Contributing Analysts

Dave Vellante

David Floyer

Stu Miniman

Dr. Ralph Finos

Premise: Cloud Computing is the 3rd major wave of change that is impacting the IT industry, with the impacts expected to be at least an order of magnitude larger than the Client-Server era. Wikibon looks at the leading factors that will define, influence, shape, and disrupt the Cloud Computing industry for the next decade.

It’s been over 15 years since Google began using commodity hardware and distributed applications to build the world’s largest service provider infrastructure. It’s also been over 15 years since Salesforce, NetSuite and WebEx created the SaaS industry and began renting business software to customers over the Internet. While many elements of cloud computing are now often taken for granted, the foundational elements have been in place for more than a decade. But as the pace of business changes and global pressures are shifting the competitive landscape, the broader IT industry is now attempting to harness the power of Cloud Computing as it moves into it’s second decade.

Wikibon Research – Cloud Computing (2015-2025) – PDF (full slides)

Wikibon has been covering Cloud Computing since the 2000’s, but tectonic shifts are happening which will likely change the industry in ways that will not only impact leading IT vendors and their partners, and ultimately will create new business models for end-user customers.

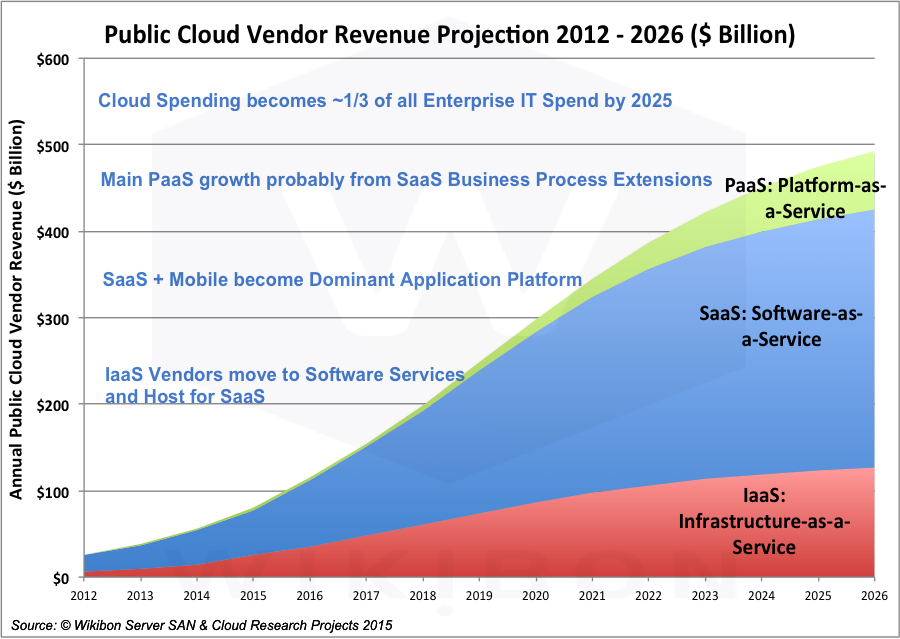

While there is still much research to be done and revenue trends to be modeled, Wikibon has already begun making revenue forecasts for the next decade. Wikibon expects that at least one-third (33%) of all IT spending will move to the public cloud by 2026, with all three Cloud Computing areas having significant growth.

This trend of moving larger portions of IT budgets towards public Cloud Computing is already beginning to have a significant impact on the IT vendor marketplace. Within the last 12-24 months the market has seen significant mergers, established companies leaving certain market segments, and new challengers begin to rapidly grow their market share. These changes are forcing business to not only re-evaluate their vendor/sourcing relationships, but also begin to think more strategically about how these IT trends will impact the stability of their business.

The Impact of Software

At the core of this transformation is software. While software has obviously been a part of IT since the 1950s, the dynamics of software have radically changed over the past decade, which is creating the new foundation for much of how IT will exist moving forward. As Marc Andreessen (co-founder at Netscape; VC at Andreessen/Horowitz) famously said in 2011, “Software is eating the world.” The impact of that statement has been far-reaching, as the advances in software have impacted nearly every aspect of our personal and business lives, as well as every global industry.

Software has shifted from driving business productivity with applications like ERP, CRM and Collaboration to driving completely new business models that are changing and disrupting almost every industry around the world. The footprint of many companies has shifted from large factories to physical storefronts to digital websites, and now it may only be a mobile application. While companies such at Tesla, Netflix, Uber and AirBnB have captured many of the recent headlines, incumbent business of every size are also trying to become more digital and more agile through new usages of software. They are evolving from running their business on Systems of Record to building greater market insight through Systems of Intelligence. Social engagement and real-time data analysis, created through Systems of Engagement, are also priority areas for businesses attempting to shift their focus of value-creation.

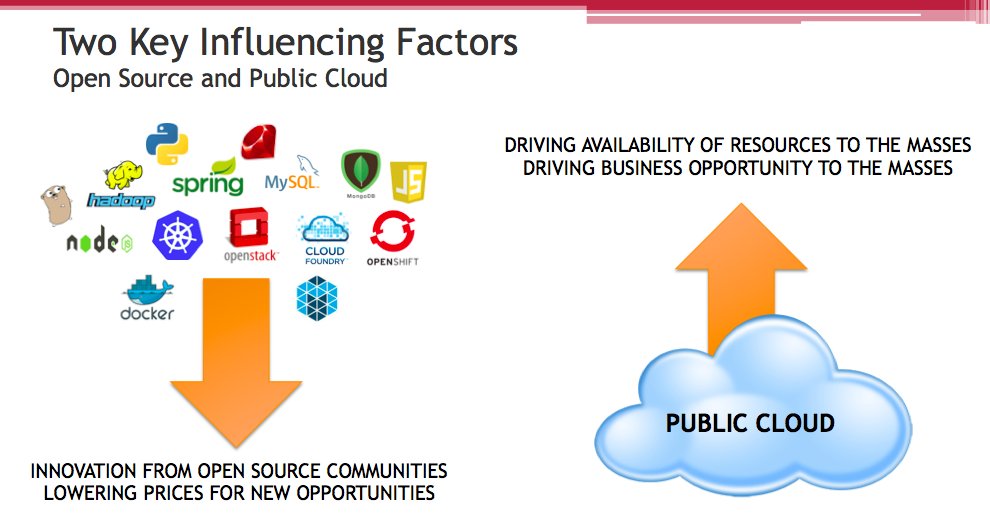

At the core of these recent software revolution are two key attributes – Open Source Software and the availability of Public Cloud resources. While not every company utilizes these resources today, their impact is far-reaching on the IT industry.

Open Source Software and the communities (e.g. Apache Foundation, Linux Foundation) that form around new ideas are playing a significant role in where innovation is shifting. While large IT vendors still have massive R&D budgets to build commercial software, the leading edge implementations are increasingly coming from open source communities. In many cases, large IT vendors are beginning to actively contribute engineering resources and software to these projects in efforts to either grow existing or emerging markets, or use open source as a competitive weapon vs. competition in the marketplace. Many of the largest contributors to popular Cloud Computing projects (e.g. Linux, Open vSwitch, OpenStack, Cloud Foundry, Openshift, etc.) are large commercial vendors with dedicated staffing.

Nearly all of the leading public Cloud Computing companies leverage open source software to deliver the majority of their services to the market. This software allows them to minimize or avoid licensing costs, which helps them deliver their services at much lower prices and at much larger scale. In addition, the learnings of the open source community are integrated within these projects, helping multiple web scale providers to solve challenges that didn’t exist before the pre-2000s growth of the Internet.

As mentioned before, commercial software and on-premises IT are still the dominant portion of IT spending in Mid-market, Enterprise and Government segments. But Wikibon is increasingly hearing from our community members that they are exploring open source alternatives and developing the skills and process to expand their IT domain to leverage public cloud resources to solve business challenges. While these transitions often take 5-10 years to occur, due to legacy application portfolios, process and skills; there is a clear understanding from these businesses that the pace of change going forward will have to be much faster than in the past if they wish to remain competitive in their given market segment.

The Increasing Pace of Change in Technology

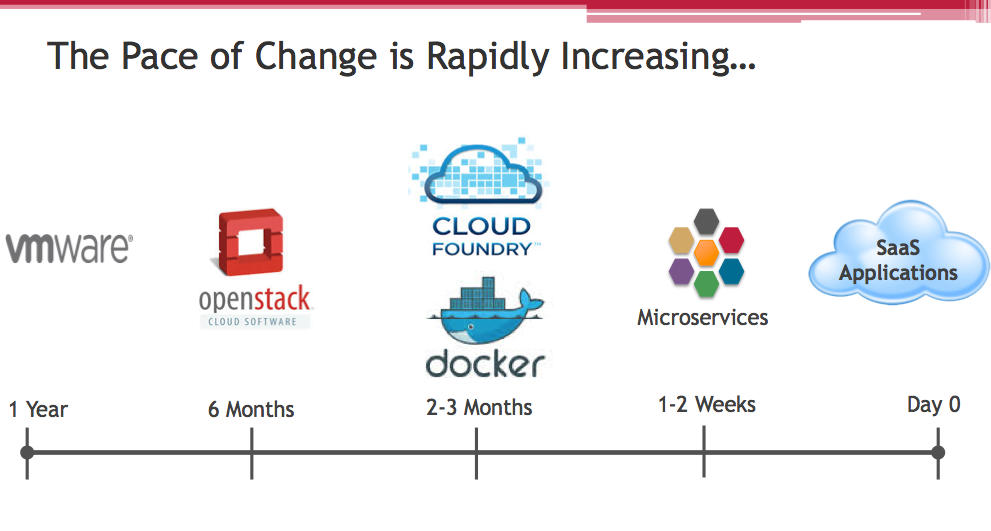

As Wikibon observes the trends around Cloud Computing, some trajectories and timelines are still somewhat uncertain. We understand that change in non-greenfield environments is traditionally slow and complicated, due to existing applications and data. But one thing that is very clear is that the pace of innovation and change is rapidly increasing. Figure 5 attempts to showcase this by showing the pace of updates from several major technologies, development and consumption models.

This pace of innovation is not only inspiring, but it also creates significant levels of confusion and stress for IT organizations trying to balance near-term and long-term strategies. Which areas have the potential to create significant improvements for the business and which ones are little more than hype? The confusion is amplified when IT organizations consider the new consumption models available (e.g. open-source, public cloud, managed private cloud, SaaS, PaaS, etc.). Each of these options present new budgeting models to consider, as well as integration and migration costs, security impacts and potential changes to sourcing and partnering models.

Business and Technology Perspectives

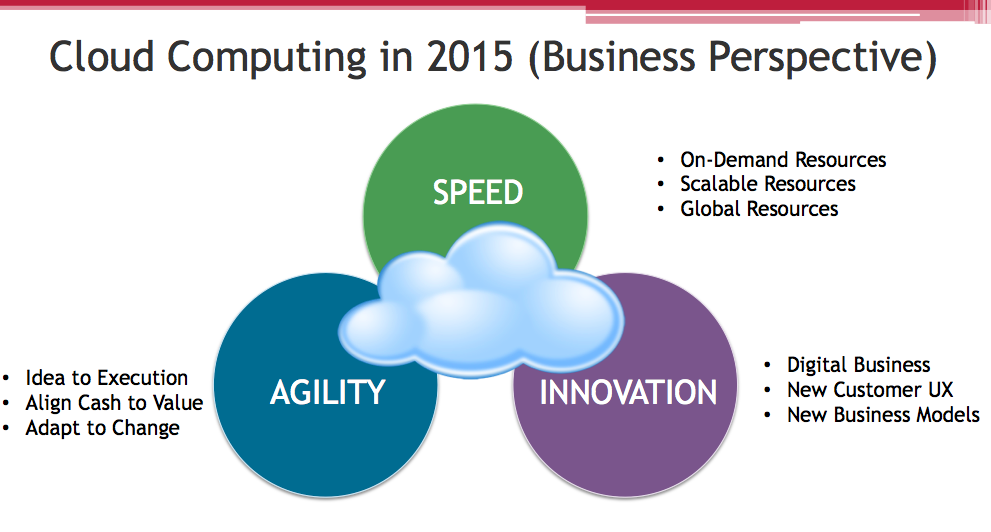

With Cloud Computing creating a macro-level shift in how IT delivers value to the business, it’s important to simultaneously look at it from both Business and Technology perspectives. With the increasing use of technology to create business differentiation, Wikibon believes that it is more critical than ever that Business leaders and Technology leaders be tightly aligned in how strategic planning is executed. In 2015 (and beyond), it is a rare occurrence for any business-led project to not be a technology-centric project. The ability to reduce the time between business idea and business execution will determine which companies are able to create and sustain business differentiation in a given market. The choice to focus on new business innovations vs. internal cost reduction has impacts on the necessary technology skills as well as the business’ ability to do strategic planning

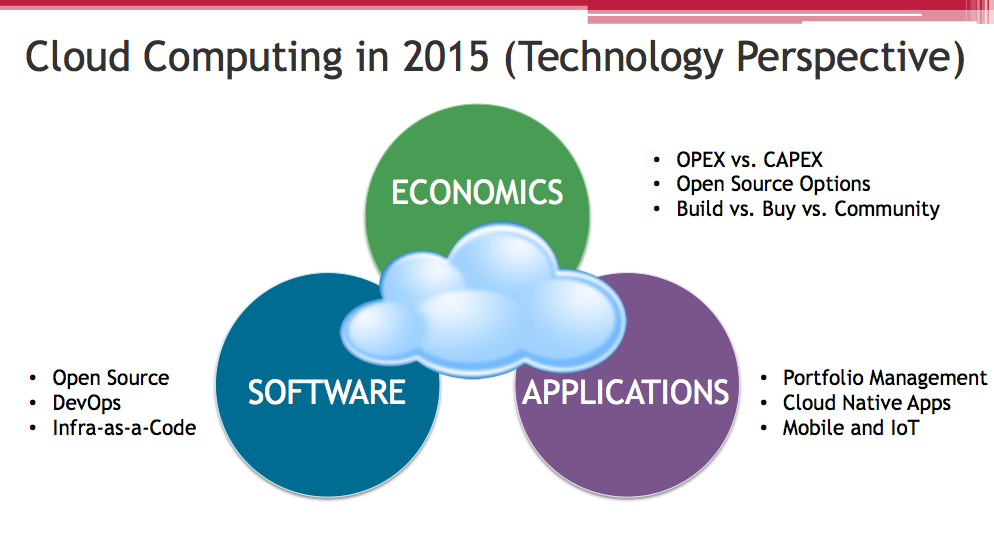

Speed of execution and the Economics of technology consumption are tightly coupled elements. The choice to place technology on-premises vs. a Public Cloud impacts not only the technical implementation, but the associated cash flows of the business. In a digital business world, business Innovation is increasingly being driven through the delivery of new Application which interact with the market in new ways (e.g. Mobile, Real-Time Analytics, Sensors, etc.). And business Agility is directly impacted by the lack of rigid constraints, hence why more IT focus is being shifted to increasing the velocity that they are able to deliver not just software, but the entire set of IT services to both internally and externally facing audiences.

The movement to more agile software delivery models, based on platforms that abstract away the underlying complexities of infrastructure, coupled with DevOps operational practices and cultures, will be the drivers for business differentiation over the next decade.

Managing the Breadth of Application Portfolios

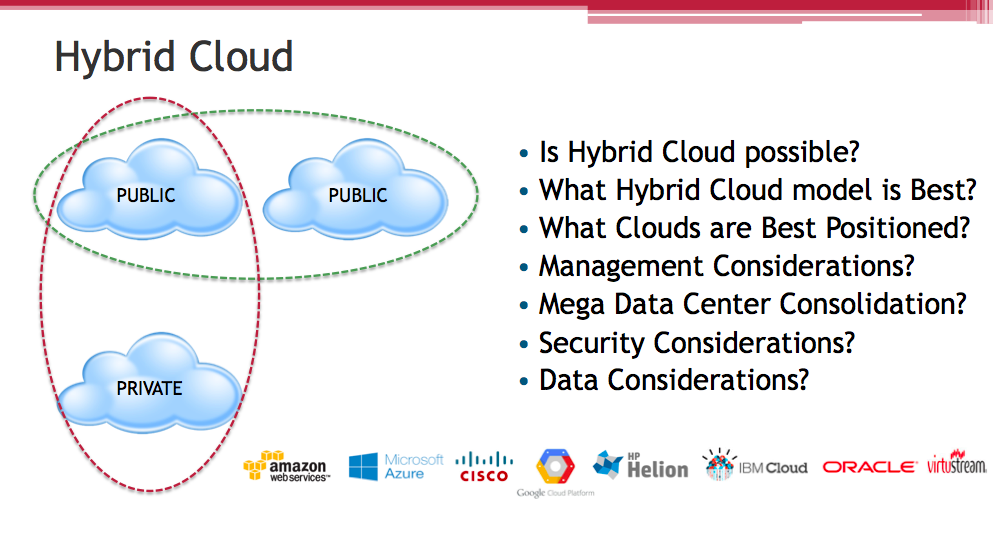

Over the past 3-4 years, CIOs have consistently ranked “Hybrid Cloud” as their #1 or #2 implementation priority. Wikibon has questioned the maturity of existing Hybrid Cloud offerings, but the reality of the Hybrid Cloud discussion is that the focus of this CIO priority is not on Clouds, but rather on Applications. Hybrid Cloud is an application portfolio discussion. The challenge facing CIOs is how to best manage their existing application portfolio. They must balance where to make investments; either maintaining and enhance existing applications or developing new applications to differentiate the business. This decision-making process must not only consider the prioritization within the portfolio, but must now consider new options about placement of applications (internal Data Center, Private Cloud or Public Cloud). These considerations all come with tradeoffs that impact budgeting, data management, application integrations and portability and existing skills and processes.

Wikibon’s Infrastructure practice is focused on the segment of the application portfolio which will remain unmodified, but will be optimized through virtualization and the shift to converged, hyper-converged infrastructure and engineered/converged systems. Wikibon’s Cloud practice is focused on the transformation of the portfolio that will move to a Private Cloud, Public Cloud or potentially be replaced with SaaS applications or new Cloud Native applications.

The first challenge for any CIO in application portfolio management is the massive, on-going investment required to maintain Systems of Record which support the core functions of the business. This is the 80% of IT budgets that rarely changes, and often limits new innovation from within IT. Over the past 12 months, more CEOs and CIOs are beginning to recognize that while these systems are critical, they are also not providing unique differentiation for the business. This has CIOs beginning to rationalize whether they can migrate these systems to Cloud platforms (costly; complex integrations) or they should consider alternative SaaS -based platforms. Due to the complexity of system-wide data integrations, large migrations are typically not successful or encouraged. An alternative approach is to look at ways that new Systems of Intelligence can be integrated with the critical legacy applications.

In this video, Alan Nance (VP of IT, Royal Philips) discusses the mandate from his CIO to radically change how they spend up to 90% of their IT budgets, moving them towards a models that drives more differentiation for their changing business landscape.

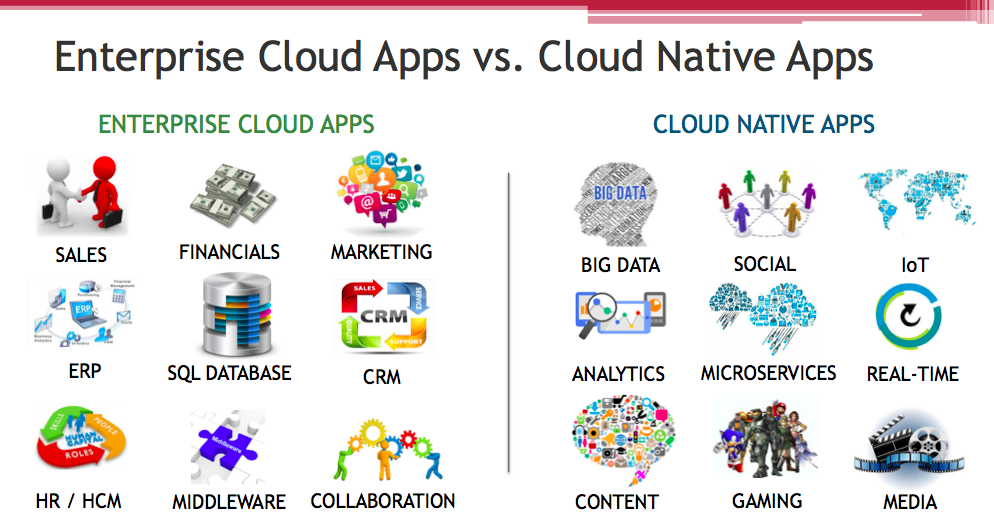

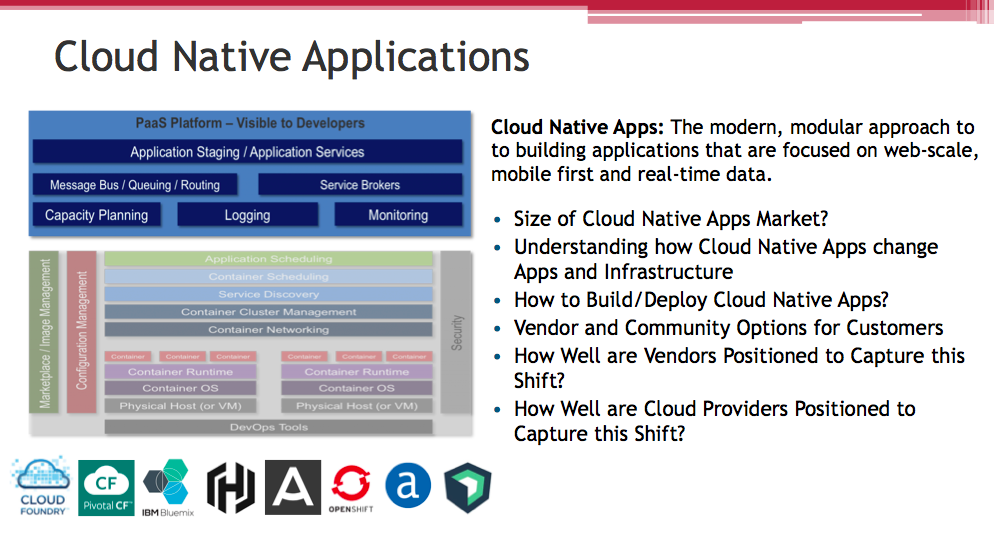

One approach to integrating the Systems of Intelligence is through modern Cloud Native applications and platforms. Whereas the Systems of Record would often focus on back-office systems, Systems of Intelligence are being placed closer to customers and community interactions. These systems allow the collection of data closer to the end-users (or the edge of a network; e.g. sensors) and allow data to be processed in batch or real-time. While these applications may not be transactional, they are shaping the end-user experience and allow the business to take actions on those inputs in a more timely manner, with greater levels of personalization.

These applications are also where businesses are focusing the bulk of their DevOps transformations. As these types of applications require frequent updates and modifications, they are ideal for Continuous Integration and Continuous Deployment (CI/CD) environments. They are also where the shift to microservices architectures are gaining traction, as modular components can be modified and reused as the end-user facing applications evolve.

Another option for CIOs is to explore the possibility of replacing non-differentiated systems with SaaS applications, especially ones that have been fully-depreciated or serve a lesser function than when they were originally deployed. In other cases, the SaaS applications offer similar Systems of Intelligence capabilities as Cloud Native applications, especially as they allow custom-integrations back to legacy systems, without the need to allocate costs to data centers or aspects of operations teams.

Barriers to Adoption

In laying out a Cloud Computing strategy that extends more than 18-24 months, it is important to remember that the pace of business adoption does not always match the pace of technology adoption. In most cases, it can be a laggard by 2-5 years, depending on geography or industry.

There are many real-world barriers that can either slow implementations or completely stop any progress. The models for all aspects of Figure 12 are well understood for today’s application portfolio, as they have evolved and adapted over the last 15-20 years. Modifying, adjusting or often breaking these known models is why many greenfield environments are often highlighted as examples of success in Cloud Computing. The opportunity for businesses over the next 5-10 years is to use business-centric rationale to once again influence these models to allow technology to improve business differentiation and value creation. This will not be an easy task, as the IT generation that built these frameworks is getting closer to the twilight of their careers and have become more risk-averse to change. As described in “The Innovator’s Dilemma“, today’s IT organizations face the challenge of disruption from systems that are deemed to have lesser functionality and address lesser problems than the systems that dominate the IT landscape today. Just as many IT vendors are struggling to create strategies that allow them to succeed in the Cloud Computing era without disrupting their Client-Server era franchises, many IT organizations must find the right balance between investments in Systems of Record and evolving Systems of Intelligence and Systems of Engagement.

Call to Action: There is no denying that the economic and innovation impacts of the Cloud Computing era are beginning to have an impact on both IT organizations and IT vendors. CIOs are no longer in a position to watch the chessboard evolve, but rather they need to actively drive a vision, strategy and execution models for their business to manage hybrid application portfolios and define their plans for Systems of Intelligence and Engagement. This evolution will be complex, so it is important to seek guidance from experts that have practice experience in reducing the learning curve of these transitions.