In this episode of theCUBE Insights, Powered by ETR, we put forth our 2020 predictions using insights gleaned from theCUBE blended with the ETR spending data.

2019 marked our tenth year of doing theCUBE. Over that time we’ve had the pleasure of covering nearly a thousand events and milestones including the exit from the great softness of 2008 2009 and the tracking of a ten year bull market led by the tech sector. We’ve covered the era of data, seeing the rise and profitless prosperity of the Big Data and open source Hadoop movement where we predicted that practitioners, not vendors would benefit the most from big data. We covered many dozens of acquisitions including the $60B EMC chess move by Michael Dell and the launch of hundreds of startups in flash, hyper-converged, Big Data, AI, Blockchain, Crypto, SaaS and security. But there will be other days to review theCUBE’s ten years.

This post is all about predicting the future using data and insights.

Changing Dynamic in Digital

Let’s get into the data and start with high level spending. Remember in October 2019, ETR released its survey results and stated that we’re coming out of a multi-year investment cycle in digital transformation. Enterprise IT buyers have learned what works and on which technologies they’re going to double down. They’re now narrowing their investments on emerging technologies and picking winners for next gen tech. At the same time they’re cutting redundancies from legacy players that they were keeping as a hedge. Buyers are picking bundled suites from a handful of mega vendors and solidifying investments.

We’re seeing a multi-generational dynamic repeat itself where buyers are creating a balance between the convenience of packaged offerings (i.e. bundles) and leveraging best-of-breed tech for innovation.

On balance the ETR data shows that a contraction in spending and tepid CIO sentiment is impacting emerging vendors as well as traditional players. These trends are most pronounced in the very largest organizations which have always been the best bellwethers in ETR’s data.

Here’s what one IT executive said recently that I think sums up the situation:

This sentiment validates what many of the customers convey to us on theCUBE.

The Macro Economic Picture and Tech’s Role

Looking at the macro economy. GDP growth is going to land at about 2.3% this year give or take. It’s not going to hit the Trump administration’s goal of 3 percent plus, but consumers are powering steady growth.

IT spending should grow at about a point or two above GDP so let’s put that at 4%. In December we saw a powerful “Santa Claus Rally” and the S&P held above 3200. The tech sector has been a powerful tailwind for stocks. We think that may take a breath in early 2020 but expect continued strong growth in tech in 2020 tied to the strong economy after a Q1 pause. We could see the S&P flirt with 3700 or even higher in 2020 and tech will be a benefactor of that momentum, providing impetus for continued growth.

So much of 2020 is going to be about the election and the election is going to be about the economy. We predict the economy will remain steady and as the IT leader quoted from the ETR survey said earlier, they will be operationalizing what’s been purchased. Here’s what’s different in 2020. Tech projects have been historically risky investments and have required higher internal rates of return to get approved.

But the cloud has altered two factors. One is that it has allowed more experimentation for way less money. Second is the cloud – by shifting CAPEX to OPEX allows for much more incremental, lower risk investments. So we think you’ll see continued steady growth powered by the cloud, which allows experimentation and importantly – higher hit rates of success. These successful projects will throw off cash for companies and CFOs are getting on board, realizing that IT does matter…maybe not in the form that Nick Carr envisioned, but a new generation of IT that creates competitive advantage.

Cloud Spending will Moderate but Continue to Steal Share

Which brings us to the next prediction. The growth in cloud computing will moderate but will also continue to steal significant share from on-prem spending. The narrative that the pendulum is swinging back is a false narrative in our opinion. Rather the pendulum has swung and the cloud is the underpinning of innovation. Having said that we do think we’re seeing a bit of an equilibrium in spending where buyers have identified those workloads that will remain on Prem – which is why you see for example AWS, Azure and Google making moves in hybrid / on-prem offerings.

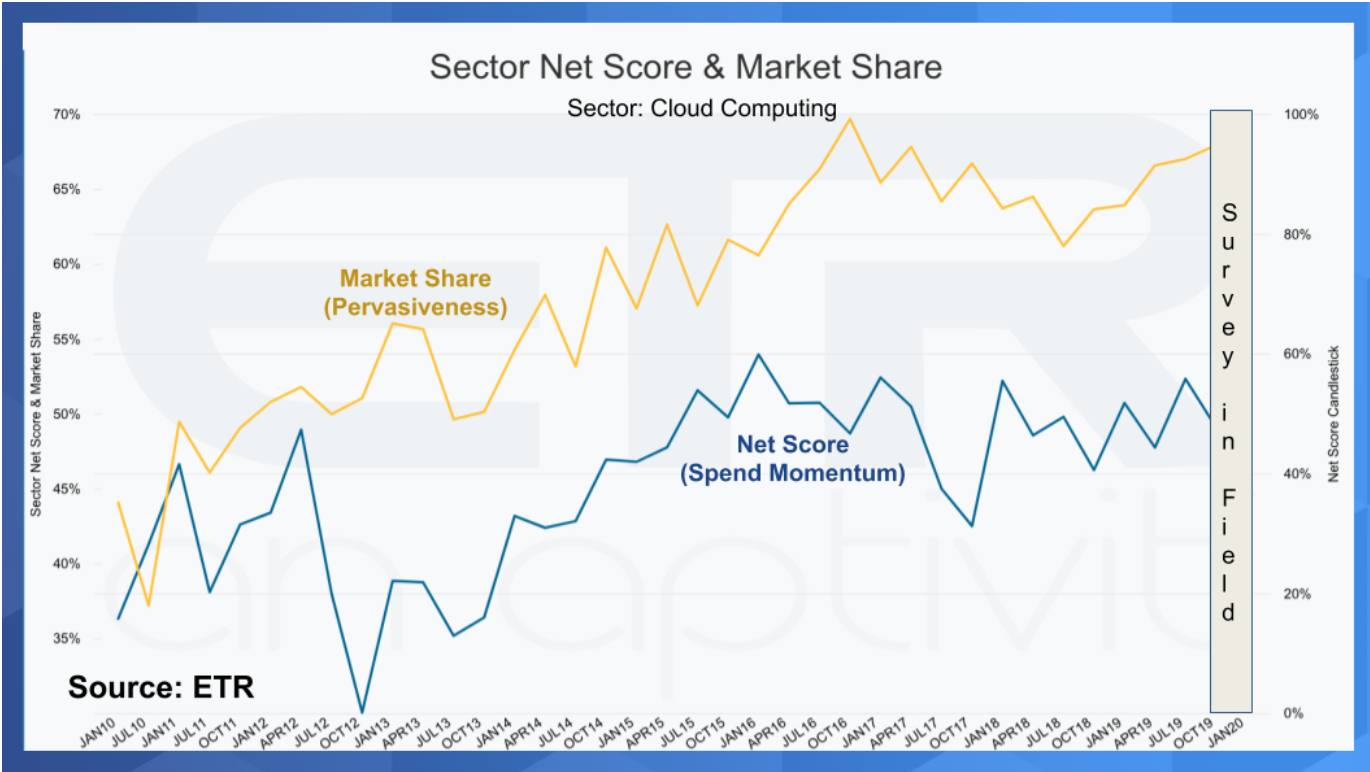

The chart above shows data from 2010 through the October 19 survey on Cloud spending. We have to block out the 2020 survey as it’s currently in the field and we’re not allowed to show that data just yet. The Yellow line is market share which in ETR parlance is pervasiveness or mentions in their surveys of a specific sector as a percent of the total spending sample. The blue line is spending momentum measured as net score – which essentially subtracts the percent of customers spending less from those spending more. The long steady march of cloud as you can see continues and there’s no indication that it’s going to abate. That said, the penetration of cloud has become much more meaningful so share gains will be more hard fought.

Cloud’s Size will Make Share Gains Harder

Now you may see this as a non-prediction or a hedge. It’s not. Let’s be clear. Cloud will continue to steal share from On-prem but share gains for the cloud vendors will be more difficult. Which is part B of this prediction.

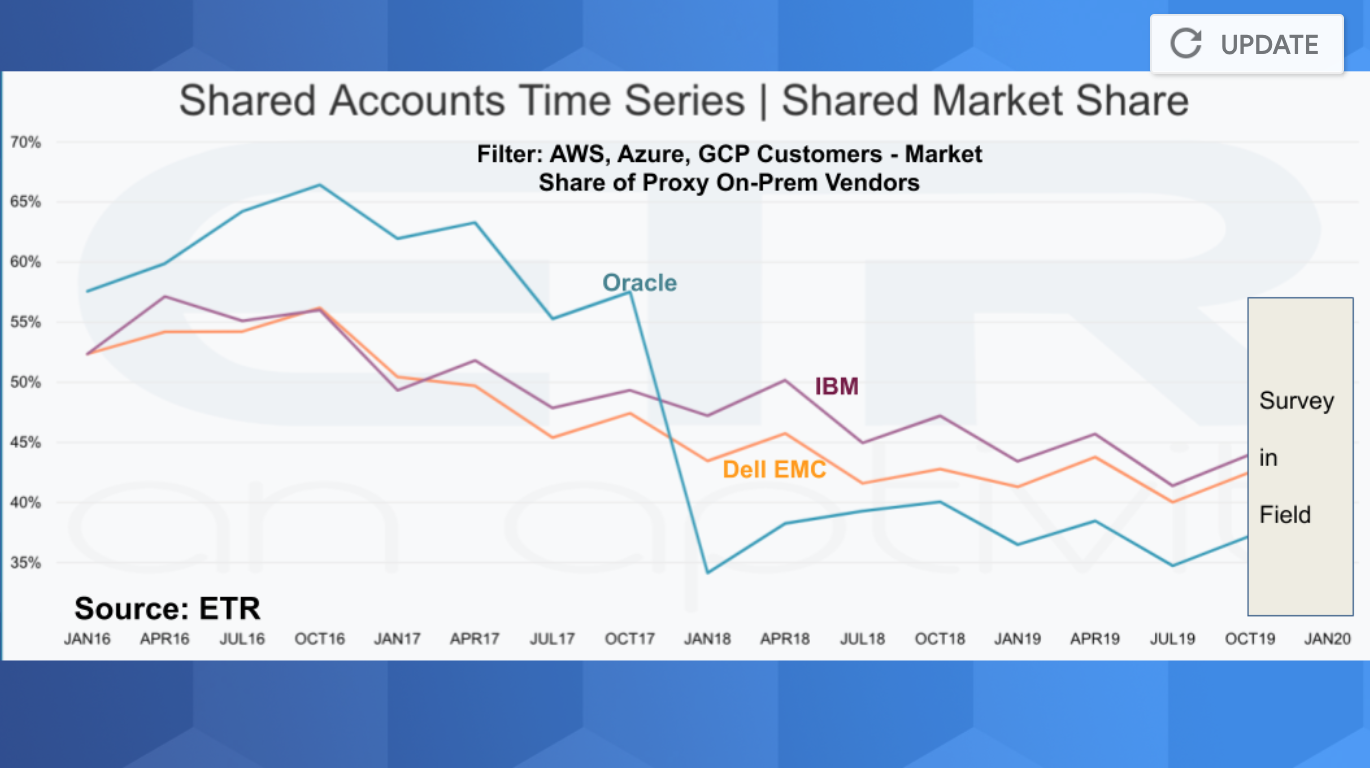

The chart above is market share from ETRs Jan 2016 survey through October 2019. And we’re showing spending for three on-prem vendors within AWS, Azure and Google Cloud accounts…picking on Oracle, IBM and Dell EMC as three prominent on-prem proxies. You can see the steady decline in market share for these companies. And even though there’s a bit of an uptick in October we don’t see this as a reversal. What’s going to happen in our view is that traditional On-prem vendors are going to step up their cloud strategies specifically with multi-cloud management. This will be the case with Dell leveraging VMware…and in the case of IBM, they’ll try and leverage Red Hat in the multi-cloud game and both IBM and Oracle, who both have public clouds – will dig their heels in, get customers in a headlock and provide big financial incentives for them to use their captive clouds.

Predicting Five Winning Companies in 2020

With the high level spending comments made earlier and that cloud discussion as a backdrop, the question is which companies will do well in the coming year. We’re going to call out five companies that we want to highlight where the ETR data intersects what we’re seeing on theCUBE. The prediction is these five players will do well in 2020, they will power through any downturn in spending and they will thrive in the face of the cloud share shift.

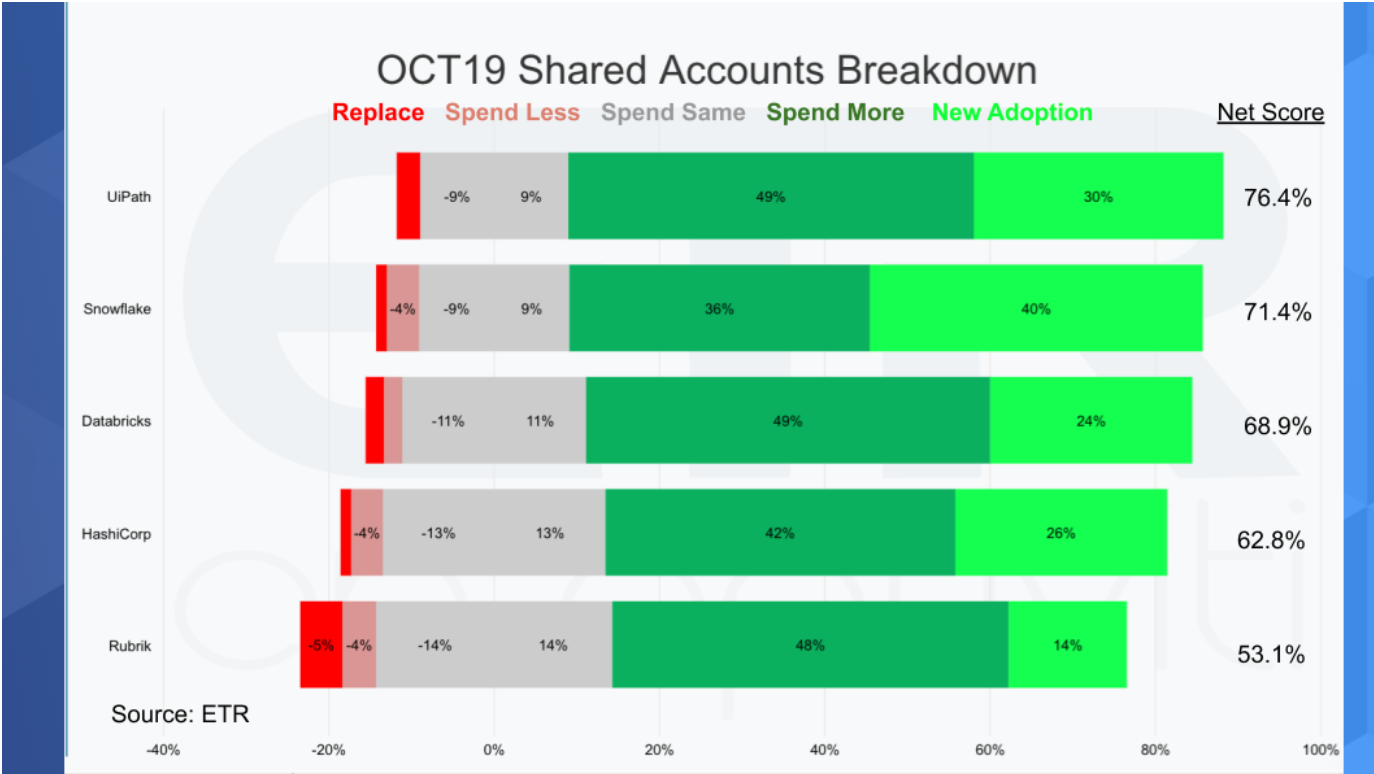

This chart shows data from the ETR October 19 Survey. It lays out net score or spending momentum for these companies that we’re predicting will be winners in 2020 and beyond. The five companies are UiPath, Snowflake, Databricks, HashiCorp and Rubrik.

UiPath

Let’s start with UiPath. They are the leader in robotic process automation. We think RPA will do well even in a downturn because even more companies will be looking to automate and save money in a software climate. Automation Anywhere is another player in this space that’s doing very well. We predict that UiPath will come out on top in this space but both companies can do well.

Snowflake

Snowflake is changing the analytic database market. We’ve covered them in previous Breaking Analysis segments and they will continue to thrive in our view. They are 100% cloud based and participate in all popular cloud platforms. Ironically, they compete with RedShift from AWS who continues to copy some of the innovations that Databricks popularized. We saw this at the most recent AWS re:Invent where Amazon announced that it is allowing more granular scaling of compute and storage independently. Snowflake was founded on this premise and was the key innovator in that regard. Nonetheless, AWS and Snowflake are strong partners and there’s room for both companies to thrive.

Databricks

Which brings us to Databricks. We’re seeing a new type of workload emerge in the cloud for modern analytic databases where organizations are taking all this data that they have in the cloud. Structuring it within a Snowflake database (for example) and bringing Databricks tooling to the equation to be able to query and visualize the data in real time. AWS plays here as well with RedShift and of course selling lots of EC2. All major cloud players are seeing this type of workload enter the mix and it will be a strong area of growth in 2020 and beyond.

Hashicorp

Next we want to focus on Hashicorp. Hashi is capitalizing on the trend toward cloud native computing. The company provides open source tooling for developers and is all about simplifying application deployment, independent of underlying platform (virtual, container, cloud). Five years ago the players in this space that got the attention were Chef, Puppet Ansible and SALT. Today – especially on theCUBE you hear the most about Hashi and Ansible. In fact at AnsibleFest on theCUBE we heard tons about HashiCorp. So they both complement and compete with the older players – kind of like Spark within the Hadoop ecosystem. Hashi has raised about $174M in VC and as you can see they have very strong spending momentum in the ETR data set with a net score of 63%.

Rubrik (and Cohesity)

Finally we want to talk about Rubrik which has been a consistent performer in the ETR data set. They are trying to transform backup into a data management discipline. They compete with the established players in data protection like Veritas, Dell EMC, IBM and Commvault. Rubrik is not the only new or newish player here that’s doing well…as Cohesity who is relatively new and Veeam which has been around for a while, both do very well in the ETR surveys…But Rubrik has been a consistently strong performer. Cohesity has not shown as much strength in the ETR surveys but we believe they are doing very well and will show more momentum in spending surveys in 2020.

Kubernetes – Continued Strength but Eventually Invisible

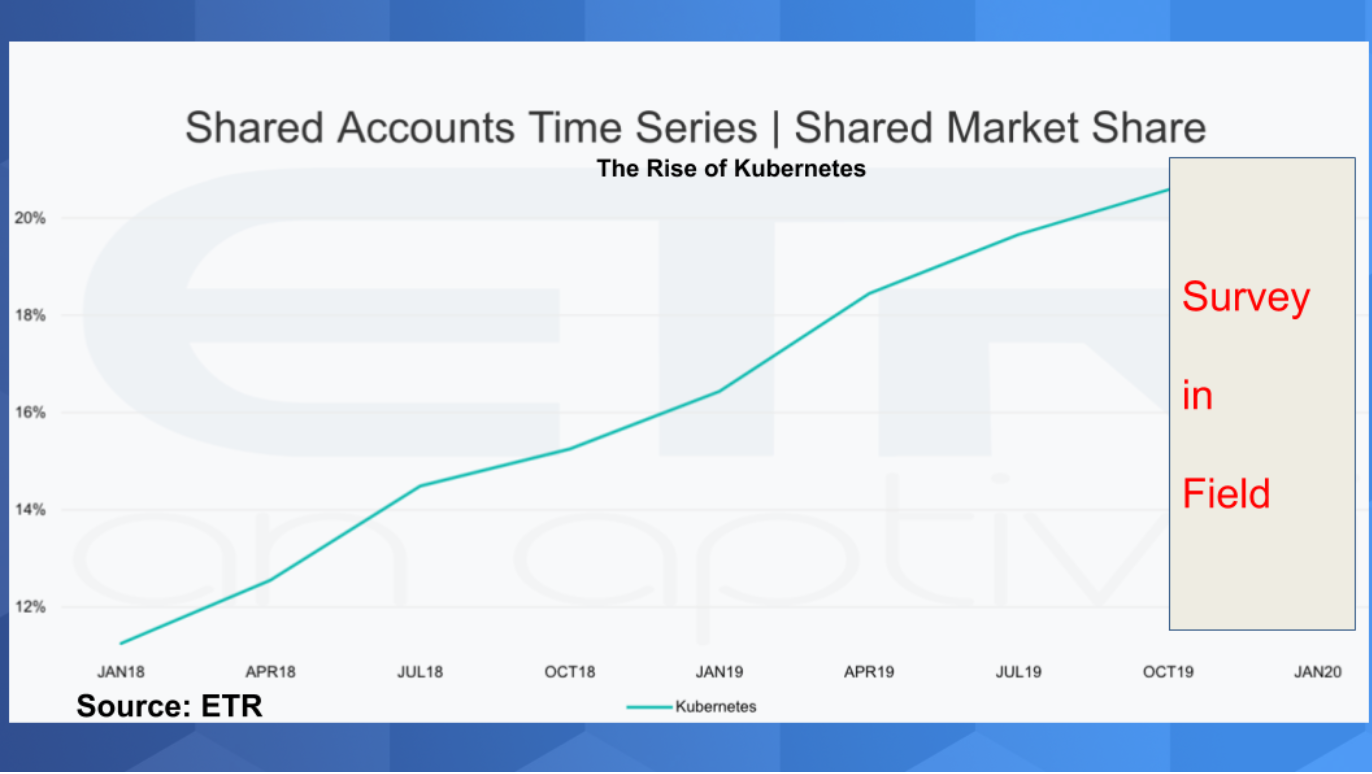

Next we want to highlight Kubernetes. The prediction is twofold – Kubernetes will continue its strong showing as this data from ETR shows.

The chart above shows Kubernetes market share in ETR parlance. Notably, in the October survey Kubernetes spend had a 76% net score – so very strong. But the other part of the prediction is that Kubernetes will become embedded into every platform and people will stop thinking about it as a separate market. Already today there’s little discussion of the idea of a Kubernetes distro. Anthos is an example of a Kubernetes stack but it can be run in the cloud, on-prem…anywhere. VMware Tanzu and Azure Arc are other examples that are not stacks but they’re management platforms that can manage anyone’s Kubernetes instances. Think of this as similar to flash storage. Remember everyone looked at flash as a separate and distinct market? Well today it’s just embedded everywhere and that’s what is happening with Kubernetes. So spending momentum will continue to be strong but by 2023 Kubernetes will ubiquitous and not thought of as a separate space.

Cyber will Remain Fragmented but Four Star Players will Emerge in 2020

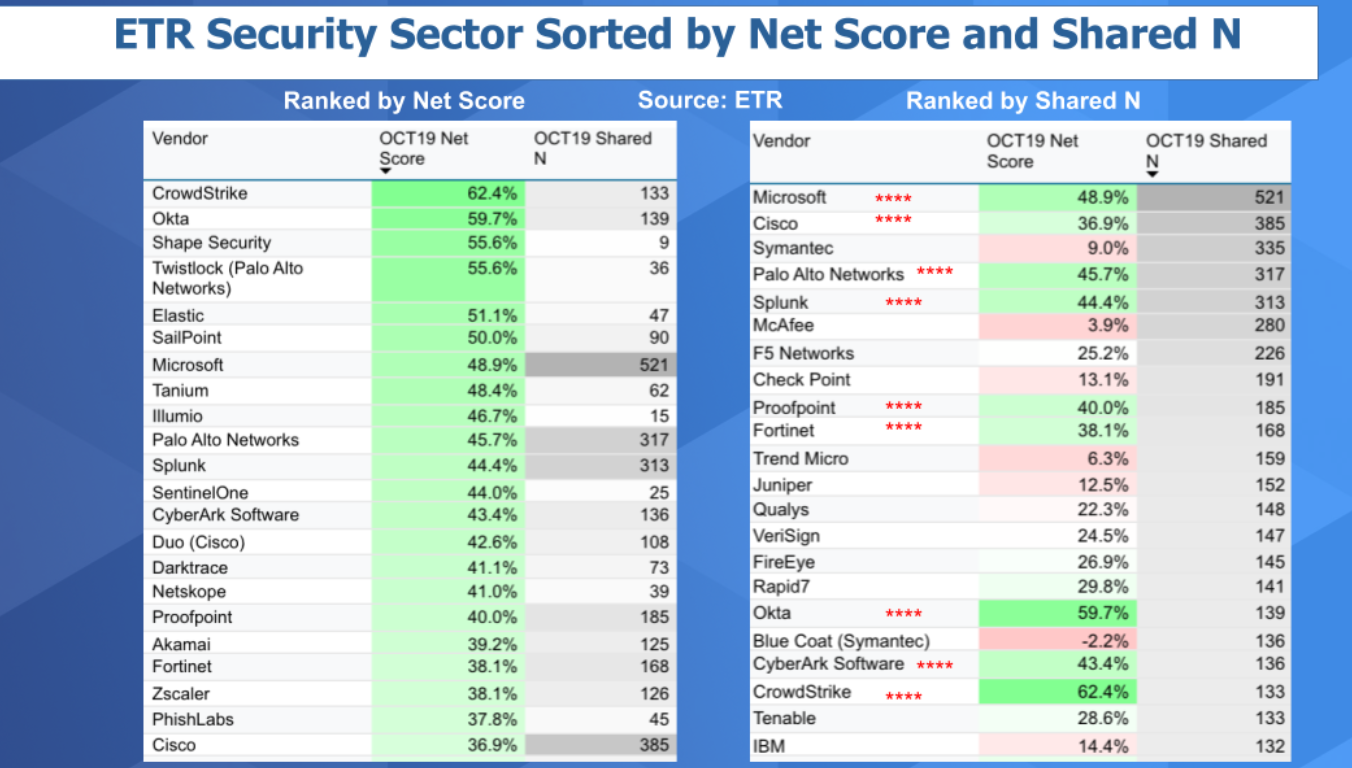

The next prediction focuses on Cyber Security. We did a Breaking Analysis earlier this year on Security and we showed the following chart. And as you can see, We’ve added a little something in the red stars for the prediction, identifying nine companies that we believe in 2020 will show both spending momentum and a large presence in the market (i.e. share gains or holding position).

The above chart shows two views of Net Score, which in the ETR data set is an indication of spending momentum. The left hand side shows the ranking by Net Score. You can see CrowdStrike, Okta, Shape Security -which was acquired by F5- Twistlock (now Palo Alto Networks) and you can see the others trailing but still solidly in the green (an indicator of momentum).

On the right hand side is Net Score but it’s ranked by Shared N – which is a measure of pervasiveness in the ETR data set. What we’ve added is the four star companies – that is those companies that have both spending momentum and are pervasive in the ETR survey. So the prediction is 2020 will see the four star companies maintain their position and gain strength in 2020. These include established players with portfolios they can bundle like Microsoft, Cisco, Palo Alto Networks, Splunk, Proofpoint, Fortinet and CyberArk Software. And then the newer companies like Okta and Crowdstrike will continue to gain share faster than the larger players. As well you may even see companies like Sailpoint, Illumio and Sentinel One emerge as four star companies.

Now the one company not on this list that is a major player in security is AWS. AWS is THE cloud security leader and is in a category all by itself in many ways.

As we cited in our Security segment earlier this year, the market is incredibly fragmented and it will stay that way. Each year we look back and say did we spend more…are we more safe? And every year the answer is Yes and No. And 2020 will be no different.

If you look at various data sources we spend approximately $120 billion annually on cyber security. The worldwide economy is about $85 Trillion. On balance we spend about .14% of our economy on security. We’re barely scratching the surface. So the market will remain highly fragmented, the rich will get richer if they have four stars and new players will continue to enter the space…we also expect M&A to remain robust.

The Edge will be Won by Developers

If you exclude our long shot that the S&P will break through 3700 next year – that makes nine. For the tenth and final prediction we don’t have hard data but we have strong opinions and that is that the Edge will be won by developers. Specifically, platforms like Outposts which are essentially programmable infrastructure bringing a cloud development platform to the edge, is how that space will evolve in our view. It won’t be won but shoving traditional servers and storage boxes out to the edge – rather it will grow by coders being able to build new applications and workloads on top of infrastructure as code.

That wraps up our 2020 predictions. We’d very much love your opinion – please leave your thoughts or predictions in the comments section of the youtube video below or on our linkedin posts where we publish these segments regularly. Or you can message @dvellante on twitter. And don’t forget this series is available on iTunes, Spotify and other podcast platforms for your listening pleasure.

Here’s the full video of this episode: