Despite its faster growth in infrastructure-as-a-service relative to AWS and Azure, Google Cloud Platform remains a third wheel in the race for cloud dominance. Google begins its Cloud Next online event starting July 14th in a series of nine rolling sessions through early September. Ahead of that, we want to update you on our most current data on Google’s cloud business.

In this week’s Wikibon CUBE Insights, Powered by ETR we’ll review the current state of cloud and Google’s position in the market, updating you on our last report from May of this year. As always, we’ll drill into the ETR data and share fresh insights from our data partner and theCUBE community.

Google First in Cloud but Late to the Enterprise Party

Google was actually very early to the cloud game. Google’s 2004 IPO was a milestone event for the tech industry and in many ways marked the end of the post dot com malaise. It signaled the beginning of a new era of innovation and pre-dated AWS. During this time Google was busy building out its massive global cloud infrastructure, probably the largest cloud in the world with undersea cables, global data centers and tools like the Google File System and Bigtable. But it took many years for Google to pull its head out of its ad serving business long enough to recognize the huge opportunity to sell its Google Cloud Platform services to enterprises.

Bigtable, Google’s NoSQL database for example was released in 2005 but it wasn’t until 2015 that Google made this service available to its customers. That was the same year Google brought in VMware founder Diane Greene to begin its enterprise journey in earnest. Google has a dizzying array of services in compute, storage, database, networking, IT ops, dev tools, ML/AI, analytics, big data, security and on and on. Name a cloud category and Google has something.

But Google to this day still hasn’t figured out how to effectively sell to the enterprise. It really struggles to find the right formula. As you know, Google Cloud brought in Thomas Kurian from Oracle to shore up its enterprise game. Of course Kurian is going to lead with Google strengths like analytics and database. But it has to have differentiation so it comes up with different pricing models like sustained discounts which automatically apply discounts for heavy usage as opposed to forcing users to buy reserved instances such as AWS.

As well, Google Cloud is more aggressive with partnering around multi-cloud with Anthos and it smartly open sourced Kubernetes to minimize the importance of where workloads run physically.

All good, but the bottom line is that these moves are necessary for Google to compete because it lags behind the leaders. And it has a long way to go before it’s going to be satisfied with the progress of the Google Cloud.

The IaaS Market in Context

This is not to say it’s all gloom and doom for Google. Far from it.

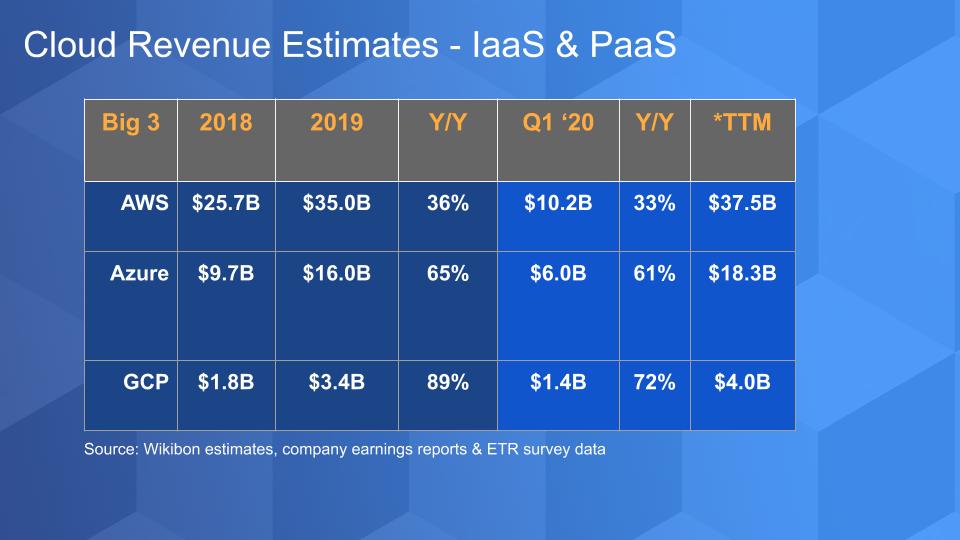

Earnings for Q2 will start rolling out later this month but the chart above shows our latest estimates of the Iaas and PaaS revenue for the big three cloud players. We have to caution you that only AWS reports clean numbers each quarter. We have to estimate Azure and Google Cloud Platform (GCP) revenue because they bundle in other services.

For example, Google reports its overall cloud numbers, which include G Suite. Microsoft reports a category called Intelligent Cloud, which includes public and private clouds, hybrid, SQL Server, Windows Server, Systems Center, GitHub, Enterprise support and consulting services. And Azure IaaS and PaaS is in that number too.

As such we have to squint through earnings reports and 10Ks to try and get to a clean IaaS and PaaS figure for these players and that’s what we show here. We want to stress a two points related to this data:

- First – on a trailing twelve month (TTM) basis – the big three cloud players now account for nearly $60B in IaaS and PaaS revenue. And this $60B on a weighted average basis is growing in the mid 40% range – so well on its way to being a $100B business just for these three firms. And as we’ve reported that momentum is eating directly into the on-premises infrastructure installed base which is a flat to declining market. That trend will play out in a big way this decade.

We predict that public cloud will outpace on-prem infrastructure by more than 1800 basis points over the next ten years.

- The second point relates to Google Cloud IaaS and PaaS growth. We peg it at greater than 70% based on public statements, reading 10Ks and ETR data, which we’ll discuss in a moment. So very healthy growth but from a much smaller base than AWS and Azure. But in our view it’s not enough. Because AWS and Azure are so large and strong growth wise, we feel Google will remain a distant third until it can much more effectively sell into the enterprise market.

Nonetheless, many companies would be thrilled to have a $4B cloud business and there’s certainly good news in the data for Google.

Customer Survey Data Shows Many Pockets of Strength

As we’ve reported, Google pushes G Suite hard as part of its cloud and often leads with G Suite in its messaging. But to us that’s never been compelling.

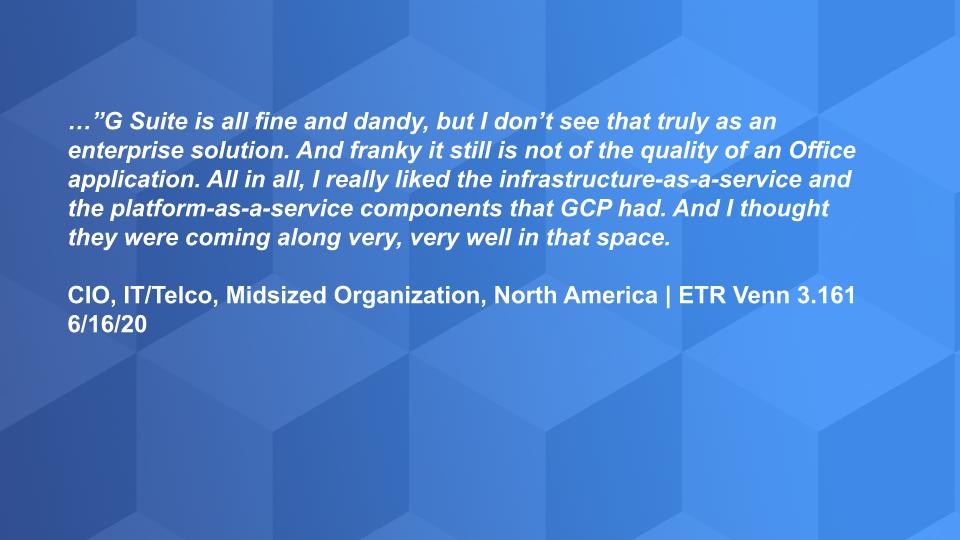

Let’s start with some anecdotal data from ETR. ETR runs a regular program called Venn in which it invites clients into a private session to listen to CIOs talk about their experiences with vendors and overall spending intentions.

We’ve had ETRs Erik Bradley on as a guest who directs the Venn program. The statement shown above from a recent session quoting a CIO at a mid-sized telco sums it up nicely.

…G Suite is all fine and dandy, but I don’t see that truly as an enterprise solution. And franky it still is not of the quality of an Office application. All in all, I really liked the infrastructure-as-a-service and the platform-as-a-service components that GCP had. And I thought they were coming along very, very well in that space.

The reason we share this is because the IT buyers we speak with are serious about exploring Google. They want options other than Azure and AWS and they see Google Cloud as having great tech.

Google Cloud Platform in the Enterprise

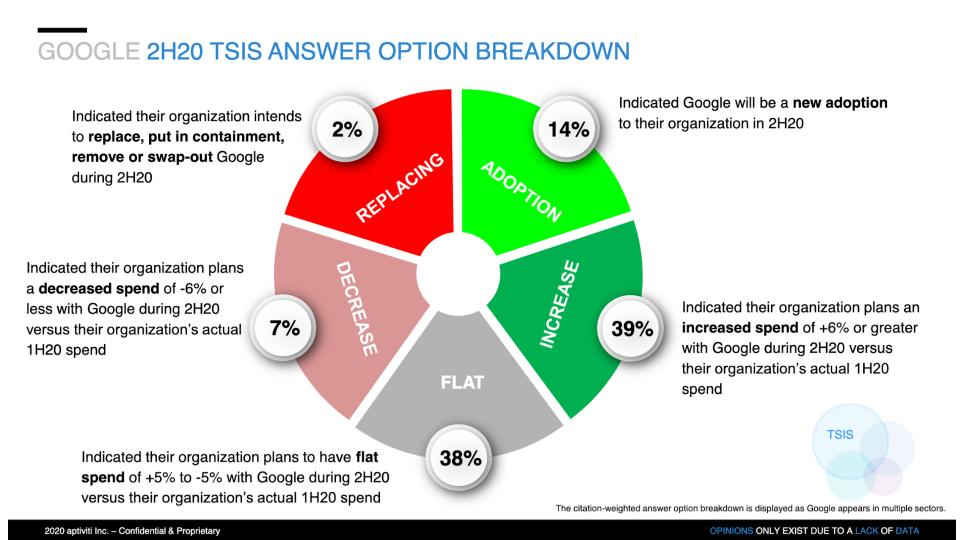

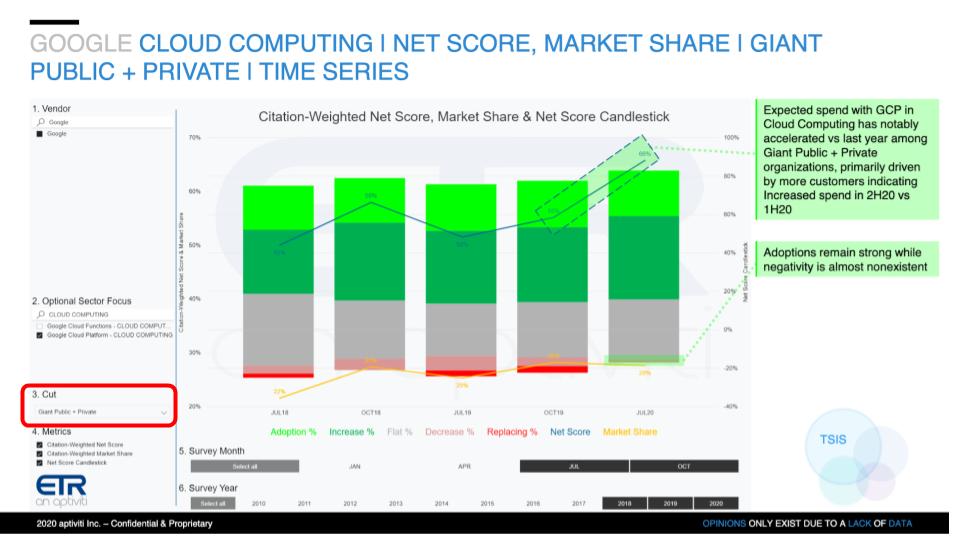

Looking into the ETR data for the most recent survey which ran in June and early July, Google Cloud is showing strength in an important bellwether sector, Giant Public and Private companies. These are the largest firms in the ETR data set and often point to secular trends. But before we get into that, let’s look at the big picture below depicting the spending momentum of Google Cloud Platform using ETR’s Net Score methodology.

Remember each quarter ETR asks its respondents are you planning to spend more or or less? In its July survey ETR focuses on second half spending. The above chart captures results across Google’s entire portfolio.

The breakdown for GCP across all sectors is shown:

- 14% of respondents are adopting new – that’s the lime green;

- 39% plan to increase spending in the second half vs first half – that’s the forrest green;

- A big fat middle at 38% is flat spending – that’s the gray area;

- 7% plan to spending less (pinkish slice);

- With 2% replacing Google Cloud this half – dark red.

We see this as mixed results. It’s not bad but it’s not off the charts either. We’ll get more information once ETR comes out of its quiet period on how this compares to Azure and AWS. Remember, Wikibon can only show limited views until ETR clients get the data and have time to act on it. But this calculates out to a Net Score of 44% which is respectable but not overly inspiring.

A Look at Spending Across the Google Cloud Portfolio

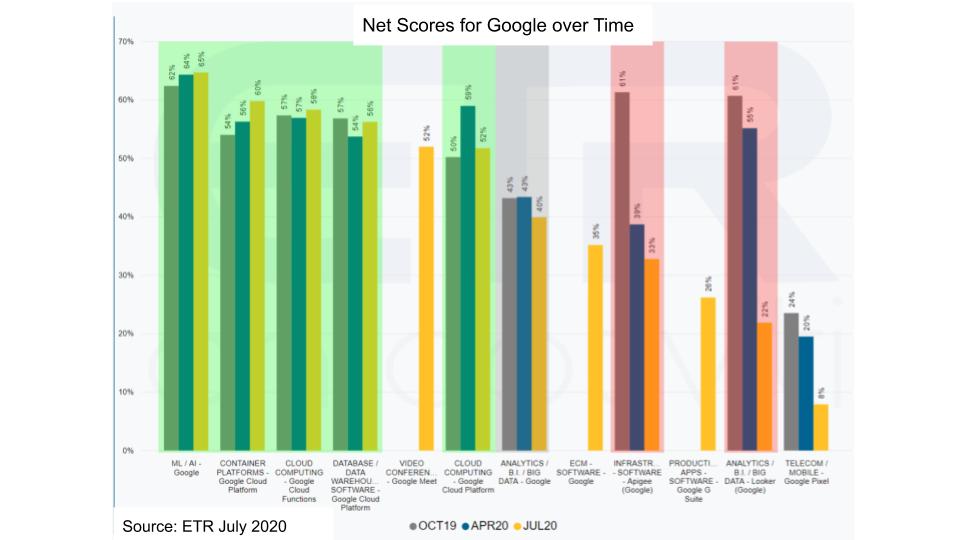

The chart below shows the Net Score comparisons across three different surveys, Oct 19, Apr 20 and Jul 20.

Reading the bars left to right you can see that the Google Cloud strong suit is machine learning and AI. Container platforms are very strong as are functions or serverless. And Database is very solid – we’ll talk more about that in a minute. Video conferencing was just added by ETR – sure it pops up with work from home (WFH). Core Google Cloud is actually holding firm when compared to October of last year. But surprisingly analytics is looking a bit softer. And ETR added G Suite in this survey with a 26% Net Score first time out which is very tepid – not impressive at all.

But overall the picture looks pretty good.

Digging into the Giant Public + Privates Bellwether

Now let’s peel the onion a bit and look closer at the results from the largest companies in the data set. The chart below shows the Giant Public + Private organizations so it would include the monster public companies but also large privates like a Cargill or Koch Industries if they responded in this survey.

And you can see above in this important sector it is a story of green with hardly any red. So quite positive sign for Google.

We think what’s happening here is these large and often far-flung organizations have realized that they have multiple cloud vendors and they’re asking their senior IT leadership to bring some consistency and sanity to their cloud strategies. So they look at the big three and say “what’s the best strategic fit for each?” So they might say let’s use AWS for core IaaS, Azure for productivity workloads and we’ll sprinkle in use Google Cloud in for certain machine learning projects.

So it’s a positive sign that we’re seeing some real strength in some of the larger accounts for Google Cloud, although interestingly, ETR tells us privately that there’s softness in the mid-sized and smaller companies that have powered AWS for so many years. So we’ll see how that plays out once ETR shares its full results with clients.

And of course COVID is the wildcard in all this – we have to take that into account and we will with Sagar Kadakia, ETRs Director of Research in the coming weeks.

A Look at Google Cloud in Database

Before we wrap we want to take a moment to talk about database. Remember, Google is playing catch up in the cloud and its marketing takes a more open posture around partners and things like multi-cloud. Contrast that to AWS for example, which is much more strict with its partners than Google.

But make no mistake, Google wants your data in their cloud. And that’s why database is so strategic and important. It’s the mother of all lock specs – just look at Oracle.

Now as we’ve reported many times, there’s a new workload emerging in the cloud around the modern data warehouse – We don’t even like that term anymore, data warehouse, because it sounds so static. But we’re talking here about workloads that bring database, machine learning, AI, data science, compute and storage along with visualization tools to deliver real time insights and operational analytics. Database is at the heart of this new workload. Win the database and everything else falls into place.

Google has six or seven database products and one of the most impressive in our view is BigQuery. For those who have followed theCUBE over the years you know we love the technology behind Google Spanner but BigQuery is where much of the action around this new workload will be happening based on our data.

Google’s Market Position in Database

Let’s have a closer look.

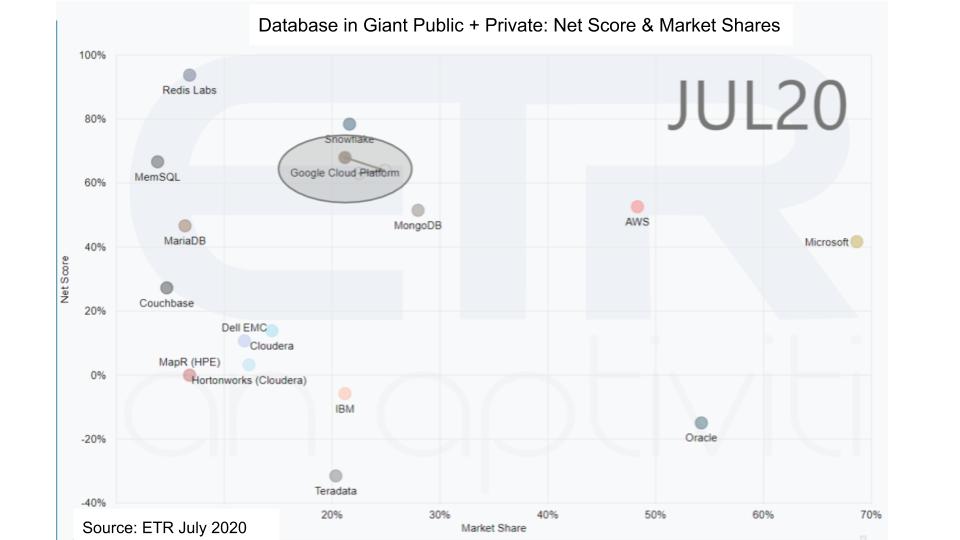

The chart above shows one of our favorite views. On the Y-Axis is Net Score or spending momentum and on the X-Axis is Market Share or pervasiveness in the database. The chart plots various database companies and their position within the all important Giant Public + Private respondents in the latest ETR survey. And you can see Microsoft, Oracle and AWS have very strong presence on the horizontal axis. Mongo looms large, MemSQL just raised $50M this past May and MariaDB just raised another $25M this month. You can see Couchbase and Redis show up – they are on our radar and we’re learning more about them continuously.

Databases is a hot market. All the cloud vendors are prioritizing database, the VCs are funding innovation and it’s because the total available market (TAM) is growing because of cloud, data AI and these new workloads.

As well in the chart you see Google strong Net Score but not the type of market presence you see from the other big cloud players. And in fact they’ve pulled back somewhat in the latest ETR survey so despite some bright spots in the enterprise it’s not quite enough just yet.

And look who is right there with Google – we know we sound like a broken record – but Snowflake is everywhere. You will find them in AWS, in Azure and on Google Cloud Platform. Now remember, Snowflake is about 1/10th the size of the Google Cloud IaaS and PaaS business but it has stronger spending momentum than all the big guys and continues to creep to the right.

Nonetheless, Google has great database tech and BigQuery is at the heart of its strategy to support analytics at scale and operationalize the data pipeline. And BigQuery is very well-designed, it started as cloud native from day 1, it’s based on serverless, is highly scalable and very cost effective.

Cloud Database Economics

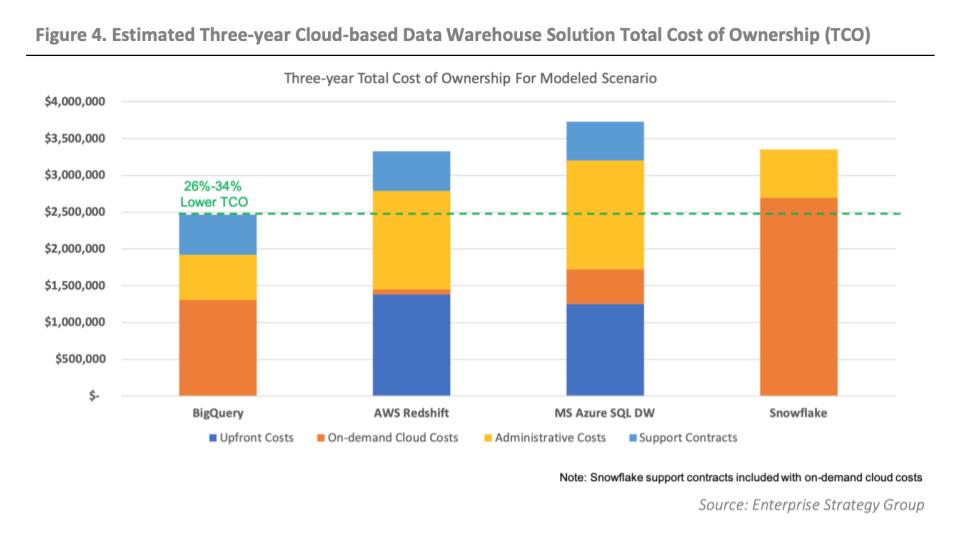

In fact ESG wrote a report comparing the TCO of the cloud databases that’s quite good. The report was commissioned by Google but it was very well done by a guy named Aviv Kaufmann. And you can see below it compares BigQuery with the other cloud databases.

Of course BigQuery wins with the lowest TCO, which it has to with a commissioned study. The author very likely chose a workload that favors BigQuery as that’s how these things go – but the report was really detailed and well researched in our view.

We have little doubt that Snowflake has an answer for that big brown bar which is on-demand cloud costs – we suspect ESG was making certain worst case assumptions about the need to over-provision resources for Snowflake, which no doubt ESG can defend but we’ll bet dollars to donuts that Snowflake has a comeback and we’ll look into that.

But the point we want to make here is that Big Query was designed from day 1 as a cloud native database. As such it’s cost effective and will be competitive from an efficiency standpoint.

So as you can see there are some bright spots in the enterprise for Google Cloud.

Final Thoughts

Having called out some of the positives – and there are many – Google Cloud is still not getting it done in the enterprise in our opinion. We certainly would not say “too little too late” but we would say they spotted the competition a huge lead. And the only reason is Google just didn’t act on the opportunities staring them in the face with enterprise cloud and finally woke up.

Enterprise sales are really hard. And Thomas Kurian, for all his experience, is coming from way, way behind with regard to enterprise go to market, processes, pricing, partnerships, special deals, etc. Google is still learning how to sell to business outcomes and is relying far too much on its technology chops, which, while impressive, are not going to win the day without better enterprise sales, marketing and ecosystem integration.

For years Google has said to the enterprise market “give me heat and I’ll add the wood.” Meaning we have the best technology so go ahead and use it. That strategy doesn’t work in the enterprise. Kurian knows it and we suspect that’s why Google is showing some strength within large customers – applying focused sales resources to nail customer success with some of its top accounts and then broadening its go to market.

We’ll learn more about Google’s intentions and its progress over the next few months as they try their online event experiment and of course we’ll be there providing our wall to wall coverage.

Remember these Breaking Analysis Episodes are all available as podcasts. ETR is exiting its quiet period this week and will be rolling out the data so check out ETR.plus. We publish weekly on Wikibon.com and Siliconangle.com and as always please comment on our LinkedIn posts we greatly appreciate the feedback.

Thanks for reading and we’ll see you next time.

Watch the full video analysis: