With John Furrier, Zeus Kerravala, Jake Kaldenbaugh and Steve Mullaney

HPE’s $14B acquisition of Juniper shines a light on two companies facing key strategic decisions. From Juniper’s perspective, growth had hit a wall and it either needed to go private or find a new path with a larger partner. HPE on the other hand needed to grow its footprint beyond what several tuck in acquisitions have provided. We believe that the acquisition makes sense for both companies and its respective bases as customers look to consolidate redundant vendors in core infrastructure sectors in order to sharpen focus and fund new innovation. While we don’t see this move as a dramatic growth driver for HPE, the acquisition will improve the quality of HPE’s earnings, bolster its free cash flow and further support strong momentum in its networking business, giving it more ammunition to compete with market leader Cisco and other networking pure plays.

Watch the full video analysis from theCUBE Collective team:

Competing with the King of Networking

Cisco has amassed a highly profitable business with networking at its core. As the company expands into security, software, collaboration, observability and other adjacencies, several companies are eyeing ways to get a piece of Cisco’s networking pie. HP, prior to its split, acquired 3Com in 2010 with the premise of creating an alternative to Cisco but the impact was minor. HP’s acquisition of Aruba, which went to HPE after the split had a dramatically more positive impact on HPE’s business and has become a fine jewel of the company’s portfolio.

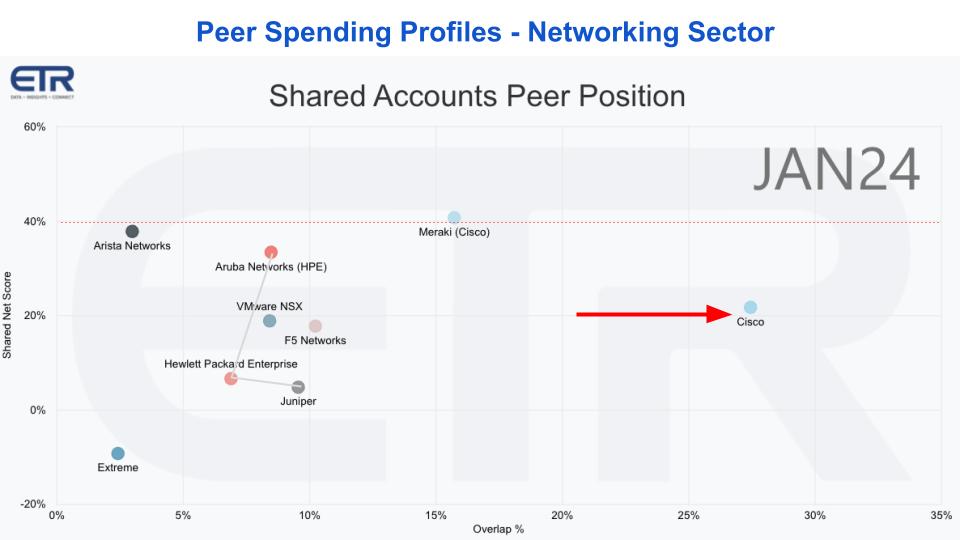

The following graphic from ETR shows the landscape of some of the key networking players.

The above data from ETR shows Net Score or spending momentum on the vertical axis and presence or pervasiveness in the data set on the horizontal axis. Anything at or near that 40% mark is considered highly elevated spending velocity.

Breaking this down a bit you have Cisco as the king of networking with a large business as you can see on the X dimension. They also own Meraki, the simplified management solution, which as you can see has very very strong momentum in the market. Notably, HPE’s Aruba also has strong momentum on the Y axis. Aruba is HPE’s networking crown jewel.

The ETR data also shows generic HPE networking, which is likely customers responding we use HPE networking versus specifying Aruba. This could include the legacy 3Com assets as well.

Juniper is kind of stuck in the pack with a Net Score in the low single digits for its networking business. It also has a security business which an asset HPE can leverage. But you put these 3 data points together and it doubles HPE’s networking business to around $10B and gives it a formidable asset to keep penetrating the market.

For context we’re positioning Arista and Extreme networks. The former which has great market momentum.

One last set of data points is we estimate that there is a 20-25% overlap between HPE networking and Juniper accounts. We estimate Cisco to have a 50% presence in those Juniper accounts. The point is Cisco looms large to be a consolidator in Juniper accounts and this move strengthens HPE’s position to fight for that business.

Networking is a Profitable Business

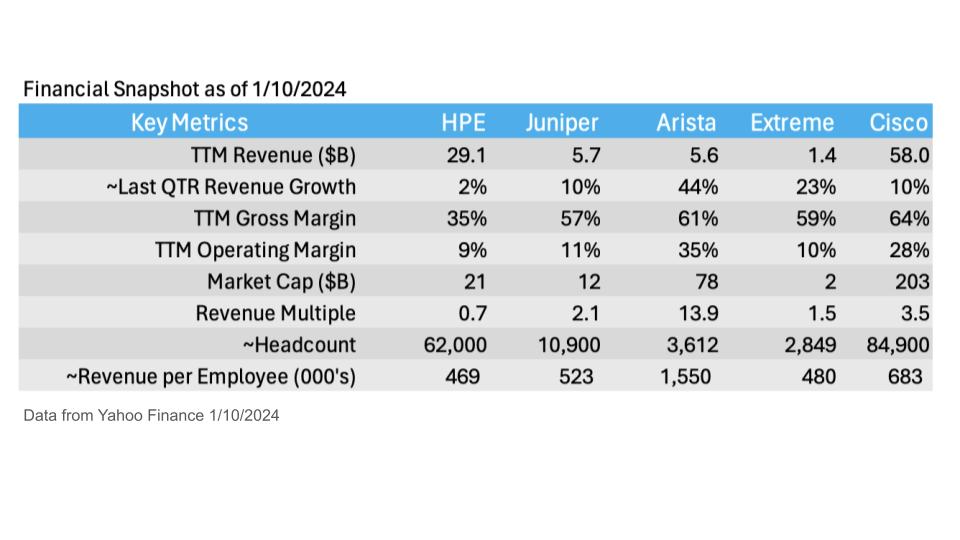

Networking is strategic and increasingly complicated. The table below shows key profitability measures of a select group of networking players and underscores why HPE would want to further invest in this business.

Above we show trailing twelve month revenue, last quarter’s growth rate, TTM gross margin, TTM operating margin, market cap, revenue multiple, headcount and revenue per employee.

The key takeaways here are:

- Networking is a profitable business — Much more so than HPE’s business overall.

- Cisco is the big player with a $60B business that everyone is going after.

- The market rewards Arista’s growth rate with a 14X revenue multiple and a margin profile that is similar to Cisco’s with Extreme as a solid niche player.

Juniper will Increase the Quality of HPE’s Financials

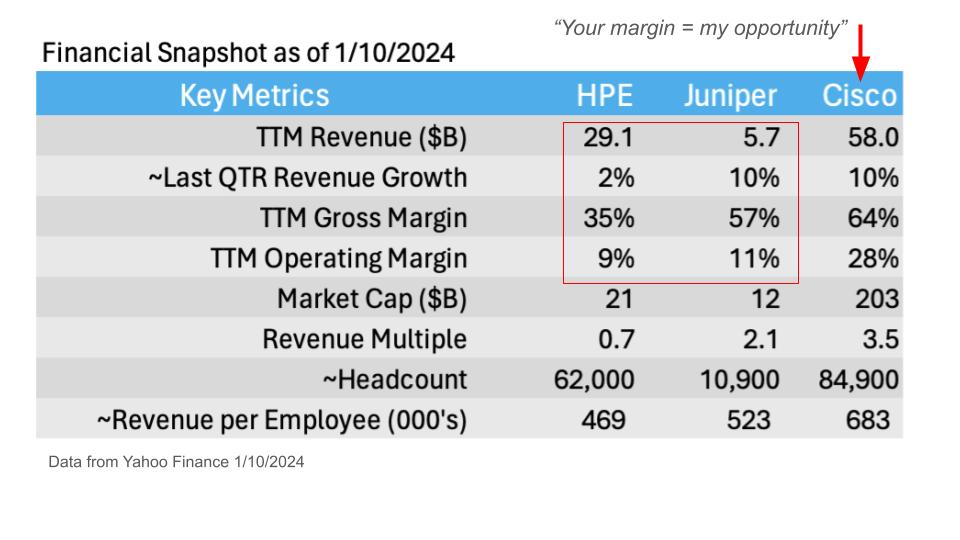

This chart below zooms in on HPE Juniper.

HPE is picking up a quality $5+B asset with some growth potential, higher than HPEs average gross margin and an operating margin that will be accretive within a year. The bottom line is this makes sense from a financial perspective and will bolster the quality of HPEs earnings.

Note that Juniper’s growth rate is overstated on this graphic as we’re only showing the most recent quarter’s revenue growth. Juniper’s TTM revenue is flat. Nonetheless, the quality of Juniper’s margin model will improve HPE’s financials and likely its market value, assuming HPE finds some go to market, services and other synergies.

Key Questions Moving Forward

We gathered members of theCUBE Collective to further analyze the impacts of this acquisition. What follows is a summary of the opinions from theCUBE Research and three industry luminaries.

The panel keys in on the complexities and potential challenges surrounding a major corporate merger, specifically focusing on aspects like timing, integration issues, and strategic implications. Concerns are raised about the difficulties typically encountered in mergers and acquisitions, such as integration, cultural clashes, and customer relations. There’s a specific focus on the consolidation of share and the execution challenges it presents. Additionally, the conversation delves into the strategic aspects of the acquisition, including its alignment with HPE’s edge-to-core strategy and the potential for growth in areas like AI and infrastructure. Our analysis also touches upon the cultural fit between the companies involved and the broader impact of such mergers on the industry, including the potential benefits for both customers and competitors.

Key Points:

- Concerns about Merger Timing and Complexity: High interest rates and the complexity of the merger are highlighted.

- Skepticism about Mergers for Share Consolidation: Historical challenges of mergers aimed at consolidating share are of concern.

- Strategic Implications for HPE: The acquisition’s alignment with HPE’s strategy and potential benefits in AI and infrastructure are notable areas of potential.

- Cultural Fit and Industry Impact: The cultural compatibility between Juniper and HPE and the broader implications for the industry are key considerations.

- Potential for Growth versus Consolidation: We believe the acquisition is primarily a consolidation play, with some potential for growth in AI and other areas.

Takeaway:

Our analysis suggests that while the merger between these companies aligns with strategic goals like enhancing HPE’s edge-to-core strategy and potentially leveraging AI, there are significant challenges related to integration, culture, and execution. The success of this merger will hinge on effectively navigating these complexities. Additionally, while there are opportunities for growth, particularly in areas like AI and distributed architecture, the primary driver of the merger appears to be consolidation, which will be beneficial for customers as it can narrow focus and enable investments in other areas of innovation. However, this move might offer advantages to competitors as joint customers adapt to significant change.

Leadership will be Critical to Success

Summary:

The panel delves into the strategic considerations and leadership dynamics of a corporate merger, focusing on Juniper’s role, the potential for growth versus consolidation and the challenges of integrating innovative technologies into larger platforms. Juniper CEO Rami Rahim’s leadership in transforming the company and the potential of Mist is, we believe, a key asset in the merger. Our analysis also touches on the difficulties of merging corporate cultures and the potential for internal conflicts. We assess other companies like Palo Alto Networks, Cisco, and Broadcom, examining different approaches to growth, innovation, and cloud integration.

Key Points:

- Leadership and Execution: Rami Rahim’s role as a key leader in Juniper and his potential impact on the merger’s success.

- Mist’s Strategic Importance: Specifically leveraging Mist for broader AI operations and its integration into HPE’s portfolio.

- Innovation vs. Consolidation: Questions remain on whether HPE can achieve growth through consolidation and innovation, similar to companies like Palo Alto Networks. We believe this is more a consolidation play than a growth move – other than it will add a one time bump to HPE’s revenue.

- Internal Conflicts and Talent Retention: Challenges in merging the cultures of Juniper and HPE, and the risk of talent attrition.

- Comparison with Other Companies: Insights into how other tech companies have navigated growth, innovation, and cloud transition with Fortinet and Palo Alto as notable success stories, which were not without real challenges.

- Cloud and Growth Strategy: The need for HPE to focus on cloud-centric strategies to achieve growth. HPE’s cloud native strategy is evolving and is today very on-prem focused.

Takeaway:

Our analysis suggests that while there are significant challenges in the merger, especially in terms of internal politics and integration, there are also opportunities for growth and innovation. The success of this merger may largely depend on effective leadership, particularly from figures like Rami Rahim, and the strategic use of assets like Mist. Additionally, the need for a cloud-centric approach is crucial for future growth, drawing parallels with strategies employed by other leading tech companies. However, the potential for internal conflict and the risk of failing to innovate could pose significant hurdles to the merger’s long term outcome.

An Insider’s Opinion of the Board Conversations that Led to this Deal

One of the panelists, Steve Mullaney is an experienced operator having led as CEO or as a senior executive at firms like Cisco, Nicira, VMware, Palo Alto Networks, Aviatrix and others. We asked him to speculate on that the board discussions were like leading up to this deal. What follows is the opinions he shared:

Summary:

The board dynamics within Juniper and HPE in the context of a potential merger likely focused on the motivations and strategic considerations from each company’s perspective. Juniper, experiencing a decade of a challenging growth environment, most likely viewed the merger as an escape route from its current stagnation. Similarly, HPE, trying to maintain relevance in a fast moving market, likely sees the merger as a necessary step. Both boards likley acknowledged the innovation and TAM expansion challenges and are looking for opportunities to reinvigorate their businesses. AI is a potential area for growth, with the merger seen as a chance to pivot towards this new direction. However, while there is hope for growth, the primary driver of the merger is consolidation.

Key Points:

- Juniper’s Stagnation: Juniper’s board is motivated by a challenging growth environment, seeking a change to break this pattern.

- HPE’s Quest for Relevance: HPE is similarly motivated by a need to stay relevant in an evolving tech landscape.

- Innovation Mandate: Both companies have hit a bit of an innovation wall and need to revitalize their strategies.

- AI as a Growth Opportunity: AI is seen as a potential area for innovation and growth in the context of the merger.

- Merger as a Consolidation Play: Despite the potential for growth, the merger is primarily viewed as a consolidation move.

Takeaway:

Our analysis suggests that both Juniper and HPE are entering the merger primarily as a strategic consolidation effort, driven by their respective challenges in growth and relevance. Companies with the maturity of HPE and Juniper have to “do something” to continue to drive innovation, with AI presenting a potential new direction for growth. The key question moving forward is whether the companies, especially under HPE’s leadership, can leverage this merger beyond consolidation and into a genuine growth opportunity in emerging technologies like AI.

Final Analysis and Takeaways

The Collective panel closes the session with the following analysis:

Summary:

We focused our closing session on the financial implications, strategic shifts, and the potential impact on the networking industry and HPE’s business. Key points include the profitability of networking compared to traditional servers, the shift from centralized to distributed computing and the integration of AI into a new network architecture. We have obvious concerns about the operational challenges of mergers like this and see it as a real test of Antonio Neri’s leadership – we feel he’s up for the task, especially if Rami Rahim stays engaged.

The importance of cloud integration, customer loyalty, and the potential for innovation in the face of financial constraints are also critical in our view. Additionally, the future of networking and the industry’s direction in 2024 are shifting, with a particular emphasis on the role of cloud networking, the integration of security with networking and the shifting strategies of other major players in the field.

Key Points:

- Profitability and Strategic Shift: Networking is more profitable (and sticky) than traditional servers, and transforming HPE from a compute to a platform company is intriguing.

- Distributed Computing and AI Integration: The industry is moving towards distributed computing, encompassing compute, storage, networking, and security, all integrated with AI.

- Operational Challenges and Cloud Integration: Merging the cultures and operations of HPE and Juniper presents challenges, with a strong emphasis on the need for effective cloud integration. With opportunities for HPE to improve its security position and move up the stack in other areas like data.

- Customer Loyalty and Stickiness: Juniper is recognized for strong customer loyalty and the stickiness of networking products, making switching vendors difficult. We see this as advantageous for HPE.

- Financial Constraints and Innovation: HPE’s debt load could impact its ability to innovate and make future “up the stack” acquisitions. However there’s potential for growth through automation and AI.

- Predictions for Networking in 2024: We expect continued consolidation in the industry, growth in cloud networking, increased importance of security in networking and more brutal competition among major players.

Takeaway:

Our analysis suggests that the merger between HPE and Juniper is strategically aligned with the shift towards a network-centric, distributed world, offering potential for long-term benefits. However, the success of this merger hinges on effectively navigating the integration of distributed computing and AI, overcoming operational challenges, and leveraging customer loyalty. Additionally, the financial aspects of the merger, while beneficial from a quality of earnings standpoint, bring concerns, especially in terms of debt and investment in innovation. Looking ahead to 2024, the industry is expected to see further consolidation, a focus on cloud networking, and significant competition among key players, all of which will shape the landscape of networking and security.

Image: Sundry Photography