In this Breaking Analysis we look at how AWS, Azure and GCP (Google Cloud Platform) are positioned to compete in the 2020’s. We’ll look deeper into the cloud market and specifically the business results and momentum of the big three US cloud players.

In this Breaking Analysis we look at how AWS, Azure and GCP (Google Cloud Platform) are positioned to compete in the 2020’s. We’ll look deeper into the cloud market and specifically the business results and momentum of the big three US cloud players.

Google last week opened up a bit and not only broke out Youtube revenues, but also its cloud business in a bit more detail. Like Microsoft, the numbers are still opaque relative to AWS disclosures which we feel are much cleaner. Nonetheless by squinting through the data we are able to better understand the momentum these three companies have in cloud and the ETR spending data gives us an added data-driven dimension.

Why the Big Three?

In this analysis we focus only on the Big Three in cloud – Amazon’s AWS, Microsoft Azure and the Google Cloud Platform. Our purpose is to analyze the U.S.-based hyperscalers who are leading the market and are bellwethers. Our current visibility on other global players like Alibaba is currently limited to only a handful of accounts globally.

We view the clouds of other U.S. players as an extension of their existing businesses and not as large scale cloud players. As an example, our estimates suggest that it would take IBM and Oracle 4-6 years to spend as much on CAPEX as Google spends in 4 months.

Coming back to AWS, Azure and GCP. Each is coming at the opportunity with a different perspective but Amazon and Microsoft have been on a collision course for a while now. Google aspires to get into that conversation. Amazon in our view has set the gold standard in cloud and specifically infrastructure-as-a-service. AWS created the market and, along with its customers, have earned the right to define the sector. Competitors like Microsoft are clever to differentiate and we explore that competitive aspect in this post.

How AWS Views the Cloud

But first let’s look at a clip of how AWS CEO Andy Jassy thinks about the goals of the AWS business. Jassy said on theCUBE:

At a high-level our top-down aggressive goals are that we want every single customer who uses our platform to have an outstanding customer experience. And we want that outstanding customer experience in part is that their operational performance and their security are outstanding. But also that it allows them to build projects and initiatives that change their customer experience and allow them to be a sustainable successful business over a long period of time and then, we also really want to be the technology infrastructure platform under all the applications of people build.

What’s interesting to us is how Jassy thinks about the AWS platform. It’s a platform to build applications. It’s not a SaaS…it’s not a platform which AWS can use to sell its software packages…it’s a place to build applications. Any application. All workloads. Globally. So when we say AWS has clean numbers it’s because AWS has a clean business– meaning, today at least, the numbers it shares are focused on infrastructure services. Infrastructure is what they do. Period. Thats what they report in their numbers and it’s much easier to understand than the other players.

Understanding Microsoft Azure and Google Cloud’s Reporting

Microsoft is doing incredibly well in cloud and we’ll come back to that. But Microsoft is taking a much different approach to the market relative to AWS. Microsoft reports cloud revenue but it comprises public, private and hybrid. It includes SQL Server, Windows Server, Visual Studio, System Center, GitHub and Azure. It also includes support services and consulting.

The key point here is Microsoft defines cloud to its advantage, which is smart, trying to differentiate with a multi-cloud, any cloud, any edge story. Think Microsoft AzureStack and Microsoft ARC, as well as other offerings that stress cross cloud, hybrid services.

Now Google as we know is a latecomer to cloud and it embraces the role of a challenger. Google’s starting point is G Suite. Google’s cloud strengths are infrastructure and analytics.

We’ll come back and explore how customers view AWS, Azure and GCP and why the buy from each later in this analysis.

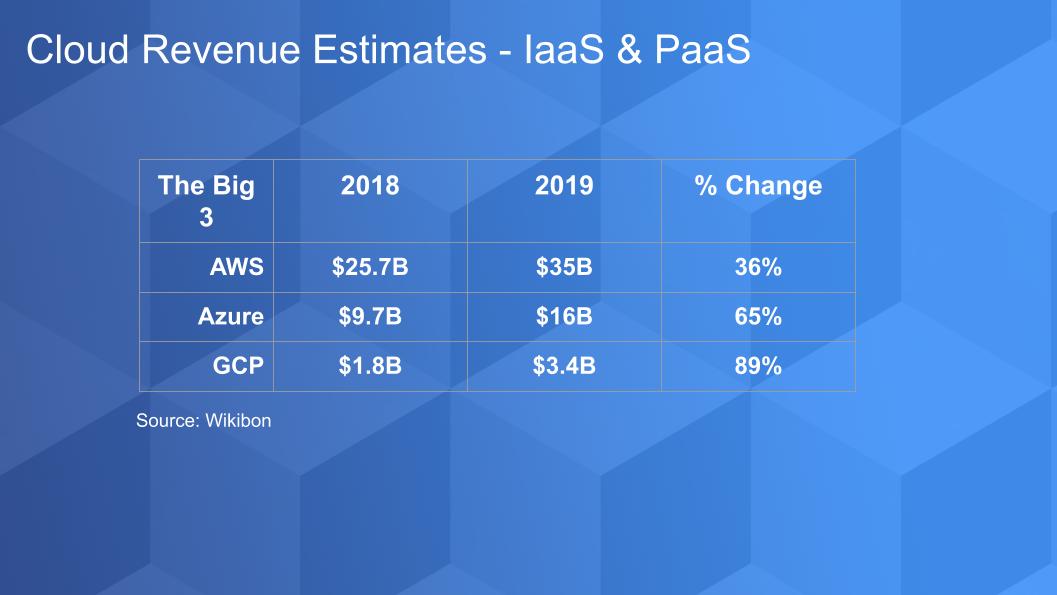

Market Share Estimates for Infrastructure-as-a-Service 2019

With that background let’s take a look at the current Wikibon estimates for IaaS revenue in 2019 for each of the Big 3 as compared to 2018.

What we show in the chart above is our estimates of AWS, Azure and GCP and their respective IaaS and PaaS revenue for 2018 and 2019. We’ve tried to strip everything else out so we can make an apples to apples comparison to the way in which AWS defines the market.

Let’s start with AWS. The street is concerned about the growth rate of AWS – it grew 35 percent last quarter – which admittedly is slowing down but did just under $10B in revenue in Q4. Consider that for a moment. AWS will probably hit a $50 billion dollar revenue run rate this year. Fifty billion! And it’s growing in the double digits. AWS will be larger than Oracle this year with Cisco in its sights.

Microsoft is very strong but remember these are estimates. They report Azure growth rates but they don’t give us a dollar figure – we have to infer that from other data. So the narrative on Microsoft is they’re catching up to AWS – and in one dimension that is true because Azure is growing faster than AWS. But AWS in 2019 grew by an amount almost equal to Azure’s entire business in 2018.

Now Google is hard to peg. The only thing we know is Google said its cloud business was $9 billion in 2019 up from $5.8 billion in 2018 up from $4 billion in 2017. So we’re seeing an accelerating growth rate that it said was largely attributable to GCP. And Google told us that GCP is growing significantly faster than its overall cloud business which remember includes G Suite.

So thats the picture we’ve created from a revenue and marketshare perspective for AWS, Azure and GCP; and we think it’s a reasonable reflection of the Big 3’s performance.

How Profitable is the Cloud?

Let’s take a moment to explore the profitability of the cloud.

On the Microsoft earnings call, top securities analyst Heather Bellini of Goldman Sachs was somewhat effusive – implying how impressed she was with with the fact that Microsoft has been consistently increasing its cloud gross margins each quarter – roughly it was up 5 points last quarter. On the Google call, Heather was pressing Google CEO Sundar Pichai on gross margin guidance for GCP – which Sundar wouldn’t answer. As well, Andy Jassy said on theCUBE last re:Invent that the cloud was higher margin than retail but at scale its a relatively low margin business as compared to software.

First – Jassy is correct – cloud is lower margin than software but he’s sandbagging a bit in our view. AWS is a great margin business in our opinion. AWS has operating margins consistently in the mid twenties – around 26 percent last quarter. While lower than Oracle’s , AWS’ are comparable to (albeit somewhat below) Cisco’s and Microsoft’s operating profit margins. And AWS touts operating margins higher than IBM. These are comps that are very profitable companies. And AWS has operating margins higher than a number of software companies including Salesforce.com, Workday, Splunk and Tableau (when it was a public company).

Now Bellini on the earnings calls was pressing about gross margin guidance which in our view are as impressive. Heres why:

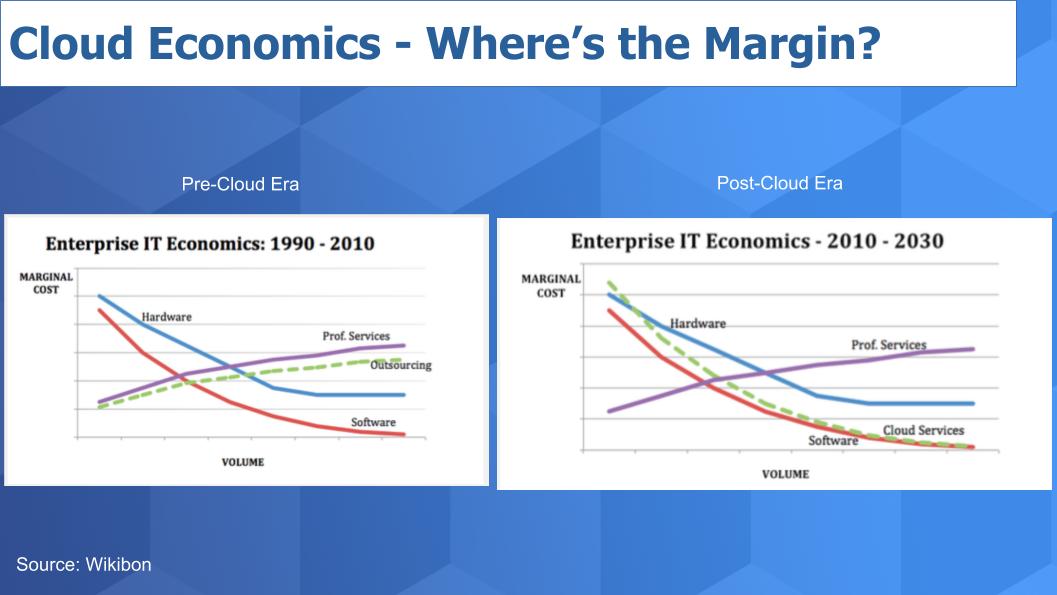

Cloud Economics 101

This is a chart we created about ten years ago but it’s worth revisiting in the context of margins for AWS, Azure and GCP.

The chart above shows a very basic view of the economics of the different sectors of the technology business – namely hardware, software and services. They each have a different margin profile as shown. On the vertical axis is marginal cost – that is the incremental cost of producing one additional unit of a product or service. On the horizontal axis is volume or scale and we’re showing the Pre0-cloud era on the left and the cloud or Post-cloud timeframe on the right hand chart.

As you can see, each segment has a different cost and hence margin profile. In hardware – you have economies at volume but you have to purchase and assemble components so at some point your marginal costs hit a floor. Professional services have diseconomies of scale meaning at higher volume things get more complex with more overhead. The red line is software…everyone loves software because the marginal costs go to zero and your gross margin approaches the cost of distributing the software – in the old days that was the cost of a diskette or a CD – so software gross margins are huge.

Now look at the green line we’ve labeled outsourcing. In the Pre-cloud era, outsourcing companies could get some economies but it really wasn’t game changing. But in the Post-cloud world the hyperscalers are driving automation and “outsourcing” IT infrastructure deployment to a cloud vendor is much more efficient.

Admittedly, we’re exaggerating the margin impact for effect because the cloud players still have to buy hardware and they have other costs but the point is gross margin on outsourcing IT to a cloud player is far more attractive to the vendor at scale than we say for professional services companies, because they automate away much of the labor costs.

Heather Bellini was essentially asking Satya Nadella “how is it you can keep expanding gross margins each quarter” and she was trying to understand if GCP gross margins were tracking similar to AWS and Azures back when they were smaller.

We think these curves give some guidance. AWS is further down the curve and more mature than other players– by perhaps as much as 2-5 years. As the other cloud players scale to catch AWS, their margins will consistently improve.

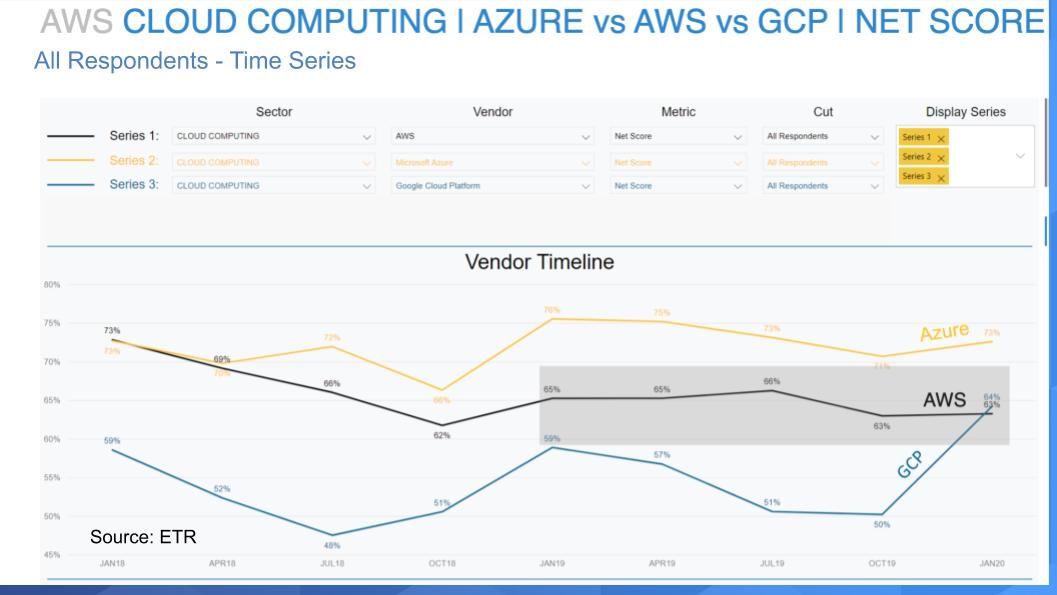

Spending Data: AWS Consistency, Azure Momentum & a Noticeable Bump for Google

The chart below shows Net Score or spending velocity for each of the Big 3 cloud players over the past nine surveys for the Cloud Computing sector. Three things stand out: 1) AWS remains very strong with Net scores solidly in the 60 percent plus range; 2) Azure has sustained a clear momentum lead over AWS since the July ’18 survey; and 3) GCP’s uptick – it’s notable and encouraging for Google.

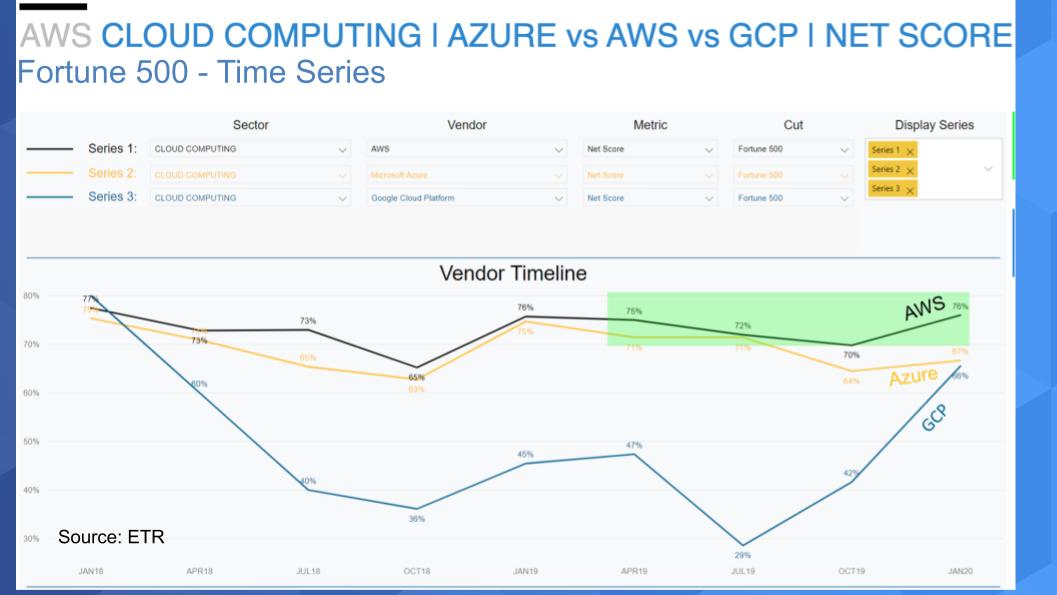

The Spending Picture in F500 Shows AWS Back on Top

Now let’s take another cut on this data and drill into the larger companies in the ETR data set.

The chart below shows what happens when you isolate on Fortune 500 respondents. Two points here: 1) AWS actually retakes the lead in Net Score or spending velocity. Even though Azure remains strong – Amazons’ showing in large accounts is very impressive – nearly back to early 2018 peak levels at 76 percent – a very strong Net Score; 2) The second point is GCP’s uptrend holds firm and actually increases slightly in these larger accounts.

So it appears that the big brands which perhaps used to shy away from cloud are increasingly adopting.

Why do they Buy AWS, Azure and GCP?

One of the impressive aspects of the ETR platform is the ability to assess drill downs, where they’ll ask specific questions that are timely and relevant. So we want to know…what every sales person wants to know – WHY DO THEY BUY each cloud?

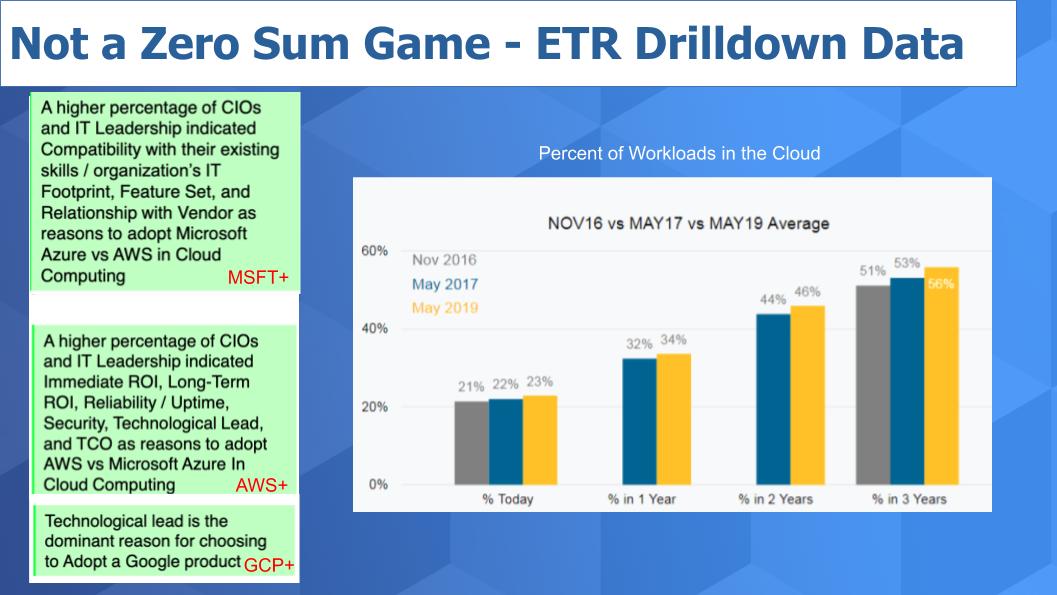

The chart below shows data from ETR drill downs. On the left side in the green are the “why they buys” for Microsoft, AWS and Google Cloud. For Microsoft, CIOs say compatibility with existing skills and the organizations IT footprint. Then feature set, etc. We believe this is Microsoft’s huge advantage. It’s just simpler to migrate work to Azure if you’re already running Microsoft apps. If Microsoft continues to deliver adequate features Azure is a no-brainer for many workloads.

For AWS the plusses are ROI and – as we’ve said many times on theCUBE, best cloud in terms of reliability, uptime, security, etc. AWS has the best cloud for infrastructure and if you’re not incurring huge migration costs or you’re not Walmart – why wouldn’t you go with the best cloud?

GCP comes down to the tech – Google has good tech and IT guys love good tech. And when it comes to analytics – Google is strong so GCP is becoming a good analytics alternative to AWS.

Cloud Adoption Levels

The right hand side of this chart shows why this is not in our view, a winner take all game. The chart shows the percent of workloads in the cloud today, in 2 years and 3 years across different survey dates. Today, extrapolating for the survey dates, the figure is between 25-35 percent of workloads have moved to the cloud. But the figure is headed to upwards of fifty percent.

This is a huge growth opportunity for AWS, Azure and GCP; as well as other global hyperscalers. Sometimes people say to us that Google doesn’t care about the cloud because it’s such a small piece of their business; or they can’t achieve number one or number two so they’ll exit the business. We don’t buy these scenarios. Cloud is a trillion dollar market and Google is in it for the long game in our view.

Things to Watch in 2020 and Beyond

Let’s wrap by looking forward to 2020 and beyond.

The first thing we want to is we’re happy Google is finally reporting its cloud revenue. But we think Google has to show more detail in its cloud business. We understand this a good first step but IT buyers we believe will want to see more data as we go forward. We will continue to push AWS, Azure and GCP for more transparency.

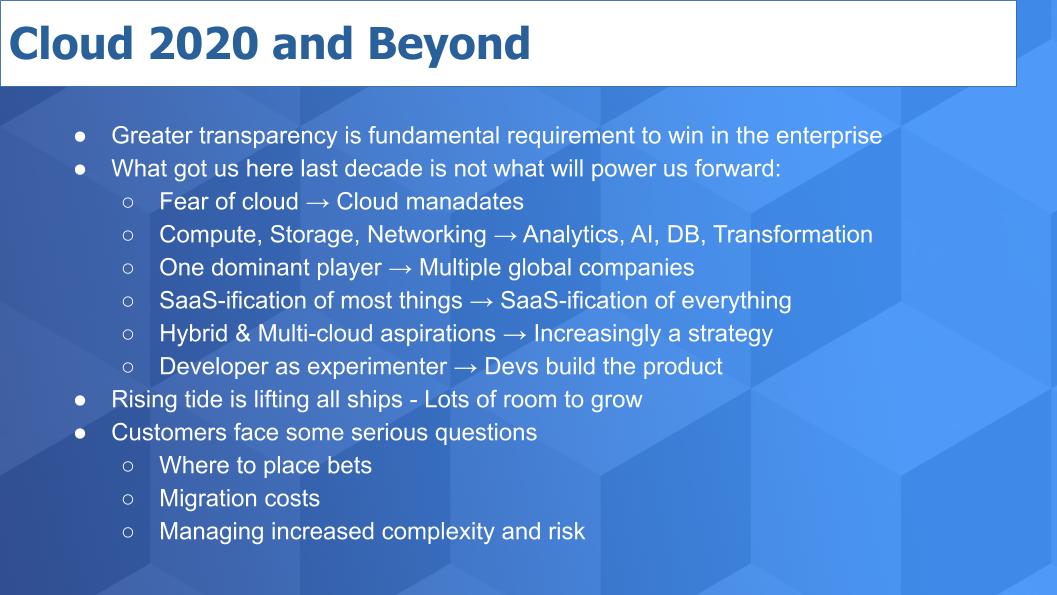

The other point we want to make is we believe we are entering a new era. The story of the past isn’t going to be the same this decade. Buyers aren’t afraid of cloud anymore…it has become a mandate. The dominant services of the past in compute, storage and networking are evolving into analytics with AI and new types of database services, which are becoming platforms for business transformation.

Competition is – as we now see – much more real today especially between AWS, Azure and GCP. Buyers have options and that is going to create more innovation. SaaS continues to be a huge factor but more so than ever. Hybrid is real and multi-cloud will increasingly become a challenge. We expect AWS will enter the multi-cloud market in a bigger way as a means of expanding its TAM and addressing customer requirements. And finally, developers are no longer tinkerers – they are the product creators.

As we’ve stated, this is a huge market and AWS, Azure and GCP can all participate as well as overseas players like Alibaba.

As a customer it’s becoming a more complicated situation. Cloud is not just about experimentation or startups – it’s increasingly becoming something that you really need to get right. Where to bet, migration, managing risk all become much more critical. On the one hand optionality is a good thing but if you make the wrong bet it could be costly if you don’t have a good exit strategy.

As always we appreciate the comments LinkedIn and on Twitter @dvellante – thanks for that. And thanks for being a member of theCUBE community.

Here’s the full video analysis: