Is multicloud a symptom or a cure? Welcome to this week’s Wikibon CUBE Insights, Powered by ETR. In this Breaking Analysis, we want to dig into the so-called multicloud arena. Some of the questions we get from our community include:

- What is multicloud?

- Do we really need it?

- What problems does it solve?

- What problems does it create?

- Is there a financial advantage to multicloud or is it just about avoiding lock-in?

- How will multicloud evolve?

- Who are some of the key players to watch and how do they stack up?

In this analysis we’ll take a stab at addressing these questions.

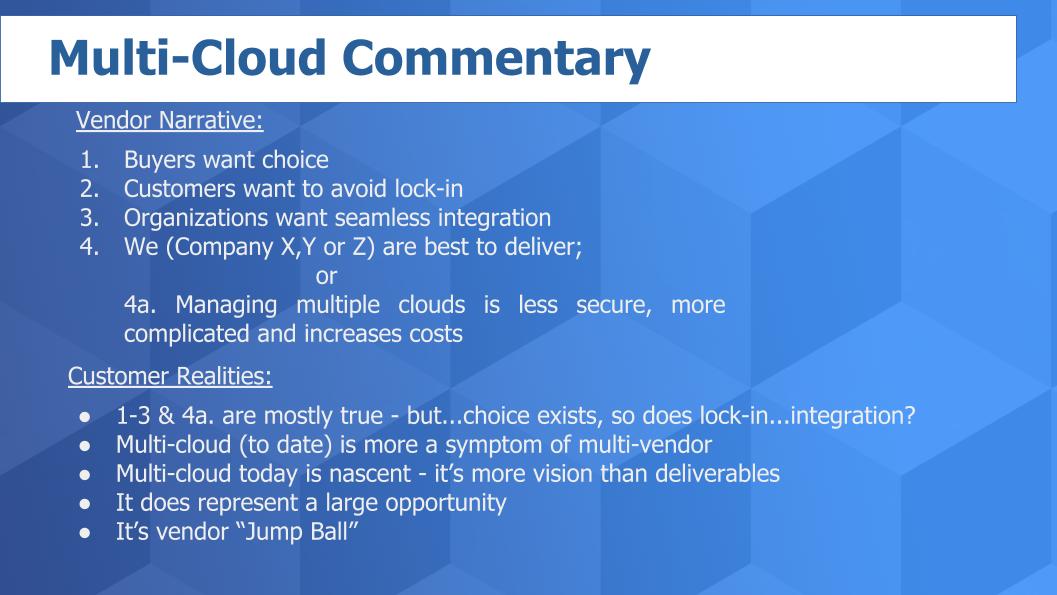

Vendor Messaging Makes a Logical Case…But

Let’s look at some of the noise in the market and try to extract the signal. What suppliers tell us is shown in the top of the chart below.

Most vendors, especially the ones trying to “cloud-proof” their on-prem business, are touting multicloud. And they tell us: 1) Customers want to avoid vendor lock-in; 2) Organizations want seamless integration across clouds; 3) They are uniquely qualified to deliver that capability.

Although as you can see in 4a. above, not everyone agrees…because some feel that multicloud is less secure, more complicated and increases costs.

Reality Check: Customers Struggle with Siloed Clouds

Recently we received a comment from an analytics pro in the financial services sector that underscores the reality of multicloud…this person said:

I have a number of AI and analytics initiatives and pretty sophisticated modeling projects going on. The data lives in multiple clouds and we use a variety of tools to extract insights and act on them. I’d like to cross-connect all these capabilities, the data and workloads running on these clouds with a consistent experience. How am I supposed to do that?

The reality is that buyers do want choice and would like to avoid lock-in – although the risk of lock-in in our experience is subservient to business outcomes. And it’s definitely true that customers want seamless integration.

Who is best positioned to deliver all these capabilities is something we’ll explore in this analysis. But generally we would say multicloud to date is more a symptom of multivendor than a clear strategy for buyers. However, that is changing and there’s a substantial opportunity in our view for providers to deliver clear value.

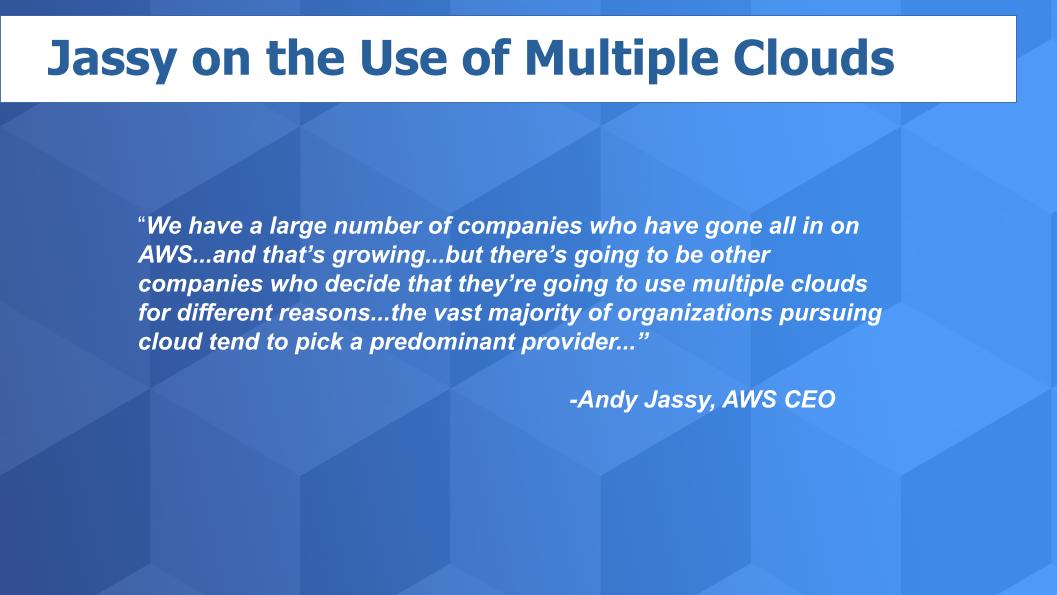

How AWS Currently Views the ‘M Word’

In an exclusive sit down with Andy Jassy prior to reInvent 2019, John Furrier asked AWS CEO Andy Jassy to talk about the use of multiple clouds. We summarize his comments below.

Jassy went on to say that the vast majority of organizations pursuing cloud tend to pick a predominant provider…that its not a 50/50 scenario. Rather its more like 70% primary 30% secondary; or 80/20 or even 90/10.

Furrier went on to paraphrase Jassy saying:

It’s not hard to find the reasons for using multiple clouds…M&A, shadow IT, developer preference…But it’s not multi-cloud by design…it’s just more of the same enterprise IT mishmash that we’ve seen for decades.

Generally we agree with Jassy’s assessment – but we do see things changing.

The Cloud Thesis

First let’s recap the basic premise. Cloud is winning in the marketplace. Building data centers is not the best use of capital unless you are a data center operator a hyperscaler or maybe a SaaS provider – maybe. So more and more work will continue to move to the cloud. We see three big waves of cloud:

- Wave 1 – Public. The first wave of the cloud was public cloud. A cloud of remote infrastructure services for obvious workloads like Web, test/dev, analytics and SaaS offerings.

- Wave 2 – Hybrid. The second wave of cloud was…or should we say is, about hybrid. Connecting remote cloud services to on-prem workloads.

- Wave 3 – Multi. The third wave which is hitting somewhat in parallel is multicloud.

Cloud is Reminiscent of Early Networking Days

It’s not a perfect analogy but these multigenerational waves remind us of the early days of networking. Some of you may remember that years ago the industry was comprised of multiple dominant vendors that controlled their own proprietary network stacks. IBM had SNA, Digital had DECNet, all the minicomputer vendors had their own proprietary NETS.

In the early-to-mid 1980s the OSI model emerged with the objective of creating interoperability amongst different communications systems by standardizing on protocols. The model had seven layers from the physical all the way through the application. But it was largely a pipe dream because it was too complicated and expected customers to rip and replace existing networks and standardize on OSI. That was never going to happen.

However it opened the door for new companies and you saw firms like Cisco and 3Com emerge with TCP/IP and Ethernet becoming standardized and enabling connections between systems. It changed the industry.

What does this have to do with multicloud?

Well today you have a similar situation with dominant public cloud leaders like AWS and Azure. In this analogy they are the proprietary, siloed networks of the past like IBM and Digital.

But ultimately, customers are going to put workloads on the right cloud for the job and that includes putting work on-prem and connecting it to the public cloud with a substantially similar and ideally identical experience. That’s hybrid. That’s todays big wave and you’re seeing it with Amazon’s Outposts and VMware with Amazon and Azure Stack.

So while all this hybrid action is getting wired customers are putting work into AWS and Azure and Google and the IBM Cloud and the Oracle cloud and so forth. Customers are wanting to connect across clouds with a substantially similar experience, which reduces costs and speeds outcomes. This is multicloud.

Now we’re not suggesting that Amazon and Microsoft will go the way of the minicomputer vendors. Today’s leaders are much more savvy and tuned in to surfing the waves. But they don’t have an automatic right of passage. If they ignore the trends they will face challenges.

The Industry Pivots to Multicloud via Kubernetes

Today we’re seeing the emergence of some big whales connecting their infrastructure – like AWS and VMware and Microsoft and Oracle and IBM Red Hat with everyone, Cisco, Dell and HPE with everyone…Google with Anthos and many players staking a claim in this hybrid and multicloud world.

But you also have these emerging players innovating. Companies like CrowdStrike in security, Qumulo in file storage, Clumio in backup and many dozens of well-funded players looking to grab a share of the multicloud pie.

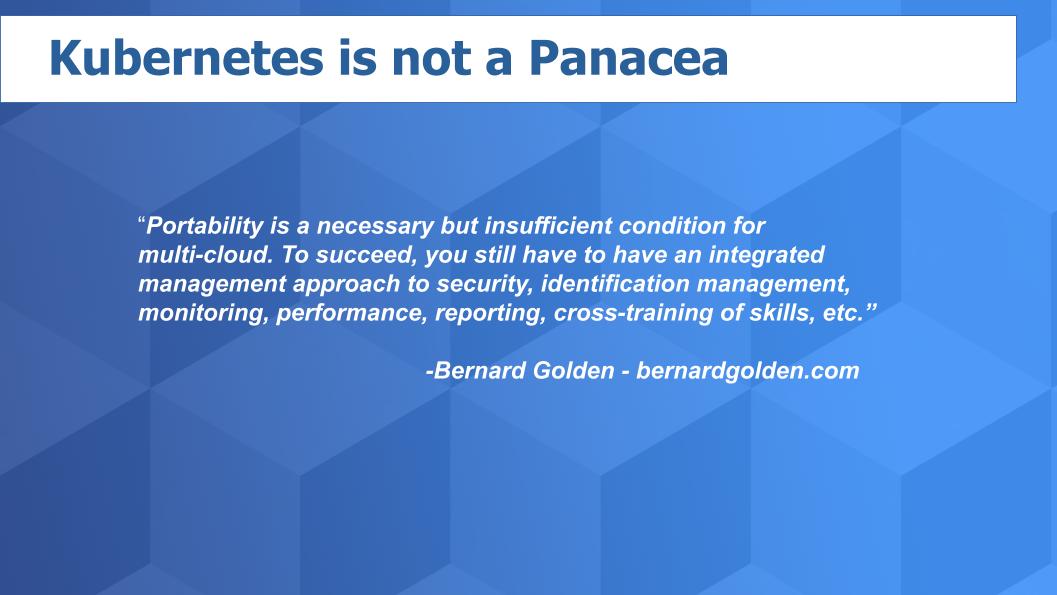

And it’s worth pointing out that they’re all going crazy over Kubernetes. Which makes sense because Kubernetes has emerged as a standard. It’s popular with developers because it enables portability and allows them to package applications and all the related dependencies and then hand that app off for testing or deployment and it will behave the exact same was as when they ran it locally.

But Kubernetes is not a panacea. Bernard Golden made a great point to us recently about Kubernetes and containers. Here’s what he said:

We see Kubernetes and its progeny becoming a ubiquitous component within virtually every vendor’s offerings. We talk today like Kubernetes is this separate entity. Over the next couple of years we see it becoming invisible.

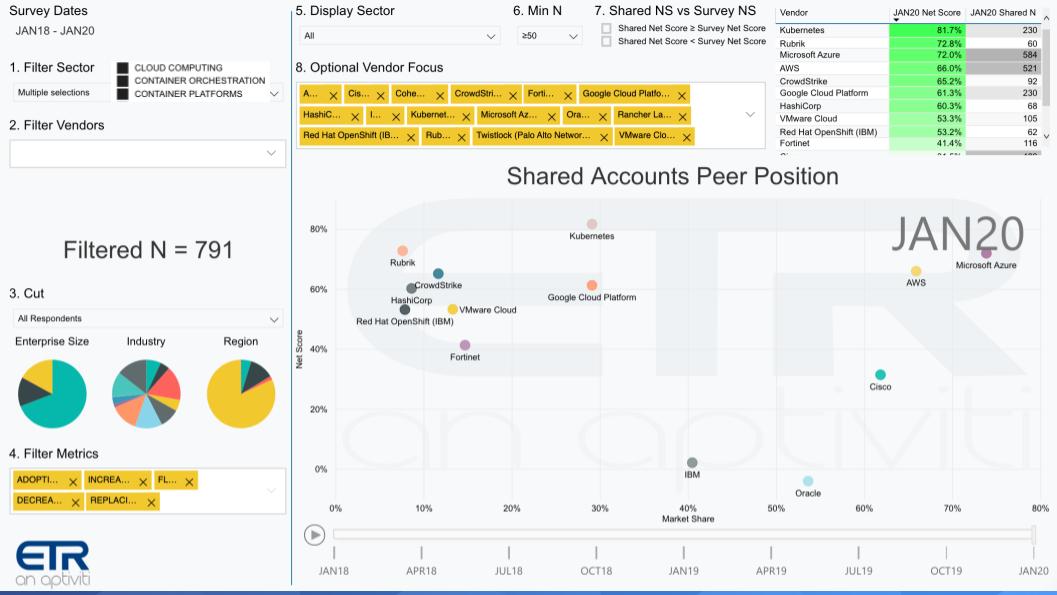

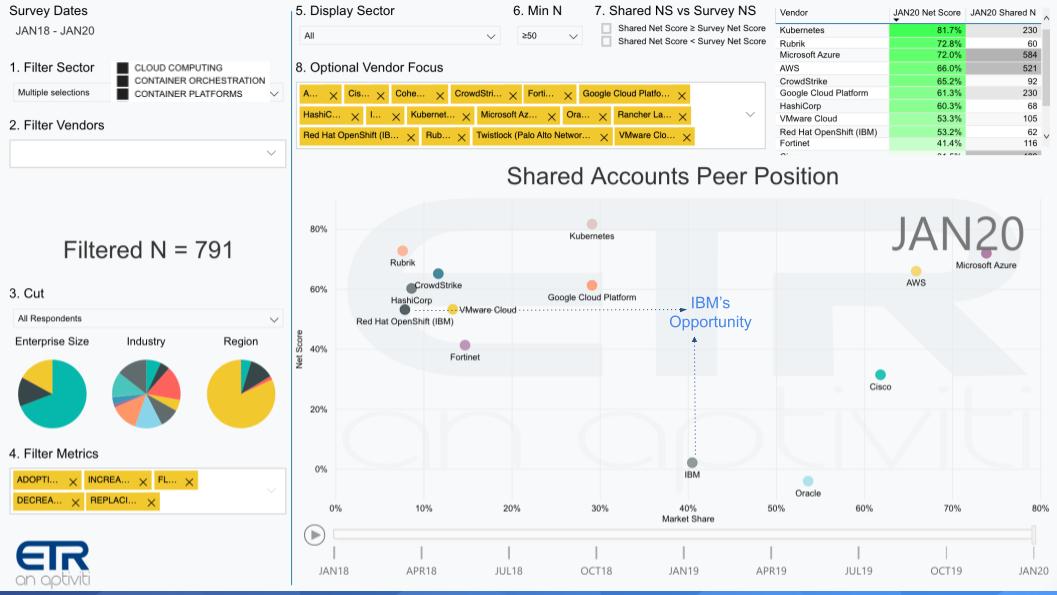

Sizing up the Multicloud Landscape

As we always do in these segments, we want to bring in the ETR perspective ETR has lots of data on multicloud from their Venn meetings and other surveys. But what we’ve done in the chart below is pulled some data that we are using as indicators and proxies for multicloud.

You can’t go out and buy some multicloud today…there is no standardized product or solution. What we have to do is highlight some of the trends in the data and draw some inferences by using proxies.

What the chart above shows is the relative position of a number of companies that are participating in the multicloud arena. The chart plots each vendor’s Net Score, or spending momentum on the Y-Axis juxtaposed to Market Share on the X-Axis, which is a measure of pervasiveness.

What we have done is filter on three sectors – cloud, container orchestration and container platforms. So these are buyers – 791 of them as you can see by the N – who are spenders in these three areas. And we are isolating on a select group of company names. As a last filter we selected only companies with 50 or more results from this multicloud sector proxy.

The following points are relevant:

- We understand Kubernetes is not a company. However, ETR captures spending on Kubernetes. It’s one of the hottest areas in the data set with a nearly 82 percent Net Score. So we show that as a reference point.

- We highlight Azure and AWS. Once again, as in previous Breaking Analysis segments, we see those two out in the lead with both companies showing very strong spending momentum. While AWS doesn’t explicitly have a multicloud offering, in our view, you can’t talk about multicloud without including the leading cloud supplier. You also see Google – it doesn’t have the Market Share (pervasiveness) of the big 2. However, Google ios showing a strong Net score and well-positioned for multi-cloud with Anthos.

Remember this is a proxy we are running. Its not necessarily a reflection of a firm’s specific multicloud offering – it’s an indicator based on the filters we ran.

Multicloud is not Just Big Companies

Now let’s take a look at some of the others. Rubrik, the data protection specialist, and Crowdstrike the security darling, show strength. Both have multicloud offerings and strategies. Hashicorp also stands out an is an important player in our view as they provide developer tooling to run, secure and deploy applications across clouds.

VMware Cloud (VCF) is right there in the mix. You also see Fortinet as well executing from a security position with a nice cloud portfolio, especially in SD-WAN.

How IBM, Oracle & Cisco are Positioned

We call your attention to IBM and Red Hat OpenShift in the chart below. Look at their respective positions. IBM’s spending velocity or Net Score is low but Red Hat’s is quite strong. This is new CEO Arvind Krishna’s opportunity – leverage IBM’s large installed presence and services prowess – shown here as Marketshare or pervasiveness – to shift Red Hat to the right. And leverage OpenShift’s coolness to increase IBM’s relevance and elevate its spending velocity.

If Arvind makes the kind of progress we show here, he may end up as CEO of the decade.

We also put Oracle on the chart because of their multicloud relationship with Microsoft, which we think has good potential for mission critical apps running Oracle Database as it aligns Oracle with Microsoft’s superior cloud estate. As we’ve noted many times – IBM and Oracle both have clouds. They’re not hyperscale clouds but they have large installed software franchises that can insulate them from IaaS pricing competition.

Finally we have to mention Cisco who we’ve said many times comes at multicloud from a position of strength in networking and security with a huge market presence. Not without challenges but they’re a player in multicloud as well.

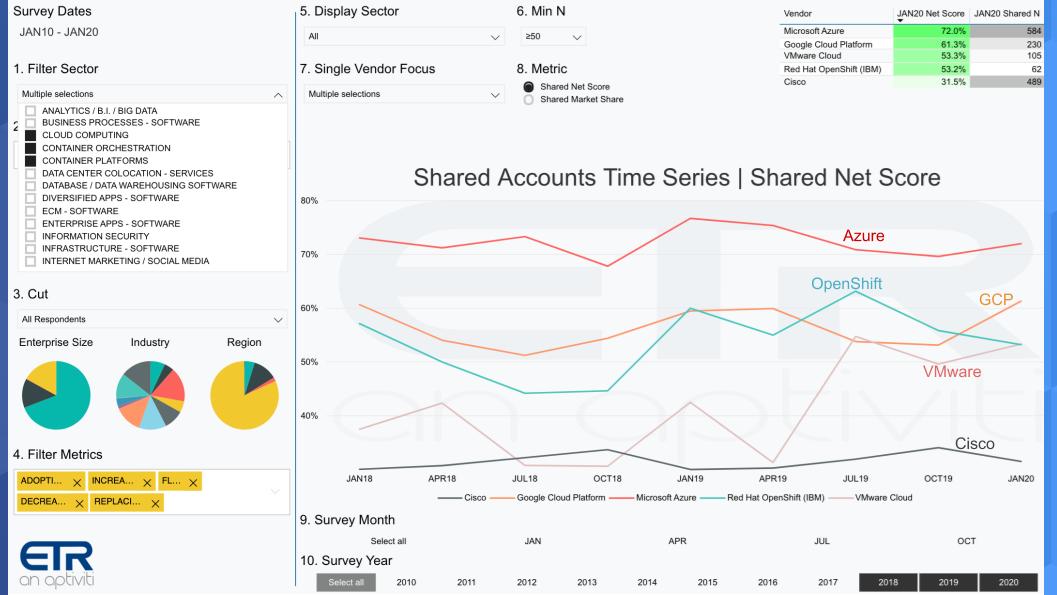

Spending Momentum of Five Whales

In the chart below, we look at some similar proxy data – basically the same cut as above – isolated on a few big players in multicloud.

The chart above shows five big players spending momentum or Net Score within cloud and container sectors. Azure leads, GCP shows strength, IBM Red Hat with OpenShift and VMware all with solid Net Scores in the green. Cisco is not as strong but its Shared N or presence in the data set for this cut is significant at 489. Only Microsoft has a larger position in these markets.

The takeaways here are: 1) This is a wide open race – you really cant pick a winner yet; and 2) Each will come at this from their own unique position of strength.

How Multicloud will Evolve

Which brings us to how we see this space evolving.

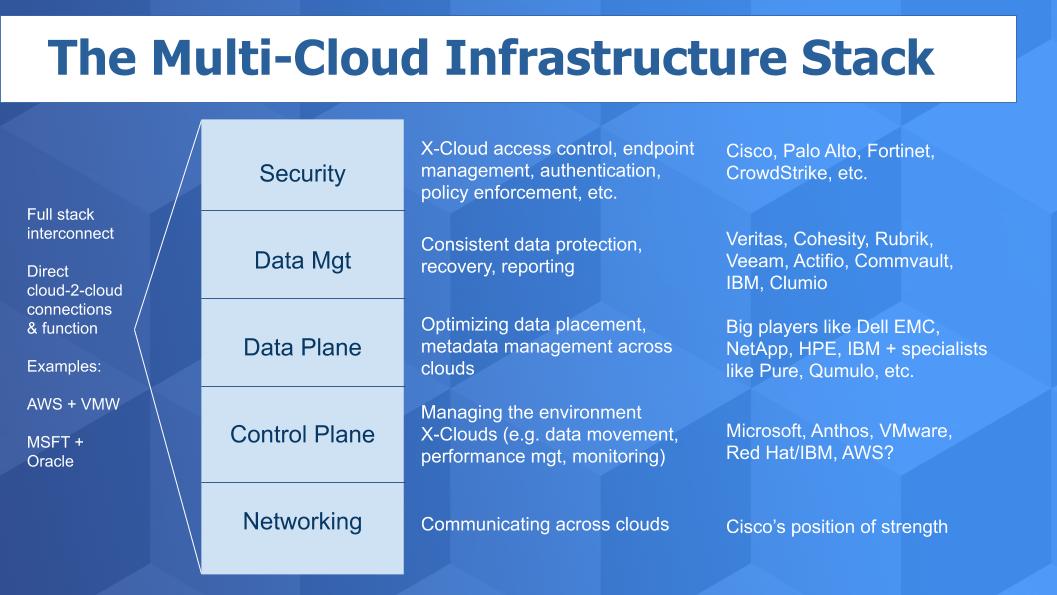

The chart below shows how we see the multicloud infrastructure stack emerging. Starting at the bottom, we show in the stack networking to cross connect clouds and this is where Cisco has to win the day. Some big players are going after the control plane including Microsoft Arc, Google with Anthos, VMware with Tanzu, IBM Red Hat and we think eventually AWS will enter the game in some form.

In the data plane you have some of the largest storage companies like Dell EMC, NetApp, HPE and IBM; as well as specialists like Pure Storage in block and Qumulo in file, bringing innovations across clouds.

Then in data management and data protection you have a number of companies like Veritas, Cohesity, Rubrik, Veeam, Actifio, Commvault, Clumio and IBM as well.

Security is a crowded and burgeoning space with big portfolio plays from the likes of Cisco, Palo Alto Networks and Fortinet along with many of the security specialists we’ve highlighted in the past – like Crowdstrike, Proofpoint and many others.

On the leftmost side of this chart we show the full stack interconnects. Here we refer to the direct cloud to cloud connections and functions up and down the entire stack. Examples are AWS and VMWare – yes hybrid but also the emerging edge…and Microsoft with Oracle.

The bottom line is we see a battle brewing between the big companies with large appetites gobbling up major portions of the market with integrated suites, and that playing out within each layer of the stack. We see competition from smaller, nimble players that are delivering best of breed function and innovation.

Summarizing Multicloud

In the chart below we re-state the questions we asked up front.

What is multicloud

First, we feel like everything in IT is additive meaning we never get rid of stuff. The typical enterprise has multiple data centers, many SaaS providers, more than one IaaS provider and is starting to think about what they are doing for Edge Computing.

There is no standard for hybrid or multi-cloud deployments. If you speak to 100 customers you’ll hear 120 different environments and even more challenges. Nonethless, we see multi- as a superset of hybrid- as a superset of public cloud.

Do we really need multicloud?

In an ideal world, no…we wouldn’t need multicloud. But we talked about how we got here earlier. How real is it? Well, companies use multiple clouds. Is it easy to do things across clouds? No. So it’s one of these problems the industry has created and now they can make money fixing it – it’s a vicious cycle, but so goes the IT business.

What problems does multicloud solve and create?

The goal of multicloud should be that it creates more value than just the sum of its individual parts. That’s not happening yet. Moving data around is a problem so ultimately the value comes from being able to bring cloud services to data that resides in a distributed global system. As Bernard Golden implied – even with Kubernetes this experience is far from seamless. So we understand that technology created this problem and IT people, processes and tech will be asked to clean it up – a common story in enterprise Tech.

How will Multicloud Progress?

We talked about how multicloud will evolve along a stack that is comprised of specialists and big companies with very big appetites. Our opinion is that multicloud will evolve as a mishmash and vendor relationships, right tools for the right job, edge…IT and OT tensions, mergers, etc. will create an even bigger mess down the road. Which of course means more opportunity for the industry as a whole.

We have well funded companies that are exceedingly capable in this business and the leaders will get their fair share. Cloud is a trillion dollar market and there will not be one winner in multicloud in our view.

Who Wins in Multicloud?

We’ve tried to lay out some of the leaders within different parts of the stack but theres much more to the story. we do believe the cloud players are well positioned…right now Microsoft and Google but we definitely think AWS will play…but as well, VMware, Red Hat, Cisco etc. come at this from respective positions of strength and some have the added benefit of being cloud agnostic. This is a two-edged sword because they either have no cloud or one that’s not competitive with hyperscale cloud

Google Cloud is the possible exception because it’s behind AWS and Azure, so it must play nice with multicloud. But eventually Google wants data to land in its cloud.

And as always – the specialists will solve problems that are too small initially for the big companies to see but these areas will grow and allow some of the upstarts to reach escape velocity.

Multicloud, in and of itself, is becoming real…one that we believe will be attacked from a position of strength within the stack with specialists opportunities up and down the stack.

We appreciate the comments we get on our LinkedIn posts and on Twitter @dvellante so thanks for those. Also, you may want to check out this ETR Tutorial we created, which explains their spending methodology in more detail.

Here’s the full video analysis of this week’s segment: