In the next 3-5 years, we believe a set of intelligent data apps will emerge requiring a new type of modern data platform to support them. We refer to this as a sixth data platform. In our previous research we’ve used the metaphor “Uber for everyone” to describe this vision; meaning software-based systems that enable a digital representation of a business. In this model, various data elements, such as people, places and things, are ingested, made coherent and combined to take action in real time. Rather than requiring thousands of engineers to build this system, we’ve said this capability will come in the form of commercial off the shelf software.

In this Breaking Analysis, we explore the above premise and welcome Ryan Blue to this, our 201st episode. Ryan is the co-creator and PMC chair of Apache Iceberg. He is a co-founder & the CEO of Tabular, a universal open table store that connects to any compute layer, built by the creators of Iceberg.

[Note: We recognize that there are other formats such as Hudi and Delta that will contribute to future data platforms. For this Breaking Analysis our main focus is on Iceberg and its disruptive potential].

TL;DR

The Evolution of Open Storage Management and Its Impact on Modern Data Platforms

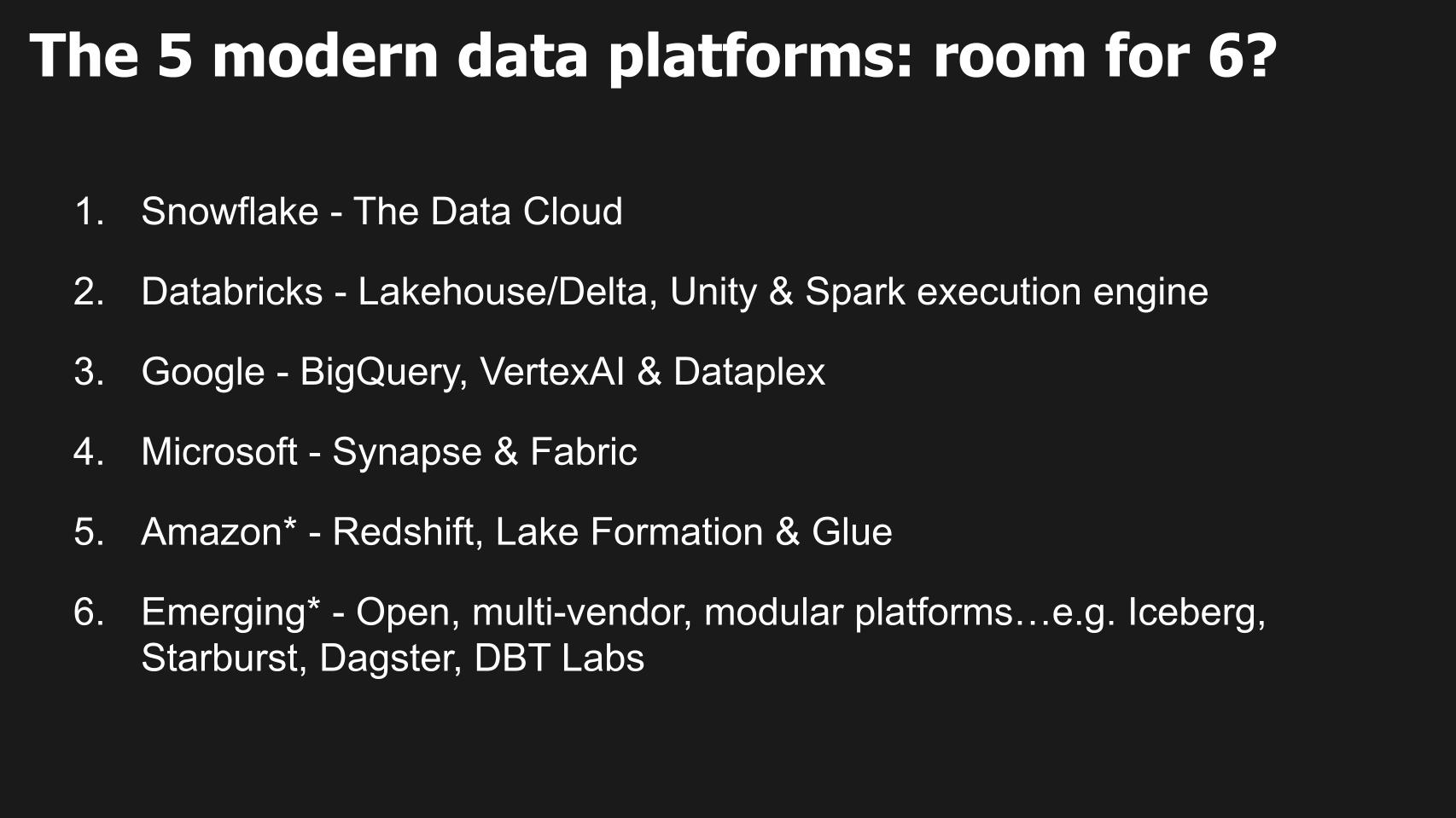

Figure 1: The five modern data platforms and the products that comprise their systems along with some examples of contributors to the sixth data platform.

*AWS and emerging modular platforms are today largely bespoke products and tools that have the potential to become platforms.

Introduction

Open storage managers, like Tabular and its use of Iceberg, in combination with other tools and products, have the potential to revolutionize the architecture and business models of existing data platforms. We use the term “platform” to represent an architecture comprising multiple products and tools that work in combination. Platforms have more comprehensive problem solving objectives than individual products and are more extensible in a variety of dimensions (see this more detailed description by Blaise Hale).

Traditional Data Platforms Create Lock-in by Owning the Data

Historically, data platforms control customer data. Even though storage and compute may be architecturally distinct, they are effectively integrated. This integration means that owning the data gives platform vendors control over various workloads. This control spans business intelligence, data engineering, and machine learning due to the concept of data gravity and the need to share via pipelines.

The Shift Towards Open Data Storage Increases Competition

Independent management of data storage and permissions gives customers more optionality and forces vendors to compete for every workload based on the business value delivered, irrespective of lock-in.

Data Sharing Redefined

Data sharing within a single enterprise in the future necessitates the ability to read and write a single instance of the data using an open storage format. This forces multi-vendor standards for data sharing between enterprises.

Examples of Players of the Emerging Modern Data Platform & Future Competitive Landscape

- Snowflake might excel as the most performant business intelligence service.

- dbt Labs could manage data pipelines using tools like PySpark or Spark SQL on AWS EMR, offering cost efficiency.

- Databricks might be the most functional for feature engineering and ML training tasks using the same shared data.

- Even business intelligence tasks face competition. Tools like dbt’s semantic layer and Atscale can cache regularly queried metrics while maintaining permissions in sync with the DBMS.

- Shift in governance: The ownership and management of permissions has shifted away from being the sole responsibility of the DBMS.

Challenges Ahead

A significant challenge with modular storage is determining the optimal balance of governance between database management systems (DBMS) or query engines and open storage platforms like Iceberg and other open table formats.

Key Issues Posed by George Gilbert

- Will modular components such as Iceberg and Starburst complement the incumbent platforms or will customers use them to assemble a full alternative?

There’s a big delta between the data platforms we have today and that vision of the real-time intelligent data app. And the biggest questions we have are: 1) Are components such as Iceberg going to offer plug-in alternatives to components of today’s data platforms? Or 2) Will customers use them to compose and assemble an alternative data platform? And 3) What are the trade offs between an open modular version, if it’s possible, and the integrated, typically simpler but generally more expensive offerings?

Ryan Blue’s Opening Comments

- The incumbents are already becoming more modular. They’re not monolithic systems.

- Snowflake is opening up for access by Spark, for example.

- The big question is how long until the components from different vendors work together more easily.

So when when you guys talk about these platforms I think that we’ve already seen the modularity starting to creep in. If you look at just the last three of these Google, Microsoft, Amazon and to a certain extent Databricks and Snowflake coming on board, we’re already seeing that these are not platforms that are a single system, like a single engine, a single storage layer.

These are already complex things made of very diverse products. So you’re already seeing engines from the Hadoop space and Microsoft Synapse, right? It’s SPARC, right? SPARC is also part of the Databricks platform. A huge imperative for Snowflake these days is how do we get data to people that want to use Spark with it. And so I think we’ve already started to see these systems decomposing and becoming a collection of projects that all work together rather than one big monolithic system.

The question has to do the with all the VC investment that you were alluding to. How how long are we going to wait until all of those components work together really well? And what needs to change.

[Listen to Ryan Blue’s opening comments regarding the five modern data platforms].

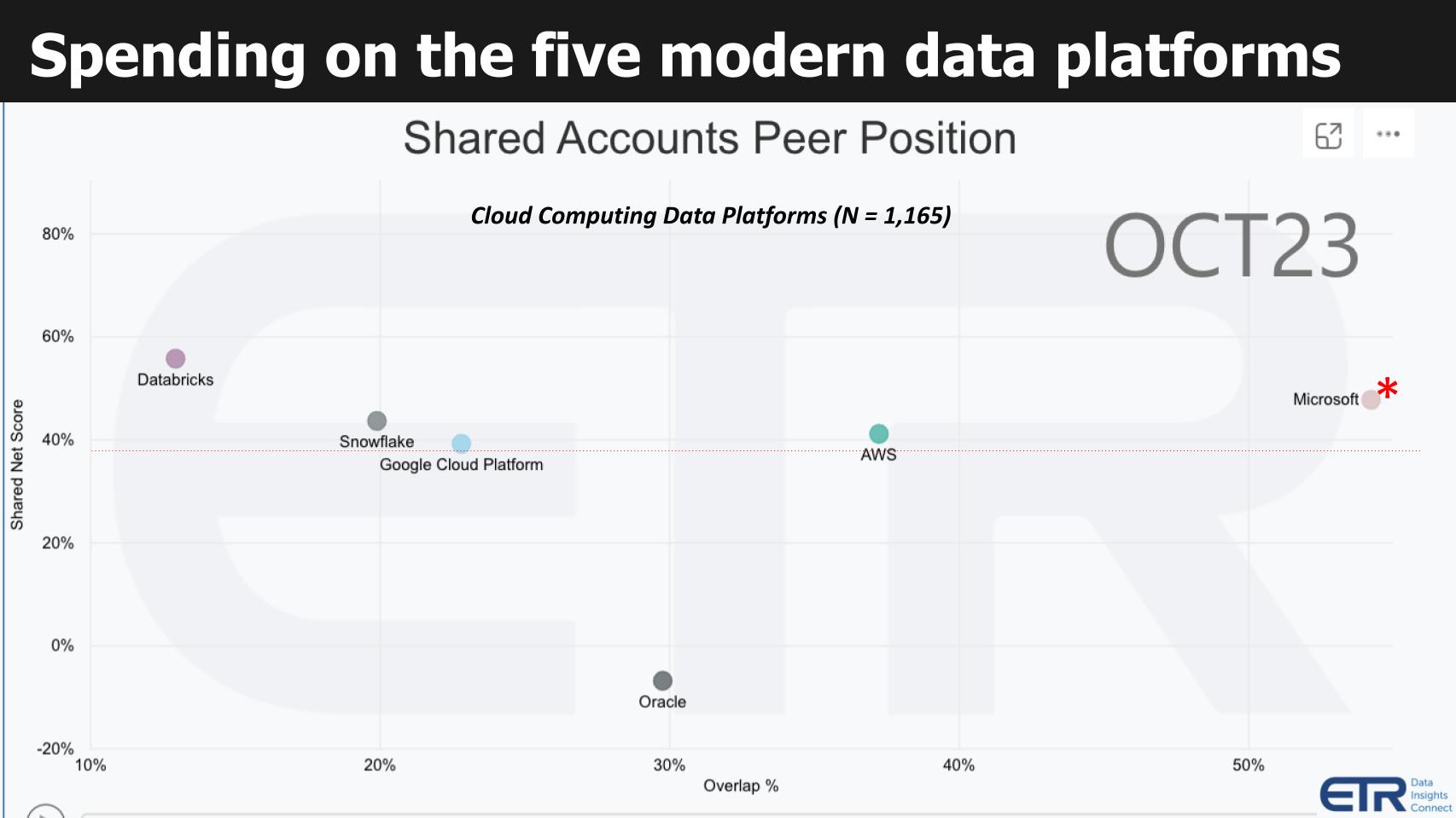

Assessing the ETR Spending Data on the Big 5 + Oracle

Figure 2: ETR’s Technology Spending Intentions Survey shows spending momentum and market presence for the major data platform vendors. X axis represents account penetration. Y axis represents spending momentum.

The graphic above shows spending data within the cloud for the leading data platforms. This specific cut of the data is for database and data warehouse offerings filtered by cloud customers. We include Oracle in deference to the database king, which continues to aggressively invest adding capabilities to its data platforms. It also provides relative context because Oracle has a sizable presence and is mature.

The Y axis shows Net Score or spending momentum. It is a measure of the net percent of customers in the survey (N=1,165 cloud customers) spending more on a specific vendor platform. The X axis labeled as Overlap is an indicator of presence in the data set and is determined by the N’s associated with a specific vendor, divided by the total N of the sector. Think of the horizontal axis as a proxy for market presence.

The red dotted line at 40% is an indicator of highly elevated spending velocity on a platform.

The following key points are notable:

- Virtually all data platforms have seen spending headwinds due to the macro economic environment.

- Microsoft is ubiquitous as shown on the X axis due to its large installed base. There’s probably lots of SQL Server finds its way into the survey (hence the red asterisk).

- Databricks has the highest Net Score but is relatively nascent because its SQL data warehouse is a more recent market entry.

- Over the past several quarters, Snowflake has continued to penetrate the market on the X axis but its Net Score has decelerated dramatically. Based on an analysis of the data, this is due not from customers spending less or churning but rather an increase in the percentage of Snowflake customers shifting from a posture of spending more to one of flat spend.

- AWS’ bespoke set of database services continues to maintain a strong Net Score and AWS’ presence in the data remains impressive.

- Oracle as you can see above has a prominent presence but is essentially living off its installed base.

Remember this data does not represent spending levels. Rather it is is measure of the percent of customers taking specific spending actions (i.e. add new, spend more, flat spend, spend less, churn).

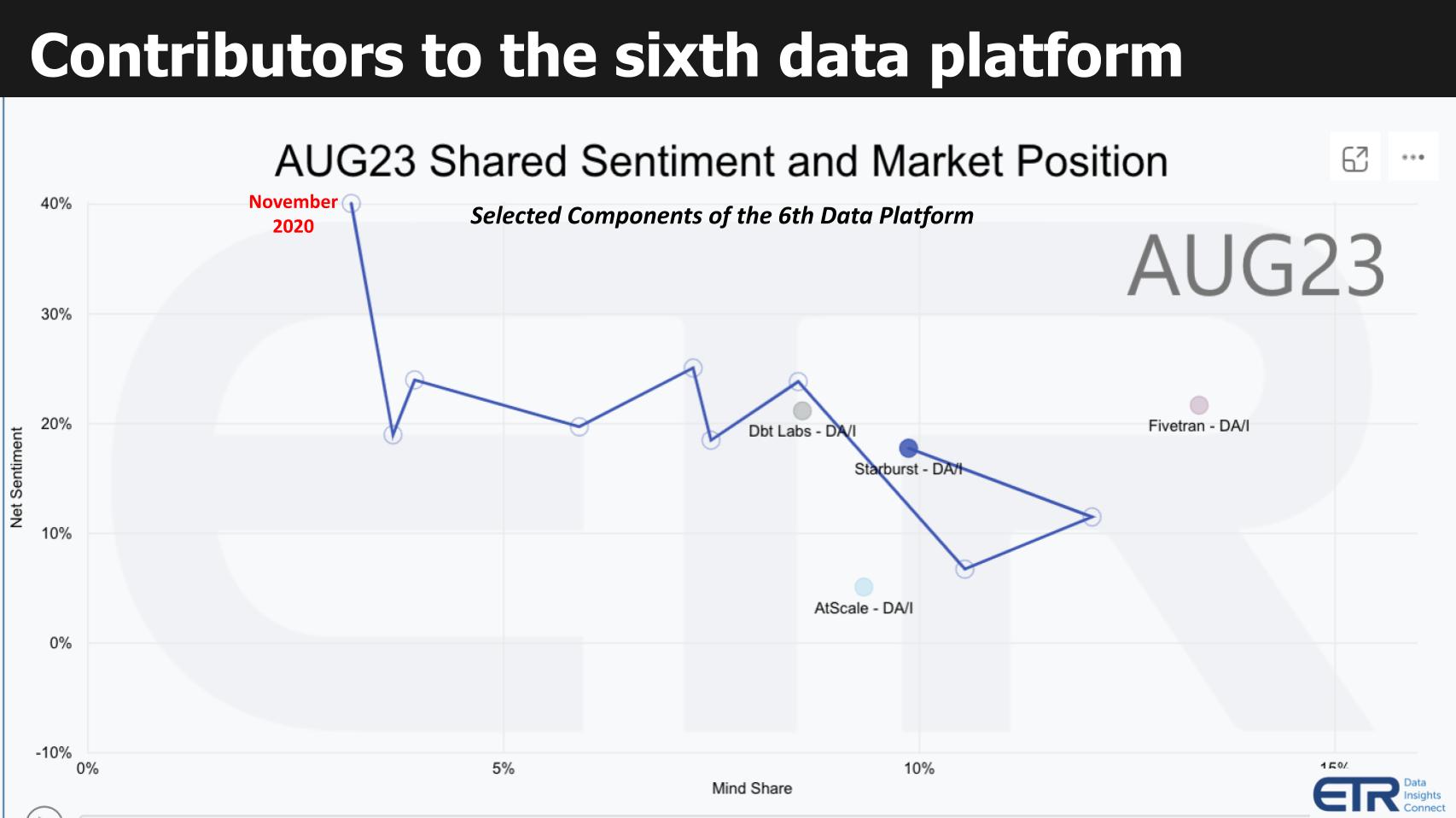

Emerging Components of the Sixth Data Platform

Figure 3: ETR’s Emerging Technology Survey (ETS). X axis is mindshare. Y axis is net sentiment.

Another capability of ETR’s data set is seen above from the ETS survey which measures the sentiment and mindshare for non-public companies. In the graphic above we chose to highlight four contributing players to the sixth data platform including Fivetran, dbt Labs, Starburst and Atscale.

The squiggly line at Starburst shows the positive progress since November of 2020. Note that each of these four would show a similar trajectory which is one reason why we chose to highlight them.

- Net sentiment is a measure of the net percent of customers that intend to engage with the platform. It “nets out,” for example, customers that have no intention of engaging.

- Among components of an emerging 6th data platform, Starburst, dbt, Fivetran, and Atscale show growing mindshare and have respectable or strong sentiment.

- We see companies like these as important contributors and indicators of an emerging sixth platform. Whether they have the funding, vision, execution ethos and staying power to become a sixth platform is unclear at this time.

The Modular Decomposition of Integrated Data Platforms and the Emergence of Multi-Vendor Modules

Key Issues Posed

- Are the integrated data platforms modularizing or are a bunch of multi-vendor components emerging – or both?

- What use cases are drawing these multi-vendor components into the market?

- Snowflake started out as an integrated system but added progressively deeper Iceberg support – what does this imply?

- Do markets like this start with integrated products and then modularize and what does that mean for the future of data platforms?

Ryan Blue’s commentary on the data presented above and these key issues:

The integrated vendors supported open storage because they wanted access to more data

But once customers can use open formats, their data is no longer trapped in vendor silos.

If you take both Databricks and Snowflake, they want access to all of the data out there. And so they are very much incentivized to add support for projects like Iceberg. Databricks and Snowflake have recently announced support for Iceberg, and that’s just from the monolithic vendor angle, right? I don’t think anyone would have expected Snowflake to add full support for a project like Iceberg two years ago.

That was pretty surprising. And then if you look at the other vendors, they’re able to compete in this space because they’re taking all of these projects that they don’t own and they’re packaging them up, as, you know, out of the box data architecture. One of the critical pieces of this is that we’re sharing storage across these projects, and that has for the data warehouse vendors like Snowflake, the advantage that they can get access to all the data that’s not stored in Snowflake. But I think a more important lens is from the buyer or the user’s perspective where no one wants siloed data anymore and they want a essentially what what Microsoft is talking about with Fabric. They want to be able to access the same datasets through any different engine or means, whether that’s a Python program on some developer’s laptop or a data warehouse at the other end of the spectrum like Snowflake. So it’s very important that all of those things can share data. Of course, that’s that’s where I’m coming from.

That’s what I’m most familiar with. You know, if you go above the the layer of those engines, I’m less familiar, but we even see that that consolidation with integrations like Fivetran writing directly to Iceberg tables.

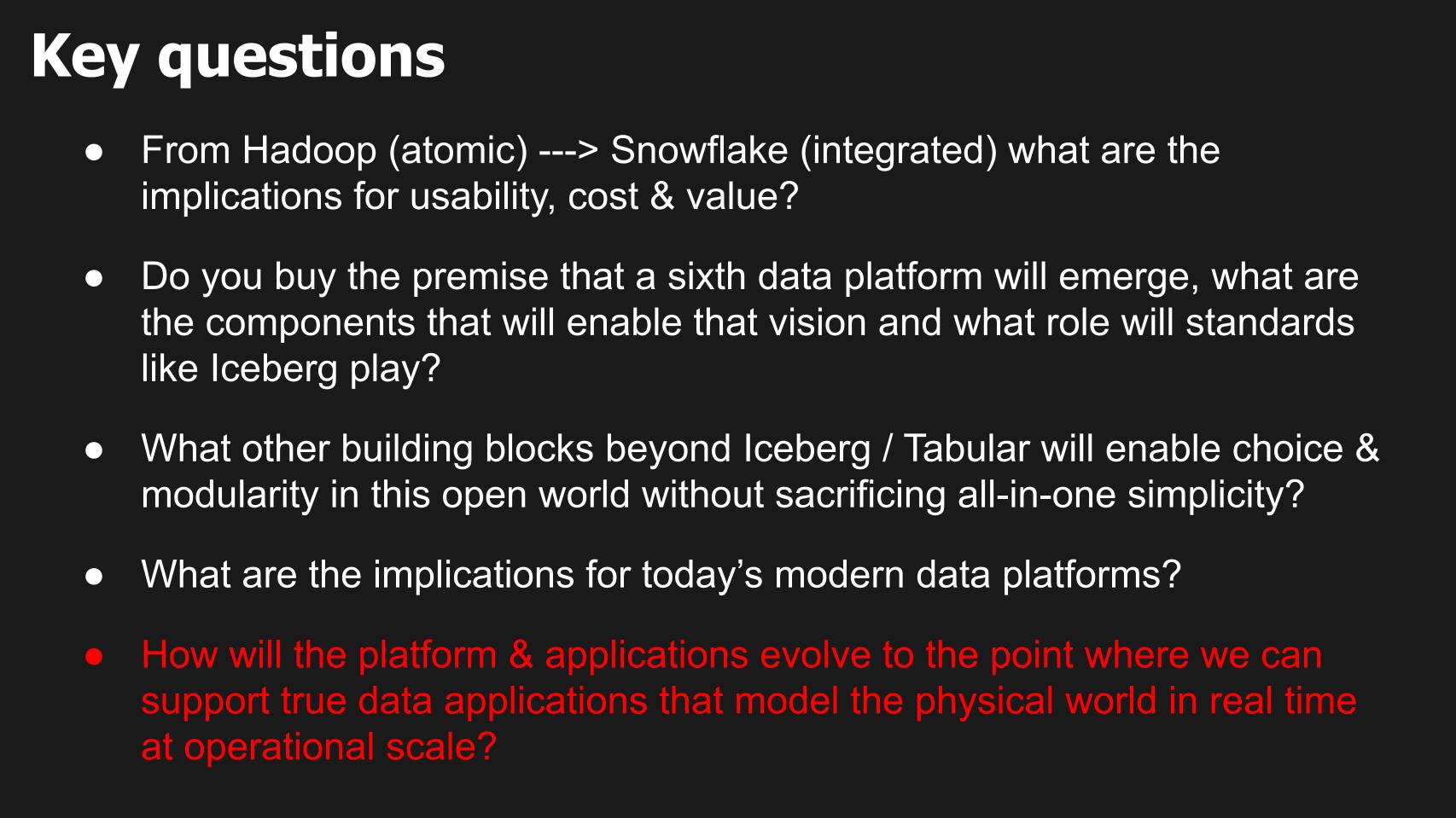

Five Key Questions Related to the Emergence of a Sixth Data Platform

In this next section we review critical questions that we feel are central to understanding the emergence of a sixth data platform. We’ll combine a summarization of comments with verbatim statements and provide video links to specific sections of the conversation.

Figure 4: Key questions Ryan Blue of Tabular addresses about multi-vendor data platforms with open storage.

In the ever-evolving world of data platforms, we saw the journey from the atomic and fragmented Hadoop ecosystem to the highly integrated systems of today, exemplified by Snowflake. We see a future of more pivotal shifts. Recent trends raise pivotal questions about usability, cost, and value in the data landscape.

- From Hadoop to Snowflake: Hadoop’s complex architecture was service-heavy and required specialized expertise, often from external consultants or in-house experts in proverbial “lab coats.” Despite its promise, Hadoop struggled to gain substantial traction due to multiple factors:

- Complexity.

- Disruption from Apache Spark.

- The cloud’s increasing dominance.

Consequently, the data industry gravitated towards more integrated platforms like Snowflake.

- The Snowflake Proposition: With its integrated approach, Snowflake presents a unique value proposition. However, insights gleaned from the recent Snowflake Summit suggest some tension:

- Ecosystem partners and customers increasingly indicate that organizations are conducting data engineering work outside of Snowflake, primarily due to cost concerns.

- Snowflake counters this by emphasizing the full value attained when such operations are performed inside Snowpark, championing the integrated total cost of ownership (TCO) benefits of Snowflake’s approach.

- The Current Landscape:

- ETR data points to a recent deceleration in Snowflake’s momentum, especially concerning the percentage of customers spending more and new customer adds.

- Yet, Snowflake’s integrated value proposition remains a strong selling point.

Central Debate: What are the ramifications of this shift for usability, cost, and value? A belief in an open, modular world is essential, and the question remains: How will the intersection of integration and modularity define the future of data platforms?

As we delve deeper into this discussion, the challenge is to dissect the balance between an open modular system and the benefits of an integrated approach. As well, can open modularity simulate the benefits of an integrated system?

How these elements shape the future trajectory of data platforms remains a topic of fervent debate and exploration.

Ryan Blue’s Commentary

- Storage shared by multiple products is the biggest change in DBMS architecture and business model in more than a decade.

- Even though storage and compute were architecturally separate, they were de facto integrated by the vendors.

- Once a vendor owned your data, they owned all your future workloads.

- The new modularity inherits the spirit of the Hadoop world where you assumed batch, streaming, and ad-hoc engines all shared the same data.

- That shared data storage is the assumption behind Iceberg.

I do believe in the modular world. I think that the biggest change in databases in the last ten years easily, if not longer, is the ability to share storage underneath databases.

And that really came from the Hadoop world because those of us, we weren’t wearing lab coats, but those of us over there, we sort of had as an assumption that many different engines, whether they’re streaming or batch or ad hoc, they all needed to use the same data sets. So that was an assumption when we built Iceberg and other similar formats.

And that’s what really drove this change to be able to share data. Now in terms of cost and usability, that is a huge disruption to the business model of basically every established database vendor who has lived on the Oracle model. And it’s not really even the Oracle model. It’s just that storage and compute have always been so closely tied together that you couldn’t separate them.

And so by winning workloads, winning datasets, you also were winning future compute whether or not you were the best option for it, best option meaning what people knew how to use best in terms of performance and cost and things like that. And so the the shift to sharing data means we can essentially move workloads without forklifting data, without needing to worry about how do we keep it in sync across these products, how do we secure it.

All of those problems have been inhibitors to moving data to the correct engine that is the most efficient or the most cost-effective, etc. So I think that this shift to open storage and independent storage in particular, is going to drive a lot of that value and cost efficiency.

[Watch and listen to Ryan Blue’s commentary on sharing underlying storage].

Key Issue: What’s the Ideal Governance Approach in a Shared Storage Model

George:

- Once you have shared storage separate from compute, something has to manage transactional consistency, permissions, and broader governance policies.

Let me follow up on that because you said two things in there which were critical. With shared storage you compete for what’s the best compute for that workload. But someone still has to govern that data.

And let me let me define what I mean by governance. It’s got to make sure that multiple people are reading and writing. And I don’t mean just a single table because you might be ingesting into multiple tables. Someone’s got to apply permissions and the broader governance policies. So, it’s not just enough to say we’ve standardized the table format.

Something has to make sure that everything’s copacetic, to use a technical term. What are those services that are required to make things copacetic, whether it’s transactional support, whether it’s permissions or broader governance? Tell us what you think needs to go along with this open data so that everyone can share it.

Ryan:

- Data lakes have a massive gap.

- In order to share data between any compute engine, storage now has to own permissions.

That’s a great question.

I think that access controls are one of the biggest blind spots here. So, the data lake world, which is essentially what I define as the Hadoop ecosystem after it moved to the cloud and started using S3 and other object stores, is a massive gap for the data lakes and for shared storage in general. You know, spoiler or disclaimer, this is what my company Tabular does.

We provide this independent data platform that actually secures data, no matter what you’re using to access it, whether that is a Python process or Starburst, for example. So I think that that is a really critical piece. What we’ve done is actually taken access controls, which, if you have a tied together or glued together storage and query layer, those go in the query layer because the query layer understands the query and can say, you’re trying to use this column that you don’t have access to. In the more modern sixth platform that you guys are talking about that has to move down into the storage layer in order to really universally enforce those access controls without syncing between Starburst and Snowflake and Microsoft and Databricks and whatever else you want to use at the query layer. Right?

[Watch and listen to Ryan Blue explain how Tabular is addressing the governance challenge of shared storage].

Dave:

- Iceberg is clearly a foundational component of this sixth data platform.

- But the rest still seems a little fuzzy.

You started getting into sort of the components. Obviously Iceberg is one of them that is going to enable this vision. And the role that Iceberg plays is it sounds like you’re sort of aligned with that. There may be some fuzziness as to how that all plays out, but this is something that George and I definitely want to explore.

Ryan:

- The sixth data platform is probably not going to be a distinct product.

- All incumbent vendors are probably going to standardize on certain components

- If Snowflake and Databricks can agree on Iceberg, that’ll likely be the standard for everyone

- We still have to standardize things like views, encryption, catalog interaction, etc.

- The sixth data platform is going to be all players sharing data within the context of the same architecture.

Yeah, I think that the sixth data platform is as good a name as you can come up with, right? I don’t think that we know what it’s going to be called quite yet. I don’t know that I would consider it distinct because I think what’s going to happen is all five of those players that you were talking about, plus Oracle plus IBM and others, are going to standardize on certain components within this architecture.

or

Certainly shared storage is going to be one. And I believe that Iceberg is probably that shared storage format because it seems to have the broadest adoption. You know, if Databricks and Snowflake can agree on something, then that’s probably the de facto standard. We are still going to see what we can all agree on as we build more and more of those standards in the Iceberg community.

We’re working on shared things like views, standardized encryption, you know, ways of interacting with a catalog, no matter who owns or runs that catalog. And I think those components are going to be really critical in the sixth data platform because it’s going to be an amalgam of all of those players sharing data and sharing or being part of the exact same architecture.

- As the data platform evolves to support more real-time or operational applications, we can’t count out Oracle.

- But applications that look more like Uber are still some years out.

- We still need to see relational knowledge graphs and transactional relational document databases mature.

And, you know, George, you and I debate quite frequently what about Oracle? And and to Ryan’s point, these existing five are clearly evolving. You’ve seen Oracle. I mean, Oracle, somebody announces something and then Oracle, Larry will announce it and act like they invented it. And so they’ve maintained at least their spending on R&D and preserved their relevance, which is a good thing.

But but I think, George, the thing that we point to is the real-time nature that Uber for all, which we feel like many of these platforms are not in a position to capture, and that’s maybe a little more forward-thinking or some years out.

But the idea that we’ve talked about things like the expressiveness of graph databases with relational query flexibility. Or we’ve seen products like Fauna being able to sync data across multiple documents in real time. Those are some of the things that we’re thinking about and why we feel that some of the five are going to be challenged.

How to Maintain Data Integrity. Which Layer of the Stack is Responsible?

George:

- What goes in the storage manager?

- How do you manage transactional integrity?

- How far up the stack do you go?

You’re talking, Dave, now, closer to real world intelligent data apps that we were describing with Uber for all. In that world you’ve got digital twins fed in real-time.

And let me sort of map that back to Ryan and where we are today. Do you see a path, Ryan, towards adding enough transactional consistency or a transactional model that you can take in real-time data that might be ingested across multiple tables and you understand windows. At the same time, you can feed a real-time query that’s looking at historical context.

And then I guess what I’m asking is how far up this stack you’re going. The other part is related to who’s ensuring data integrity and essentially access integrity? Where are the boundaries?

Are there boundaries? Is it going to be all in the storage manager? Enlighten us about the integrity and then how you start mapping that to higher-level analytics. And in digital representations, digital twins, it’s a big question but help us on it.

Ryan:

- Iceberg and Delta already have transaction protocols.

- But table updates currently have an update latency challenge that favors throughput.

- We still have to figure out how to merge streaming data with historical data.

Yeah. So I think you you brought up a couple of different areas, and I’ll address those somewhat separately.

So first of all, in terms of transactions, that’s one of the things that the open data formats, and I’m including just Delta and Iceberg in that, what they do is essentially have a transaction protocol that allows you to safely modify data without knowing about any of the other people trying to modify or read data there.

The two formats do that and are open source. So that I think is a solved problem. Now, the the issue that you then have is they do that by writing everything to an object store and cutting off a version, which is inherently a batch process. And that’s where you start having this mismatch between modern streaming, which is a micro-batch streaming operation and efficiency. Because you need to, you know, at each point in time commit to the table, every single commit incurs more work or something like that.

So in order to get towards real-time, you’re simply doing more work and you’re also adding more complexity to that process. So I think that essentially you’re seeing cost rise at least linearly, if not exponentially, as you get closer and closer to real time. I think that the the basic economics of that makes it infeasible for in the long term to really make that real-time something that you’re going to use 100% of the time.

And this is the age-old tradeoff between latency and throughput. If you want lower latency, you have lower throughputt. If you’re willing to take higher latency, you have higher throughput and, thus better efficiency. So I think that where we need that streaming and the sort of constantly fed data applications, those are going to get easier to build, certainly.

But I think that after those challenges is probably where you’re going to go and store data, make it durable for this sixth data platform. And it’ll be interesting to see the interplay between those real-time sort of streaming applications and how we sort of merge that data with data from the lake or warehouse.

What are the Building Blocks Beyond Tabular and Iceberg to Deliver Comparable Value to an Integrated System…A Netflix Example

Dave:

- We want to explore the belief that data applications that orchestrate the real world like Uber are going to be mainstream.

- What are the missing building blocks, especially with respect to today’s modern data stack?

We think about when we had Uber on, they were sort of describing how they attack that trade-off not as a bespoke set of applications but combining different data elements – riders, drivers, ETAs destination fares, etc. But you could see sort of industry 4.0 applications. So the potential is there but your premise has always been it’s it’s going to apply to mainstream businesses.

I think we’ve hit on all of these questions at least in part. Ryan, what are the building blocks beyond Iceberg and Tabular that are going to enable choice and modularity in this world? What are the implications for today’s modern data platforms?

And we’re talking about how applications will evolve where we can support this physical world model? I think I’m hearing from from Ryan, George, that if that’s kind of somewhat limited, at least today, in terms of our visibility and scope of the activity is going to be really along these analytic applications. But you’re seeing a lot of analytic and transaction activity coming together.

George:

- It sounds like if you want a real-time system of truth, you’re going to use an operational database?

- And you’re going to use a separate historical system of truth?

Let me let me follow up on that, Dave. Ryan, what you were saying, you get only so far with trying to get asymptotically to approach greater efficiency in terms of real-time, ingest. What I’m inferring from what you’re saying is if you want a real-time system of truth, you’re going to use an operational database.

If you want a historic system of truth that’s being continuously hydrated, that might be a separate analytic system.

Is my understanding right? Is that how you see the platform evolving, where you’re going to have a separate operational database and a separate historical system of truth, a term from Bob Muglia?

Ryan:

- The way we are tearing down the data silos between platforms is essentially to trade-off some of the machinery that would support real-time applications – at least in the short-term.

- We won’t merge those worlds any time soon. But we can make it easier to use real-time and historical systems together.

- We did that at Netflix. The developer could get data that was milliseconds old as well as two years old nearly seamlessly.

So, yes, I think I would subscribe to that view, at least in the short term.

The the way that we are tackling the challenge of tearing down the data silos between these data platforms that you know, the major players that you had up on the earlier slide, the way that we’re doing that is to essentially trade off some of the machinery that would go to support those real-time, sub-second latency applications.

So I don’t think that that we’re going to approach merging those two worlds any time soon. However, I’m a big believer in usability, and it’s not that we need to merge those two worlds, it’s that it needs to appear like we are, right? We can have separate systems that make a single use case work across that boundary. Netflix did this, I think classically with logs coming from our applications. We had telemetry and logs coming from runtime applications that are powering the Netflix product worldwide.

We need access to that information with millisecond latencies. Iceberg was not a real-time system that provided that. We kept it all in memory because that was what made the most sense. But absolutely for historical applications we did. And to a user that tradeoff was seamless. So you would go and query logs from your running application and you’d get logs that are fresh to the millisecond.

But you could also go back in time two years, you know, things like that. Those are the applications that are coming.

[Watch and listen to Ryan Blue discuss how to tear down data silos using a Netflix example].

How to Hide the Differences Between Real-time and Historical Domains at the Developer Level

George:

- How were you able to hide the difference between real-time and historical domains from the developer at Netflix?

How did you provide that seamless simplicity to the developer so that they didn’t know they were going against two different databases? How could building a data app hide of those different data storage domains?

Ryan:

- At Netflix the application back-end was responsible for receiving all the logs almost in real-time and managing the hand-off between Iceberg for historical data and in-memory for real-time data.

Through building a data app that was a ton of work and understood both of those data storage domains. So the app or the back end, at least, was responsible for receiving all of the logs in a almost real time and for storing them and managing that handoff between in-memory and iceberg.

George:

- Help us understand exactly what governance data, including permissions and technical metadata, goes into storage.

- What metadata stays outside storage?

A follow up question for Ryan. I just want to understand what has to go down into storage (from the DBMS), like permissions and maybe technical metadata that is stored as part of Iceberg.

You know, like what what the tables are, what columns are there? You know, what tables are connected in this one repository or if I don’t even know if it’s called a database and then does that interoperate with a higher level open set of operational catalogs like like a Unity (from Databricks) or today what’s inside Snowflake?

In other words, is there is there a core set of governing metadata that’s associated with the storage layer and then everything else, all the operational metadata above that is interoperable with these open modular compute engines?

Ryan:

- We distinguish between technical metadata to read and write Iceberg data and higher-level operational metadata that’s separate.

In terms of Iceberg, we do make a distinction between technical metadata required to read and write the format properly and higher level metadata.

And that higher level metadata we think of as business operations info, even things like access controls and our back policy and all of that. That’s a higher level that we don’t include. And even the Iceberg open source project, the technical metadata is quite enough to manage for an open source project.

Implications for Today’s Modern Data Platforms

George:

- The business model of data management changes. Vendors have to compete for every workload.

- Is metadata management (an operational catalog) the new gateway or chokepoint for data management?

We need to build higher level structures on top of that. The reason I ask, Ryan, this is critical because you identified how the business model of all the data management vendors changes when data is open and they don’t get to attach all workloads just because they manage that data. Now they have to compete for each workload on price and performance.

So my question is this. I go back to this question about who keeps the data copacetic. The more metadata that you have essentially governs all that data. It sounds like that’s the new gateway. Is that a fair characterization or is there no new gateway?

Ryan:

- Access controls and certain governance operations need to move into the storage layer catalog that is standardized.

- Beyond that, it’s still unsettled.

- But we need to solve the problem of customers copying data between vendor platforms today.

I think that it is absolutely critical to have a plan around that metadata.

We don’t really know how far we’re going to go down that road. So I think that today there’s a very good argument that access controls and certain governance operations need to move into a catalog and storage layer that is uniform across all of those different methods of access and compute providers. What else goes into that, I think is is something that we’re we’re going to see.

I think that that is by far the biggest blocker that I see across customers that I talked to. You know, everyone has already Databricks and Snowflake and possibly some AWS or Microsoft services in their architecture and they’re wondering how do I stop copying data? How do I stop syncing policy between these systems? I know that we need to solve that problem today. But the higher level stuff, because usually, you know, like we work with a financial regulator that has their own method of tracking policy and translates that into the role-based access controls underneath.

You know, how you manage that policy may be organization specific, it might be something that that evolves over time. I think it’s you know, we’re we’re just at the start of this market where people are starting to think about data holistically across their entire enterprise, you know, including the transactional systems, how that data flows into the analytics systems, how we re secure it and have the same set of users and roles and potentially access controls that follow that data around.

This is a really big problem and I wish I had a crystal ball, but I just know that the next step is to to centralize and have fewer permission systems and, you know, just one that maybe covers 95% of your analytic data is going to be a major step forward.

[Listen and watch Ryan Blue discuss the future of data management and the unknowns on the horizon].

The Power of Inertia: How will Data Platforms Evolve Given Today’s Customer Preferences?

George:

- The world is moving to a data-centric world from a data platform-centric world.

I guess my follow up question for Ryan would be, now that we’re we’re prying open some of these existing data platform they had they had modularity, but generally they were working with their own modules. And you’re providing now open storage that can work across everyone so that we have a data-centric world instead of a data platform-centric world.

And my question would be where everyone’s now got to compete on workloads. What are the workloads that are first moving to a modular world where people are saying, let me choose at a more appropriate price or performance point for data that I can maintain in an open format.

Ryan:

I think right now companies have a different problem. It’s not like they’re they’re looking at this and saying, who? I want to move this workload. Or maybe they are, but it depends on where they’re coming from. If you already have Spark and you need a much better data warehouse option, then you might be adding snowflake. You might also be coming from Snowflake and going towards ML in Spark.

You know, those, those sorts of things. I can’t really summarize that. I would say that the biggest thing that we see in large organizations is that you have these pockets of people that, you know, this group really likes Spark. This group is perfectly happy running on Redshift. Someone else needed the performance of Snowflake and the CIO level is looking at this as what is our data story? How do we fix this problem of needing to sync data into five different places?

I was talking to someone at our company that used to work in ad tech just this morning and he said that they had, you know, five or six different copies of the exact same data set where different people would go to the same vendor, buy the dataset, massage it slightly differently to meet their own internal model and then use it.

And it’s it’s those sorts of problems that it’s like, let’s just store it once and like, let’s store all of this data once and make it universally accessible. We don’t have to worry about copies, we don’t have to worry about silos, we don’t have to worry about copying governance policy. And is it leaking? Because, you know, Spark has no access controls. While I’ve locked everything down in, say, Snowflake or Starburst.

It’s just a mess and so the first thing that people are doing is trying to get a handle on it and say, we know we need to consolidate this. We know we need to share data across all of these things. And thankfully, we can these days. Ten, ten years ago, the choice was we can share data, but we have to use Hadoop and it’s unsafe and unreliable and very hard to use.Or we can continue having both Redshift and Snowflake and Netezza in our our architecture,

So we’re we’re just now moving to where it’s possible and we’re we’re discovering a lot along the way here.

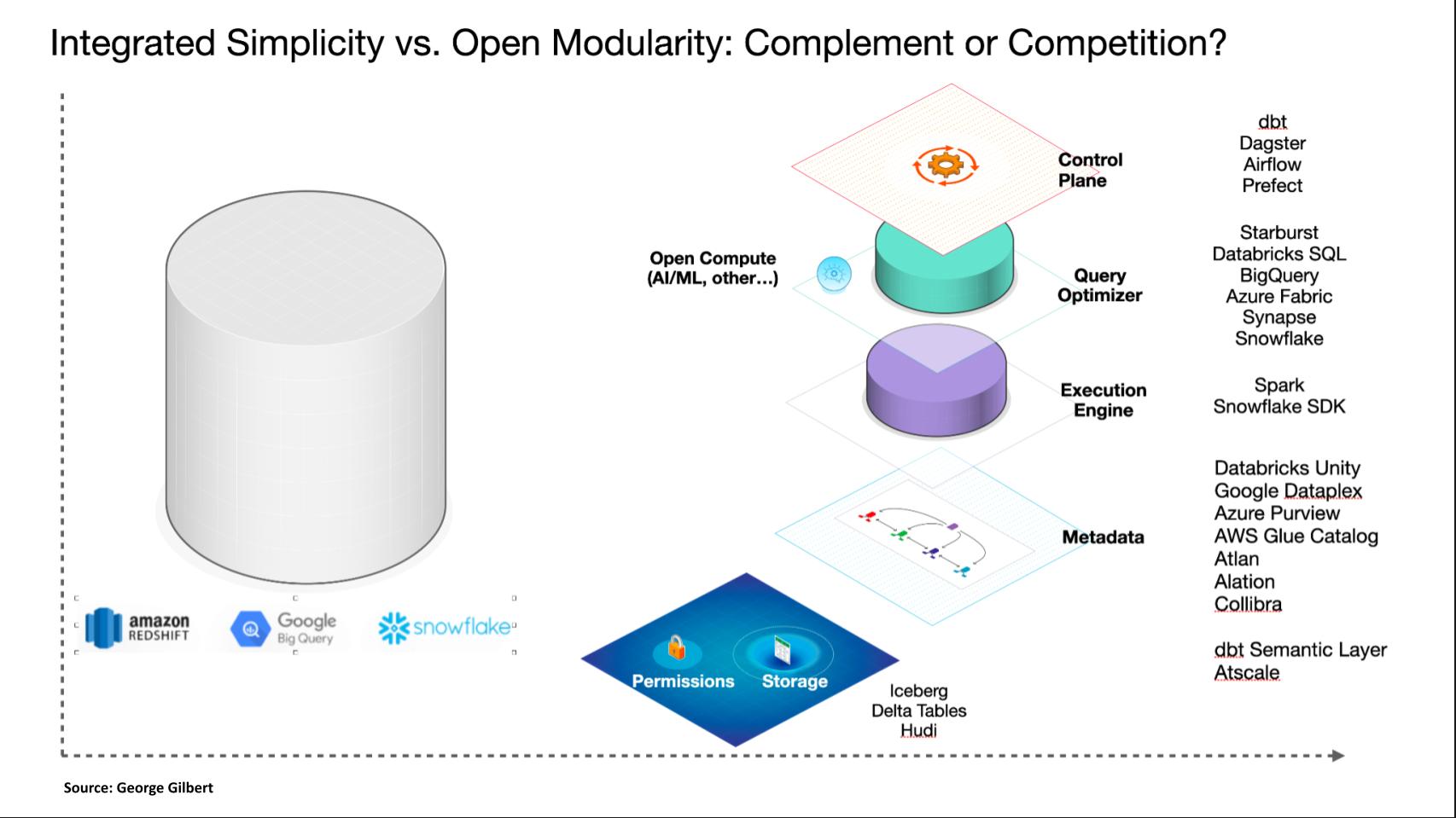

Integrated Simplicity Vs. Open Modularity: Complement of Competition

The above graphic is an attempt to illustrate what we see unfolding in the market that Ryan is helping us articulate. As we start on the left and we had a device or data platform-centric view of the world where it might be Redshift or Snowflake, where the state of the art of technology required us to integrate all the pieces, to provide the simplicity and performance the customers needed.

But as technology matures, we can start to modularized and the first thing we’re modularizing is storage. Now it means we can open up and offer a standardized interface to tables, whether it’s Iceberg or Delta tables or Hudi. And what Ryan is helping us articulate is that permissions have to go along with that. And there’s some amount of transaction support in there.

And then we’re taking apart the components that were in an integrated DBMS. Now, it doesn’t mean you’re going to necessarily get all the components from different vendors, but let’s just go through them. There’s a control plane that that orchestrates the work today. We know these as dbt or Dagster, Airflow or Prefect. There’s the query optimizer, which is the hardest thing to do where you can just say what you want and it figures out how to get it.

And that is also part of Snowflake and Azure synapse of Fabric or Databricks, which built their own Databricks SQL, separate from the Spark execution engine. The execution engine is an SDK sort of non SQL way of, of getting out the data. That was the original Spark engine. Snowflake has an API now, but we believe it goes through their query optimizer.

And there’s the metadata layer which goes beyond just the technical metadata. And this is what we were talking about with Ryan, which is how do you essentially describe your data estate and all the information you need to know about how it hangs together? And that’s like AtScale with its semantic layer, there’s Atlan, Alation, Collibra which are sort of user and administrator catalogs.

But the point of all this is to say that we’re beginning to unbundle what was once in the DBMS. That’s just the way Snowflake unbundled what was once Oracle, which had compute and storage together. They separated compute from storage and now we’re separating compute into multiple things to Ryan’s point. So that we can use potentially use different tools for different workloads and that they all work on one shared data estate that the data is not embedded in and trapped inside one platform or engine.

Final Thoughts by Ryan Blue

That’s the big question. How are we getting there? Do we have the components right? What is it all going to look like when we get there? It has big implications for for the products customers buy and for the business model of the vendor selling to them.

Ryan:

- We need both modularity and simplicity.

- Database services from the query layer are moving to the storage layer.

- Simplicity of access for OAuth is a key initiative.

- Lessons from Hadoop’s failings.

So just the high level modularity versus simplicity, I think we absolutely need both, right? The modular it is is clearly being demanded. The simplicity always follows afterwards. You know, databases, power applications. So there’s always been a gap in code and who controls what. And and these things, we’re just adding layers.

We pretty much know the boundaries between a database and an application on top of it and making that a smooth process. I think that we’re doing that again, separating that storage and compute layer. But we absolutely need both. And this is where some of the newer things that we’ve been doing in the Apache Iceberg community come into play. Standardizing how we talk with catalogs, making it possible to actually secure that layer and say, ‘hey, this is how you pass identity across that boundary.’

We’re also moving database services from the query layer for maintenance into the storage layer. That’s another thing that’s moving…that modularity needs to be followed by the simplicity, for instance things that use OAuth. We’re pioneering a way to use OAuth to connect the query engine to our storage layer so that you can just click through and have an administrator say, ‘Yes, I want to give access to this data warehouse, to Starburst’ or something like that.

That ease of use, I think is is really the only thing that is going to make modularity happen because, I mean, again, the big failure of the Hadoop ecosystem was that simplicity and that usability we have. We’ve only been able to see the benefits of that by layering on and maturing those products to add the simplicity. And so that’s absolutely a part of where we’re going.

[Listen to Ryan Blue summarize his final thoughts on the conversation].

Keep in Touch

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image: George Gilbert