Enterprise software markets are dominated by mega cap companies like SAP, Oracle, Salesforce and Microsoft. SaaS leaders like ServiceNow and Workday have solidified their market positions by to a great extent, replicating the Salesforce model in their respective domains. There is still room for innovative upstarts that are introducing new cloud native services and value pricing models but the traditional space is maturing with possible disruption coming from cloud developers and ecosystems.

Enterprise Software and Systems of Record

Enterprise applications are an enormous market – $500B+ depending on what you include – and they’re enormously important to organizations globally. Essentially the world’s businesses are running on enterprise applications. Companies’ processes are wired into these systems and the investments in people, process and technology are vital to their daily operations. The problem is many of these systems are decades old. Markets have changed but the installed ERP system at your company – for example – fundamentally hasn’t.

In this week’s Wikibon CUBE Insights, Powered by ETR, we’re going to do a data download on the enterprise software space and put forth some themes from the community and our thesis around this very important segment.

We’d like to acknowledge the contribution of our friend Sarbjeet Johal who helped formulate the premise for this post.

The Scope of Enterprise Applications

Software markets span many categories. Systems of record (e.g. transactional), systems of intelligence (e.g. analytics) and systems of engagement (e.g. social and collaborative platforms). This research focuses on the core enterprise apps that companies rely on to run their businesses. The systems of record. Examples include the ERP/financial systems, HR, CRM, service management, supply chain management and the like. We may touch on some other areas but this is the core we will drill into.

These are big markets. Customers spend many hundreds of billions of dollars in these area. And it’s a mature market as you’ll see from the data. Today, it’s good to be in the technology business. Tech is doing better than most sectors And within technology it’s better to be in software because of the economics and scale. And if you have a SaaS cloud model it’s even better.

But the market is fragmented – not nearly as much as it used to be but there are many specialized areas where leaders have emerged. ServiceNow in ITSM or Workday in HCM are good examples of companies that have focused and then exploded. We saw ServiceNow blow past Workday’s valuation – it was nearly 2X Workday’s before Workday crushed earnings this past week and was up 15% after its earnings release. ServiceNow, which took a slight breather earlier this month was up on Workday sympathy after Workday announced. Salesforce also beat earnings last week and stunningly, replaced Exxon Mobil on the Dow Industrials – imagine that.

Digital Transformation and Systems of Record

Digital transformation is the big cliche you hear from all tech companies and especially software players. What does digital transformation mean for systems of record? Well, often it means the systems are old and need to be updated. This is especially true for the mega caps and legacy systems like Oracle, SAP, Peoplesoft, JDE and even Microsoft. Take ERP and some of the mature products for example. Oracle R12, SAP R3/R4, etc. Many of these systems were put in 15 years ago and they need to “transform.”

These systems are generally burnt in. Many were installed in 2005 before the iPhone. Before social media. Before machine learning and AI made its big comeback. Before cloud. These systems were built on Internet 1.0.

The business of a company that installed these systems years ago has change, but the software running it really hasn’t. It happens every 10-15 years – companies have to upgrade or re-implement their systems and optimize for the way the business now runs. Because they have to be more competitive and agile.

And if you’ve made loads of custom modifications you’re really in trouble if you need to upgrade .

This is one reason why pure play companies like ServiceNow and Workday have done so well. They are best of breed and they’re cloud. And it sets up that age old battle that we always talk about – BoB vs integrated suites. Companies like Salesforce, Workday and ServiceNow are expanding their portfolios into suites of products. Will this make it harder for them to remain specialized leaders? And will it leave room for disruptors?

Themes from the Community

We’ve definitely seen this schism play out between on-prem and cloud plays and that’s created some challenges for the legacy vendors. People working remotely has meant less on-prem action for the legacy companies. In many cases they’ve gone out and acquired to get to the cloud. And/or they’ve had to re architect their software like Oracle has done with Fusion.

But think about something like Oracle financials. Oracle is migrating them to Fusion. Or SAP R3/R4 with SAP pushing HANA…all this is going to cloud-based SaaS.

So the companies that have been pure SaaS are doing better – and we say quasi modern on this slide above because Salesforce, ServiceNow, Workday, Coupa, NetSuite (Oracle), Success Factors (SAP), etc….these are actually pretty old companies. Earlier part of the 2000’s or 1999 in the case of Salesforce.

And we’re seeing some really clear pricing trends in the market. Things are moving quickly to OPEX models. You have the legacy perpetual pricing model giving way to subscriptions and now we see companies like Datadog and Snowflake with consumption based pricing – fees charged as a true cloud. And we think that will spill into SaaS applications.

One of the concerns we’ve heard from the community is some of the traditional players that were able to hide from COVID earlier this year with deferred revenue, might not have enough deferred dry powder to continue to power through the pandemic. But so far the picture continues to look relatively strong.

A final thought on disruption and something we discussed this week with Sarbjeet Johal. The disruption of this market – or maybe it’s not just disruption, but new opportunity – perhaps comes from cloud and developer ecosystems. We had a conversation about the PaaS layer in between IaaS and SaaS with Jerry Chen of Greylock on theCUBE way back in 2013. Seven years ago he called for the stitching together of multiple SaaS platforms.

As well at the time, people were talking about whether AWS was going to enter the applications market and the thesis here is no or not in the near future. Rather the disruptive play and this is Sarbjeet’s premise – is to provide infrastructure for innovation and a PaaS layer for differentiation. And developers will build modern cloud native apps to compete with or add value to SaaS platforms. Or both. This is intriguing to us and will likely play out over the next decade. But it will take a while because these SaaS players are getting huge and continue to pour money into their platforms and develop their own PaaS layers.

The Relentless Shift from CAPEX to OPEX

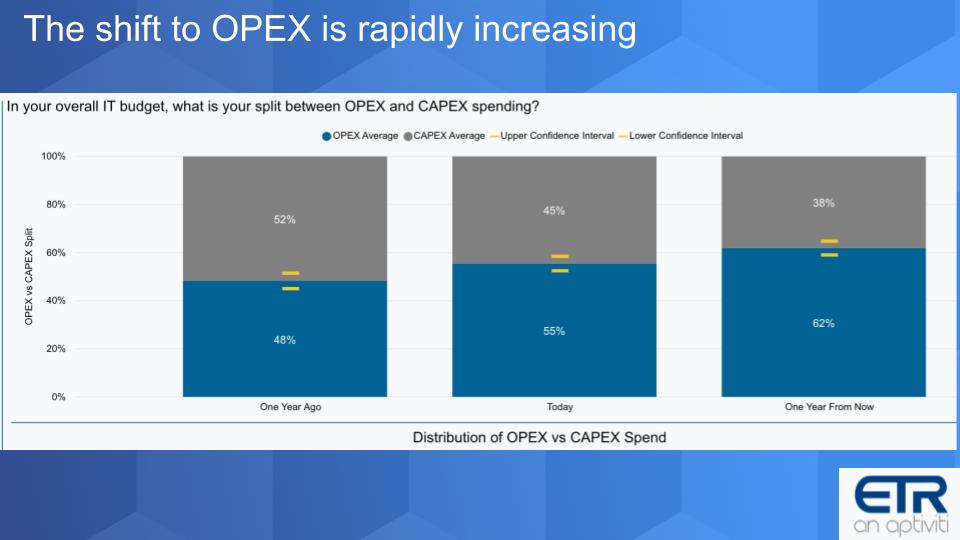

Of course the shift to OPEX was well in play pre-COVID. But the trend has been accelerating.

The chart above shows data from an August ETR survey asking people to express their split between CAPEX and OPEX spend. And you can see the trend is clear from 48% last year, 55% today and moving to over 62% a year from now. No surprise but we think it could happen even faster depending on the technical debt organizations have to shed. And hence the attractiveness of the SaaS cloud players.

Measuring Momentum for the Leading Enterprise Application Vendors

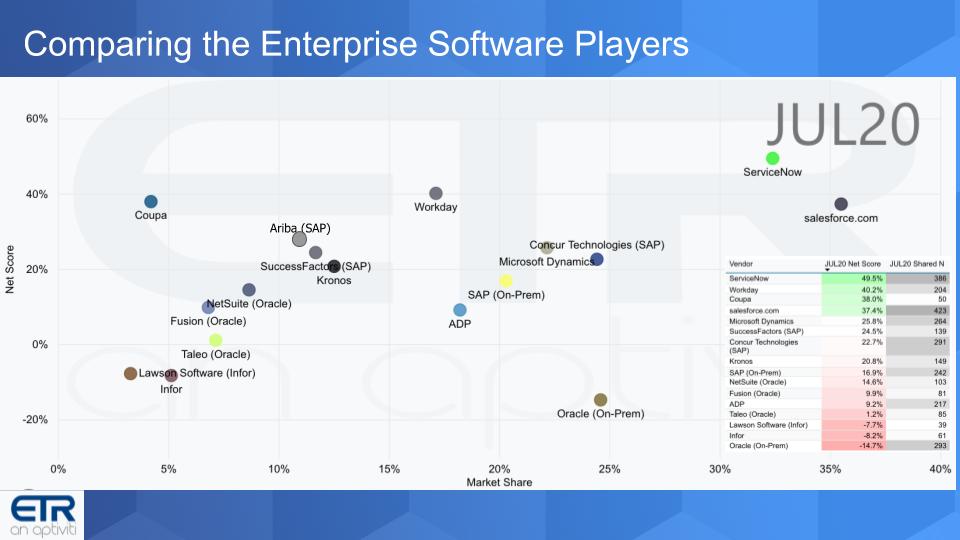

The chart below shows one of our favorite views. We juxtapose Net Score on the vertical axis with Market Share on the horizontal plane. Net Score is a measure of spending momentum. Each quarter ETR asks buyers are you planning to spend more or less and they subtract the less from the more to derive Net Score. Market Share is a measure of pervasiveness in the data and is derived from the number of mentions in the sector divided by total mentions in the survey. And you can see each metric in the superimposed table.

As we stated earlier, this is a pretty mature market and you can see that in the table based on the relatively large number of responses within the Shared N for each company. As well, most have middle of the road Net Scores. And there’s lots of red.

There are some standouts however as you see in the upper right. Namely ServiceNow and Salesforce with strong momentum and market presence. These are two pretty remarkable companies. ServiceNow entered the market as a help desk / IT Service Management player and has expanded its TAM dramatically. To the point where they’re aiming at $5B in revenue. Salesforce was the first cloud CRM and is pushing $20B in sales. We’ve said many times these two companies are on a collision course and we stand by that as any of the next great software companies – and these are two – will compete with all the mega caps, including Oracle, SAP and Microsoft.

The Super Cap Players

Microsoft with Dynamics shows up like they always do in the data. We’re like a broken record on Microsoft…they’re everywhere in the survey. Now Oracle and SAP have been extremely acquisitive as you can see from their many discrete assets on the chart. We’ve said many times on theCUBE that Larry Ellison used to denigrate his competitors for writing checks, not code. But he saw the consolidation trend happening in the ERP space before any of the other players and acted by hiring Charles Philips (Chuck back then) to execute a successful M&A strategy. The $10B Peoplesoft acquisition in 2005, Oracle’s first real large M&A move, set off a trend in enterprise software that did a few things.

First, it began the move to solidify Oracle’s position further up the stack. It also set Dave Duffield and Aneel Bhusri off to create a next generation cloud software company in Workday – which you can see in the chart has a Net Score up there with ServiceNow, Salesforce and Coupa. And it also led to the development of Oracle Fusion middleware, which was designed as the integration point for all these software platforms that Oracle bought.

This is important because Oracle is moving everything into its cloud and you can see that in its on-prem Net Score which puts it deep into negative territory.

Now SAP on the other hand has much higher Net Scores than Oracle. And you can see it’s acquired SaaS properties like Ariba, Concur and Success Factors which have decent momentum. But SAP is not without its challenges.

With SAP, HANA is the answer to all its problems. The problem is that it’s not necessarily the answer to all of SAP customers’ problems. Most of SAP’s legacy customers run SAP on Oracle or other databases. HANA is used for the in-memory query workload but most customers will continue to use other databases for their systems of record. So this adds complexity. But admittedly, HANA is very good at the query piece.

However SAP, never did what Oracle did with Fusion, which as you might recall took more than a decade to get right. HANA is SAP’s architectural attempt to unify the SAP portfolio and get off Oracle but it is many years away and it’s unclear when or even if they’ll ever get there.

Drilling into Net Score / Spending Velocity

Below is a look at a similar set of companies in the enterprise applications space, but we wanted to show you this view because it gives you a detailed look at ETRs Net Score approach and tells us a few more things. Remember this is a survey of technology buyers with nearly 1,200 responses.

The chart above shows the Net Score granularity for the enterprise players we were just discussing. Net Score is actually more detailed than what we described earlier. It is derived from a calculation comprising responses in five categories:

- Lime green is new adoptions.

- Forrest green is growth in spend of 6% or more.

- Gray is flat.

- Pink is a budget shrink of 6% or more; and

- Red is retiring the platform.

Net Score is calculated by subtracting the sum of 4 & 5 from the sum of 1 & 2.

So what this tells us is that there’s a big fat middle of flat spending in these accounts. The lime green or new adoptions is pretty small but you can see NetSuite jumps out for new adoptions as they’ve been very aggressive going after smaller and mid-sized companies. And Coupa, the spend management specialist, shows reasonably strong new adoptions.

ServiceNow is interesting to us. It doesn’t show many new adoptions. They’ve landed the ship and have really penetrated larger companies. And while the new adoptions are not off the charts the spending more category (forrest green) is very very strong at 46%. And the other really positive thing for ServiceNow is there’s very little red. This company is a beast.

Salesforce similarly does not show strong new adoptions but 40% of its customers plan to spend more in the 2nd half of 2020. For a company the size of Salesforce, that is pretty impressive.

Workday has a similarly strong spending profile.

And at the bottom of the chart you see a fair amount of red as we saw on the XY graph.

Another View of Net Score.

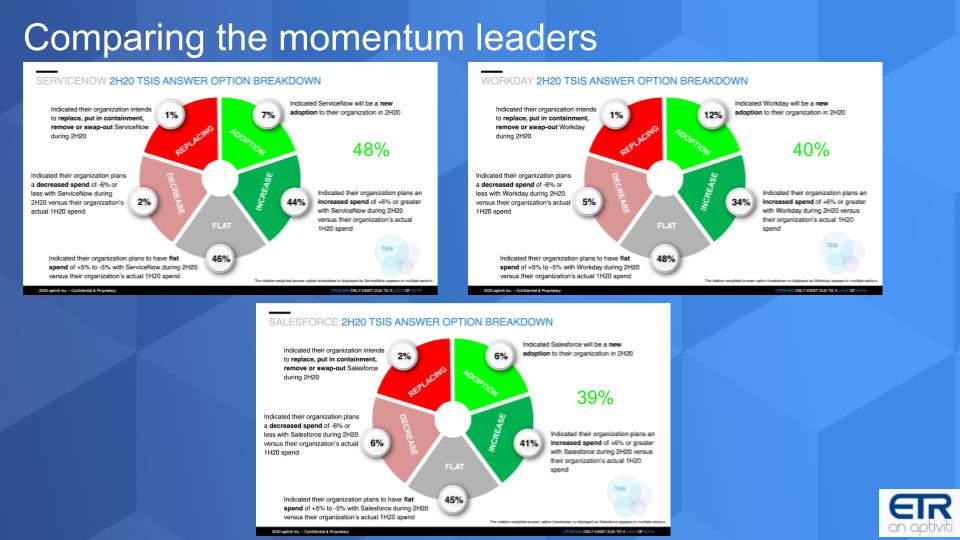

The slide below shows a zoom in for selected companies and expands the scope beyond just enterprise applications. The charts show Net Scores across all the company’s portfolio and reflects a macro view of spending momentum in all categories. This is a zoom in, which shows those bar charts but in a pie format for ServiceNow, Workday and Salesforce. And we’ve put the Net Score for these three in green.

ServiceNow at 48% is very good for a company headed toward $5B. Same with Workday at 40% a company of similar size. And Salesforce has a comparable Net Score and is significantly larger revenue-wise– roughly 4x those two.

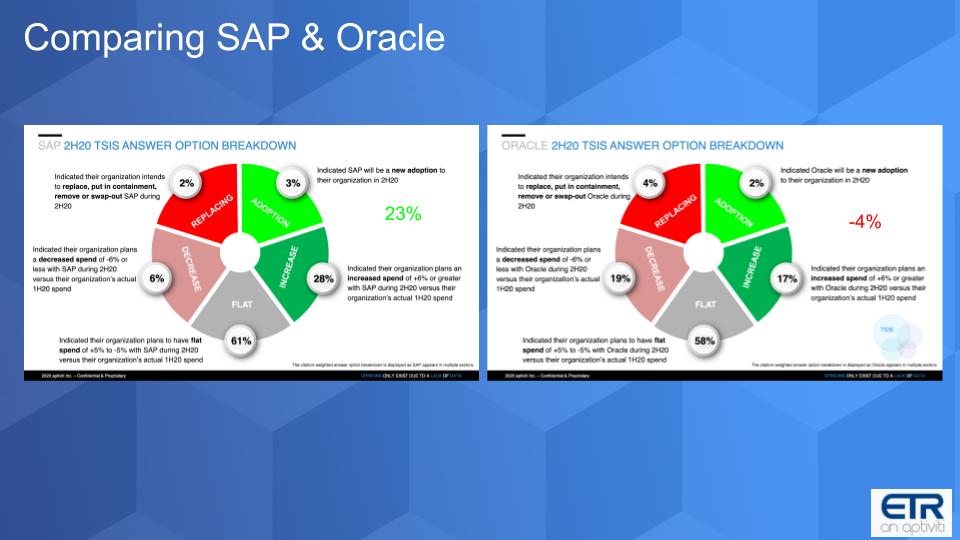

Below is the same view for SAP and Oracle. So you can see, substantially lower than the momentum leaders in terms of Net Score. These are much larger companies. SAP is about $33B and Oracle closer to $40B in revenue. But Oracle especially is seeing some headwinds from organizations spending less, which drags its Net Score down. BUT – you’re not seeing much replacement in Oracle’s base because as we said at the top, these systems are fossilized and many are running on Oracle. And the vast majority of mission critical workloads are especially running on Oracle.

Also remember this isn’t’ a revenue weighted view. Oracle charges a steep license premium for its database, based on the number of cores and it has a big maintenance stream. So while its Net Score is weak, it’s cash flow is not.

Summarizing the Enterprise Applications Market

We have here a very large and mature market but the semi-modern SaaS players like Salesforce, ServiceNow and Workday have gone well beyond escape velocity and solidified their positions as great software companies. Others are trying to follow suit and compete with the biggest of the bigs i.e. SAP and Oracle. We didn’t talk much about Microsoft but, as always, they show up prominently.

What we think is interesting are the competitive dynamics we talked about earlier. The newer SaaS leaders are disrupting Oracle and SAP but they also are increasingly bumping into each other. ServiceNow, for example, has HR and they say they don’t compete with Workday and that’s true. But they do eye each other carefully and angle for account control. Same thing with Salesforce. It’s the software mindset. The bigger software companies get, the more they think they can own the world. Because it’s software and if you’re good at writing code and you see a profitable opportunity that can add value for customers you tend to go after it.

We didn’t talk much about M&A but that will continue here. Especially as these companies look for TAM expansion opportunities bringing in new capabilities around data, analytics, ML, AI and the like. And industry specialization. You’ve seen Oracle pick up vertical industry plays, as have IBM and others. And as digital transformation continues, you’ll see more crossing of the industry streams.

The disruption isn’t blatantly obvious right now other than the SaaS clouds going after SAP and Oracle. It’s because these companies are deeply entrenched in their customer organizations and change is risky. But the cloud developer, open source, API-based trend could lead to disruptions but we wouldn’t expect that until the second part of this decade as cloud ecosystems evolve.

Remember these episodes are all available as podcasts – please subscribe. We publish weekly on Wikibon.com and Siliconangle.com so check that out and please do comment on the LinkedIn posts we publish. Don’t forget to check out ETR for all the survey action. Get in touch on twitter @dvellante or email david.vellante@siliconangle.com. And remember, Breaking Analysis posts, videos and podcasts are all available at the top link on the Wikibon.com home page.

Thanks everyone, be well and we will see you next time.

Watch the full video analysis: