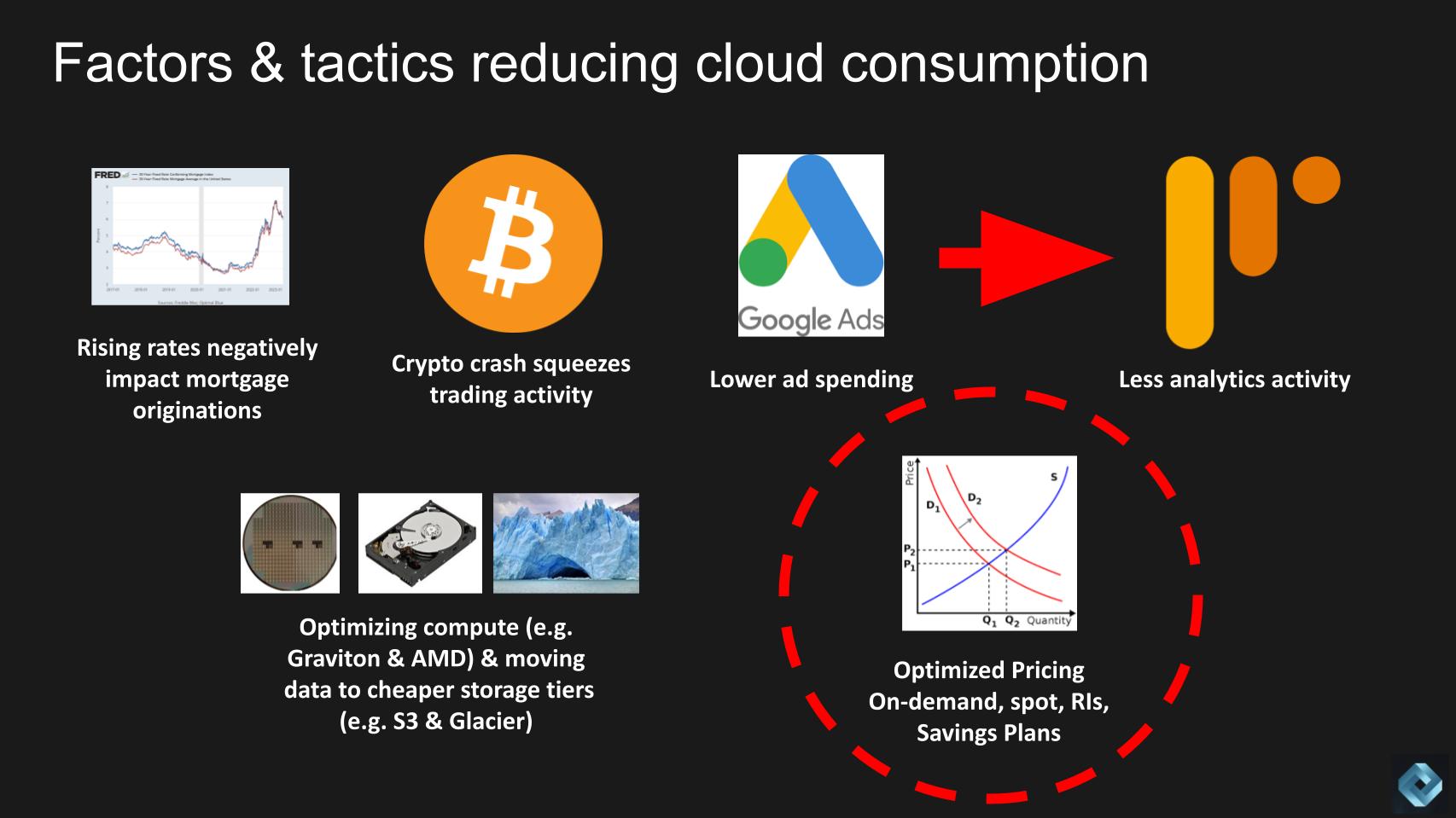

Cloud Pricing Plans Encourage Cost Optimization

Below is a chart we showed last quarter identifying the major factors impacting cloud demand.

Today we want to focus on optimization. Newish cloud savings plans were introduced prior to the pandemic, but they were largely overlooked during the COVID tech bubble because money was cheap and many businesses were booming. However during the pandemic several industries affected by the pandemic began to take advantage of these plans but it was hidden by the surge in cloud demand overall. Toward the end of 2021, we began to see early inning signs of optimization kicking in more broadly where customers took a harder look at the spectrum of pricing options and began to get more aggressive about cost cutting.

On the chart above we show on-demand, which is the most expensive, spot pricing, then reserved instances (RIs) and then savings plans. These savings plans yield the most savings in the form of credits. A simplified way to think about cloud pricing is it’s always calculated on-demand but with credits it’s like getting an instant coupon applied at checkout. With savings plans you get the most credits. As we entered 2023 the shift toward more attractive pricing models accelerated and will continue indefinitely in our view because it is becoming part of the corporate muscle memory.

Aggressive and ongoing cost optimization is not a negative for cloud demand in our opinion. Rather it will drive more demand in the long run and serve to make the cloud even more attractive going forward as organizations operationalize cost optimization into their processes and do more with less.

Tactically, we believe consumption trends related to the macro are the primary driver of the cloud spending slowdown, not cost optimization. Specifically, over a contract term of one or three years, revenue will generally not be negatively affected by cost optimization. However within a specified term, customers will dial down consumption based on their specific outlook. Hence our premise that cost optimization is an attractive feature of the cloud, not a bug in the system.

We believe this dynamic will hold true for cloud-native, consumption priced platforms from not only the hyperscalers but other technologies suppliers such as Snowflake, Databricks, MongoDB’s Atlas, Couchbase Capella and many others.

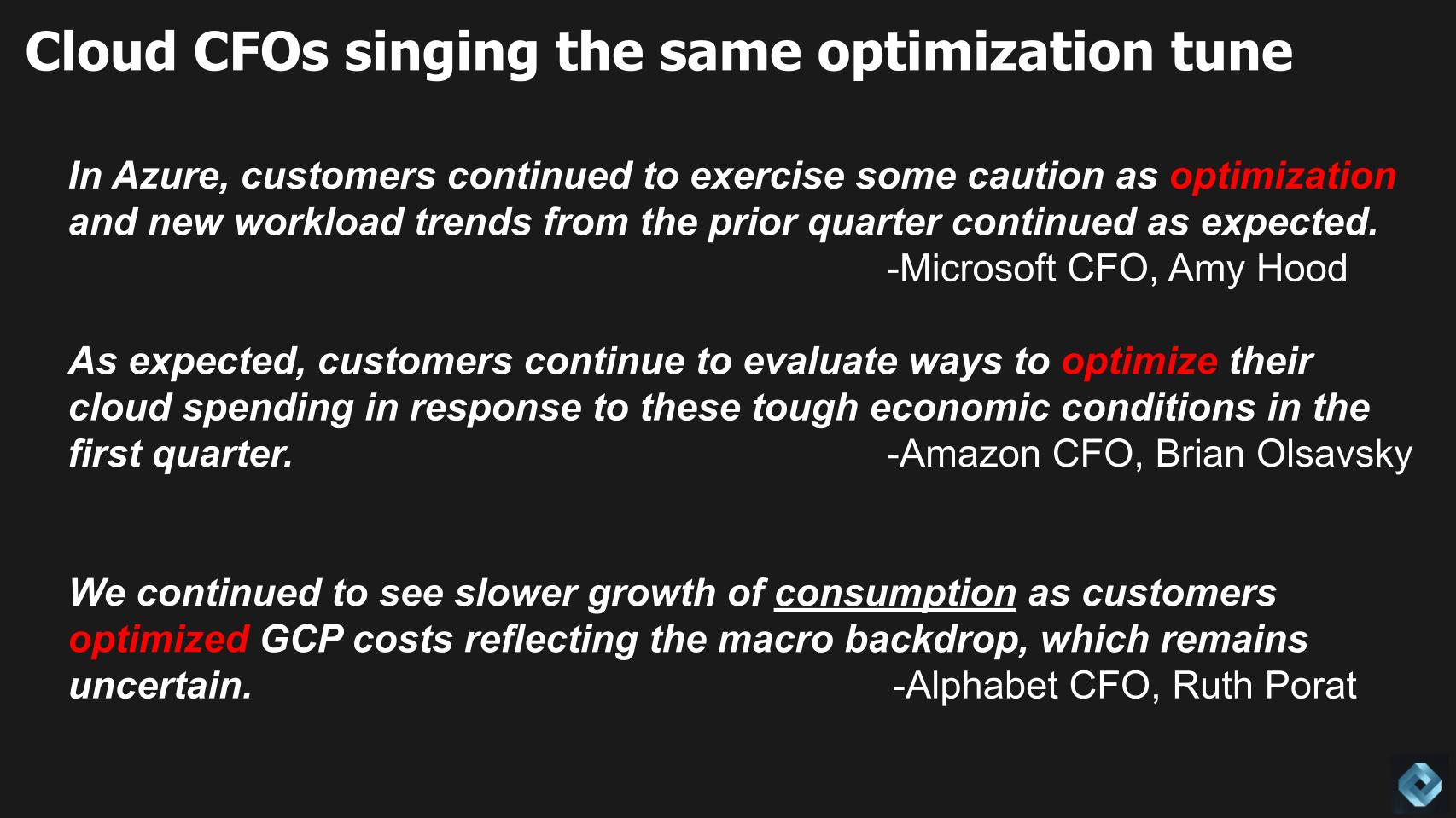

Cloud CFOs all Cite Optimization as a Trend

Now cloud companies generally and AWS specifically have been transparent and even proactive about cloud optimization. The reason being they’re well aware of the customer spending climate and rather than fight fashion they’re leaning in and encouraging customers to sign up for one year or three year savings plans. Commit to buying more and spend less per drink. Importantly, this enhances CFOs’ revenue visibility within a term.

Here’s what all three hyperscale cloud companies’ CFOs said this week on their earnings calls.

Microsoft CFO,Amy Hood said:

In Azure, customers continued to exercise some caution as optimization and new workload trends from the prior quarter continued as expected.

Amazon’s Brian Olsavsky commented:

As expected, customers continue to evaluate ways to optimize their cloud spending in response to these tough economic conditions in the first quarter.

Ruth Porat’s comment on Google Cloud:

We continued to see slower growth of consumption as customers optimized GCP costs reflecting the macro backdrop, which remains uncertain.

All three companies’ CFOs cited optimization and each firm implied in its remarks that they were supportive of these customer trends. Amazon in particular emphasized its long game and our sources suggest that unquestionably, AWS is aggressively going after longer term deals to focus on lifetime value versus short-term revenue optimization. Our research suggests that optimization, in and of itself, is probably not as much of a revenue suppressor as you might think. Consumption patterns will fluctuate monthly but over the term, revenue will be predictable.

In general, cost optimization plans come in the form of credits and these are typically use it or lose it. Meaning the credits are good until they expire. Credit rules follow clear but often complicated rules with which customers should become familiar as it will help choose the right plan and reduce costs. Larger customers can negotiate with cloud vendors to extend or tap new credits contingent upon renewing or extending a term.

Remember when negotiating, a cloud vendor is more motivated by lifetime value (i.e. revenue over a term) versus obtaining the highest fee for an individual service. This is another aspect of the cloud operating model that on-premises vendors are still learning

The bottom line is our current working assumption is that monthly consumption patterns are dampening growth rates. Cloud price optimization will continue indefinitely, but in and of itself it won’t hurt revenue. Rather when demand picks up lower cost will translate into higher consumption that will lift revenue.

This a reason to be bullish on hyperscale clouds.

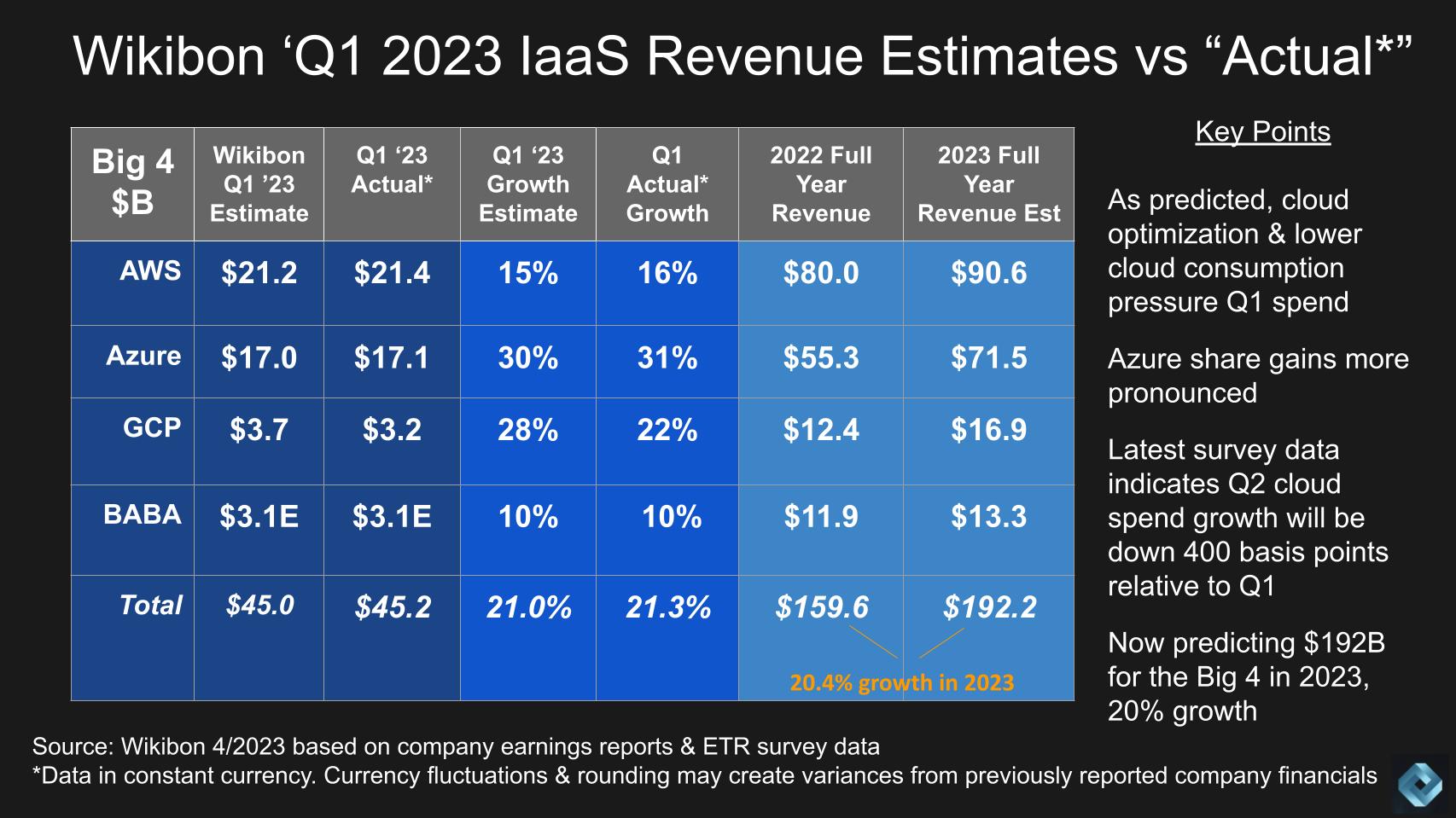

Quarterly IaaS Data Shows Microsoft now 80% of AWS Revenue

Below we show our latest quarterly hyperscale cloud numbers.

We’ve been modeling this data since before AWS began sharing revenue publicly and are one of the few firms to regularly track and freely share IaaS and PaaS revenue from the hyperscalers on an apples-to-apples basis.

The chart shows our Q1 2023 revenue estimates for AWS, Azure, GCP and Alibaba as compared to the actuals. Note that Alibaba hasn’t reported yet so they’re still estimates. So you can see, with the exception of GCP we were right on the numbers. AWS we had at 15% year on year growth and they came in at 16% or $21.4B for the quarter. Our Azure estimates were for 30% growth and they came in at 31% or $17.1B and GCP we had at 28% growth but we’ve lowered that to 22% or $3.2B. We’ll come back to that in a moment.

Overall we had the market growing at 21% in the quarter and we’ve only slightly increased that to 21.3% which yields $45.2B for the quarter. We’re now forecasting $192B for the year or 20.4% annual growth in 2023, which is slightly lower than our Q1 forecast.

A couple other points worth noting:

- Azure continues to gain share and is now 80% of AWS’ revenue;

- We’re lowering our outlook for Q2 and Q3 and forecasting an uptick in Q4. Our latest read on Q2 is growth rates will continue to decelerate by around 400 basis points.

The action in the market Friday was interesting. Amazon and AWS earnings well exceeded expectations as AWS operating income was $5.1B or 106% of Amazon’s operating income. Sequentially down but better than expected. As well, Amazon overall came in better than consensus. The stock went up after hours but then retreated to the downside because of concerns over AWS’ growth rates. So despite the consistent operating profit from AWS, investors are concerned about the near term future. But as we’ve said, our data shows AWS being very aggressive in trying to get customers to sign up for longer term deals and we see this as a positive long term for the company.

One other point is Google Cloud reported $191M in operating income, reversing a nearly half-a-billion-dollar loss from last quarter, exhibiting good cost cutting by Google. More on Google Cloud in a moment.

How Many Times can you Say AI?

Of course all three companies emphasized generative AI on their calls with AWS the most recent entrant in the race with Bedrock. It’s interesting because it looked like Microsoft was behind technologically and then from a business model standpoint cut to the front of the line with OpenAI and ChatGPT and all the marketing buzz. But Google is going to embed AI into everything – as are Microsoft and AWS. Google has been at this for a while. So has AWS which recently exposed a differentiated strategy – essentially the same way it approaches cloud – building blocks for developers. AWS announced a three layer cake approach with new silicon chips, Bedrock, which is LLMs as a service and app builder support with a tool called Code Whisperer.

AWS is the most focused on letting customers build their own LLMs, which will be attractive to a lot of firms concerned about IP leakage. But Google and Microsoft undoubtedly will offer such options as well.

Reading the Tea Leaves on Google Cloud Platform

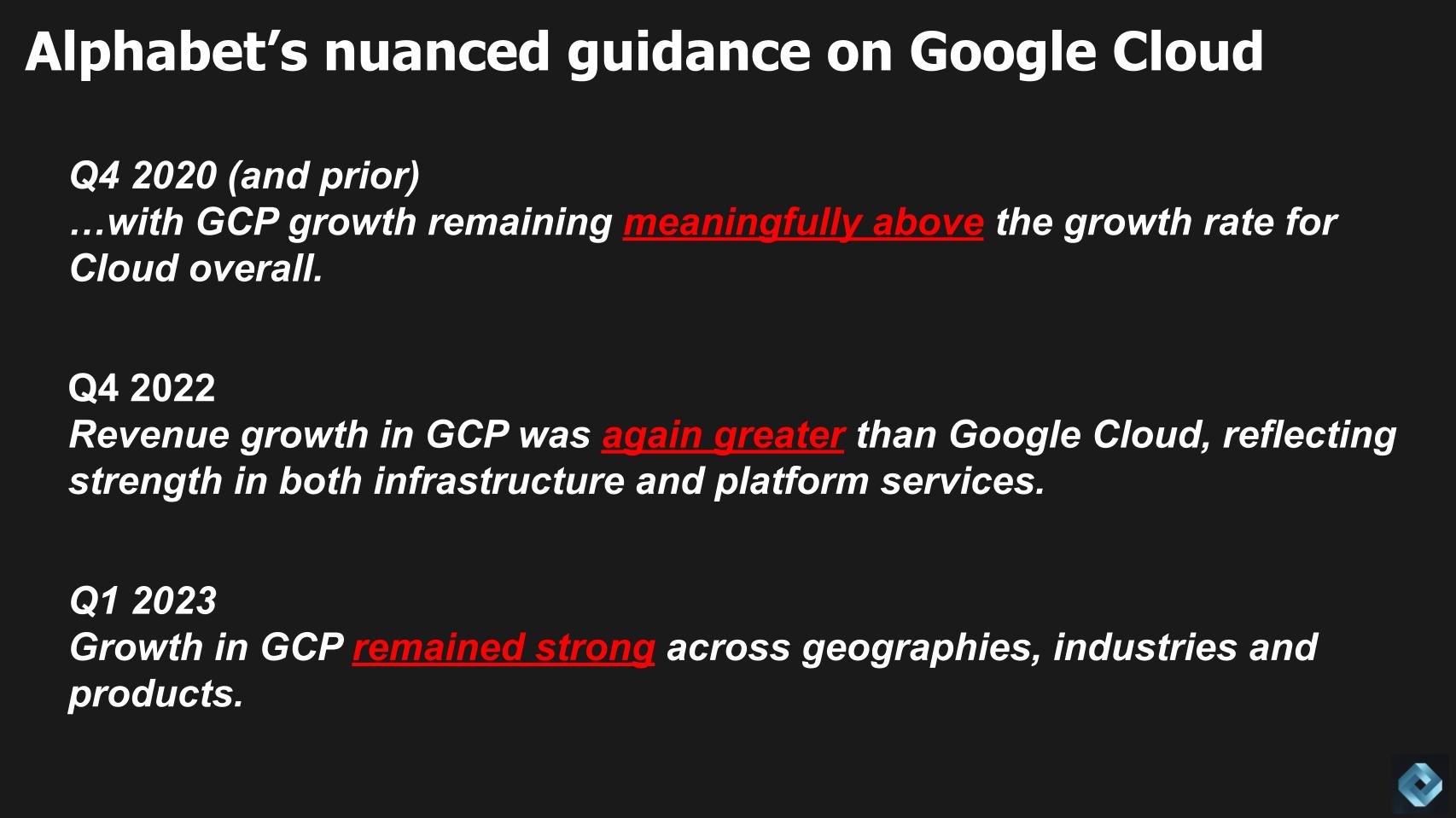

Coming back to Google for a moment we want to share something that nobody really talks about. And something we pay close attention to because remember we’re trying to get to an apples-to-apples comparison with IaaS and PaaS. Only AWS makes it easy. Azure gives a growth rate and Google gives relative indicators. But look how Alphabet’s narrative has changed with respect to Google Cloud Platform revenue guidance.

Q4 2020 (and prior)

…with GCP growth remaining meaningfully above the growth rate for Cloud overall.

Q4 2022

Revenue growth in GCP was again greater than Google Cloud, reflecting strength in both infrastructure and platform services.

Q1 2023

Growth in GCP remained strong across geographies, industries and products.

To us this is an indication that for the first time, GCP grew more slowly than Google Cloud overall.

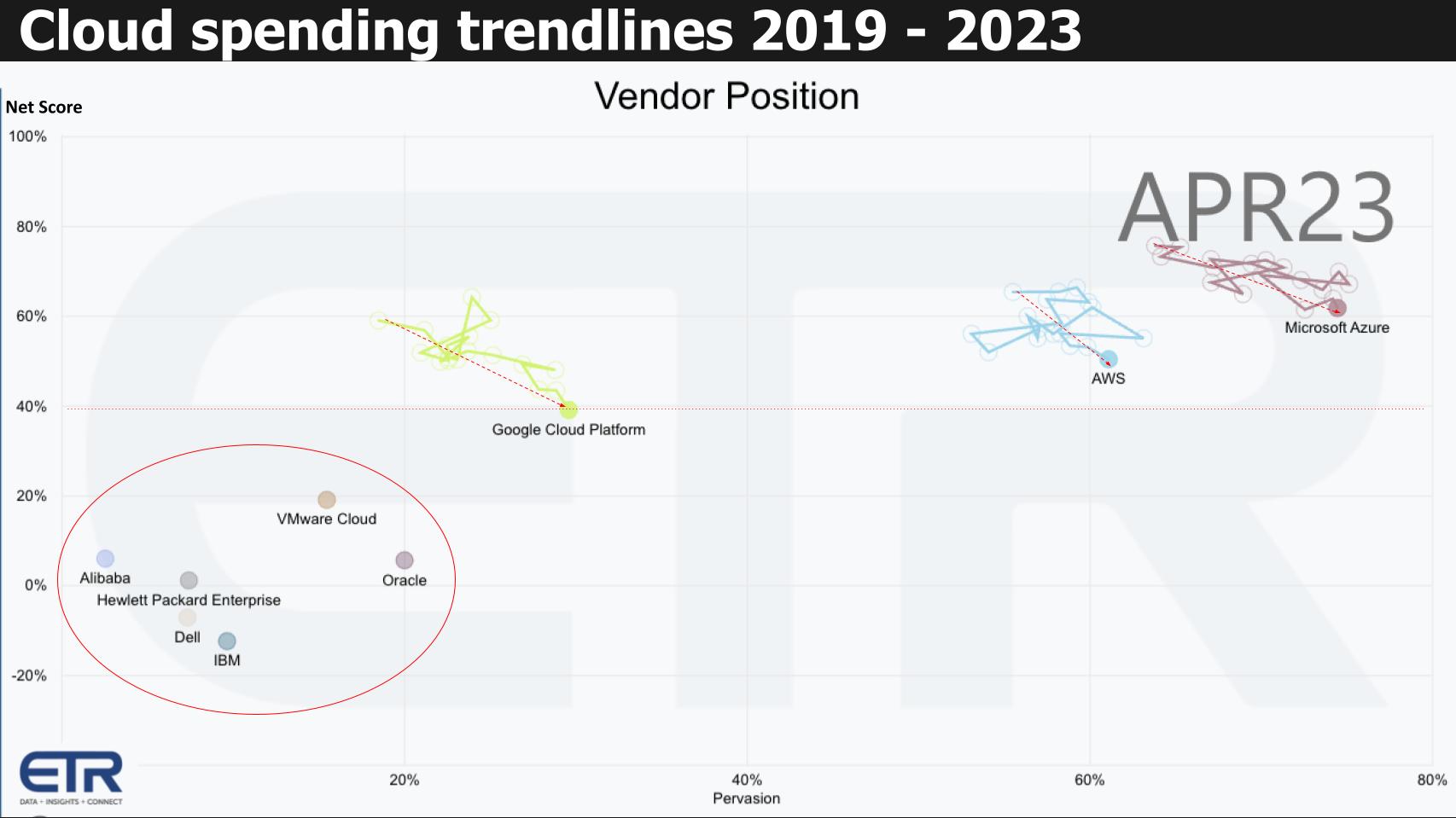

ETR Data Confirms the Cloud Deceleration

The deceleration is not confined to Google. But if you go back and look at Azure when it was around the same size as GCP at just over $3B it was growing at 85% year over year. So unfortunately for Google that’s the penalty for getting in late and the challenge of course of the first tech downturn since really the cloud took off.

This chart above plots Net Score or spending momentum on the Y axis with Pervasion or presence in the ETR data set on the X axis. We’ve annotated the Big 3 players with the squiggly lines which show quarterly positions going back to 2019. So the bad news is the consistent deceleration but all three have become more prominent in the data, moving to the right. It’s no surprise but they’re all playing the long game and they have the resources to compete over many years. Remember, the red dotted line at 40% indicates a highly elevated spending velocity. So all three are still above that line.

We’ve also circled the so-called hybrid cloud vendors that have a big on-prem presence. Their momentum matches their lower reported growth rates and they also were late to cloud. HPE with GreenLake and Dell with APEX are just starting to get noticed in the ETR surveys. IBM cloud has stalled in the data set and retreated from a market presence standpoint. Oracle on the other hand has actually made meaningful progress on the X axis over time. VMware Cloud (e.g. Cloud Foundation) has also held up well and VMware Cloud on AWS (not shown) is performing better than any of the traditional vendors shown.

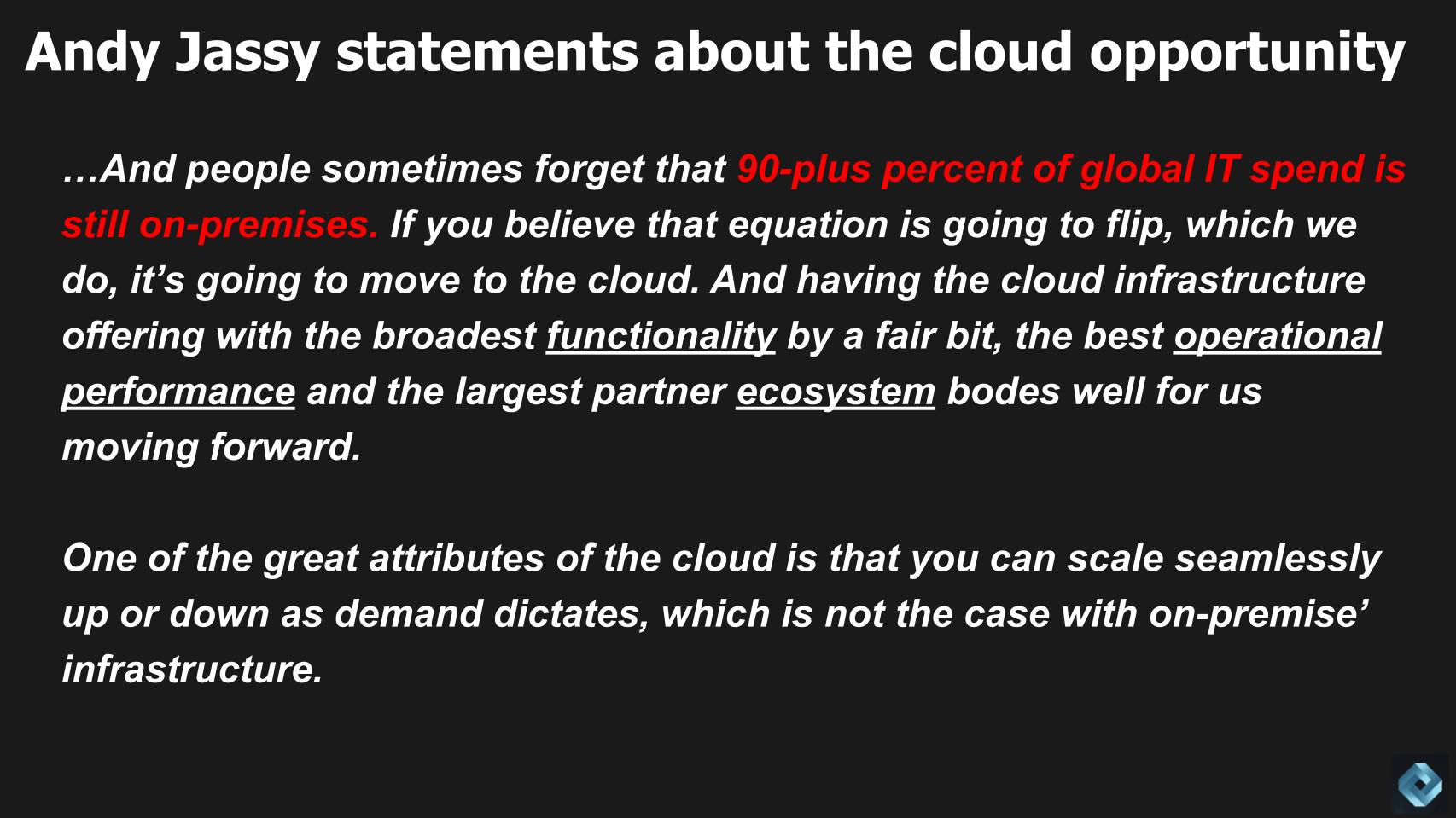

Unpacking Andy Jassy’s Statements

In thinking about how this all plays out in the future let’s take a look at some of the comments from Andy Jassy on the earnings call Thursday night.

Jassy continues to emphasize one of the fundamental assumptions AWS shares:

People sometimes forget that 90-plus percent of global IT spend is still on-premises. If you believe that equation is going to flip, which we do, it’s going to move to the cloud. And having the cloud infrastructure offering with the broadest functionality by a fair bit, the best operational performance and the largest partner ecosystem bodes well for us moving forward.

And…

One of the great attributes of the cloud is that you can scale seamlessly up or down as demand dictates, which is not the case with on-premise’ infrastructure.

We think both of these statements are meaningful but are evolving and can be challenged. Specifically, cloud is growing so much faster than on-prem and the the last several years we’ve heard this 90% figure. Excluding telco for a moment because that’s a different animal, most IT spend is on services and most services deals today have some type of public cloud component. So the 90% figure is probably no longer correct. Moreover, AWS at $90B and Azure at $70B this year start to become the largest enterprise tech vendors. Dell is the largest enterprise technology company but if you exclude PCs, AWS is much bigger in the enterprise as is Azure.

Now the flip side of this is the second part of Jassy’s quote that you can’t scale up and down seamlessly with on-prem. Well with services like GreenLake and Apex that is beginning to change as well. Sure you have to install the equipment and that is going to take some time but once that’s done you’re simulating a cloud operating model and that will definitely keep some folks spending on-prem. So the battle is just beginning here.

The key point we want to emphasize is we would re-frame Jassy’s to emphasize business transformation versus IT transformation. In other words:

- There’s plenty of room for cloud to grow but the value proposition is shifting from eliminating undifferentiated heavy lifting in IT, to eliminating undifferentiated heavy lifting in business. This is a multi-trillion dollar opportunity that transcends traditional IT spend and definitely comprises Telco and industry 4.0;

- With foundation models like GPT, the cloud with its pace of innovation, rich functionality and strong ecosystem is the likely place where this transformation will occur.

And in our view, AWS is exceedingly well-positioned to capitalize.

What Does the Survey Data Say About Cloud’s Share of IT?

Let’s look at some ETR data on this topic.

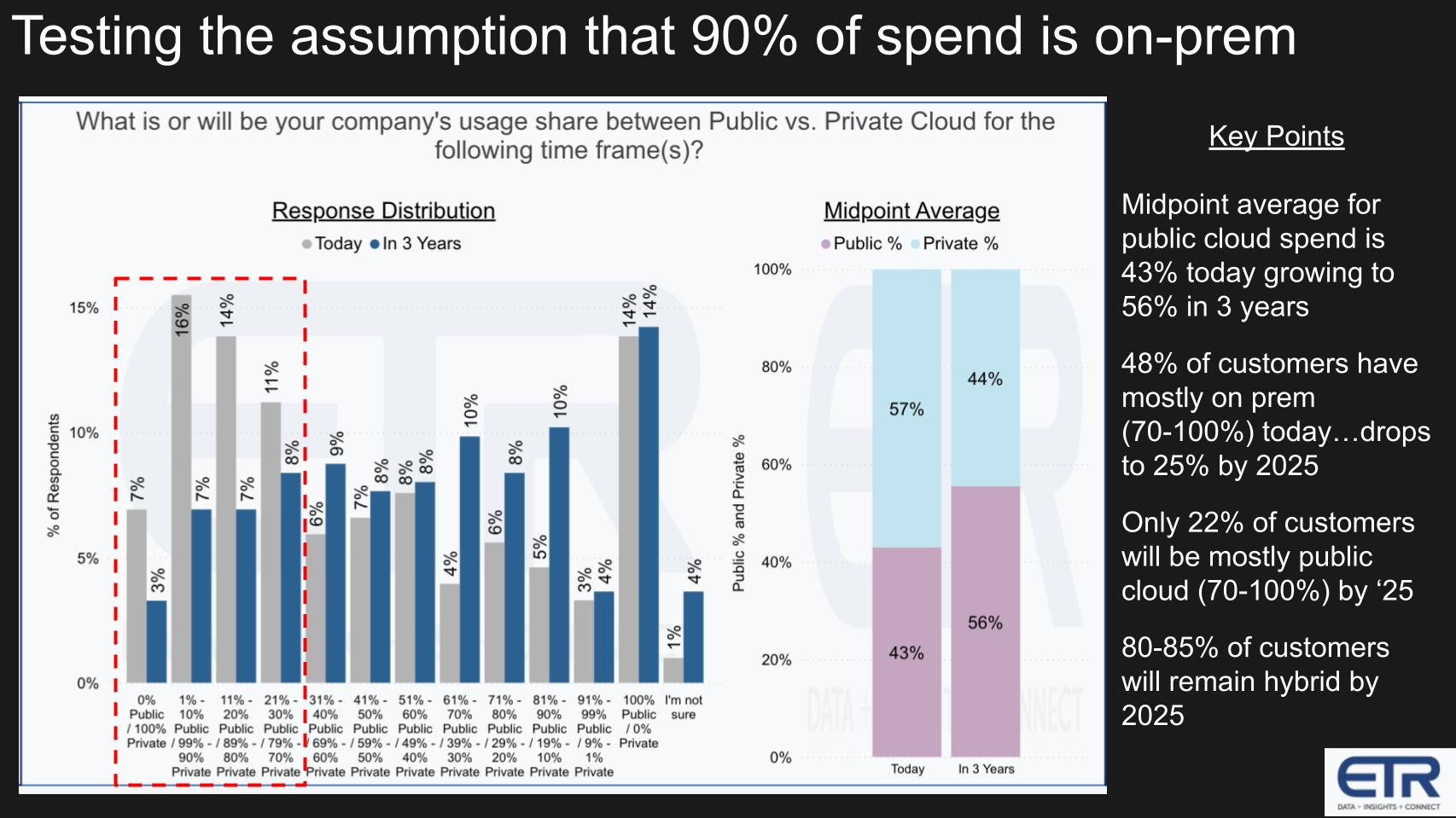

In a drilldown survey last fall ETR asked customers their usage percentages between public and private cloud at that time and three years down the line. We put a dotted line around those responses that said 70% or more would be on-prem and it turns out that in the fall of last year, that figure was 48%, declining to 25% by 2025. And only 22% of customers said they’d be mostly public cloud (i.e. 70% or more) by 2025. Importantly, 80 to 85% of customers see themselves as remaining hybrid through the middle of the decade.

Now AWS likes to use the phrase “in the fullness of time,” which most certainly extends beyond 2025.

But we would say this…when you strip out services and isolate on compute, networking and storage well over 10% of spending is in the cloud – probably closer to a third or more. Maybe even as this chart shows on the right…the midpoint averages – could be 43% moving toward 56% by 2025.

Now having said that, when you start thinking about telecomms and edge and satellites and a new set of emergent use cases there’s plenty of room for growth. But the big wave of cloud in terms of eliminating the undifferentiated heavy lifting in data centers has largely taken place in our view. And now it’s going to come down to: 1) How effective incumbent vendors are at mimicking the cloud operating model and reducing the attractiveness of moving workloads to the cloud; and 2) Innovation for new data driven workloads.

How AI will Impact Business in the Future

The cloud players have the leg up when it comes to this opportunity because they have the data, the tooling, the ecosystems and the massive CAPEX infrastructure that continues to expand. While incumbents will unquestionably leverage AI and it will help their businesses remain stable, it’s unlikely that they’ll meaningfully close the gap on the hyperscalers.

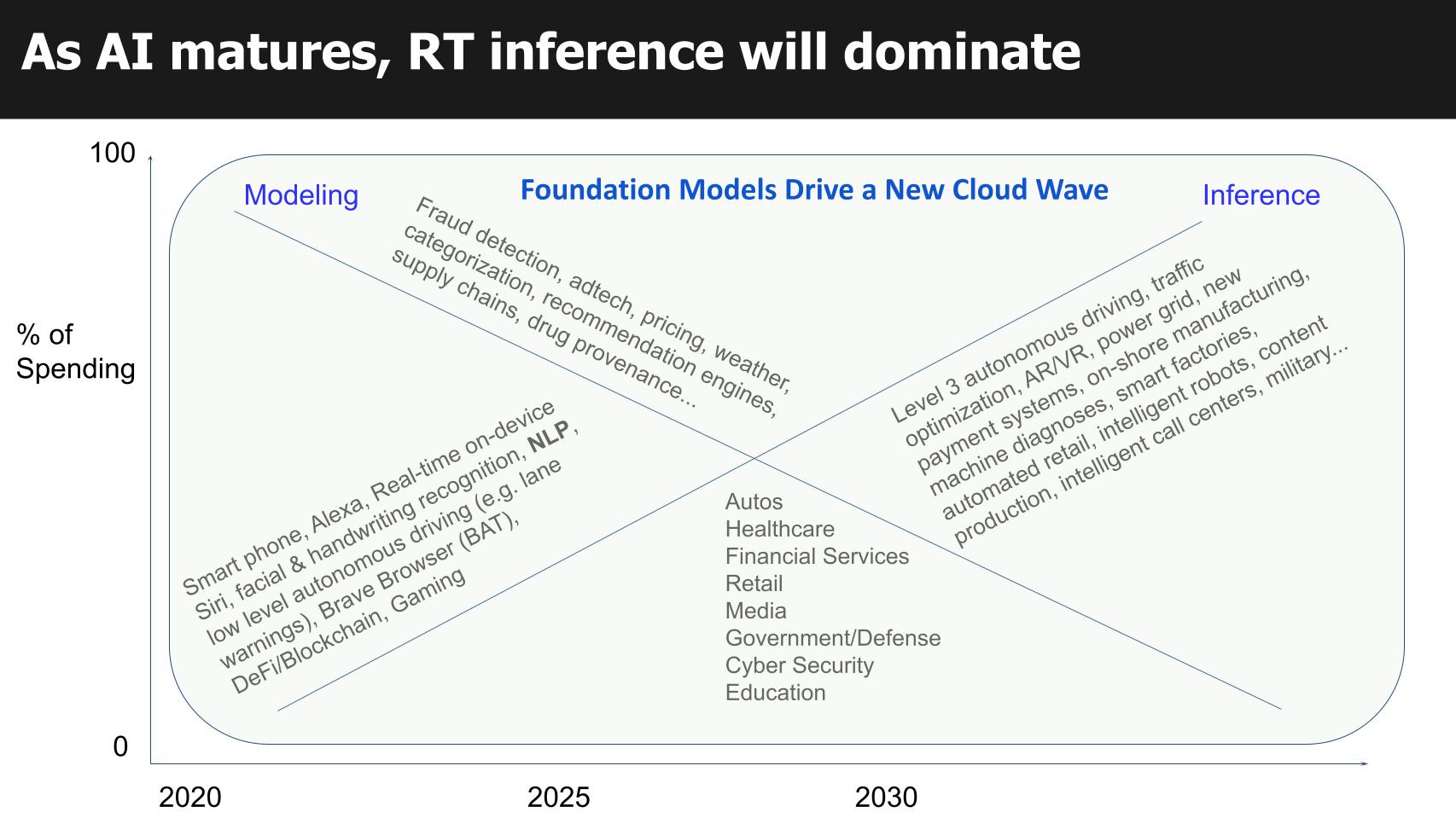

We shared the chart below a while back when we were opining about the future of semiconductors and the impact of Arm designs in the data center and at the edge.

The point of the graphic is that most AI to date has been focused on modeling in the cloud and we predicted that over the next few years the equation would flip to where AI inference would become a dominant force. And we highlighted NLP and used smart phones, Alexa and other proxies from mobile to predict a ubiquitous use of AI in virtually all industries and applications.

Now we didn’t predict the ChatGPT effect would storm the castle the way it has….But there are three points here: 1) a lot of the early generative AI activity is going to be happening in the cloud, across multiple clouds and the supercloud will extend to the edge. It’s early days and the cloud players have the tools, the technologies, the partnerships and the scale economies to lead; and 2) Massive data demands, low power requirements and distributed computing will require new architectures from silicon to databases to apps – all the way up the stack. Amazon’s new chips for training and inference are timely given all the AI hype but they’re also instructive.

As we’ve reported, AWS is on a new silicon S-curve and is leading. Google, Microsoft and Alibaba are all following with their own designs and the four hyperscalers will drive costs down. Price might be a different story but their cost structures will be superior; and 3) we still believe that edge use cases will become a massively disruptive force and Arm-based designs will be at the center of the disruption. Intel is doing everything it can to keep up but it doesn’t have the volume advantage and there is no foreseeable path to Intel regaining the volume manufacturing lead. Arm wafer volumes and TSM are the dominant economic forces thanks to Apple and unless there’s a radical event – like China invades and pirates TSM – this will be the case for well over a decade.

Near Term Cloud Outlook

Let’s bring it back to cloud in the near to mid-term.

The macro and the fed are still the main drivers of spending patterns. That said optimization is here to stay – it’s part of the IT muscle memory.

We expect cloud growth to decelerate in Q2, stay flat in Q3 and we think Q4 will bring an acceleration to cloud growth. Nothing crazy…we think we’ll see growth rates uptick a few percentage points in Q4 but it will depend of course on the broader economy. It seems the Fed is intent on suppressing inflation, jobs and wages and the government is uninterested in austerity so this could mean more pain in the economy.

All that said, cloud growth will continue to significantly outpace overall IT spending rates, which are now projected to come in at mid 3% growth this year…While the hyperscalers will grow 5-6X that rate.

AI is deflationary and that could be the savior to a concerning fiscal and monetary policy. Foundation models will be a tailwind for all companies that can leverage them to cut costs and automate and they’ll be especially beneficial to cloud players. From silicon to large language model services up to the apps.

The outlook is mixed. Banks are down, GM beats and raises, toothpaste and diapers are more expensive as it food, housing is soft, advertising is down but Meta grew and tech is generally beating earnings estimates…but growth capital is drying up and shifting to early stage companies developing AI platforms. So maybe this is a signal that we’re returning to a new normal where not everyone can just fall out of bed and do well, and not every company is negatively impacted by the macro.

So it’s back to doing your own homework, analyzing the market, doing a risk analysis, placing bets and executing.

Isn’t that the way it’s supposed to be?

Keep in Touch

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image: mpfphotography

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.