Contributing Author: David Floyer

Intel’s big announcement this week underscores the threat that the United States faces from China. The U.S. needs to lead in semiconductor design and manufacturing; and that lead is slipping because Intel has been fumbling the ball over the past several years. A mere two months into the job, new CEO Pat Gelsinger wasted no time in setting a new course for perhaps the most strategically important American technology company. We believe that Gelsinger has only shown us part of his plan. This is the beginning of a long and complex journey. Despite Gelsinger’s clear vision, deep understanding of technology and execution ethos, in order to regain its number one position, Intel will need help from partners, competitors and very importantly, the U.S. government.

In this Breaking Analysis we’ll peel the onion of Intel’s announcement, explain why we’re not as sanguine as was Wall Street on Intel’s prospects and lay out what we think needs to take place for Intel to once again become top gun; and for us to gain more confidence.

The Urgent Need for Change

You may recall that in January we dismissed analysis that suggested Intel didn’t have to make any major strategic changes to its business. Rather we said the exact opposite.

Our view at the time was that the root of Intel’s problems could be traced to the fact that it was no longer the volume leader, because mobile volumes dwarf those of x86. As such we said that Intel couldn’t go up the learning curve for next gen technologies as fast as its competitors and it needed to shed its dogma of being highly vertically integrated. We said Intel needed to more heavily leverage outsourced foundries. But more specifically, we suggested that in order for Intel to regain its volume lead it needed to spin out its manufacturing and create a joint venture with a volume leader, leveraging its U.S. manufacturing presence.

More specifically, we suggested that in order for Intel to regain its volume lead it needed to spin out its manufacturing and create a joint venture with a volume leader, leveraging its U.S. manufacturing presence.

This, we still believe with some slight refreshes to our thinking based on what Gelsinger has announced.

Three Pillars of Intel’s Announcement

There were three main parts supported by many details within Intel’s announcement, which was a first rate production for what it’s worth.

Gelsinger made it clear that Intel is not giving up its IDM or integrated device manufacturing model. He called this IDM 2.0 which comprises Intel’s internal manufacturing, leveraging external foundries and creating a new business unit called Intel Foundry Services.

So ok, Gelsinger said we’re not giving up on integrated manufacturing…however we think this is nuanced. Clearly Intel can’t, won’t and shouldn’t give up on IDM. However we believe Intel is entering a new era where it is giving its designers more choice. This was not explicitly stated per se, however we believe Intel’s internal manufacturing arm will have increasing incentives and pressure to serve its designers in a more competitive manner. We’ve already seen this with Intel finally embracing EUV, extreme ultraviolet lithography.

Gelsinger basically said that Intel didn’t lean into EUV early on and that created more complexity in its 10 nm process, which rippled into its 7nm production and …well, you know the rest of the story. But since mid last year Intel has embraced the technology. However, as a point of reference, Samsung started applying EUV for its 7 nm technology in 2018 and began shipping in early 2020. So as you can see it takes years to get this technology into volume production.

The point is that Intel realizes it needs to be more competitive and we suspect it will give more freedom to its designers to leverage outsource manufacturing. But Gelsinger clearly signaled that IDM is not going away.

Intel as External Foundry

The really big news, however is that Intel is setting up a new division with a separate P&L that will report directly to Pat. Essentially it’s hanging out a shingle and saying we’re open for business to make your chips. Intel is building two new fabs in Arizona and investing $20B as part of this initiative. While Intel tried this early last decade, Gelsinger says this time we’re serious and will do it right. We’ll come back to that later in this post.

This organizational move, while not a spin out or JV as we recommended, is a core part of the recipe we saw as necessary for Intel to compete. It must have a structure with leadership, measurements and incentives that allows it to benchmark against the leading foundries. And it must have a line of demarcation to0 satisfy its prospective customers, many of whom are competitors.

Why is Intel Making These Changes?

Lots has changed in the world of semiconductors since Pat left Intel in 2009.

Some key changes in the market are notable:

x86 Dominance. Back when Pat was at Intel in the 90’s, Intel was the volume leader and crushed the competition from RISC chips.

Mobile Tsunami. When Apple changed the world with iPod, iPhone & iPad, it changed the game in semis and the volume equation flipped to mobile.

Outsourced Foundries. That led to big alterations in the way chips were manufactured. Specifically, most of the world has separated design from manufacturing. We now see firms going from design to tape out in 12 months versus 3 years. A good example is Tesla and its deal with Arm and Samsung.

Intel’s Dominance is Challenged. As a result, Intel has gone from #1 in foundry in terms of clock speed, wafer density, volume, lowest cost, highest margin…to falling behind TSMC, Samsung and alternative processor competitors like Nvidia and Arm.

Volume Shifts to Arm. Volume is still the maker of kings – that hasn’t changed – and it confers advantages in terms of cost, speed and efficiency. But Arm wafer volumes we estimate are 10X those of x86 that’s a big change since Pat left Intel more than a decade ago.

Digital Pivot Creates a Long-Term Supply Squeeze. There’s also a major chip shortage today but we think it’s somewhat different than the typical semiconductor boom and bust cycles. Semiconductor consumption is entering a new era of use cases from automobiles to factories to every imaginable device, piece of equipment and infrastructure. Silicon is everywhere.

America’s Dominant Position is Precarious. But the biggest threat of all is China. It wants to be self-sufficient by 2025. It’s putting $60B into chip fabs and there’s more to come. China wants to be the new economic leader and semiconductors are critical to that goal.

How Real is the Threat From China?

Now there are those that deny the China threat.

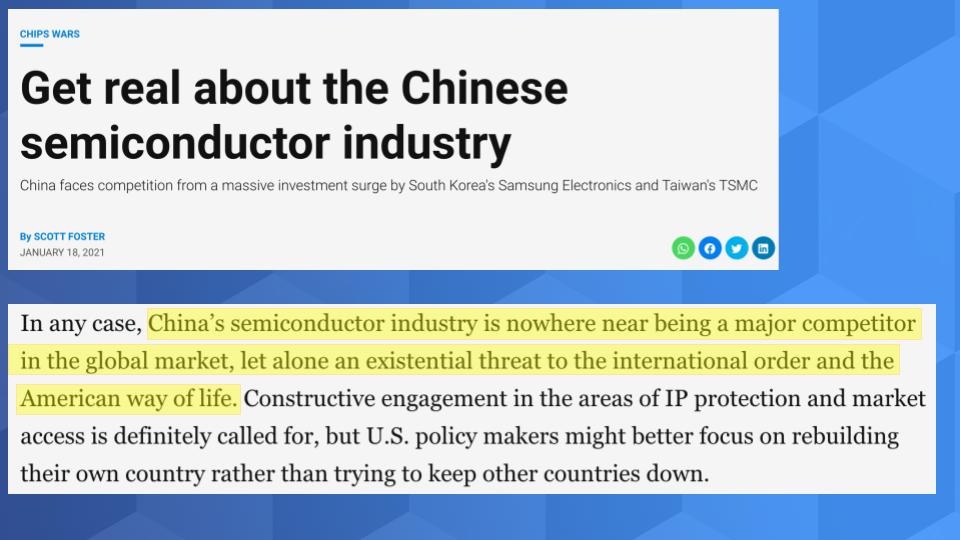

This recent article from Scott Foster lays out some great information but one thing that caught our attention is his statement that China’s semiconductor industry is nowhere near being a major competitor in the global market, let alone an existential threat to the international order and the American way of life. We really think Scottie is stuck in the engine room and can’t see the forest through the trees.

Sure you can say China is way behind. Take NAND for example. Today China is at 64 3D layers whereas Micron is at 176. By 2022 China will be at 128 and Micron well over 200. But talk to us in 2025 – we think China will be at parity.

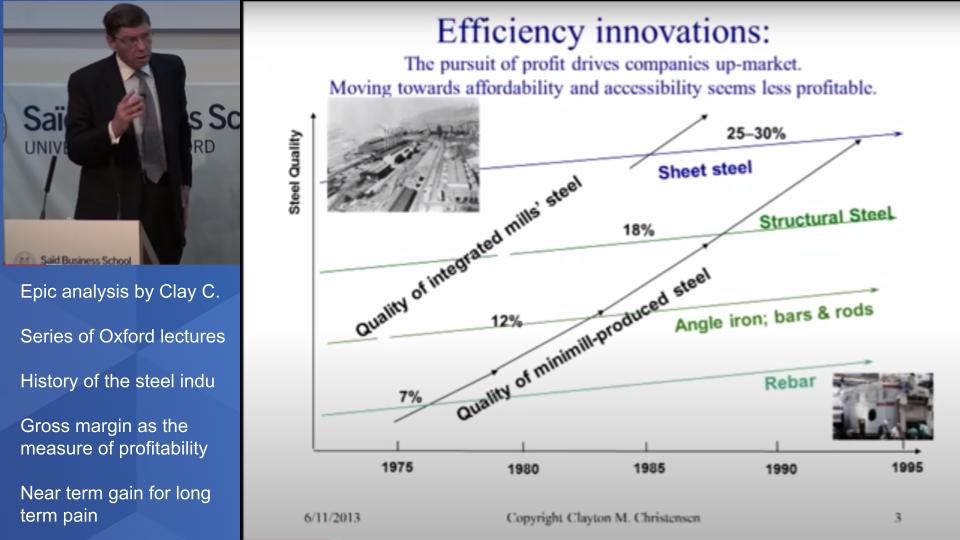

What Would Clayton Christiansen Think?

The type of thinking that says don’t worry about China in semis reminds us of the epic lecture series that Clay Christensen gave as a visiting professor at Oxford university on the history of and the economics of the steel industry; among other topics.

If you haven’t watched this series it’s highly recommended. It’s one of his many lasting gifts to the business world. Basically Christensen took the audience through the dynamics of steel production and he asked the question. Who told the steel manufacturers that gross margin was the #1 measure of profitability? Was it god he joked? His point was when new entrants came into the market in the 70’s they were bottom feeders, going after the low margin, low quality, easiest to make rebar sector. And the incumbents pulled back and their mix shifted to higher margin products and their gross margins went up. And life was good.

Who told the steel manufacturers that gross margin was the #1 measure of profitability?

Until they lost the next layer up the stack…then the next….then the next until it was game over.

Intel Revises Financial Forecasts Citing Supply Chain Issues

One of the things that was lost in Pat’s big announcement on the 23rd of March was that Intel revised its financial guidance, painting a rosier picture relative to its previous forecasts, but the guide was below consensus on revenue and earnings. The company cited strong demand for PCs but a revenue squeeze to to the industry-wide supply chain issues. The stock went up the next day on the momentum of the big announcement.

When asked about gross margin in the Q&A – yes gross margin is a, if not the key metric in semis – Intel’s CFO, George Davis explained that with the uptick in PC demand there is a product shift to the lower margin PC sector and that puts pressure on gross margins. And revenue because PC chips are less expensive than server chips and the industry-wide shortage of components is problematic for Intel.

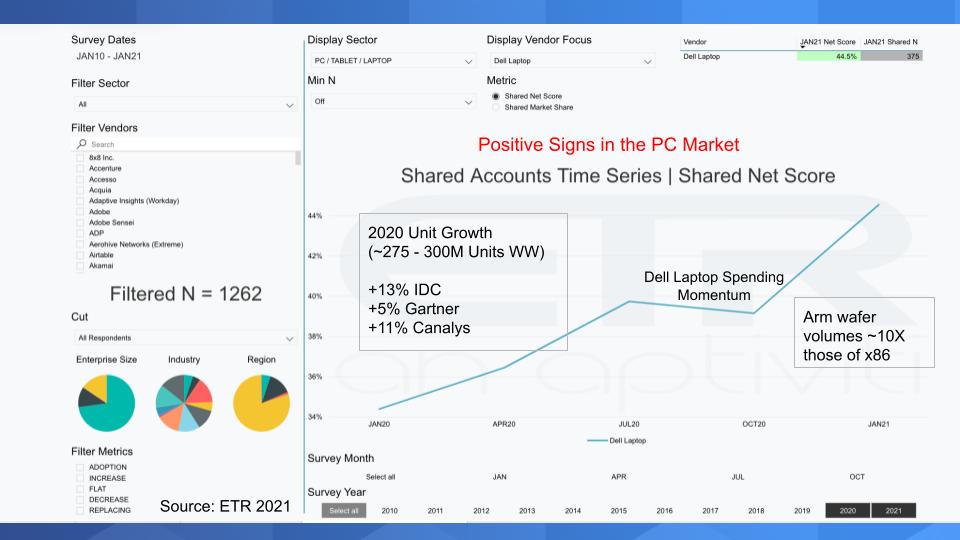

PC demand is indeed strong as shown in the chart below from ETR, showing spending momentum over time for Dell’s laptop business with selected market data inserted.

Note the data in the inset showing the unit growth and the market data from IDC, Gartner and others. As we pointed out on our last Intel note, PC volumes peaked in 2011 and that’s when the “long Arm of Wright’s Law” began to eat into Intel’s dominance. Today Arm wafer production is far greater than Intel’s and…well you know the story.

The irony here is the very market that conferred volume advantage to Intel (PCs), had a slight uptick last year, which was great news for Dell…but according to Intel it pulled down margins. The point is Intel is loving the high end of the market because it’s higher margin and more “profitable.”

We wonder what Clay Christensen would say to that?

There’s more to this story. Intel’s CFO blamed supply constraints on Intel’s revenue and profit pressure. Yet AMD’s revenue and profits are booming. So are TSMC’s. Only Intel can’t seem to thrive when there’s a massive chip shortage.

Analyzing Intel’s Big Moves

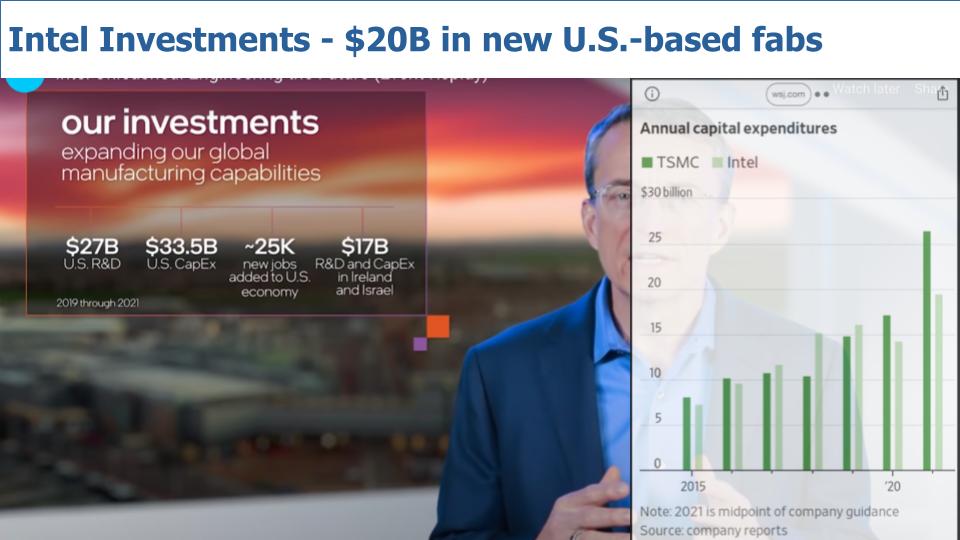

Intel is for sure going for it, investing $20B in two new U.S.-based fabrication facilities.

The chart above shows Intel’s investments since 2019 in U.S. R&D, U.S. CAPEX, the job growth created, as well as R&D and CAPEX investments in Ireland and Israel. We added the bar chart on the right from a WSJ article that compares TSMC CAPEX in the dark green to that of Intel in the light green. TSMC surpassed the CAPEX investment of Intel in 2015 and then Intel took the lead again in 2017 and was hanging on through 2019 but last year TSMC took the lead and it appears to be widening quite substantially. Leading us to our conclusion that these moves by Intel will not be enough. We believe Intel needs to do much more, which we’ll address later.

Partnerships & Packaging

Where this announcement gets quite interesting is how Intel is trying to leapfrog its competitors with packaging, and the friends it’s making to do so.

Intel was late to the party with SoC, system on a chip. And it’s going to use its packaging prowess to try and leapfrog its competition. SoC bundles GPU, NPU, DSUs, accelerators, caches and other components on a chip. So it gives much better use of real estate. Intel wants to build system on package, which will disaggregate memory from compute in an innovative way.

Remember today, memory is very poorly utilized. Intel is going to create a package with thousands of nodes comprising small processors, big processors, alternative processors (Arm processors), custom silicon…all sharing a pool of memory. This is a huge innovation. It’s important because it will give Intel’s prospective foundry customers more flexibility and optionality. We’ll come back to this concept and provide more detail below.

Partnerships – Some Old Some New

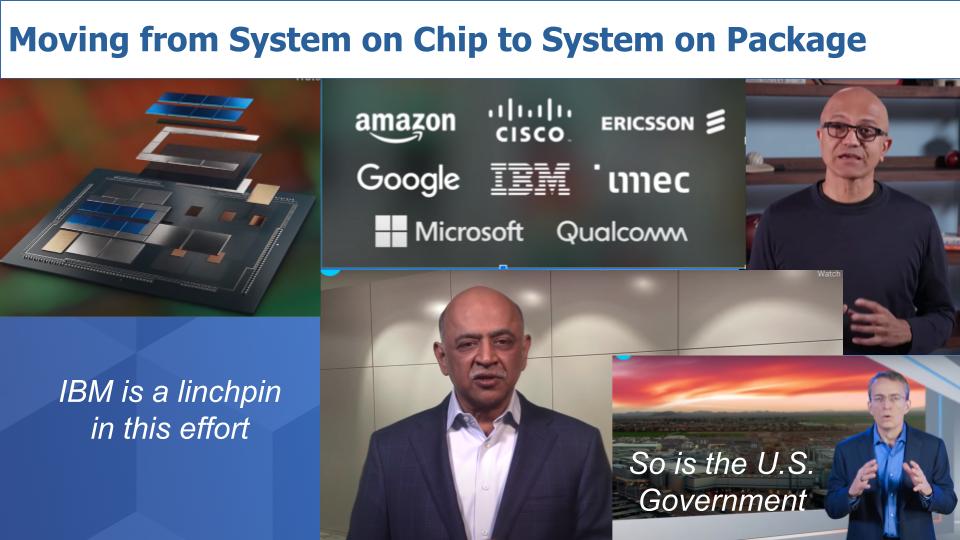

As part of the announcement, Intel trotted out some big name customers, prospects and even competitors that it wants to turn into prospects. Amazon, Google, Microsoft and Cisco – who are designing their own chips…as does Ericsson and look – even Qualcomm on the list in the graphic below. Intel wants to earn the right to make chips for these firms. Many, like Microsoft and Google would be happy to do so because they want more competition, better sourcing and lower prices. And then there’s Qualcomm. Well if Intel can do a good job and be a strong second source…why not? One reason is they compete aggressively with Intel but it’s possible. And with a severe capacity shortage even probable if Intel can execute.

But the two most important partners on the slide above are IBM and the U.S. government.

IBM is a Major Piece of the Puzzle

Many people will gloss over IBM in this announcement and think it’s only about quantum computing. They’ll write that off as a distant future innovation. This is understandable but we think this announcement goes beyond a futuristic (albeit strategically important) technology. We believe IBM is one of the most important pieces of Intel’s reinvention puzzle. Yes IBM. IBM actually has some of the best semiconductor technology in the world.

Specifically, IBM has a superb architecture with Power 10 and is 2-3 years ahead of Intel. Yes Power. IBM is the world’s leader in terms of its ability to disaggregate compute from memory and scale to 000’s of nodes and pool memory across resources in the package. IBM leads in power density and efficiency, and is looking at a 20X increase in AI inference relative to its previous generations.

We believe Pat has been thinking about this and said “how can I leapfrog SoC…Well, I’ll use our outstanding process manufacturing and tap IBM as a partner for R&D and architecture to build the next generation of systems on a package that are more flexible and performant than anything out there.”

The U.S. Military Needs Top Gun Capabilities

What IBM is developing and Intel contemplating is super high end stuff. And guess who needs really high end, massive supercomputing and AI inferencing capabilities? The U.S. Military. Pat said straight up…we’ve talked to the government and we’re honored to be competing for the government / military chip foundry.

We think Intel will have to fall down to lose the government foundry business.

And by making the commitment to foundry services we think Intel will get a huge contract from the government – as large as $10Billion dollars or more – to build a secure government foundry and serve the military for decades to come.

Pat was asked at the announcement: “is this foundry strategy viable without the help of the U.S. government?” And Pat – of course – said that this is the right thing for Intel, independent of the government opportunity. We haven’t received any commitment or subsidies, etc. Ok…fine.

But we all know what’s happening here. The U.S. government wants Intel to win. It needs Intel to win and its participation greatly increases the probability of success for Intel.

Unfortunately It’s Still Not Enough for Intel

Let’s look in more detail and some of the challenges and positive trends for Intel.

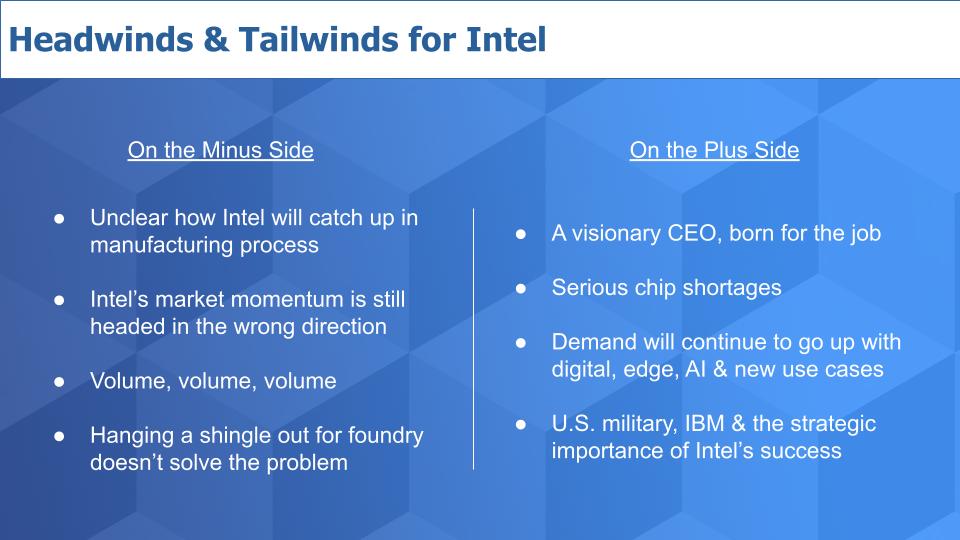

Challenges

The headwinds for Intel are many. It can’t just flick a switch and catch up on manufacturing leadership. It will take four years and lots can change in that time. Intel’s market momentum, as seen by its financials, is headed in the wrong direction. Moreover, where will the volume come from? It will take years for Intel to catch up to Arm volumes and it is going to have to fight to win that business. It will fight gallantly, we have no doubt under Pat’s excellent leadership – but the foundry business is a different animal.

Consider that Intel’s annual CAPEX expenditure is roughly 20% of its revenue. TSMC spends 50% of its revenue each year on CAPEX. It’s a fundamentally different business. It’s good that Pat is creating a separate business, he has to do so. But we’re not pounding the table saying Intel’s worst days are over. We don’t think they are.

In Fairness…

Now there are some real positives. Pat Gelsinger was born for this job. He proved that the other day even though we already knew it. We’ve never seen him more excited and clear headed. We agree that the chip demand dynamic is going to have legs this decade and digital, edge, AI and new use cases will power that demand.

Intel is too strategic to fail and the U.S. government has huge incentives to make sure Intel succeeds.

But it’s still not enough in our opinion because, like the steel manufacturers, Intel’s real advantage is in the high margin business. And without volume, China will win this battle.

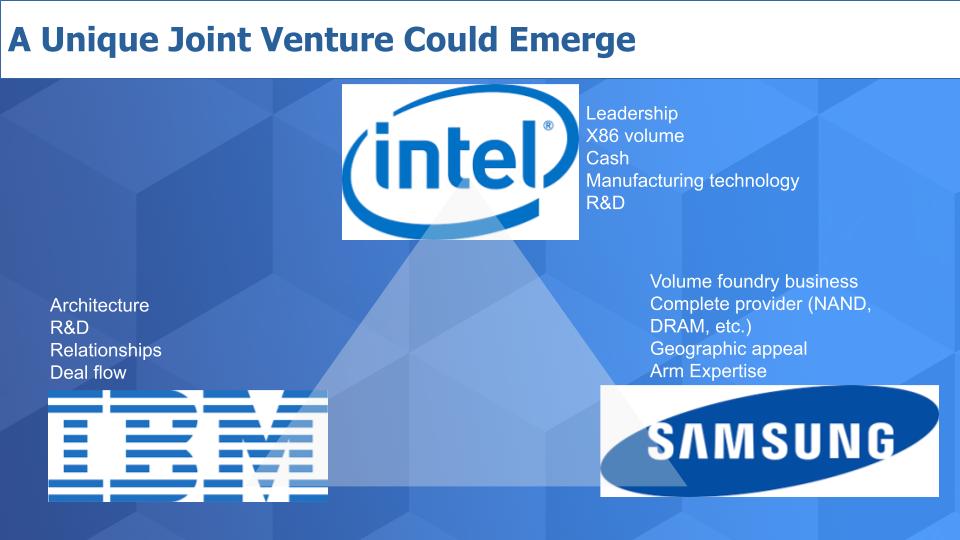

Is Pat Gelsinger Delusional?

No, we don’t think so. We believe Pat has not shown his entire hand and is has more dry powder. We continue to believe a new joint venture structure will emerge.

We see a triumvirate emerging in a new joint venture that is led by Intel. It brings x86 volume, cash, manufacturing prowess, R&D, global resources and so much more than we show above. I

BM as we laid out brings architecture, its R&D, long standing relationships and deal flow – it can funnel its business to the JV as can parts of Intel. We see IBM getting a nice license deal from Intel and/or the JV – it has to get paid for its contribution. And it will get a sweet deal on the manufacturing fees.

But it’s still not enough to beat China. Intel needs volume and that’s where Samsung comes in. We think Samsung makes more sense than TSMC as the JV partner. It has the volume with Arm, the experience a complete offering and it is IBM’s strategic manufacturing partner and we think IBM is key to this deal.

We also think South Korea is more geographically appealing than Taiwan. Not to mention that TSMC doesn’t need Intel. Intel can get a better deal from #2 Samsung and together these three – in this unique structure – could give it a chance to become #1 by the end of the decade or early in the 2030’s.

We believe Pat is laying the groundwork and will construct some type of unique partnership or collaboration with deep engineering ties. Without such help we believe Intel will fail.

Thoughts From the Community

Finally we want to leave you with some comments and thoughts from two individuals who provided input that we felt was worth sharing.

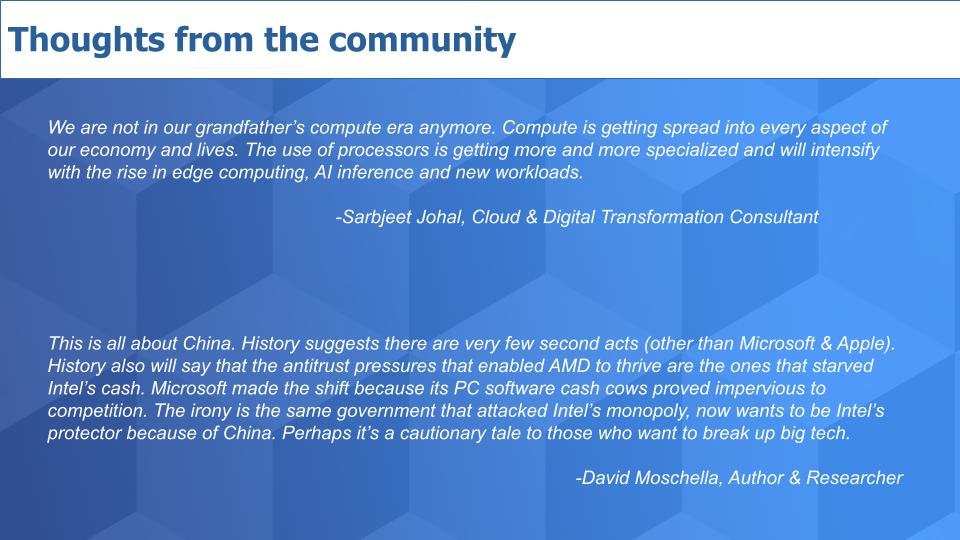

First Sarbjeet Johal sent this to us last week.

We are not in our grandfather’s compute era anymore. Compute is getting spread into every aspect of our economy and lives. The use of processors is getting more and more specialized and will intensify with the rise in edge computing, AI inference and new workloads.

We agree with Sarbjeet and that’s the dynamic on which Pat is betting big.

But the bottom line is summed up by friend and mentor David Moschella.

This is all about China. History suggests there are very few second acts (other than Microsoft & Apple). History also will say that the antitrust pressures that enabled AMD to thrive are the ones that starved Intel’s cash. Microsoft made the shift because its PC software cash cows proved impervious to competition. The irony is the same government that attacked Intel’s monopoly, now wants to be Intel’s protector because of China. Perhaps it’s a cautionary tale to those who want to break up big tech.

Wow – What more can we add to that?

Keep in Touch

Remember these episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image credit: ink drop

Note: ETR is a separate company from Wikibon/SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.