Introduction

Converged infrastructure is a large and growing market opportunity requiring huge investments in technology, integration, service delivery, and channel partnerships. All the major systems, storage, networking, and management suppliers have a stake in this market as users are increasingly demanding simplified deployments and fewer siloed solutions. Buyers appear ready to trade individual component performance for integration, marking a turning-point in data center infrastructure.

Converged infrastructure (CI) is an integrated set of compute, storage, and networking components with infrastructure management software that provides a single logical chunk of hardware and software that is either specifically engineered together or at the very least tested and proven in a variety of configurations and applications. Converged infrastructure simplifies hardware and software management and accelerates the deployment of infrastructure for private clouds.

In February Wikibon developed a back of the napkin forecast for the converged infrastructure space. The catalyst for this effort was new data from EMC’s 10K regarding its recognition of VCE revenue and expenses.

We have further refined our figures providing additional granularity on the market data and are providing this update in the Wiki.

Key Findings

Virtually all major infrastructure providers are going after the converged space to either attack legacy installed bases or protect turf. HP, IBM, Oracle, Dell, Cisco, EMC, NetApp, VMware, and VCE all have plays in this space, as do Microsoft and Intel. What follows are our key findings from this research:

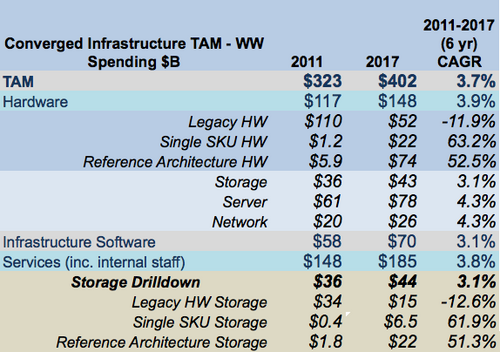

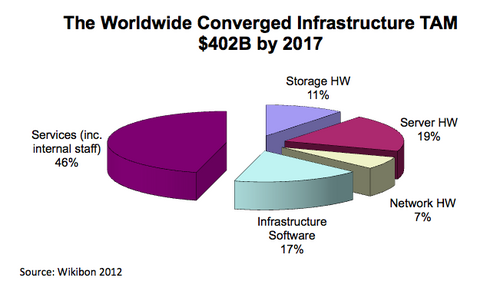

- The converged infrastructure market essentially comprises the entire infrastructure space and is enormous, with a projected $402B total available market (TAM) by 2017.

- Nearly 2/3rds of the infrastructure that supports enterprise applications will be packaged in some type of converged solution by 2017.

- Converged infrastructure comes in two main flavors: a single SKU and a reference architecture. Both of these categories will significantly outpace the growth of legacy, purpose-built infrastructure designed to support a single application. Reference architectures will capture half of the opportunity by 2017 and represent the largest piece of the converged pie.

- The six-year CAGR from 2011 – 2017 for converged reference architectures is 52.5% while single SKU will grow at 63.2% over that same period. Legacy “roll-your-own” infrastructure will decline at an 11.9% CAGR over that same time period.

- Meanwhile, the overall sever, storage, network, and infrastructure market will grow slowly at a six-year CAGR of between 3%-4% over the same timeframe.

- Despite the trend to simplification, converged infrastructure will drag along significant planning, design, deployment, management, and maintenance services. By 2017, services will capture 46% of spending from the $402B TAM.

- The channel will play a significant role in converged infrastructure adoption. Virtually all suppliers are trying to increase the productivity of their sales teams, and the channel will provide leverage and scale for suppliers.

- The channel will demand choice and flexibility in terms of hypervisor, server vendor, network technology, management softwar, and even storage.

Methodology

We estimated the TAM by assuming that the entire server, storage and networking markets were candidates for CI. We set a baseline in 2011 for the entire market based on industry data that is available in published reports, financial analyses, and other public sources, and forecast that through the 2017 timeframe. We also used spending data from the Wikibon community, which included software and services components. We then estimated the percentage that were today and in the future specific to CI, using data from vendor statements and surveys regarding single SKU and reference architecture solutions in the marketplace today.

For this research we defined three deployment options as:

- “Legacy – Roll Your Own” – meaning bespoke stovepipe purchases where the customer or channel does the integration and the solution is purpose-built for a specific application.

- “Reference Architecture” – meaning the configuration has been tested and documented, and best practices have been studied, quantified, and packaged as a solution.

- “Single SKU” – meaning hardware and software have been pre-engineered, tested, configured, packaged and delivered as a single block of infrastructure with very little or no flexibility with respect to choice of server architecture, storage arrays, hypervisor, and management software.

Note: We included reference architectures from Web giants (e.g. Google, Facebook, etc), telcos, SIs, and large customer “roll your own” ref archs.

Market Assessment

TAM will reach $402B by 2017.

We’re defining the TAM as data center infrastructure that includes hardware (servers, storage and networking), infrastructure software (e.g. systems management, backup, etc.) and related services (including internal staff). Here’s the breakdown of the TAM.

Table 1 shows the TAM for converged infrastructure is enormous and essentially comprises the entire server, storage, and network market as well as associated management software and drag along services. The table shows:

- The TAM,

- Two hardware drilldowns of the TAM – one showing legacy versus single SKU versus reference architecture; the other showing the hardware breakdown into storage, server, and networking.

- Separate line items for infrastructure software and services that when combined with the hardware line item sum to the CI TAM in total.

- A storage drilldown.

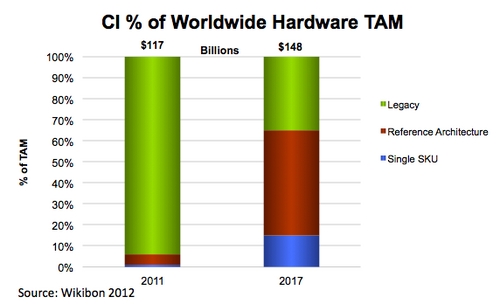

The biggest change in this space has come in the form of single SKU solutions that have software and hardware components that are engineered together. The two most prominent examples are Oracle’s Exadata (including Exalytics and Exalogic) and VCE’s Vblock. Cisco’s decision to start selling servers with its UCS system and Oracle’s acquisition of Sun completely changed the landscape. HP countered by acquiring 3Com and IBM subsequently acquired BNT. Simultaneously Dell has been aggressively acquiring storage and networking companies to increase its IP portfolio.

These moves have set up the large players to offer single SKU solutions, and others are competing here also. For example, HP offers a single SKU solution called VirtualSystem and Avnet sells a single SKU FlexPod. IBM, HDS, and Dell also sell single SKU solutions. Here’s a blog from Wikibon describing these systems in more detail.

The dramatic shift in landscape is shown in Figure 1, with legacy roll-your-own, purpose-built infrastructure declining rapidly and becoming too expensive for all but the most demanding and mission critical applications or those that are simply too risky to alter. We are in a “land grab” window where the major disruptors like Oracle and VCE are targeting the legacy bases of HP and IBM, while those two giants use their vast portfolios and services organizations to compete.

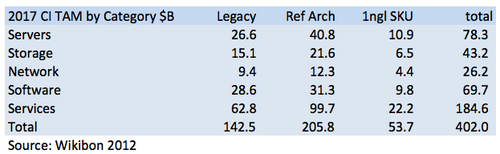

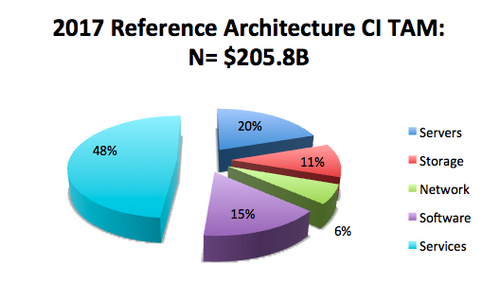

As seen in Table 2, while single SKU solutions have created much buzz in the market, the largest opportunity remains with reference architectures, capturing $205.8B or more than half of the TAM. Single SKU solutions offer very little or no choice in terms of technology options. VCE’s Vblock, for example, is limited to VMware as its hypervisor. Oracle’s Exadata is virtually all-Oracle technology with very little flexibility from a technology choice standpoint. The advantage is like an iPhone – it’s all integrated. The disadvantage is that single SKU solutions offer little or no choice for shops that want heterogeneity.

Increasingly, customers and the channel are looking for options and choice, and so-called reference architectures, which are proven and tested in the lab and often in the field, are becoming a popular option with the channel and many end-customers who may specify their own reference architectures internally. Certainly this is the case with Web giants such as Google and Facebook, but increasingly large commercial customers are creating their own reference architectures, working with primary suppliers. Figure 2 shows the segments of the Reference Architecture opportunity.

The Services Angle

Figure 3 underscores that services remains the largest market, despite the simplification trend of converged infrastructure.

Last year, SiliconAngle launched ServicesAngle, an online publication dedicated to IT’s largest market. Services is a market in flux, as the new cloud services players are disrupting the traditional businesses of IBM, HP, CSC, and Accenture. Companies like Dell have made acquisitions (e.g. Perot Systems) to get in the game, and EMC Global Services has been quietly expanding beyond support into consulting and training/education.

Services remain a huge market and its relationship to converged infrastructure and the services implications is significant. As indicated earlier, the CI land-grab means drag-along services for those suppliers and their partners that can establish a footprint. From a channel perspective, this opens new opportunities for consulting, design, implementation, and management services, especially related to private and hybrid cloud deployments.

Action Item: Converged infrastructure is coming to a private cloud deployment near you. Practitioners must trade-off the simplicity of a single SKU with the flexibility and choice brought forth by reference architectures. All converged solutions will generally bring some degree of lock-in, which will vary by the degree of flexibility built into the solution. At the same time the greater the integration, the greater the value in terms of speed to deployment, simplicity of management, and reduced risk. Also, the greater the degree of integration, the higher the CAPEX hit. However, operationally, greater integration means more simplicity and less TCO over the long haul. Whatever the choice, customers must recognize that purpose-built architectures will increasingly be confined to those applications that can absolutely justify the greater costs.

Footnotes: See Wikibon Primer on Converged Infrastructure for review of many of the products in this space.