Last year we noted in a Breaking Analysis that the cloud ecosystem is innovating beyond the notion of multicloud. We’ve said for years that multicloud is really not a strategy but rather a symptom of multivendor. We used the term supercloud to describe an abstraction layer that resides above and across hyperscale infrastructure, connects on premises workloads and eventually stretches to the edge. Our premise is that supercloud goes beyond running services in native mode on each individual cloud. Rather supercloud hides the underlying primitives and APIs of the respective cloud vendors and creates a new connection layer across locations.

Since our initial post, we’ve found many examples within the ecosystem of technology companies working on so-called supercloud in various forms. Including some examples that actually do not try to hide cloud primitives but rather are focused on creating a consistent experience for developers across the devsecops tool chain, while preserving access to low level cloud services.

In this Breaking Analysis we share some recent examples of supercloud that we’ve uncovered. We also tap theCUBE network to access direct quotes about supercloud from the many CUBE guests we’ve recently had on the program. Here we test the concept’s technical and business feasibility. We’ll also post some recent ETR data to put into context some of the players we think are going after this opportunity and where they’re at in their supercloud buildout.

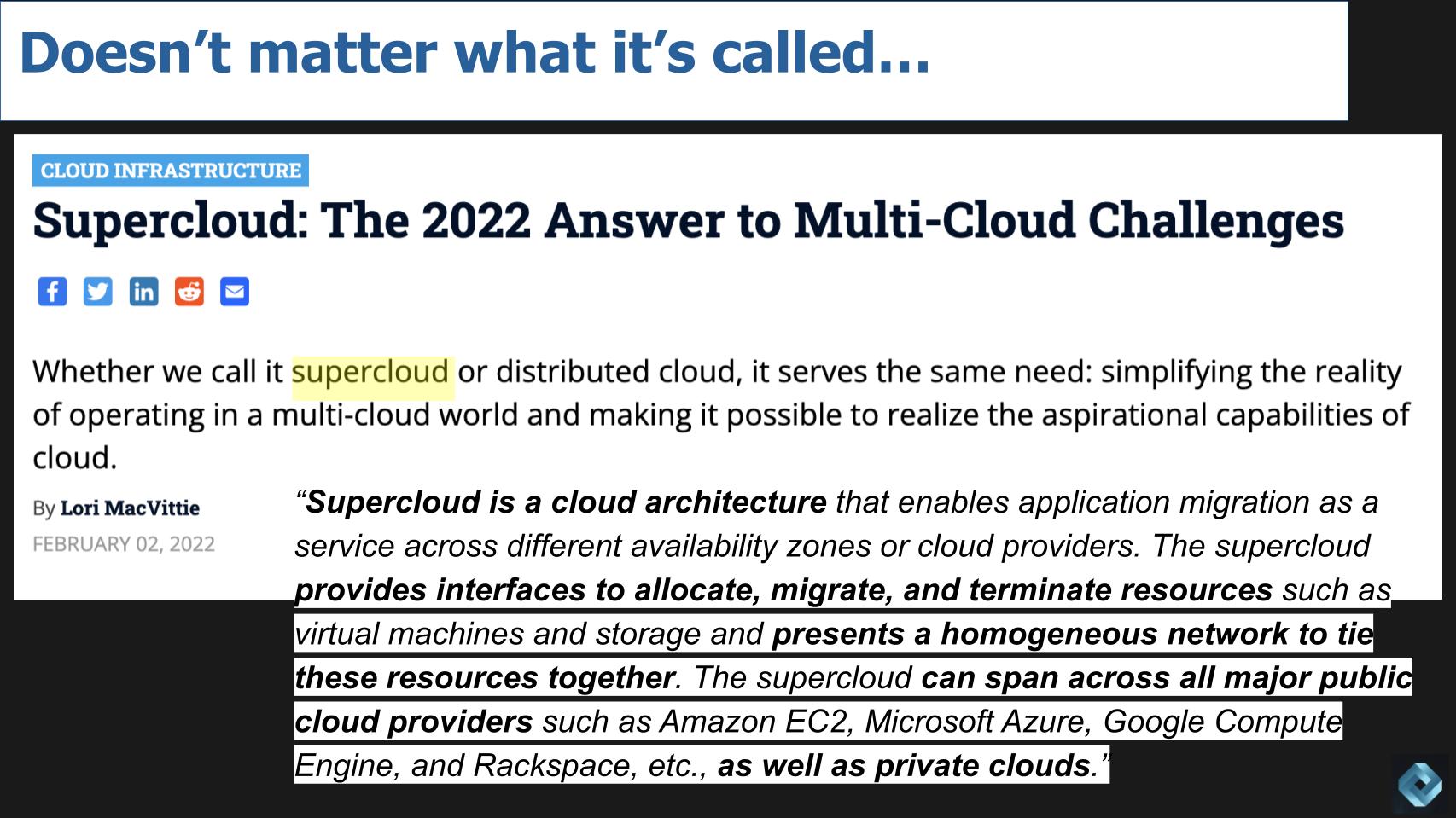

Supercloud: The 2022 Answer to MultiCloud challenges.

In our background research we found an article from earlier this year by Lori MacVittie entitled Supercloud: The 2022 Answer to Multi-Cloud challenges.

What really interested us here is not just the title…but the notion that it really doesn’t matter what it’s called. Supercloud, distributed cloud, someone even called it metacloud recently – we’ll get to that. Lori is a technologist and a developer by background. She wrote that she’s partial to the supercloud definition put forth by Cornell, which is shown above.

The Cornell definition sounds about right. It doesn’t touch on edge and maybe that’s prudent. Nonetheless, the Cornell statement provides further confirmation that something new is happening out there.

Business & Technology Execs Weigh in on Supercloud

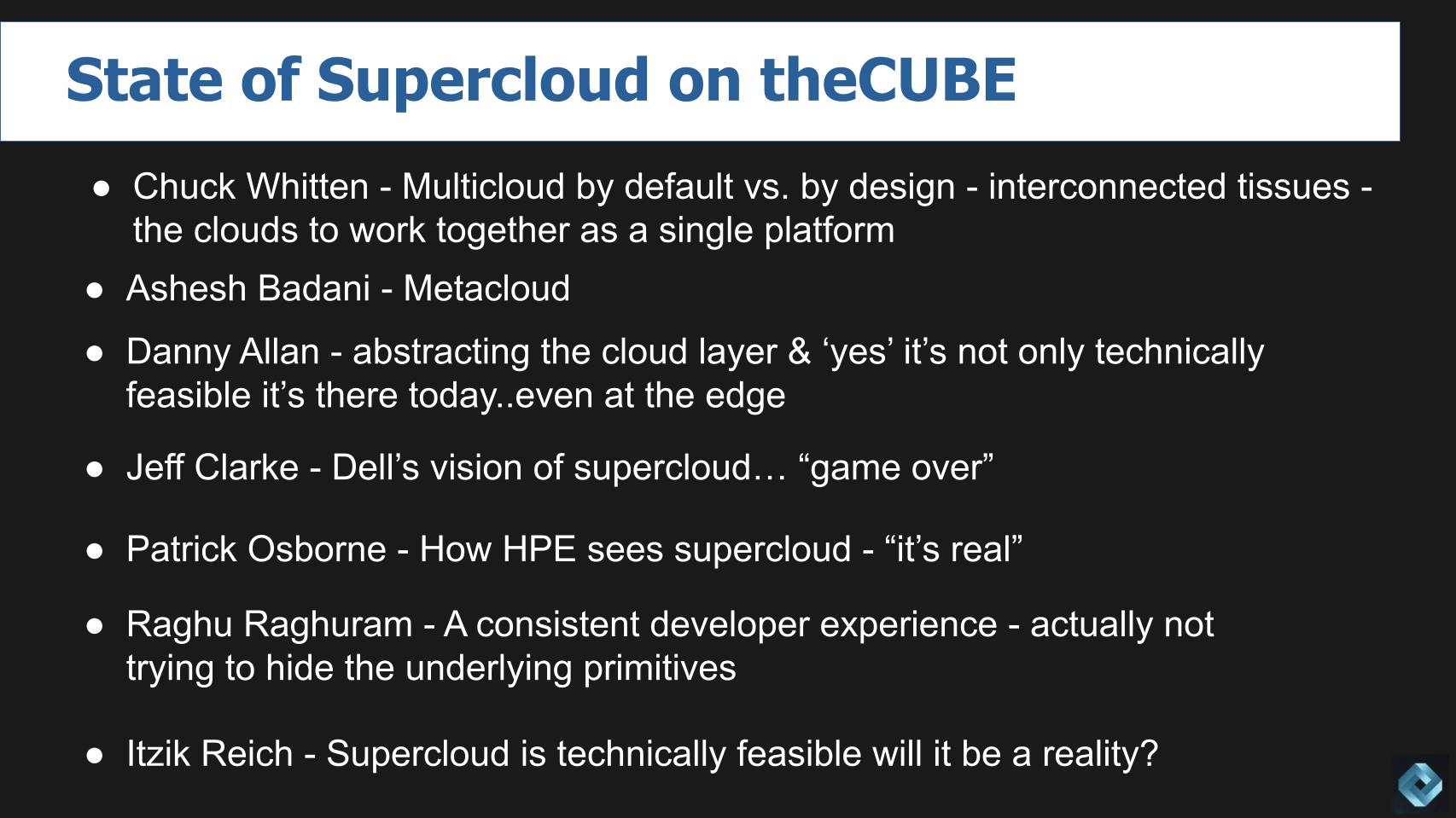

In the past several weeks and months we’ve interviewed a number of executives, technical experts, CTOs, product developers and industry leaders on supercloud. Here’s a summary list of the people whose verbatim quotes we’ve captured on the topic.

Chuck Whitten is Dell’s new co-COO and most likely part of the succession plan many years down the road. He coined the phrase multicloud by default vs multicloud by design and provides a business perspective. We’ll hear from Chuck a couple of times including one where John Furrier asks him about leveraging hyperscaler CAPEX.

Ashesh Badani heads products at Red Hat and talks about the metacloud. Again it doesn’t matter to us what you call it.

We have a couple of clips from Danny Allan who is CTO of Veeam and can get super technical. He talks about how Veeam abstracts the cloud layer and he describes what a supercloud is to him. And then we bring edge into the discussion. The bottom line from Danny is we want to know…is supercloud technically feasible and is it a thing?

Then we have Jeff Clarke who is Dell’s co-COO and Vice Chairman. He lays out his vision of supercloud in the context of what John Furrier calls a “business operating system” Jeff has a drop the mic moment when he says if we can do _____…it’s game over.

Patrick Osborne is VP of the storage business unit at HPE. Given that Jeff Clarke of Dell, one of HPEs largest competitors, has a game over strategy, we wanted to understand how HPE sees supercloud. The bottom line according to Patrick is “it’s real.”

Raghu Raghuram, CEO of VMware throws a curve ball at the supercloud concept…he flat out says “no we don’t want to hide the underlying primitives.” Raghu explains that VMware’s strategy is to create a consistent developer experience in the DevSecOps toolchain & kubernetes runtime environments. Where VMware tooling connects all the elements in the application development stack.

We end on Itzik Reich, a technologist and technical team leader who has worked as a go between customers and product developers for years, translating requirements into product. We ask Itzik if supercloud is technically feasible and will it be a reality?

Here’s a summary of the comments from these CUBE guests.

Chuck Whitten – Multicloud by Default vs. Multicloud by Design

In his keynote at Dell Technologies World, Whitten talked about multicloud by default versus multicloud by design. We asked what he means by that:

Well, look, customers have woken up with multiple clouds, multiple public clouds, on-premises clouds; increasingly as the edge becomes much more a reality for customers clouds at the edge. And so that’s what we mean by multicloud by default. It’s not yet been designed strategically. I think our argument yesterday was, it can be and it should be. It is a very logical place for architecture to land because ultimately customers want the innovation across all of the hyperscale public clouds. They will see workloads and use cases where they want to maintain an on-premise cloud, on-premise clouds are not going away. I mentioned edge clouds, so it should be strategic. It’s just not today. It doesn’t work particularly well today. So when we say multicloud by default we mean that’s the state of the world today. Our goal is to bring multicloud by design as you heard.

[Listen to Chuck Whitten’s commentary].

Ashesh Badani – Metacloud

Since you and I talked, Dave, I’ve been spending some time noodling just over the question of supercloud. And you’re right. There’s probably some terminology, something that will get developed either by us or in collaboration with the industry. Where we sort of almost have the next almost like a Metacloud that we’re working our way towards.

[Listen to Ashesh Badani explain Metacloud].

Danny Allan – Supercloud & Veeam’s Portable Data Format

We were having a discussion with Danny Allan on theCUBE and we asked him to explain the nuance of the statement that “snapshots don’t equate to backup” and how that relates to supercloud. Here’s what he said:

We manage both the snapshots and we convert it into the Veeam portable data format. And here’s where the supercloud comes into play. Because if I can convert it into the Veeam portable data format, I can move that OS anywhere. I can move it from physical to virtual, to cloud, to another cloud, back to virtual, I can put it back on physical if I want to. It actually abstracts the cloud layer. There are things that we do when we go between cloud some use BIOS, some use UEFI, but we have the data in backup format, not snapshot format, that’s theirs, but we have it in backup format that we can move around and abstract workloads across all of the infrastructure.

>>And your catalog is control in control of that. Is that right?

Yeah it is, 100%. And you know what’s interesting about our catalog, Dave, the catalog is inside the backup. Yes. So here’s, what’s interesting about the edge, two things, on the edge you don’t want to have any state, if you can help it. And so containers help with that You can have stateless environments, some persistent data storage But we not not only provide the portability in operating systems, we also do this for containers. And that’s true. If you go to the cloud and you’re using say EKS with relational database services RDS for the persistent data later, we can pick that up and move it to GKE or move it to OpenShift On-Premises. And so that’s why I call this the supercloud, we have all of this data. Actually, I think you termed the term supercloud.

>>Thank you… I mean, I’m looking for a confirmation from a technologist that it’s technically feasible.

It is technically feasible and you can do it today.

[Listen to Danny Allan describe the technical aspects of Veeam’s approach to supercloud].

Jeff Clarke – “Game Over”

John furrier asked Jeff Clarke: “You said also technology and business models are tied together and an enabler. If you believe that then you have to believe that it’s a business operating system that customers want. They want to leverage whatever they can. And at the end of the day, they have to differentiate.” Clarke responded as follows:

Well, that’s exactly right. If I take that in what Dave was saying and I summarize it the following way, if we can take these cloud assets and capabilities, combine them in an orchestrated way to deliver a distributed platform… game over.

[Listen to Jeff Clarke’s mic drop “game over” comment].

Patrick Osborne – Hewlett Packard Enterprise

Given that HPE is one of Dell’s largest competitors and hearing Jeff Clarke’s “game over” comment, we wanted to see how HPE was thinking about supercloud. Remember, HPE and Dell are in a mindshare battle right now both pushing and evolving their respective as-a-service offerings, HPE GreenLake and Dell APEX. Here’s Patrick Osborne’s take:

We have a number of platforms that are providing whether it’s compute or networking or storage, running those workloads… they plumb up into the cloud, they have an operational experience in the cloud and they have data services that are running in the cloud for us in GreenLake. So it’s a reality, we have a number of platforms that support that. We’re going to have a a set of big announcements coming up at HPE Discover. So we led with Alletra and we have a block service. We have VM backup as a service and DR on top of that. So that’s something that we’re providing today. GreenLake has over, I think it’s actually over 60 services right now that we’re providing in the GreenLake platform itself. Everything from security, single sign on, customer IDs, everything. So it’s real. We have the proofpoints for it.

[Listen to Patrick Osborne talk about HPEs GreenLake services & the fit with supercloud].

Raghu Raghuram – Consistent Developer Experience with Access to Primitives

VMware is now a completely independent company after the Dell spin. For years between EMC’s Federation and Dell’s acquisition of EMC, VMware was a participant in shuffling the deck with a number of what we called the “island of misfit developer toys,” stemming from acquisitions EMC had made, including most notably Pivotal. During its Dell-owned tenure in 2019, VMware launched Tanzu, a suite of software tools to manage Kubernetes clusters across private and public clouds. Importantly, Tanzu enables K8s to be treated as first class citizens in VMware. It’s VMware’s competitive offering to Red Hat’s OpenShift and will enable the building out of superclouds. As our supercloud definition cites, a PaaS layer across clouds is a necessary enabler to building superclouds.

Here’s how Raghu describes VMware’s strategy when we asked him about supercloud:

So I want to clarify something that you said because this tends to be very commonly confused by customers. I use the word abstraction. And usually when people think of abstraction, they think it hides capabilities of the cloud providers. That’s not what we are trying to do. In fact, that’s the last thing we are trying to do. What we are trying to do is to provide a consistent developer experience regardless of where you want to build your application. So that you can use the cloud provider services if that’s what you want to use. But the DevSecOps tool chain, the runtime environment which turns out to be Kubernetes and how you control the Kubernetes environment, how do you manage and secure and connect all of these things. Those are the places where we are adding the value.

And so really the VMware value proposition is you can build on the cloud of your choice but providing these consistent elements, number one, you can make better use of us, your scarce developer or operator resources and expertise. And number two, you can move faster. And number three, you can just spend less as a result of this. So that’s really what we are trying to do. So I just wanted to clarify the word abstraction.

In terms of where are we? We are still, I would say, in the early stages. So if you look at what customers are trying to do, they’re trying to build these greenfield applications. And there is an entire ecosystem emerging around Kubernetes. Kubernetes is not a developer platform. The developer experience on top of Kubernetes is highly inconsistent. And so those are some of the areas where we are introducing new innovations with our Tanzu Application Platform. And then if you take enterprise applications, what does it take to have enterprise applications running all the time be entirely secure, et cetera…

[Listen to Raghu Raghuram clarify VMware’s position on the abstraction layer].

Chuck Whitten – An Interconnected Tissue

Well, look, the multicloud by default today are isolated clouds. They don’t work together. Your data is siloed. It’s locked up and it is expensive to move and make sense of it. So I think the word [John] and I were batting around before, this is an interconnected tissue. That’s what the world needs. They need the clouds to work together as a single platform. That’s the problem that we’re trying to solve. And you saw it in some of our announcements here that we’re starting to make steps on that journey to make multicloud work together much simpler.

>> It’s interesting, you mentioned the hyperscalers and all that CapEx investments. Why wouldn’t you want to take advantage of a cloud and build on the CapEx and then ultimately have the solutions machine learning as one area. You see some specialization with the clouds. But you start to see the rise of superclouds, Dave calls them, and that’s where you can innovate on a cloud then go to the multiple clouds. Snowflakes is one, we see a lot of examples of supercloud…

>> Project Alpine was another one. I mean, it’s early, but it’s clearly where you’re going. The technology is just starting to come around…it’s real.

Yeah. I mean, why wouldn’t you want to take advantage of all of the cloud innovation out there?

[Listen to Chuck Whitten’s commentary on leveraging hyperscale CAPEX infrastructure].

Itzik Reich – Is the Supercloud Feasible?

I think it is. So for example Caitlin Gordon, which I believe you’ve interviewed earlier this week, was demonstrating the Kubernetes data mobility aspect which is another project. That’s exactly part of the rationale. The rationale of customers being able to move some of their Kubernetes workloads to the cloud and back and between different clouds. Why are we doing that? Because customers wants to have the ability to move between different cloud providers, using a common API that will be able to orchestrate all of those things with a self-service [platform] that may be offered via the APEX console itself. So it’s all around enabling developers and meeting them where they are today and also meeting them into tomorrow’s world where they actually may have changed their mind to do those things. So yes we are working on all of those different aspects.

[Listen to Itzik Reich talk about the reality of supercloud].

Sizing up a Few Supercloud Players

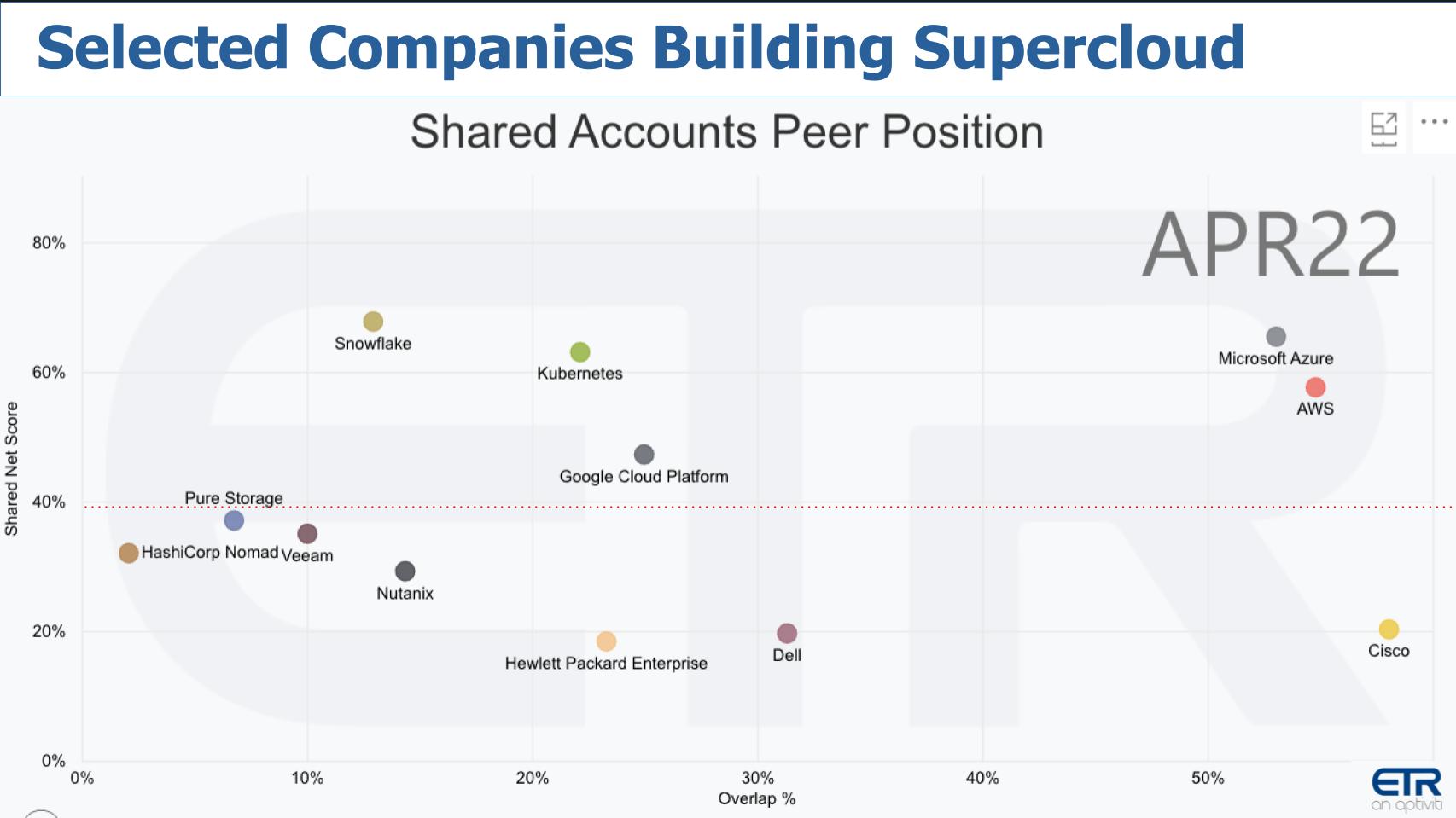

Let’s quickly look at some ETR data. ETR doesn’t have a category called supercloud, but we can infer from the data the survey the relative scope of some possible competitors.

Above is an XY graph that plots Net Score or spending momentum on the Y axis and Overlap or pervasiveness in the ETR data set on the X axis. The red dotted line is rarified air where anything above that is considered highly elevated. We plot Azure, AWS, GCP and Kubernetes as reference points and we’ve cherry picked a few players we believe are building or important for supercloud buildout.

Snowflake we’ve talked about a lot. We see the Snowflake Data Cloud as a supercloud in the making. Pure storage made public the early part of its supercloud journey at Accelerate 2019 when it unveiled a hybrid block storage service in AWS. Hashicorp is enabling infrastructure as code across different clouds and locations. Nutanix is embarking on a multicloud strategy but is doing so in a way that we believe is supercloudlike.

Now Veeam – we were just at VeeamOn 2022 – and this company has tied Dell for the #1 revenue player in data protection according to IDC. It likely won’t be long before it holds that position alone as it’s growing faster than Dell in the space. Veeam is a pure play vendor and you heard their CTO Danny Allen’s view on supercloud earlier in this episode. According to Allan they’re doing it today. And we’ve also heard extensive comments from Dell and HPE, plotted above. Two companies that are finally embracing the cloud and formulating more cogent as-a-service strategies.

And finally Cisco. We don’t have any direct quotes or data at this time other than to show you the size of Cisco’s footprint in the ETR dataset on the X axis. This ETR data includes a cut across all sectors of the ETR taxonomy and you can see the magnitude of Cisco’s presence– it’s large. We feel Cisco had better be building a so-called supercloud or something similar or they will be left behind. We’re quite certain Cisco will be in the game.

Risks to the Supercloud Scenario

So we’re seeing lots of evidence that what we said last year is taking shape and supercloud is becoming a thing; and really is the future of cloud. But there are risks to this scenario that we want to acknowledge.

First – we could end up with a bunch of bespoke superclouds that don’t talk to each other…that would not be ideal. Now one supercloud is better than three separate cloud native services that do the same thing from the same vendor – one for AWS, one for GCP and one for Azure. So maybe that’s not all bad but it’s not the preferred customer outcome.

To point number two, we hope there evolves a set of open standards for self-service infrastructure and federated governance that enables data sharing. Ideally that evolve as a horizontal layer versus a set of proprietary vendor specific tools that only work within the confines of a single vendor offering.

As well we see the potential for edge disruptions changing the economics of the data center. Edge in fact could evolve on its own, independent of the cloud and even fork cloud economics. In fact David Floyer sees the edge differently from Danny Allan. Floyer says he sees a requirement for distributed stateful environments that are ephemeral; where recovery is built in. You may be thinking, “stateful ephemeral…isn’t that an oxymoron?”

According to Floyer:

If it’s not ephemeral, the costs will be prohibitive. The biggest mistake companies will make is thinking the edge is an extension of their current cloud strategies. Companies must completely reimagine an integrated file and recovery system which is much more data efficient.

And he believes that the technology will evolve and ship in such massive volumes that eventually new architectures will seep into enterprise cloud and distributed data centers and disrupt the status quo.

In other words, as David Moschella recently wrote – we’re about 15 years into the most recent cloud cycle; and history shows every 15-20 years or so, something new comes along that is a blind spot for and highly disruptive to existing leaders.

As such, #4 above becomes really important in our view. Remember, in 2007, before AWS introduced the modern cloud, IBM outspent Amazon and Google in R&D and CAPEX; and was comparable to Microsoft. But instead of inventing the cloud, it spent hundreds of billions on stock buybacks and dividends and completely whiffed on the opportunity.

Innovation rewards leaders and while it’s not without risks, innovation is what powers the technology industry. It always has and likely always will.

Keep in Touch

Thanks to Stephanie Chan who researches topics for this Breaking Analysis. Alex Myerson is on production, the podcasts and media workflows. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.