Co-Authors: Brian Gracely, Stuart Miniman

Premise: At some point in the lifecycle of every technology project, product or service, there comes a time when it has to re-evaluate how well it is aligned to the current demands of the marketplace. At the 2016 North American OpenStack Summit, the OpenStack community was going through a period of introspection, transformation and evolution. What started as a small community hoping to disrupt the largest public clouds and private clouds has evolved into a large community that is beginning to branch out in new directions.

Wikibon spent the week at OpenStack Summit speaking with the OpenStack Foundation, industry thought-leaders, leading vendors and many end-user customers about where they see the State of OpenStack in 2016 and beyond. The full set of discussions can be found here. From those discussions and many others with community members, Wikibon came away from the event with 5 key takeaways.

[Community] The OpenStack community of vendors has grown and consolidated in expected and healthy ways.

In many ways, the evolution of OpenStack has paralleled the evolution of the Linux market. At one point, there were nearly a dozen different vendor-specific OpenStack distributions trying to gain traction in a small market footprint. Likewise, there were 15+ Linux distributions back in the late 1990s and early 2000s. Just as Linux consolidated down to just a few main distributions (Red Hat, Canonical, SUSE), the OpenStack community has contracted the distributions through acquisitions or natural market-driven reductions (HPE Helion, Mirantis, Red Hat). In addition, the OpenStack Foundation has put programs in place to certify and validate interoperability between different OpenStack implementations. Not only does this consolidation bring together groups of OpenStack engineers, but it also forced some companies to rethink their go-to-market and revenues models.

VIDEO: Jonathan Bryce (@jbryce, OpenStack Foundation Executive Director) and Mark Collier (@sparkycollier, OpenStack Foundation COO) talk about the evolution of the OpenStack community and where it will evolve over the next few years.

[Operations / Consumption] Invisible OpenStack is the best OpenStack.

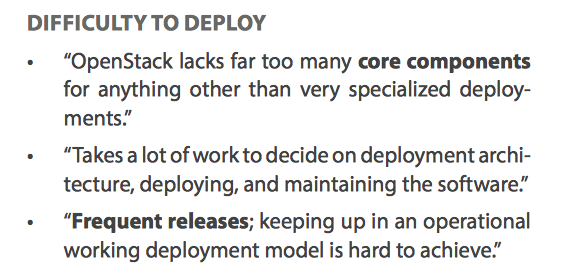

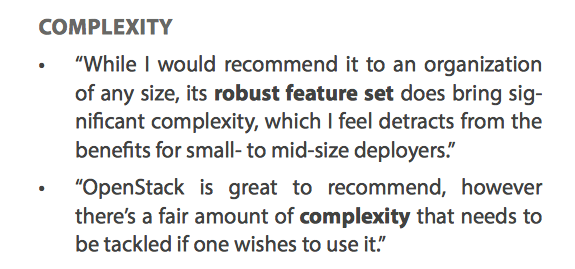

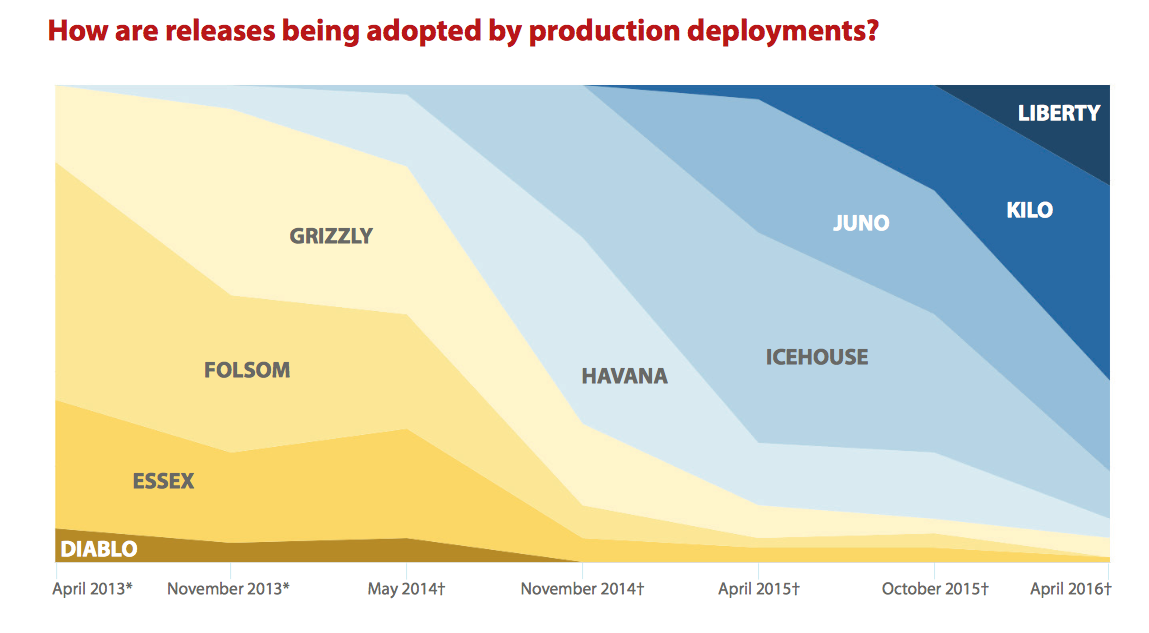

It’s no secret that part of the reason for OpenStack’s adoption rate has been end-user frustration with the complexities of operating an OpenStack environment. This has been openly discussed at previous OpenStack events and is highlighted in the OpenStack User Survey (April 2016).

The challenge of upgrading OpenStack from release to release was once again highlighted in the User Survey. Far too often, end-users say that they need to build a new environment with the latest release instead of upgrading the existing environment. This challenge has been a significant focus are of the OpenStack working-groups over the last two releases (Kilo, Mitaka) and user-feedback highlights that progress is being made.

Due to these challenges, new consumption models have emerged in the market that allow end-user customers to consume programmatic infrastructure (e.g. OpenStack) as a service. Offerings that deliver these capabilities include Cisco MetaPod, IBM Bluebox, Platform9, Rackspace and ZeroStack. These offerings allow customers to have physical resources that are either in their own data center or any remote data center (e.g. CoLo, Cloud provider) and the OpenStack services are centrally maintained and managed. In essence, the OpenStack portion of the service is invisible to the customer. This allows their IT organization or developers to remain focused on applications and projects they help drive revenue for the business.

VIDEO: Ajay Gulati (Founder/CEO of ZeroStack) talks about delivering OpenStack-as-a-Service to the market

[Revenues] Is there enough revenue to continue the momentum?

Regardless of the number of attendees at the event or the technical progress of the working groups, the topic of revenues always comes up at the OpenStack Summit. The reported earnings of AWS ($2.56B, Q1FY’16) and VMware ($1.59B, Q1FY’16) are always considered benchmarks for the OpenStack community. Both of those companies have been in business for 10 years or more. As with most open source software projects, it can be difficult to compare revenue because many early-adopter companies use the free version of the software rather than paying a support license, using professional services or consuming a paid service.

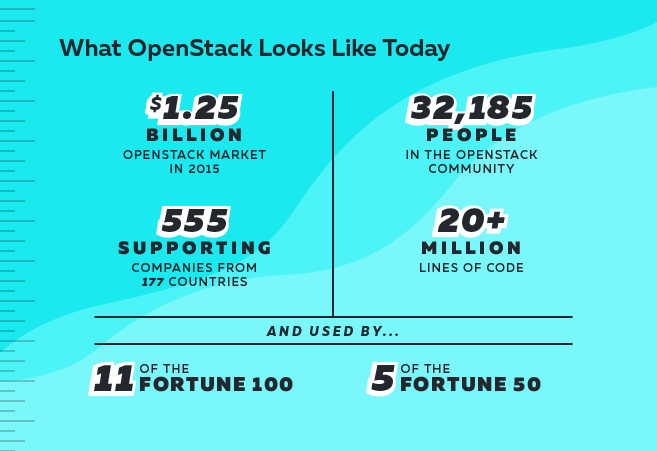

At this point in time, none of the major OpenStack vendors (Cisco, HPE, IBM, Mirantis, Red Hat) break out the individual revenues associated with their Red Hat business. The data (below) from Rackspace shows that the overall market is $1.25B, with some industry projections near $3-4B by 2018. Wikibon believes that the leading vendors are currently at or below a $100M/yr run-rate for OpenStack-related business (hardware, software, services).

Wikibon aligns OpenStack to our definition of True Private Cloud (On-Premises and Hosting), which we project to grow from $7B in 2015 to $201B in 2026 (36% CAGR), and be 31% of infrastructure spend. As the market demands more earnings transparency from public cloud providers, we also expect that OpenStack vendors will need to become more transparent about OpenStack-specific revenues if they want to maintain customer’s confidence in future of OpenStack.

[Use-Cases / Markets] NFV is emerging as a leading use-case.

The biggest surprise and most frequently discussed topic at OpenStack Summit 2016 was Network Functions Virtualized (NFV), an evolving networking architecture where edge-services (e.g. load-balancing, caching, proxying, firewall, IDS/IPS) are virtualized and run as software services on x86 servers instead of traditional networking equipment. This is an architectural movement that has been popularized by the largest telcos, as they prepare for even greater 5G data usage-models from mobile devices and IoT devices.

At the 2015 OpenStack Summit in Japan, NTT was named the SuperUser award winner. In 2016, AT&T was named the winner, with Verizon being named a finalist. The NFV use cases make sense for the telcos because they require the ability to orchestrate on-demand network-services as device usage continues to grow, and the OpenStack and OPNFV working groups may prove to be a path of lesser complexity to define new standards rather than going through existing standards-bodies. While the percentage of telco OpenStack users is considerably smaller than IT organizations, it is highly likely for this market-segment to generate as much or more revenues for OpenStack vendors in the next 3-5 years.

VIDEO: Chris Emmons (Director, Network Infrastructure Planning at Verizon) discusses their NFV rollout using OpenStack

[Technology Ecosystem] The OpenStack Foundation finally understands OpenStack’s role in a bigger Cloud Computing world.

For many years, OpenStack billed itself as “the OS for the Cloud”. Each new year brought out new projects and working groups (e.g. PaaS, Containers, Big Data, etc.), often expanding into areas well beyond the original Infrastructure-as-a-Service (IaaS) vision of OpenStack.

At the 2016 OpenStack Summit, the OpenStack foundation clearly highlighted that in order for OpenStack to be successful, it would need to work more closely with a series of other technologies. During the 2015 summits in Vancouver and Tokyo, container technology (e.g. Docker, runC) was one of the most in-demand technologies for learning and expanding the OpenStack footprint. In 2015 the focus was on having an option to run end-user applications in containers, instead of virtual machines being the only option.

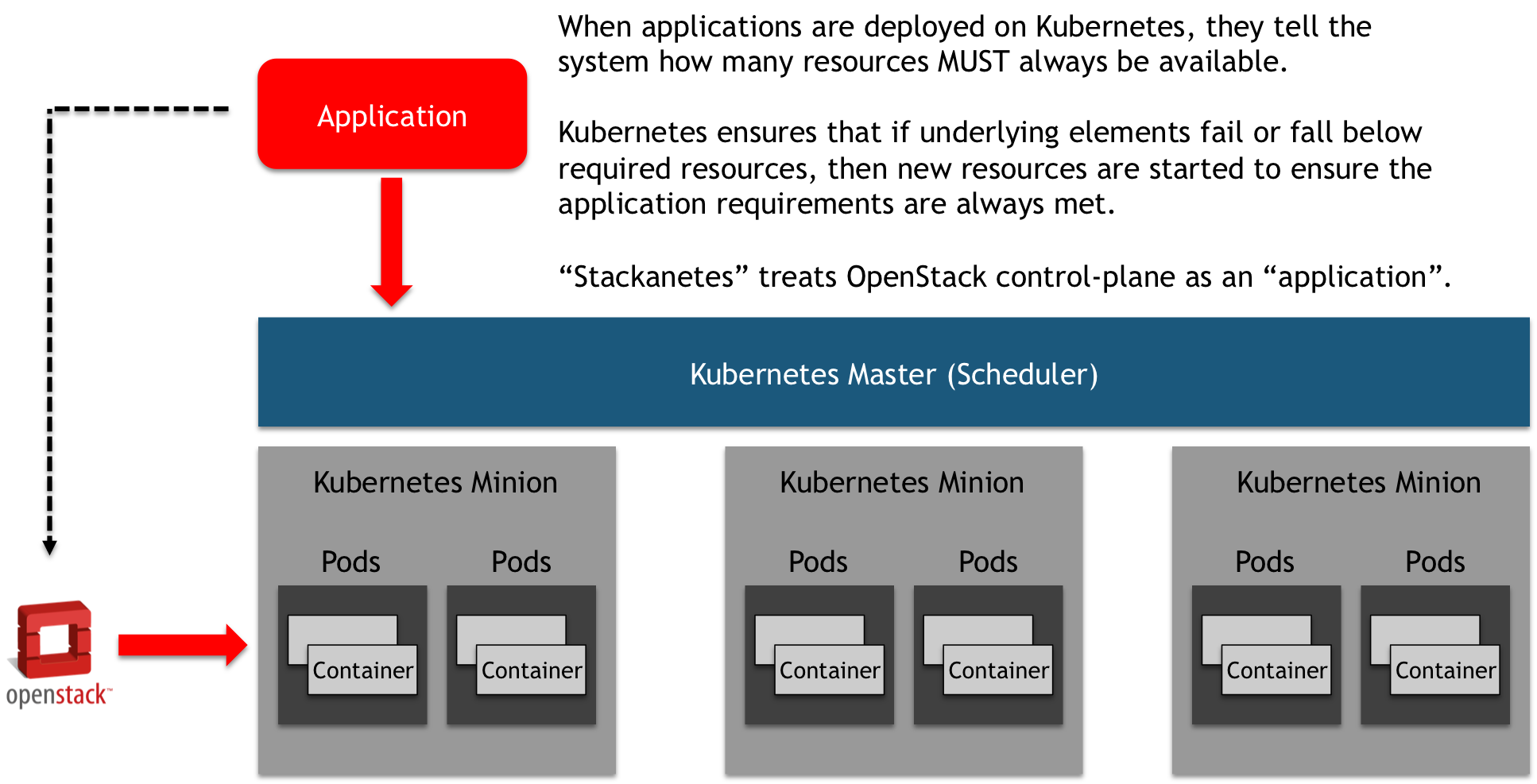

At the 2016 summit, a new concept was introduced – running OpenStack on containers. The example used at the summit was called “Stacknetes”, where the OpenStack control plane becomes an application that runs on top of containers that are scheduled and managed by Kubernetes.

The design thinking behind the Stackanetes project is that the OpenStack control-plane could benefit from the scalability and resiliency that Kubernetes provides. By having OpenStack appear to Kubernetes as an “application” rather than being a Cloud Management Platform (CMP), OpenStack can focus on managing localized services and resources, and Kubernetes can ensure that the OpenStack control-plane is highly available. This type of design thinking makes sense when companies like AT&T talk about rolling about 150+ global locations. It also makes sense to have OpenStack focus their engineering efforts on creating a stable, operator-friendly IaaS framework.

Action Item: As we stated in our OpenStack Summit wrapup videos (Day 1, Day 2, Day 3, Wikibon believes that the OpenStack community and technology has stabilized to the point where Private Cloud deployments are realistic for many customers. Customers should be exploring the breadth of consumption models which best align to their existing skill-sets and business goals, learning from some of the struggles of IT organizations in the past – e.g. building and operating OpenStack from trunk is extremely difficult.