In this week’s episode of theCUBE Insights, Powered by ETR, we dig into the”Trillionaire’s Club.” This Breaking Analysis looks at how the big tech companies have changed the recipe for innovation in the enterprise. Specifically, as we enter the next decade we believe it’s important to reset how we look at innovation and the factors that will determine winners and losers. This includes both the sellers of technology and the buyers who apply technology and how it will set the stage for the several decades of economic growth.

In this week’s episode of theCUBE Insights, Powered by ETR, we dig into the”Trillionaire’s Club.” This Breaking Analysis looks at how the big tech companies have changed the recipe for innovation in the enterprise. Specifically, as we enter the next decade we believe it’s important to reset how we look at innovation and the factors that will determine winners and losers. This includes both the sellers of technology and the buyers who apply technology and how it will set the stage for the several decades of economic growth.

Premise

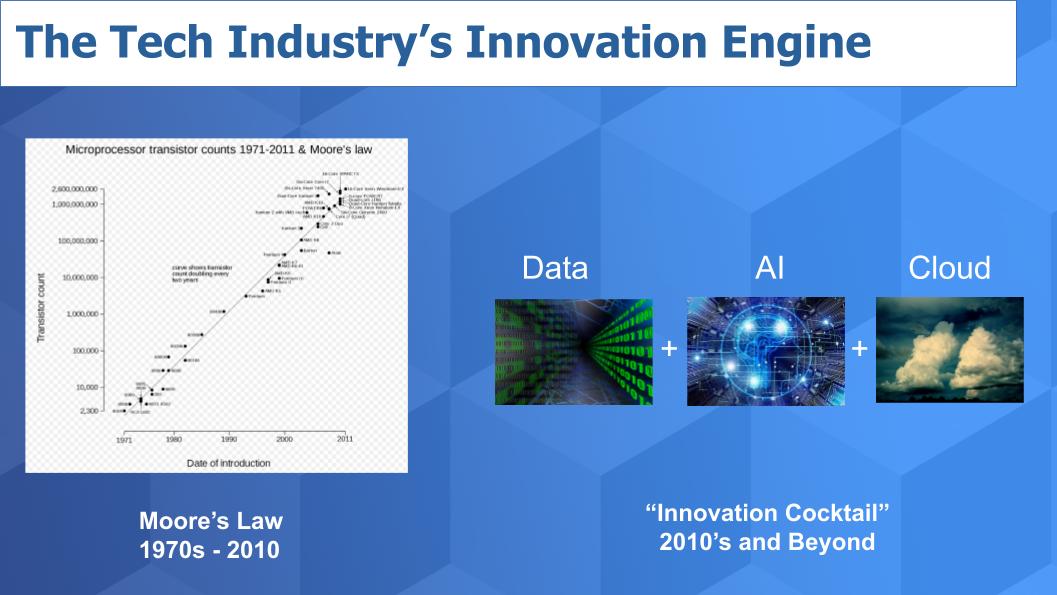

Here’s premise we want to put forth. The source of power in the technology business has been permanently altered. There is a new “cocktail” of innovation that will far surpass Moore’s law in terms of its impact on the industry.

As shown in the chart below, the technology industry has marched to the cadence of Moore’s Law for the past fifty years. That is the doubling of transistor counts every 18 months as shown on the left hand side. This translated as we know into a game of “Chase the Chip”, where being first with the latest and greatest microprocessor brought competitive advantage. We saw Moore’s Law drive the PCs era, client server innovations and it powered the Internet (notwithstanding the network effects of Metcalfe’s Law). It drove the semiconductor industry, the storage business and enabled generations of software to support enterprise automation.

The New Innovation Cocktail

But there’s a new engine of innovation – or what we sometimes call the “Innovation Cocktail.” That’s shown on the right hand side where data plus machine intelligence (i.e. AI) and Cloud are combinatorial technologies that will power innovation for the next 20 plus years. More specifically, ten years of gathering big data have put us in a position now to apply AI. Data is plentiful…insights are not and AI unlocks insights. The cloud brings three things: 1) Agility; 2) Scale and 3) The ability to fail quickly and cheaply. We believe it is these three elements and how they are packaged and applied that will determine winners and losers in the next decade and beyond.

Why is this era now suddenly upon us? We believe there are three main factors. One is cheap storage and compute. Combined with alternative processor types like GPUs that can power AI. And finally the amount of data now readily available to organizations.

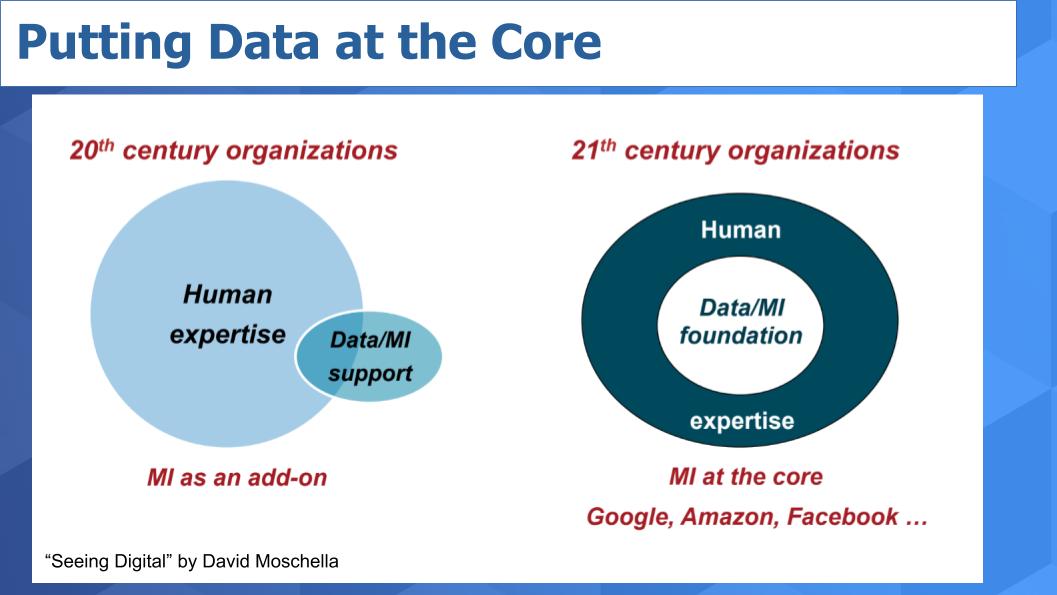

Digital Leaders put Data at the Core

In his ground breaking book Seeing Digital, author David Moschella underscores this point as shown in the diagram below. Incumbent organizations born in the last century organized largely around human expertise or processes or hard assets like factories or a bottling plant for example. These were the engines of competitive advantage. Todays’ successful organizations put data at the core. They live by the mantra of data driven…it’s foundational to them. And they organize expertise, processes and people around the data.

Moschella brought this point home point home in his book and we’ve updated the data here to reflect current market conditions. Just observe the market capitalizations of the top five public companies in the US market. Apple, Microsoft, Google, Amazon and Facebook. We dubbed this chart Cuatro Comas! as a shout out to Russ Hannamen, the crazy billionaire supporting character in the Silicon Valley series on HBO. Each of these companies, with the exception of Facebook, has hit the Trillion dollar club. AWS – like Mr. Hannamen – hit Trillionaire status back in September 2018 but fell back down and lost a comma. These five data-driven companies have surpassed big oil and big finance. The next closest company is Berkshire at $566B. And we would argue if it hadn’t been for the fake news scandal, Facebook probably would be right the trillion dollar valuation range as well.

With the exception of Apple, these companies aren’t highly valued because of the goods they pump out…rather – and we would argue even in the case of Apple – they’re highly valued because they’re leaders in digital and in the best position to apply machine intelligence to massive stores of data that they’ve collected over the past decade. And they have massive scale economics thanks to the cloud.

The Consumerization of IT has Translated to Enterprise Presence

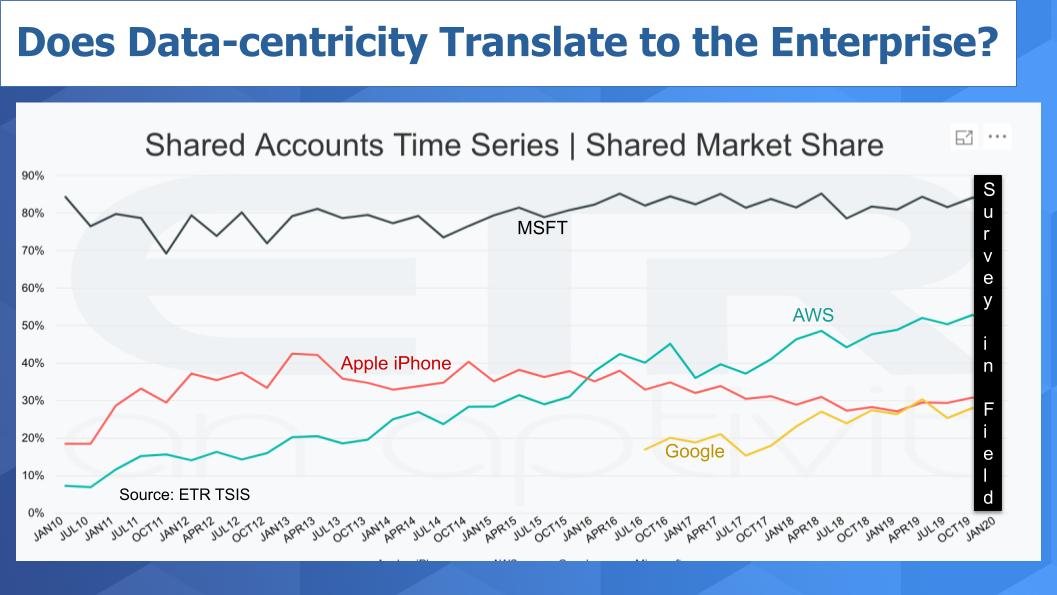

We fully understand that the success of some of these companies is largely driven by the consumer. But the consumerization of IT makes this even more relevant in our view. Let’s bring in some ETR data to see how this translates to the enterprise tech world.

This chart above shows market share for Microsoft, AWS, Apple iPhone and Google in the enterprise all the way back to 2010. Admittedly, the iPhone is a bit of a stretch but kindly give us some latitude on this point. Remember, marketshare in ETR terms is a measure of pervasiveness in the data set (i.e. mentions of a supplier divided by total mentions). Look how Microsoft has held its ground. And you can see the steady rise of AWS and Google. If we superimposed traditional enterprise players like Cisco, IBM, Hewlett Packard Enterprise, Dell EMC, etc. – that is companies that aren’t competing with data at the core of their companies, don’t have a cloud and aren’t generally seen as leaders in AI – you would see a steady decline. We’re required to black out the Jan 2020 survey results but that data will be made public shortly after ETR exits its self imposed quiet period.

We realize Apple iPhone is not a great proxy and Apple isn’t an enterprise tech company but we would argue that Apple’s real value and a key determinant of success going forward lies in how it uses data and applies machine intelligence at scale over the next decade to compete in apps and digital services, content and other adjacencies. And we would say this for these five leaders and virtually any company in the next decade.

The Cloud is Funding AWS’ Entry into Adjacent Industries

The bottom line to us is digital means data and digital businesses are data-driven. Data changes how we think about competition. Just look at Amazon’s moves in content, grocery, logistics…Google in automobiles…Apple and Amazon in music. Notably, Microsoft positions this as a competitive advantage…especially in retail touting Walmart as a partner, not a competitor a la Amazon. The point is that digital, data, AI and cloud bring forth highly disruptive possibilities and are enabling these giants to enter businesses that previously were insulated from outsiders.

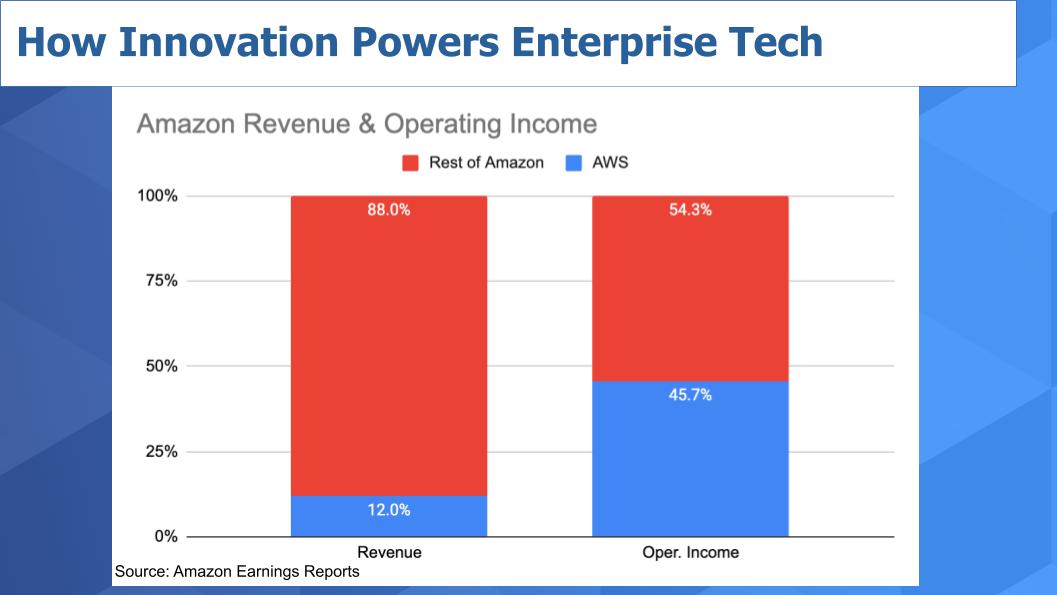

And in the case of the cloud, it’s paying the way. Just look at the data from Amazon in the above chart. The left bar shows Amazon’s revenue. AWS represents only 12 percent of the total company’s turnover. But as you can see on the right hand side it’s almost half of the company’s operating income. So the cloud is funding Amazons entry into all these other businesses and powering its scale.

A key point is that data, as the new source of competitive advantage, allows data-driven companies to enter industries where historically, the barriers of entry were enormous and insulated incumbents from disruption. Because competition is increasingly determined by who has the best data, these tech giants are able to enter new businesses swiftly, with powerful and disruptive impacts.

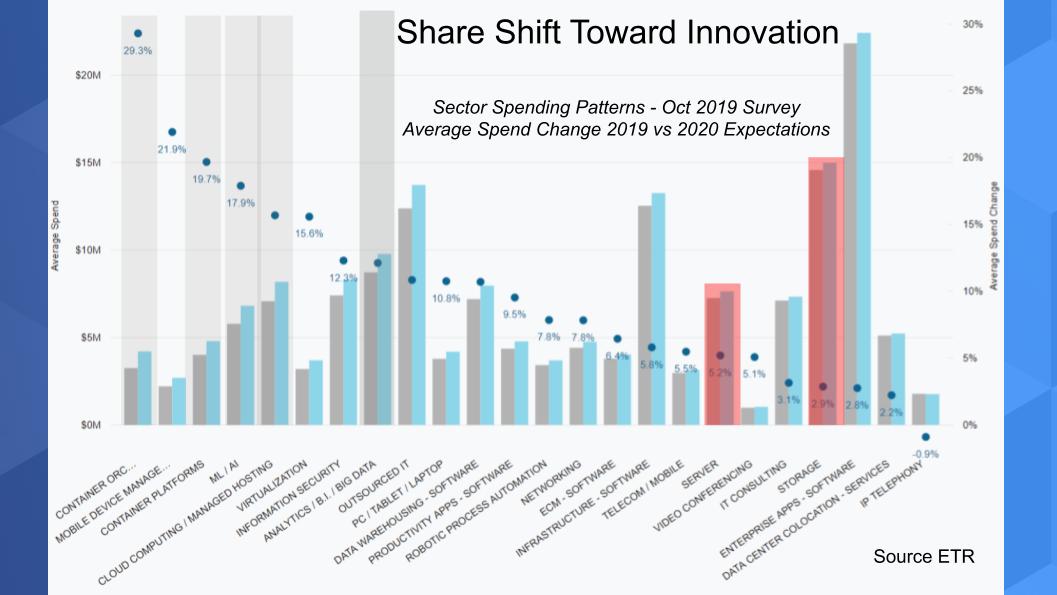

New Innovations are Causing Share Shifts in the Enterprise

Let’s bring in some ETR data to show whats happening in the enterprise in terms of share shifts. The chart below is a double Y axis graph that shows spending levels on the left hand axis, represented by the bars, and the average change in spending represented by the dots.

Focus on the dots and the percentages. Container Orchestration at a 29% change, container platforms show a 19.7%. These are cloud native technologies and it’s becoming clearer that customers are voting with their wallets. Machine Learning and AI, show a nearly 18% uptick in the ETR spending surveys, cloud computing itself, still in the impressive 16% range ten plus years into the cloud. Look at analytics and big data solidly in the double digits growth ten years into the big data movement. So you can see the ETR data shows that the spending action is around cloud, AI and Data– the “Cocktail” technologies– the gray highlighted sectors.

And in the red highlighted segments are Moore’s Law technologies like servers and storage– and you can see they are are growing more slowly in terms of spending outlooks.

Now thats not to say they go away. We fully understand you need servers and storage and networking and databases and software to power the cloud. But this data shows that right now, these discreet “Cocktail” technologies are gaining meaningful spend momentum.

How Can Incumbents Compete with the Digital Natives?

The question we want to leave you with is what does this mean for incumbents that are not digital natives or born in the cloud? The first thing we’d point, and Moschella underscores in his book, is that while the Trillionaire’s look invincible today, history suggests they are not invulnerable. The rise of China, India, open source and open models could coalesce and disrupt these leaders if they miss a step or a cycle or become less paranoid.

The second point we would make is that incumbents are often too complacent. More often than not in our experience, leading organizations in important industries either feel insulated or unmotivated to transform. This is dangerous in our view and there will be fallout as a result. We hear lots of lip service given to digital and data-drivenness but often we see companies that talk but don’t walk the walk. We believe that change will come in every industry and the incumbents will be disrupted…and this will cause action.

The good news is that the incumbents don’t have to build all the tech themselves. They can compete with disruptors by applying machine intelligence to their unique data models via their supply chains, ecosystems, manufacturing data, customer data, etc. and they can buy technologies like AI and cloud from suppliers. The degree to which they are comfortable buying from these suppliers – who may also be competitors – will play out over time but we would argue that building that competitive advantage sooner rather than later with data, and learning to apply machine intelligence to their unique businesses, will allow them to thrive.

These markets are large and the incumbents have inherent advantages in terms of resources, relationships, brand value, customer affinity and domain knowledge that if they apply and transform from the top – with strong leadership and commitment – they will survive and thrive.

Here’s the full video of this week’s Breaking Analysis. Remember these episodes are all available as podcasts and on Dave Vellante’s LinkIn feed under Posts.