Assessing the COVID-19 IT Spending Impact

In this week’s Breaking Analysis we’re changing the format a bit in an effort to get current information into your hands as soon as possible. Last week, we reported ETR results from over 1,000 CIOs and IT practitioners, and made a call that surprisingly, a large number of respondents – about 40% – indicated they didn’t expect a change in their 2020 IT spending. At the same time about 20% of the survey said they’re going to spend more in 2020, largely related to work from home (WFH) infrastructure.

Recap: Last Week, Budgets Flat – Now Calling for Slight Negative in 2020

ETR was the first to report this offset from WFH. Notably, the spending wasn’t just collaboration tools and video conferencing software. It was infrastructure around that including security, network bandwidth, desktop virtualization and other types of infrastructure to help workers increase productivity.

ETR made the call at that time that it looked like budgets were going to be flat for 2020. You also might recall consensus estimates for 2020 came into the year at about 4%, slightly ahead of GDP.

Obviously, that’s all that has changed. Last week, ETR took the forecast down to flat spending for 2020 and now this week we’ve gone slightly negative for the year.

Outlook Changes as Sentiment Turns Negative by the Day

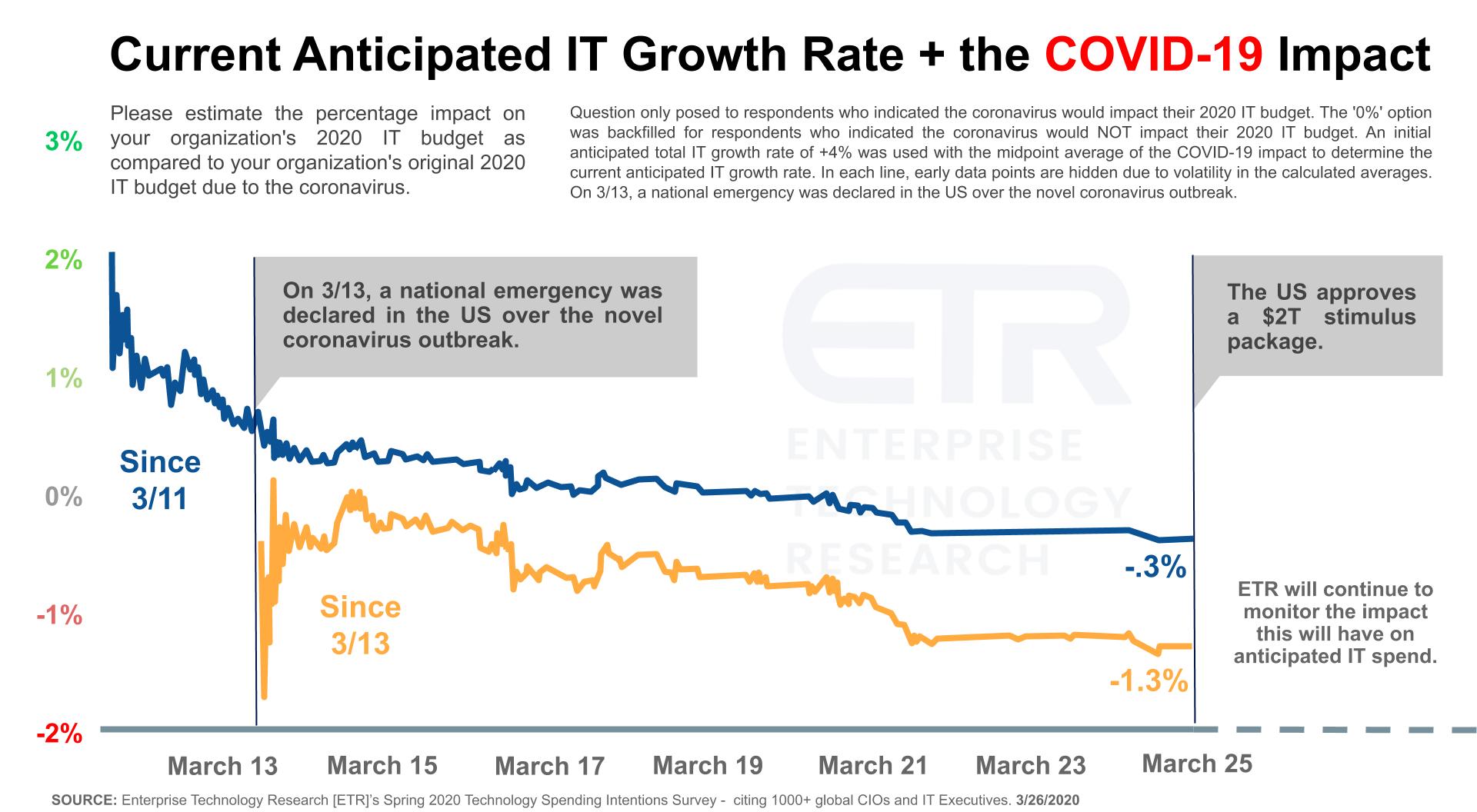

As we reported last week, the ETR surveys have run through the bulk of March. More than 1,000 CIOs and IT buyers had weighed in at that time and the number is now approaching an N of 1,300. We will keep you updated on new survey results as we assess the COVID-19 IT spending impact.

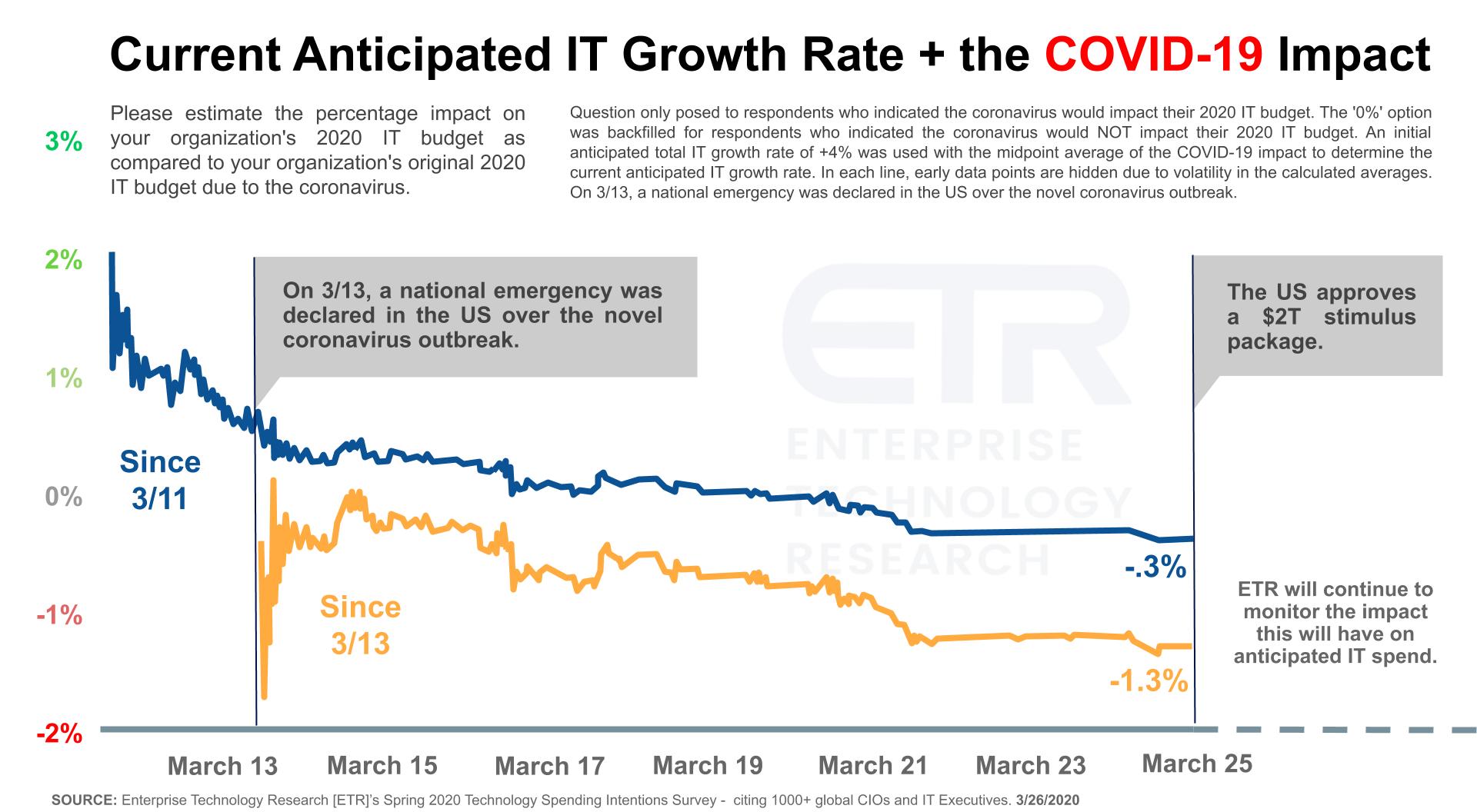

The chart above shows the change in CIOs response over time to question as to how COVID-19 will likely impact their spending in 2020. As you can see, sentiment dropped steadily after the declaration of a national emergence in the U.S (blue line). The yellow line adjusts the data and calibrates to isolate on those responses after 3/13.

We brought in Sagar Kadakia, ETR’s Director of Research to explain this dynamic further and assess theCOVID-19 IT spending impact. Here’s what he told us:

The last time we spoke, we were around an N or sample size of about 1000. And we were right around that zero percent growth rate. One of the unique things that we’ve done is we’ve left this survey open. So what that allows us to do is really track the impact on annual IT growth, essentially daily. As things have progressed, as you look at that blue line, you can really see the growth rate has continued to trend downwards. And as of just a day or two ago, we’re now below zero. And so I think because of what’s occurring right now, the overall current climate continues to slightly deteriorate.

Adjusting for Event Analysis

You can see on 3/13, a national emergency was declared and that’s really when the blue line started to decline. By resetting the data on the yellow line, and accounting only for those responses after the event, we can get a better picture of what’s actually happening in the market.

The next event we’re tracking is the sentiment after the passage of the aid package that should be approved by the House of Representatives today. This will help us further assess the COVID-19 IT spending impact.

Kadakia further explained the ETR methodology:

If you look at that yellow line again, effectively what you’re seeing is, we remove the first six or seven hundred respondents that took the survey prior to 3/13 when the US declared a national emergency. We can recalculate the growth rate. And we can see it’s around… It’s almost down 1.5%. So the beauty of doing this, really polling daily, is it allows us to be just as dynamic, as many of the organizations we survey. Remember, many CIOs report that these budget changes are going to be temporary. Organizations are figuring out what they’re doing day by day. And a lot of that is dictated based on government actions. And so uniquely here, what we’re able to do is kind of give people a range and also say, “based on these events, this is how things are changing”

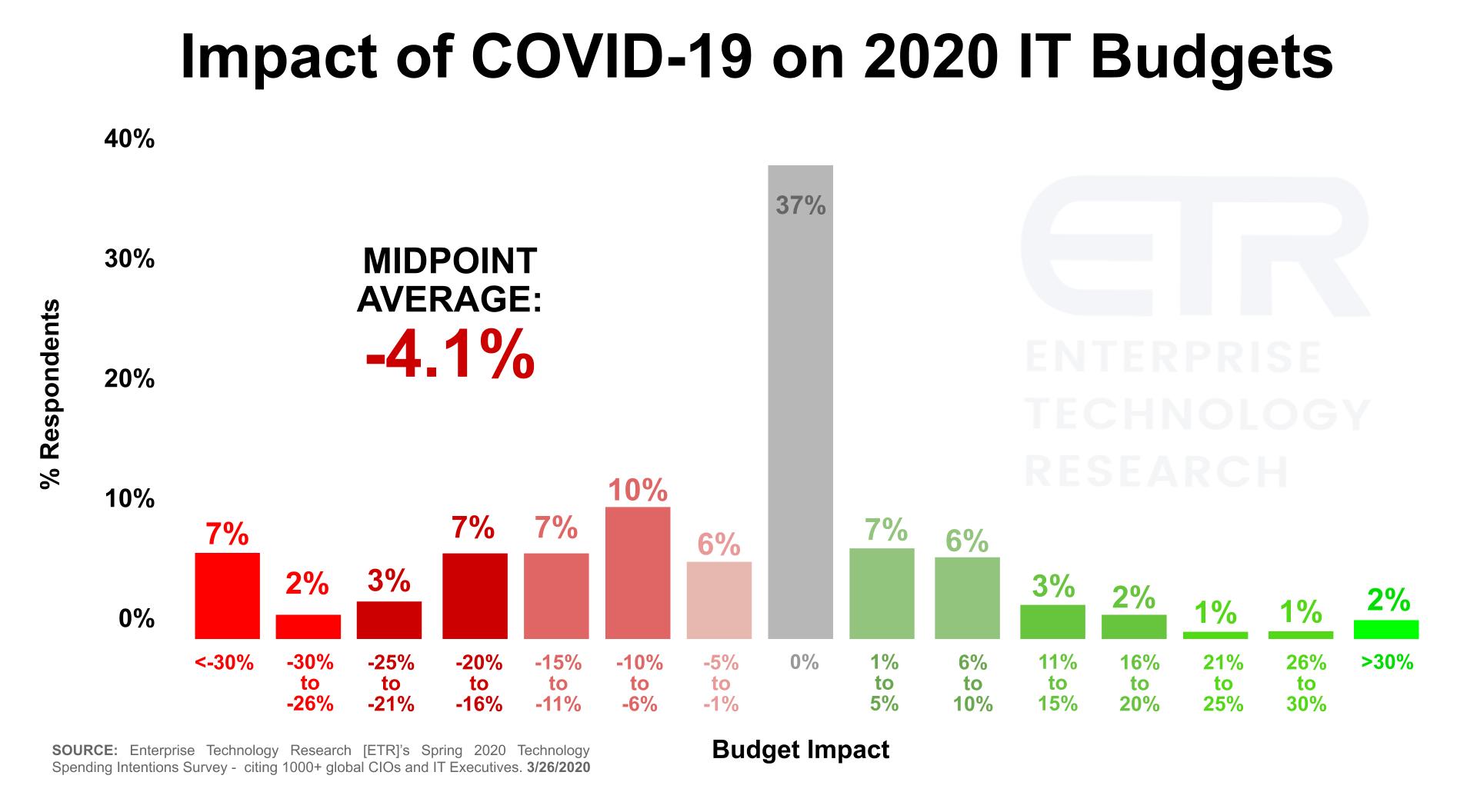

The Magnitude of Budget Changes Varies Widely

Let’s dig into the data a bit more and look at the range of expectations for 2020 IT spending.

The chart above shows the latest data from the ETR survey. Last week, the gray line (no change) was at 40% so now down slightly. A full 22% of respondents expect increased spending which is up slightly from last week. Most of the increases are in the lower range – 1-10% whereas the left side is more pronounced and negative– i.e. those expecting declines and the degree of reduction.

To summarize the key points:

- The mode response in the survey was no change; however the majority of buyers (42%) expect a decline in 2020 spending

- A full 22% of respondents expect an increase in spend for 2020

- This somewhat surprising statistic is directly a result of organizations trying to keep employees productive.

- The WFH offset not only includes video conferencing tools but also laptops, mobile device management, security, VPNs, network bandwidth, desktop virtualization and other related infrastructure.

Industries Supply Chains will Likely Worsen– Retail, Industrials, Pharma & Healthcare

According to Kadakia, ETR’s research shows that healthcare, pharma, industry materials, manufacturing and retail organizations indicate the highest levels of broken supply chains today. The expectation is that three months from now, it’s actually going to worsen.

As we discussed last week, we don’t expect a V-shaped recovery. Things are not likely to improve in the next few weeks or even the next month or two. CIOs are indicating that they expect conditions to worsen in the supply chain side and on the demand side, the industries getting hit the hardest are retail, consumer, airline and certain delivery services. These sectors also expect demand to worsen in the near term.

Some additional thoughts on industry change:

- We believe that the COVID-19 crisis will accelerate digital transformations. We’ve cited many times that much of the digital transformation narrative has been lip service as CEOs put forth a vision but line managers, facing pressure to meet today’s P&L targets, are not as aggressive.

- The learnings from COVID-19 will inform radical change in many organizations and the tech industry structure will shift from a cloud of remote services as the disruptive force, to sets of more ubiquitous digital services across premises, cloud and edge.

- Transformations in retail were already well underway. Despite the fact that still a minority of retail sales are transacted on-line, the transformation to digital will be more pronounced coming out of this crisis.

- Airlines could see consolidation depending on what actions governments take.

- Pharma has an opportunity to develop a vaccine for COVID-19, however there are tales of caution from previous epidemics. Many chased drugs to combat ebola, SARS, MERS, etc. and ended up failing.

Organizations are Prioritizing Productivity

One of the dynamics we discussed with Kadakia is that unlike other downturns (e.g. 2000 and 2008) a primary focus today is on maintaining productivity, rather than cutting costs. We’re not saying that companies aren’t being prudent with expenses – they are – but the crisis is bringing in forced cost reductions (e.g. travel bans and cancelled events). The companies that have survived and possess strong balance sheets are trying to maintain their employees and get the most from at home workers.

This creates a two-sided dynamic. ETR data shows that the big cloud providers are showing momentum. Semiconductor companies look to be surprising on the upside as Micron just reported yesterday citing strong demand in both cloud and data center. The point is CEOs have not capitulated to the crisis – at least thus far.

Companies Showing Strength

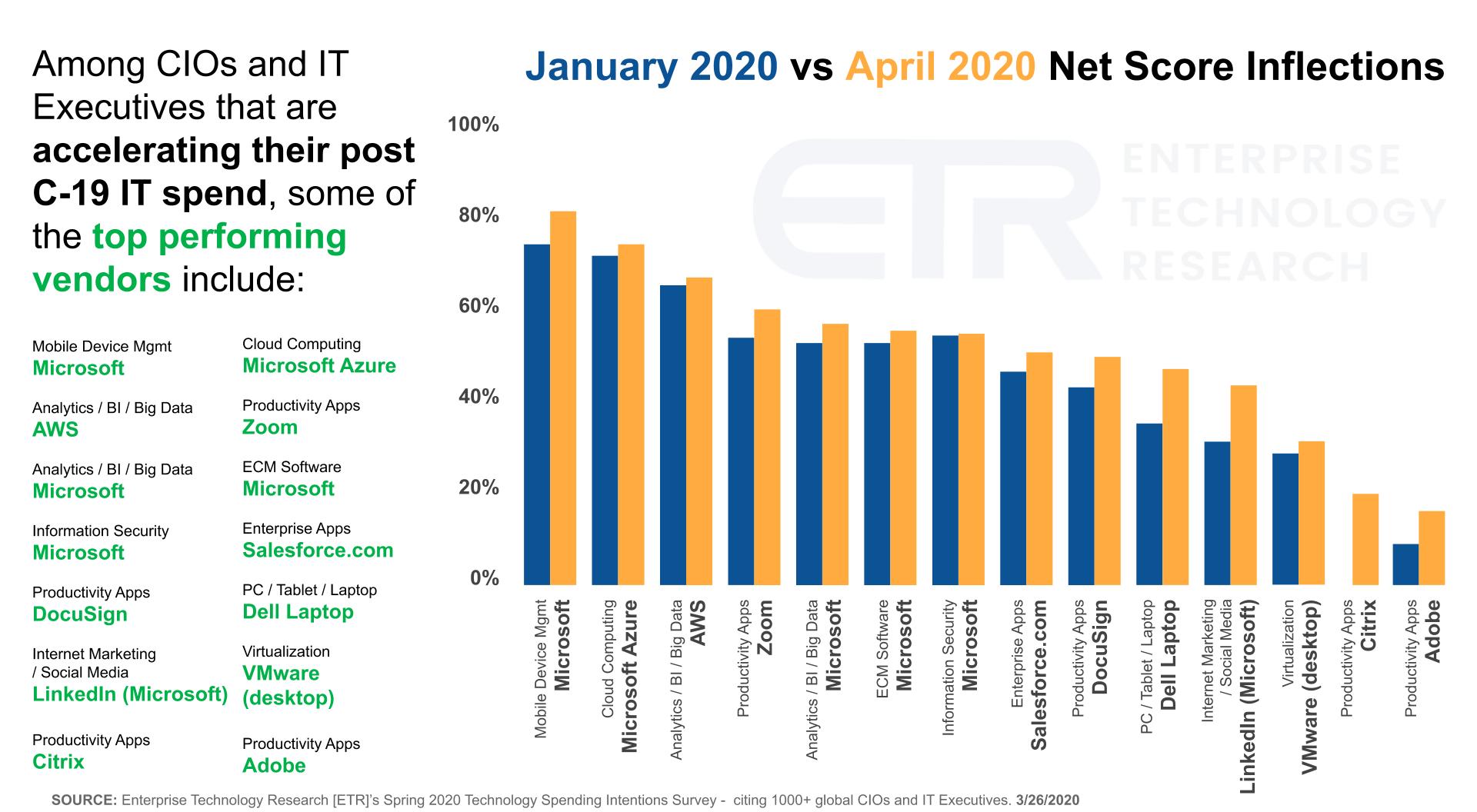

Let’s look at some of the vendor and sector data. Over the next several weeks we’ll be digging deeply into this and updating you regularly.

In the chart below we’re showing fourteen companies from the survey showing higher Net Scores in the April Survey relative to January. Remember, Net Score is a measure of spending momentum.

Not Just Video Conferencing Tools

Some of the sectors we’re calling out that have momentum right now include:

- Mobile device management (MDM).

- Collaboration tools.

- Big data, analytics & cloud – particularly the big three cloud players.

- Productivity from the likes of Docusign, Adobe, Zoom, Citrix & VMware.

- Security – showing Microsoft in this slide but we would expect some of the cyber leaders we’ve called out in the past like Crowdstrike, Okta, CyberArk and Forescout will continue to maintain some spending momentum on their products.

- Marketing – LinkedIn is showing strength as inside sales reps pound the network trawling for business.

WFH infrastructures are getting more spend for the vendors that are best positioned. Kadakia explained the above chart:

What you’re looking at here is isolated to all of those organizations and customers that indicated that they’re increasing their budgets because of COVID-19, specifically related to work from home infrastructure. And what we’re doing is then isolating vendors that are getting the most upticks in spend.

This actually really nicely aligns with a lot of the themes that we were talking about collaboration tools. You see that VMware, they’re all right on the virtualization side, MDM with Microsoft. And you’re seeing a lot of other vendors with Citrix and Zoom and Adobe. These are the ones that we think are going to benefit from this kind of Work From home infrastructure movement. And again, it’s all very… It’s not just the qualitative and the commentary. This is all analytics, we really went in and analyzed every single one of these organizations that were increasing their budgets and tried to pinpoint using different data analysis techniques, and to see which vendors were really getting the majority or the largest, pie of that spend.

Will Legacy Infrastructure Players get a Reprieve?

Recently we interviewed Sanjay Poonen, COO of VMware. He was cautious in two respects: 1) he did not want VMware to appear to be “chasing the ambulance;” and 2) he was notably sanguine about VMware’s future prospects but sensibly careful about being too optimistic in the near term. Nonetheless, VMware’s desktop virtualization and security business should be well-positioned.

[Note: Like many other major tech players, VMware has suspended forward earnings guidance].

Similarly, Michael Dell was recently quoted in CRN discussing Dell’s supply chain and in particular its ability to meet laptop demand as WFH needs surge. However the on-prem businesses for both VMware and Dell are likely to come under pressure in the near term.

This trend is not isolated to Dell. Cisco is another example of a company that will likely see bifurcated demand – i.e. a tailwind for WFH from Webex and Meraki with headwinds for on-prem,

As we’ve pointed out previously, in the past two years, organizations have experimented with digital transformations and are beginning to double down and operationalize these initiatives. As such they’ve done two things:

- Narrowed spending on emerging tech vendors by reducing experiments

- Begun to unplug those legacy systems they were running in parallel as a hedge

As we’ve also discussed, the cloud has continued its steady march, eating into on-premises infrastructure and software companies’ momentum. While the on-prem giants all have cloud plays, some are better positioned than others. For example, while we like Palo Alto Networks’ long-term prospects, the company has struggled with its cloud execution.

Others like NetApp have embraced the cloud but they’re exposure to legacy on-prem declines is substantial. Teradata similarly is being hit by cloud native analytic database growth from the likes of Snowflake and AWS RedShift.

IBM’s large services business as well as Oracle’s large on-prem software estate are exposed. The flip side is both companies have a cloud play and while not as competitive in IaaS with AWS, Azure and Google, their respective SaaS businesses somewhat insulate them from earnings disasters.

Symantec, Check Point Software, MicrosStrategy are others that ETR surveys show are currently exposed.

As Kadakia said:

There’s no reprieve for these legacy names and we don’t anticipate them getting additional spend from the WFH infrastructure movement.

The key point here is that in difficult times, people will often revert to the “safe bet” and that can benefit legacy names. But it’s very possible that dynamic won’t fully play out this time.

The bottom line is this is a “tale of two cities” — it’s not an across the board down or up scenario. You have to dig into the data by vendor by segment by vertical to really get a full picture.

What’s Next?

Our next goal with ETR is to determine whether or not the stimulus/aid package is having an impact on how people are responding. As well, we want to continue to track sentiment based on Coronavirus news as it relates to how they’re changing their budgets.

Kadakia told us that he’s watching, over the next four or five days, for an uptick in the lines here. Organizations are wrapping their heads around the federal government’s actions. While there is a roadmap in place to help us get out of this, if the news gets worse – which is likely, the lines will continue to come down.

The combination of actions by the Fed, who continue to have a number of arrows in their quiver and the U.S. federal government are key to understanding theCOVID-19 IT spending impact. However other central banks, especially in Europe, may not have as much flexibility. The market shook off the 3+ million jobless number yesterday but the impact of that carnage will likely be reflected in the market over the coming months.

The market is still functioning poorly. Despite the actions in monetary and fiscal policy, oil prices as we mentioned last week, are a big a concern. Jobless claims of 3+ million are believed to be as high as 5+ million based on analysis of Google searches by two prominent economists. What’s even more concerning is the shocking forecast that experts estimate we could lose 14 million jobs by this summer.

We’re on it

As we’ve said, it’s an uncertain and dynamic picture, so we’ll continue to forecast as accurately as possible and we’ll forecast often.

We told you last week, theCUBE skeleton crews are in the studio and we’re keeping the content flowing. Most on our team are working from home but are still on the grid. Currently, our Palo Alto studio is fully operational for four days each week capturing remote guests on camera and tying into our Boston studio operation. So get in touch if you need anything – we are here to help.

You have our commitment that theCUBE and ETR will keep you up to date on theCOVID-19 IT spending impact. ETR survey data keeps rolling in – you can get updates on their Web site as ETR is on this trend more than any other data firm we know.

Remember, these episodes are all available as podcasts wherever you listen. Ways to get in touch: Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our linkedin posts.

You may want to check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Wishing good health and safety for you and your families.

Watch the full video analysis: