Contributing Analysts: David Floyer, Ralph Finos, and Peter Burris

Premise. AWS continues to grow behind a sound strategy and excellent execution; we think this will continue. However, enterprises are looking at options for migrating all or parts of existing high-value, DBMS-based applications into the cloud. For these customers, vendors that can show the simplest like-to-like migration path for DBMS platforms are best positioned to provide cloud services.

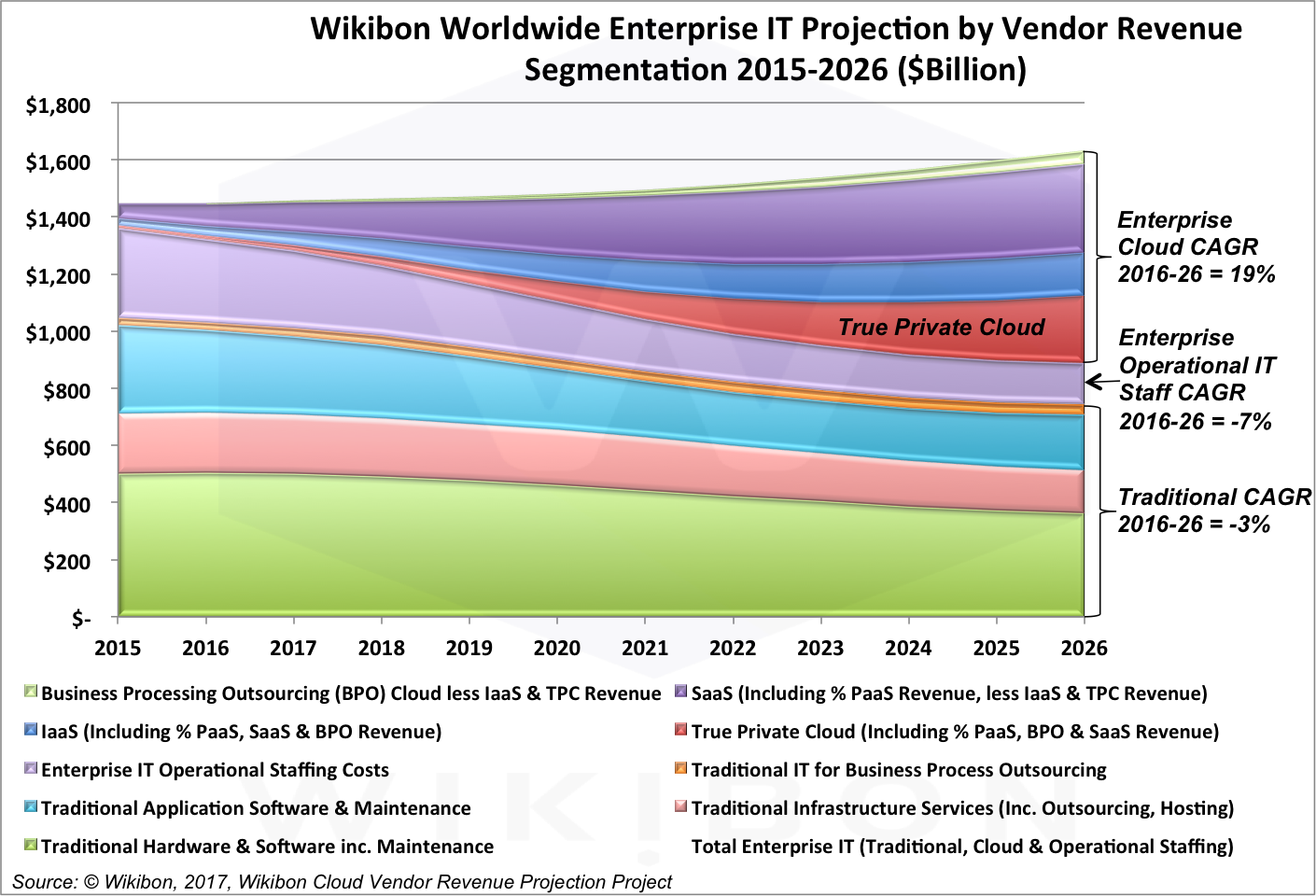

Will AWS dominate computing? Well, as software eats the world, the cloud is eating infrastructure, and no company is taking bigger bites than AWS. For the past few years, total global cloud revenues have grown over 43% per annum as businesses seek to deploy digital capabilities faster, better, and cheaper — by far the fastest growing segment of IT spending (see Figure 1). Greenfield development has driven the bulk of cloud growth: Start-ups creating SaaS companies and enterprises extending engagement capabilities to digitally-savvy customers. AWS, largely the inventor of generalized cloud services, has reaped much of opportunity, turning its first-mover advantage into sustained market leadership. Now, bolstered by cloud-based success, CIOs are exploring — sometimes driven by fiat from their boards — additional ways to utilize the cloud. A second wave of cloud adoption — hybrid cloud — is forming, and this wave is more up for grabs because:

- Greenfield applications continue to drive AWS scale. AWS remains the go-to option for greenfield apps, including entrepreneurs building SaaS companies, and that remains a sizable portion of the market. AWS is investing aggressively in capacity, capabilities, and technology integration to provide unprecedented scale efficiencies. On the basis of this segment alone, AWS will remain a potent force in computing.

- Legacy applications seek the simplest DBMS migration path. Moving legacy applications from one platform to another is hard. Put a DBMS in the middle of the application, and the effort becomes impossible for many organizations. While the AWS/VMware partnership provides a viable public alternative for VMware customers, Microsoft, Oracle, and IBM are better able than AWS to offer like-to-like cloud options for legacy DBMS and application customers.

- IoT prioritizes the edge. Because of factors like latency, entropy, regulation, security, data movement cost, and others, most processing related to IoT automation will take place proximate to the IoT events being monitored and enacted. The most likely scenario is IoT pulls the cloud to the edge, and not the cloud pulls IoT processing to centralized locations.

Figure 1. Worldwide Enterprise IT Spending Projection, Vendor Revenue Segment. Derived from the Wikibon research paper entitled “Cloud “Vendor Revenue” Projections 2015-2026” and Ralph Finos detailing Wikibon’s first-half 2017 cloud market forecast.

Greenfield Applications Continue To Drive AWS Scale

We believe that a sizable majority of SaaS start-ups target AWS cloud services, and we see little reason why this won’t continue. Moreover, AWS continues to provide superior services to enterprises seeking to extend the reach of their digital capabilities out to customers and remote or mobile employees. In addition, based on a combination of infrastructure cost and administration advantages and advanced analytic services, AWS is capturing a large portion of emerging big data workloads. These opportunities fuel significant AWS investment in new datacenter locations, dedicated bandwidth, integrated energy sources, and specialized hardware, and will continue to provide AWS with scale advantages. Despite challenges from companies like Google for greenfield cloud-based apps, we expect AWS will continue to play a central position in cloud computing for years to come.

To summarize: AWS is best positioned to win greenfield cloud business.

Legacy Applications Seek The Simplest DBMS Migration Path

As enterprises gain experience with cloud-based services, CIOs are beginning to explore approaches to migrating legacy, high-value, DBMS-based applications to the cloud. Why? Partly, it’s the carrot of modernizing IT capabilities and driving new classes of value from their digital assets. But the stick is playing a role here, too. As one CIO told us:

“I’ve been directed to get 40% of our workloads to the cloud over the next few years. The only way that happens is by moving some of our legacy.” CIO at a large financial services firm.

For those enterprises that made significant investment in VMware, the most likely path forward is VMware Cloud on AWS. Many specifics won’t be clear until the service is fully introduced later in 2017, but Wikibon believes it will provide a simple, economic path to cloud and application modernization for VMware customers.

For workloads that still run natively on Microsoft SQL Server, Oracle, and IBM DB2, the path to AWS is full of technical, licensing, and institutional potholes. To sustain customers, Microsoft, IBM, and Oracle have each made significant commitments to the cloud. Microsoft, in particular, has successfully pivoted to Azure and provides Microsoft shops a favored option. IBM has started moving long-term customers, like American Airlines, to cloud-based options, and has signaled that it will aggressively fight to sustain its customer base. The wild card is Oracle, which has proclaimed intentions to rebuild itself on a cloud foundation, but faces numerous obstacles as it attempts to do so. While the company’s application clouds and Cloud At Customer options are compelling to Oracle customers, converging Oracle’s hundreds of technology streams into a simpler set of hybrid cloud options is a significant technical and marketing challenge.

AWS is not being passive in this segment, though. The company launched the AWS Database Migration Service (DMS) in 2016. While not heavily marketed, AWS claims to have migrated 18,000 databases with DMS to date, a good starting number in a domain featuring heavy experience costs. Relative to other services that mainly utilize high-cost expertise to migrate databases, AWS DMS utilizes tooling like the AWS Schema Conversion tool and AWS IaaS resources to help facilitate a DBMS migration process. Wikibon believes the AWS DMS offering is worth exploring, but will not catalyze a wave of complex, high-value, DBMS application migrations to AWS.

To summarize: AWS’s dedication to great customer experience, leadership cloud engineering, and outstanding execution keeps it in the mix for legacy migrations, but this will be a market dogfight, and Microsoft, IBM, and Oracle (if it can execute) enjoy real technical advantages in their respective customer bases.

IoT Prioritizes The Edge

Hybrid cloud architectures that include true private cloud solutions on premises are most likely for legacy applications, but are a certainty for many IoT workloads, and most industrial IoT (IIoT) environments. The reason is simple: basic physics dictates real limits on how far data can be moved before latency creates an automation problem. Thus, even if a company wanted to move IoT data to a centralized cloud for processing, in a vast array of use cases, it couldn’t.

To accommodate the evolving impacts of edge computing, AWS is investing significantly in the Amazon Global Network, an impressive mesh of high-speed and high-quality links tying most major metropolises together; while AWS’s network won’t solve latency issues alone, it increases AWS’s control over network services. Moreover, the company is adding 4 additional regions in 2017 and expanding the number of POPs to move AWS services as close to customer locations as possible. Additionally, AWS introduced AWS Greengrass, a software package for Linux/ARM/x86 IoT nodes and devices that enterprises want to run AWS Lambda functions in environments that require local processing, feature intermittent connections, and seek to optimize data transmission costs to the cloud. Finally, AWS has introduced Snowball, an edge-based data capture device that can be left unattended at an edge location and then periodically shipped to AWS for cloud ingestion. Taken together, AWS’s IoT start is smart, but it doesn’t generally solve IoT-edge challenges.

The physical, legal, and security realities of the edge dictates that ultimately most edge data will be processed in place and that cloud services will have to move to the edge. However, at this moment, no large, traditional computing company has a clear IoT edge advantage. The companies that dominate the edge are those that offer supervisory control and data acquisition (SCADA) solutions to operational technology groups. Products from SCADA suppliers tend to be based on specialized combinations of hardware and dedicated control programs, and therefore are candidates to be “eaten by software.” The IoT edge, which is at the center of automation and other trends, is a catalyst for longer-term disruptions in computing architecture. Right now, there is no first mover.

To summarize: AWS has dipped a prodigious toe into the the flow of IoT computing, but will have to take bolder steps to bring the AWS cloud down to the edge, most likely in the form of appliances that extend AWS services and administrative control to edge use cases. However, AWS has time to take these steps; no company is in the IoT edge driver’s seat.

So, How Big Can AWS Get?

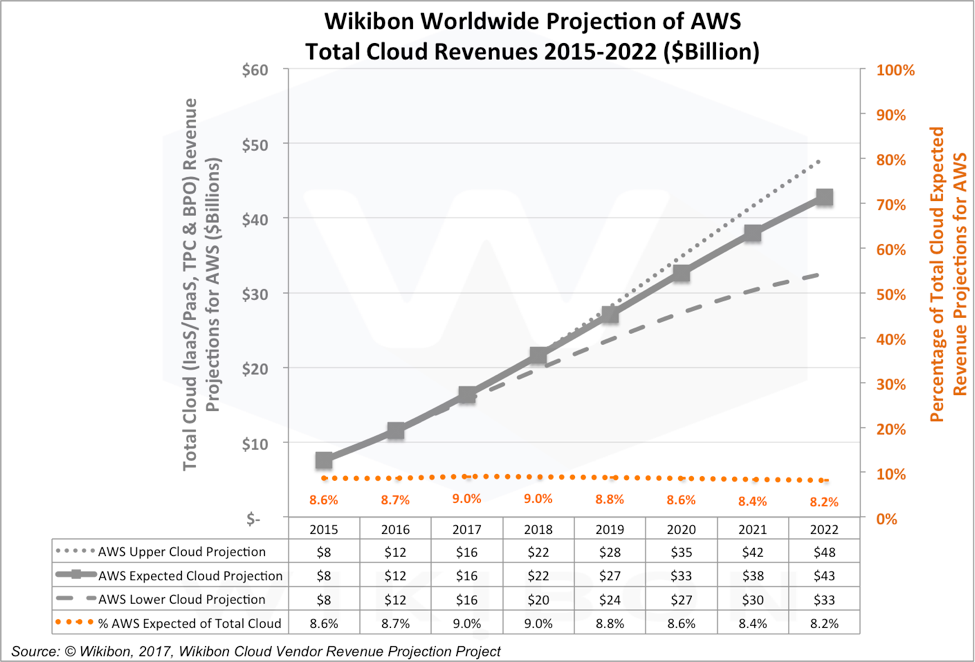

AWS leads the cloud market with a healthy 8.7% market share of 2016 enterprise cloud vendor revenue (see Figure 2). It’s strong 47% year-to-year fourth quarter growth puts it on a run rate of $14B annually. With that momentum, Wikibon believes AWS can drive revenues to $40 billion by 2022, generally sustaining share of the total cloud market steady, at 8.2%. How did we reach this conclusion?

The total enterprise cloud market is defined by Wikibon as the sum of:

- Software-as-a-Service (SaaS)

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- True Private Cloud (TPC)

- Business Processing Outsourcing (BPO)

In order to more accurately reflect vendor revenue, Wikibon has adjusted the definitions of the segments from the “Classic Segmentation” to a “Vendor Revenue Segmentation”. These segments are:

- SaaS revenues including PaaS revenue, less IaaS revenue for hosting

- IaaS revenues including PaaS, SaaS hosting revenue, TPC hosting revenue and BPO hosting revenue

- TPC revenues including PaaS, less IaaS hosting revenue

- BPO revenues including PaaS, less IaaS hosting revenue

The research entitled “Cloud “Vendor Revenue” Projections 2015-2026” provides a more extensive treatment of these definitions. Here, it’s important to note that the sum of the Classic Segmentation and the Vendor Revenue Segmentation are the same.

To devise our projections, we ran three scenarios: slower, higher, and most likely growth. The heavy line in Figure 2 is the “most likely” Wikibon projection of the AWS total cloud revenue. The dotted and dashed lines on either side are the upper and lower AWS cloud revenue projections respectively. The orange dotted line and percentage figures show the expected percentage of Total Cloud Vendor Revenue for AWS.

Figure 2. AWS Revenue Projections, 2015-2022. The heavy lines is the AWS Total Cloud Vendor Revenue, and the lighter lines the Wikibon upper and lower limits for the AWS projections. The dotted-orange lines reflect the percentage of the Total Cloud Market for AWS.

Our projections are based on our expectations of future market demand for AWS’s current portfolio. Currently, AWS competes in the IaaS/PaaS segment, and has the highest market share in the IaaS/PaaS segment. AWS also supports SaaS vendors with its IaaS/PaaS service, but has no direct SaaS investment. To date, Amazon has not offered a true private cloud solution using its own IaaS software or hardware. AWS will offer a full hybrid cloud solution for VMware users, with its decision to offer a native IaaS VMware solution separate from its own IaaS systems: VMware will directly sell this solution, starting in 2017. Most of the other hybrid services offered by AWS are low-cost data solutions as stepping stones to migration to the full cloud. We’ve outlined our assessment of AWS current strengths and weaknesses in Table 1.

| AWS Strengths | AWS Challenges |

| Low-cost storage and processor on-demand resources. | The high cost of migration of high-value, mission critical applications to run operationally in the AWS cloud. |

| Excellent IaaS and PaaS services built on providing operational solidity to open source greenfield projects. | The high cost of running high-function system-of-record databases such as Oracle, DB2 and Microsoft on AWS IaaS. |

| A very rich set of application development tools ideal for development in a cloud environment, and for deployment of greenfield applications. | The cost of migrating complex MSFT SQL Server, Oracle, and DB2 workloads to AWS Aurora, which features relatively reduced functionality. |

| A thriving application marketplace, and a sound home for startup SaaS vendors. | The migration cost and complexity of replicating complex application and data workflows that currently run on-premises. |

| Providing incubators for high-performance vector and FPGA processing. | The majority of traditional enterprises use AWS at the department level, and there is little interaction with enterprise IT. |

| A large number of datacenters in the US, and a growing number of data centers internationally. | The lack of an equivalent to the Microsoft Azure Stack or Oracle Cloud Stack, where the same software in the same environment can be run in the cloud or on-premises. |

| A potentially high quality native VMware IaaS offering, with low latency links to/from AWS IaaS/PaaS services. | The lack of distributed and integrated low-latency solutions for the “edge” in general, and IoT in particular. |

| A strong sales force that can communicate effectively with enterprise customers. | Given the current political climate, local government action against US cloud providers is likely to affect Amazon’s market share outside US international customers, and constrain enterprise cloud market share outside the US. |

| AWS is a great starting point for emerging software and service providers. | There is a significant requirement for second sourcing for IaaS (particularly in European and far-eastern countries). |

| Good customer loyalty – established AWS enterprises stick with AWS as they grow. | The cost of migration of many interconnecting workloads from AWS to other clouds is very high, because of proprietary AWS PaaS layer for orchestration and automation of workflows would need full conversion and testing as well as the migration and testing of applications and data. |

Table 1: AWS Strengths and Challenges As Hybrid Cloud Market Crystallizes

Based on the emergence of hybrid cloud and AWS’s current portfolio, Wikibon’s cloud market models suggest that AWS could attain a 40% share of worldwide IaaS Cloud Vendor Revenue, an impressive figure, but actually it is represents about 9.2% of the Total Enterprise Cloud Vendor Revenue. We show this as the upper limit in Figure 2.

The lower AWS limit in Figure 2 largely is a function of the international dynamics for cloud services. The increasingly central role of digital technology in commercial, social, and governmental spheres guarantees greater scrutiny of US-based cloud companies by EU and APAC institutions going forward, including AWS. The lower limit in figure 1 reflects this threat; should political winds blow against it, AWS market share in worldwide total cloud vendor revenue would grow to about 6.2% by 2022.

Our most likely scenario concludes that AWS can attain about a one third (33%) market share of the worldwide IaaS market, but not much more. Again, market success of this magnitude more than funds AWS technology and market innovation and ensures that it will be a major force in computing through this forecast period and beyond. However, our models show conclusively: AWS is not going to squeeze other big players out of the market. The cloud market will be turbulent and highly competitive. Ultimately, the success of Microsoft, IBM, Oracle, and others is tied to their ability to execute in their own customer bases and the emerging opportunities presented by IoT.

Action Item. AWS will remain a central force in cloud computing; all CIOs should entertain an AWS partnership. However, the cloud will not be a “winner take all” market. CIOs and business should continue to choose cloud technology and service suppliers based on business needs and workload realities. It will be a multi-cloud world.

Footnote: Data Sources

Overall cloud and individual vendor revenues are published in the Wikibon 2016 Public Cloud Forecast Update, and the True Private Cloud Projections 2015-2026. The Business Process Outsourcing revenues were projected as part of this research, but were a very small proportion of the total.

Links to details of this research and a much more detailed analysis of the methodology and conclusions will be found in upcoming Wikibon research entitled “Total Cloud Vendor Revenue Growth Projections.”