Contributing Wikibon Analysts

Ralph Finos

David Floyer

Brian Gracely

Stu Miniman

Premise

Public cloud is a disruptive technology changing the face of enterprise IT. By providing infrastructure services (IaaS), applications service (SaaS) and platform services (PaaS), cloud service providers are changing IT procurement from capital investment to operational expenditure, and allowing traditional IT to be by-passed. As the Internet of Things grows; as Internet data streams become a larger proportion of enterprise data processing; the locus of IT will shift closer to the Public Cloud, and reduce the friction for IT adoption. Wikibon expects Public Clouds to comprise about one third of total enterprise IT spend by 2026. Wikibon expects that this move will have significant impact on traditional IT hardware and software vendors.

Executive Summary

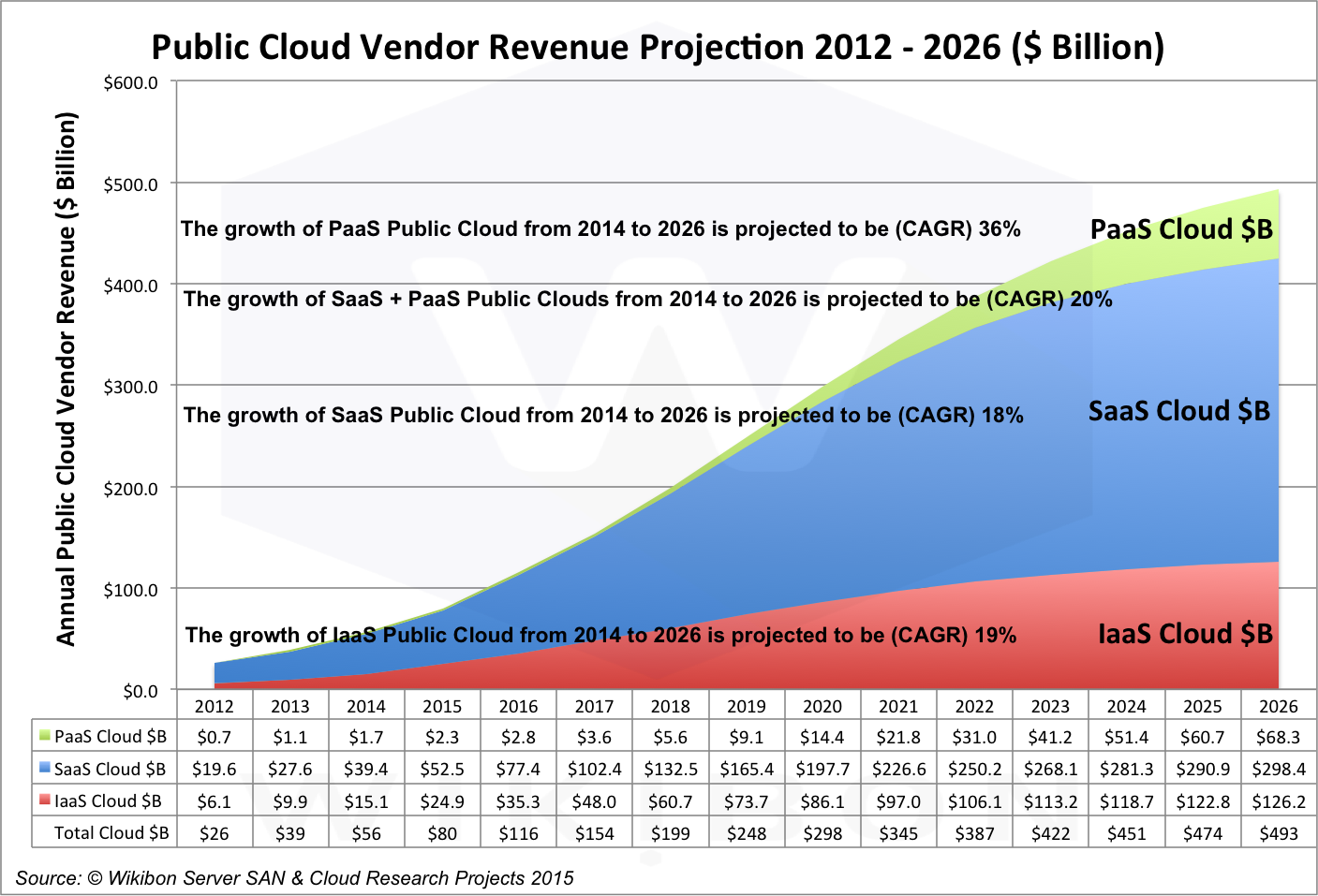

The recent earnings results of Amazon, Microsoft, and IBM indicate that Public Cloud is accelerating dramatically and will continue to do so until it grows to $493B in 2026 (20% CAGR). Each Public Cloud segment will be growing by double digits compounded annually in this period – PaaS (36% CAGR on a small base), IaaS (19%), and SaaS (18%).

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

Tier 2-4 applications, i.e., collaboration, mobile, development, infrastructure, analytics and business intelligence workloads will continue to be rapidly migrated to public clouds. Core cross-industry applications like ERP and some vertical industry workloads will be gaining significant traction in the forecast period as leading solution providers, i.e., SAP, Oracle, and others, start to move their customer bases from license to Public Cloud subscription offerings. Growth will be constrained by capacity challenges (physical data center build-out), technology challenges (application and infrastructure complexity) and business requirements such as security, data sovereignty, regulatory, and compliance considerations. Alternative approaches will include private and hybrid cloud and a continuing place for legacy workloads that are not readily addressable by any cloud technology we can foresee in the decade ahead. However, in many cases the advanced services in Public Cloud even today are more robust than in most data centers. Wikibon expects large cloud providers to continue to rapidly improve their offerings so as to mitigate lingering obstacles going forward.

The stakes for an enterprise to get its Public Cloud strategy right are very high. Wikibon believes that Public Cloud will represent as much as 33% of all IT revenue for data center infrastructure, software, outsourcing, and related services by 2026. In that scenario, uncertain market leadership could be an adoption barrier as enterprises develop their long term cloud plans. Overall, the Public Cloud market today is very fragmented with 100s of participants in most segments of traditional IT. Today’s Public Cloud market leaders – i.e., Salesforce (SaaS, CRM), Amazon Web Services (IaaS, PaaS), and Microsoft (IaaS and SaaS, SaaS for Personal Productivity) – have large positions in segments that do not significantly overlap (although Azure and AWS are going head to head more often). The traditional IT vendors – e.g., Cisco, IBM, HP, Oracle, SAP and VMware – have mostly acquired their way into the Public Cloud and are still sorting out their respective strategies. Rapid adoption of Public Cloud for Tier 2-4 workloads has enabled nearly all vendors to easily grow in at least the 20-30% range annually. Competition overall will become intense in the next decade as vendors try to achieve scale via acquisition, migrating license products to subscription products, and head-to-head competition to achieve a “cloud” brand leadership position.

Cloud Deployment Models

This report focuses on Public Cloud vs. Private and Hybrid (or Composite) markets. Wikibon follows the NIST guidelines about the types of Cloud offerings. Wikibon will be reporting on Private and Hybrid (Composite) Cloud markets in subsequent research scheduled for 2015.

- Public

- Provisioned for open use by the general public.

- May be owned, operated, and managed by an organization and it exists on the premises of the provider.

- Cloud-based application is fully deployed in the cloud and is managed and run in the cloud.

- Could be developed and/or migrated from an existing internal IT datacenter.

- Private/On-premises

- Provisioned for exclusive use by a single organization. It may be owned, managed, and operated by a third party as well as the single organization itself. It may exist on or off premise.

- Using virtualization and resource management tools for greater infrastructure and management efficiency and flexibility when the application is best deployed.

- Hybrid

- Cloud infrastructure is a composite of two or more distinct cloud infrastructures (private, community, or public) that remain unique entities, but are bound together by technology that enables data and application portability.

Public Cloud Segment Definitions

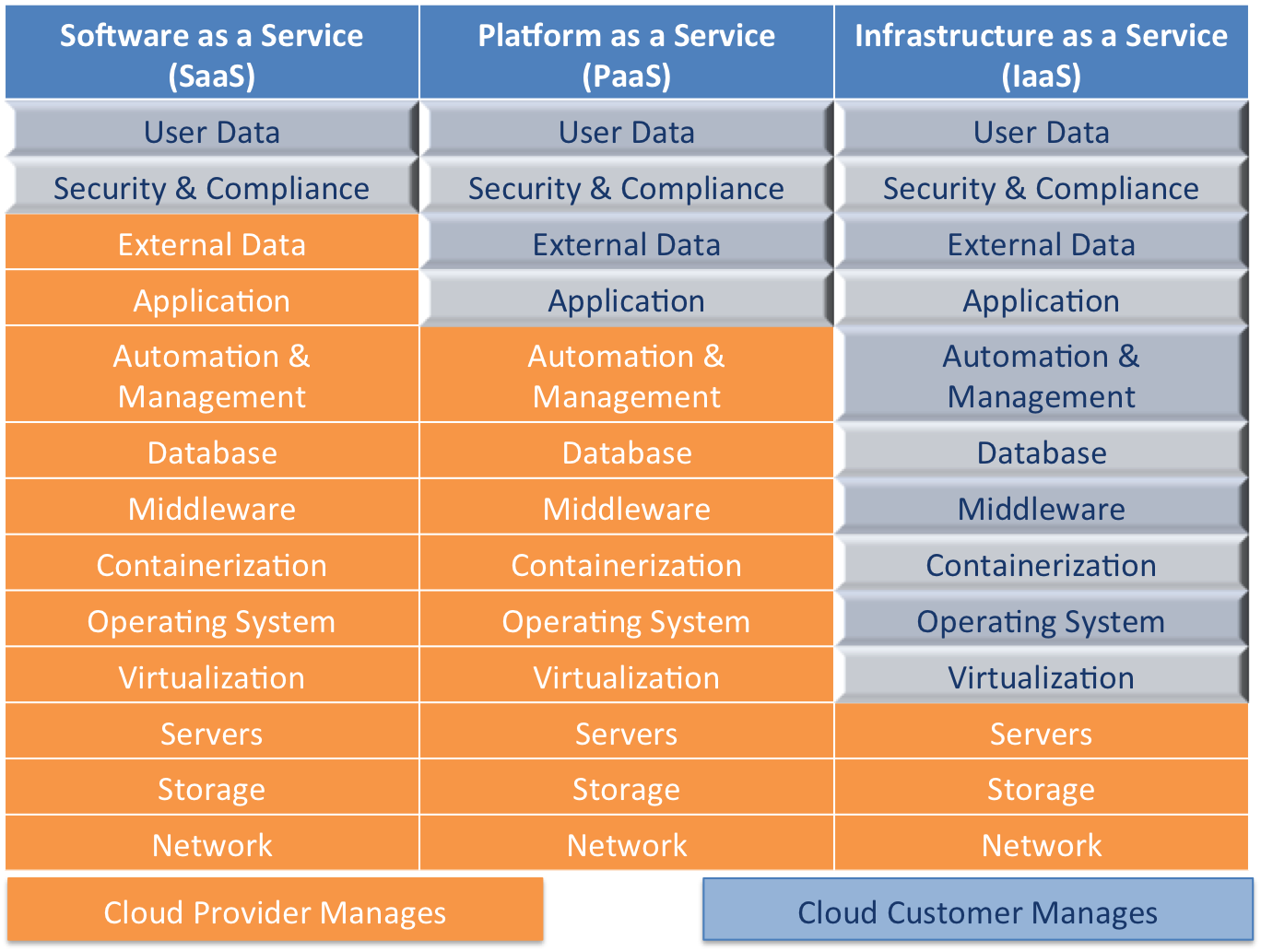

In this study, Wikibon is using the following as the definition (See Figure 2) of the architectural differentiation of SaaS, PaaS, and IaaS.

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

The operational distinctions between SaaS, PaaS, and IaaS are shown in Figure 2 and are described below:

Software-as-a-Service (SaaS)

- SaaS enables remote access of applications running as a cloud service, without directly provisioning or managing any of the middleware or infrastructure. Configuration is limited to user-specific configuration settings (e.g., bandwidth in and out of the cloud, performance tiers, data capacity, compliance report options, simple modification of input/output naming, etc.).

- SaaS runs on a fully integrated IaaS, either provided by the SaaS provider or sitting on an IaaS provider (e.g., AWS).

- The SaaS enterprise user is responsible for only user data, for security/compliance, and for managing specific configuration settings and managing service level agreements (SLAs).

- The advantages of SaaS for the user include lower investment and faster initial time to value, and faster access to application improvements.

- The advantages of SaaS for ISVs include lower support costs and faster time to value for both initial deployments and continuous updates.

- There are 100s of SaaS vendors including Salesforce.com, Microsoft Dynamics and O365, Cisco Webex, Workday, ServiceNow, Athenahealth, among many others. SaaS offerings by Oracle, IBM, SAP, and Cisco were primarily via acquisitions.

- Some SaaS providers such as ServiceNow and Saleforece.com via Force.com provide a PaaS service on top of their SaaS service (see PaaS below)

Infrastructure-as-a-Service (IaaS)

- IaaS provides enterprises with the ability to provision computing, storage, networking, and many other software services including database services, virtualization, load-balancing, security, development tools, automation, management and operations.

- Wikibon includes middleware and database services as part of IaaS, which leads to a clear distinction and definition illustrated in Figure 2 above. This is different from the definition used by some database vendors. If this becomes a significant segment, Wikibon will look at creating a separate segment of the public cloud market.

- The services are offered on demand or on a committed schedule.

- IaaS can be used to run application development, enterprise applications moved to the cloud and as IaaS services for SaaS providers.

- Examples include Amazon Web Services (AWS), Microsoft Azure, Google Compute Engine, IBM Cloud, VMware vCloud Air, Verizon Terremark, Rackspace and many others.

Platform-as-a-Service (PaaS)

- PaaS is a full application life-cycle cloud service, including initial development, testing, deployment, operations, and maintenance. It is well suited to modern continuous integration and delivery development models.

- PaaS (including IaaS) can be delivered as an integrated platform on public, private, and hybrid clouds, either integrated with an IaaS platform (e.g., Pivotal Web Services, IBM Bluemix) or as a feature on top of an IaaS platform (e.g., AWS Elastic Beanstalk).

- PaaS can also be delivered on top of a SaaS platform as a set of services which utilize the underlying SaaS and IaaS infrastructure (e.g., Force.com on Salesforce.com).

- PaaS on IaaS and PaaS on SaaS are distinct and different deployment models. In addition, Business Process as a Service (BPaaS) is an emerging extension of PaaS on SaaS. Because of the small size of PaaS at the moment, Wikibon has combined these sub-segments. Wikibon will investigate in more detail in future research.

- The advantages of PaaS include quicker time to value and lower cost of development. The disadvantages include increased overhead and less control over performance and management of the underlying infrastructure layer.

- Examples of PaaS include Salesforce’s Force.com, Microsoft Azure, IBM Bluemix, Amazon’s Elastic Beanstalk, Pivotal Cloud Foundry, Google App Engine, Red Hat OpenShift, Apprenda, Apcera, Heroku, and others. Wikibon’s PaaS definition excludes standalone development services (DBaaS, testing, Middleware-as-a-Service) that are not part of a total Public Cloud application development bundle.

Why Public Cloud?

Simply put, “Cloud computing allows computer users to conveniently rent access to fully featured applications, to software development and deployment environments, and to computing infrastructure assets such as network-accessible data storage and processing” (NIST)

While all forms of cloud (and legacy solutions for that matter) have their place, the unique value of Public Cloud (as opposed to Private and Hybrid Cloud) is characterized by:

- On-Demand usage and pricing

- Global reach

- High scalability

- Resource elasticity

- Rapidly growing set of features and services

- Capital cost avoidance

- Access to realtime and continual online application upgrades

- Ability to rapidly deploy new applications

Public Cloud Trends and Dynamics

Public Cloud revenue will grow by 20% annually to $493B 2026 (Figure 1). Each Public Cloud segment will be growing by double digits compounded annually in this period – PaaS (36% CAGR), IaaS (19%), and SaaS (18%).

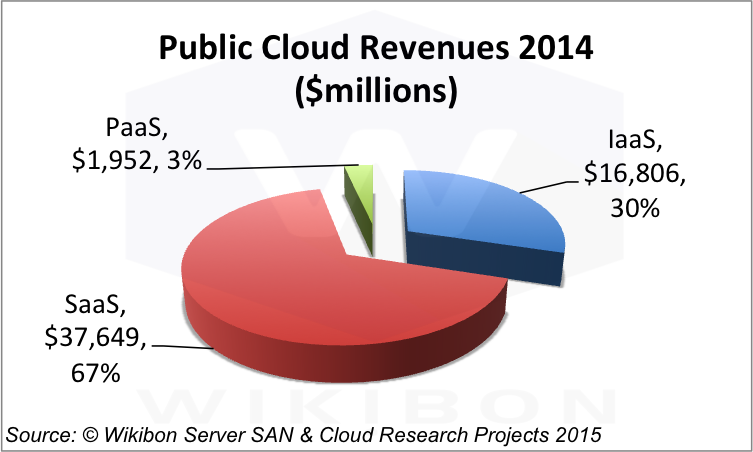

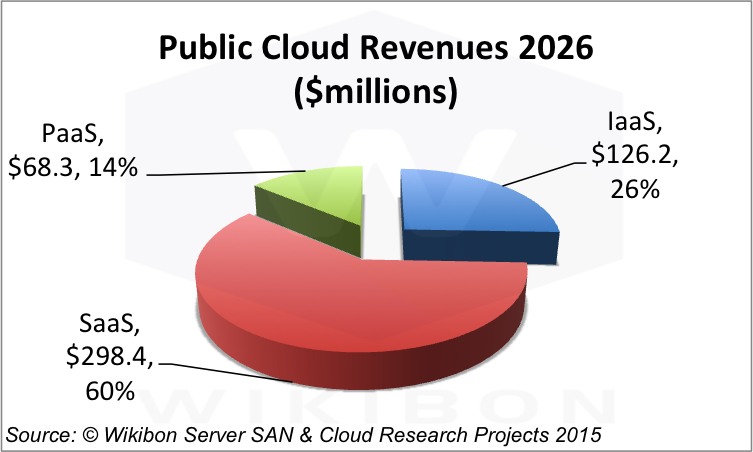

Figures 3 & 4 show the composition of the Public Cloud Market in 2014 and 2016.

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

The market will continue to be dominated by SaaS offerings through 2026. However, IaaS and PaaS together will be growing faster in the 2020s than SaaS – which will begin to reach the asymptote of the historical growth rate of licensed application software. Growth will be driven by the increasingly lower costs of infrastructure and staffing requirements, resulting in higher levels of investment in actual business applications delivering business value. The barrier will primarily be the ability of application software providers to deliver more value to support vertical market-specific and complex and large scale applications including in-line analytics. We might expect to see more private and hybrid cloud in those types of environments.

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

Wikibon believes Public Cloud PaaS is a small market today since enterprise development practices and the current tools are obstacles to widespread adoption. Saas platforms such as Pivotal’s Cloud Foundry are

However we expect these barriers to be overcome allowing Public Cloud PaaS to accelerate in the 2020s. Therefore, our PaaS forecast includes a significant amount of IaaS in the out years.

PaaS and IaaS have a significant amount of technology overlap, which is difficult to disentangle. Depending upon where it is counted, IaaS has more growth to it in the 2020-2026 time frame than we’re showing owing to its being coupled with our PaaS figures. Together, they will grow 23% compounded annually through 2026 as a function of the economies of rapidly building and deploying extensions to existing applications and deployment of new applications that create additional services and business value.

Major Public Cloud Trends

Public Cloud revenue growth is a function of a many factors and trends – including user requirements, technology capabilities, Private Cloud and legacy alternatives, as well as the uncertainties related to market leadership.

- Users – Users are growing increasingly comfortable with both the advantages of Public Cloud and the quality of the available offerings. As a result, there are fewer barriers to adoption from fear, uncertainty, and doubt. Rather users are more often focusing on the clear benefits of various offerings and weighing them against the alternatives. Of course, governance, legal and security considerations are still real obstacles, but providers are ameliorating these objections with increasingly more robust tools and infrastructure.

- Application Users – Acceptance of public cloud for many applications and infrastructure services – Cross Industry workloads, Productivity, and data center services – is widespread today. These workloads tend to be routinized functions that cross all industries – with low levels of transaction rates, database size, and security considerations. In the case of SaaS, cross-industry apps with broad appeal that can support vendor investment to meet large market demand potential are leading the way. Productivity (content management, office applications, collaboration) are relatively low risk and have low infrastructure demands as well as broad market potential are seeing even more dramatic growth. Industry-specific business applications which have (by definition) less total market demand and are more likely to have constraints on performance and regulatory concerns are still in early into Public Cloud adoption, and will have a tougher time matching the growth of the other applications.

- IT Departments – Increasingly, IT Departments are embracing both point solutions (disaster recovery, storage archiving) as well as total infrastructure solutions (especially for SMBs). As confidence in Public Cloud solutions grows, more infrastructure services will be off-loaded to IaaS providers. IT Infrastructure and Application Hosters are also embracing cloud technology offerings as part of their solutions for mid-sized and large enterprises.

- Application Developers – While Public Cloud PaaS is still in its infancy relative to SaaS and IaaS, it is a good option for applications requiring a richer development environment (i.e., developing new mobile and big data applications) and for deploying SaaS applications that offer rapid, significant early business benefits. Hybrid Clouds are an alternative when existing workflows are the target of development.

- SMB – Many Small and Medium sized businesses have direct relationships with partners and resellers. Leading infrastructure vendors such as HP and Cisco are providing enterprise class cloud infrastructure architecture and tools to enable these suppliers to meet their SMB customers demand for quality Public Cloud offerings without replacing these trusted relationships.

- Regional Trends – The US has been the leader in Public Cloud adoption – as is usually the case for new technologies. Wikibon expects Public Cloud to gain traction in Western Europe and emerging markets as offerings become more localized and trusted.

- Technology – Technology has enabled Public Cloud to be successful, and continues to break down barriers that have limited the applicability of the Public Cloud for solutions. But, the rate of progress of Public Cloud penetration will be a function of these technology factors. Indeed, in many cases the advanced services in Public Cloud even today are more robust than in most data centers.

- Communications and networking will always be a challenge for Public Cloud-based applications. Data movement is always slow and costly and whenever it is a significant factor in workload execution, it will be a barrier to a Public Cloud solution.

- Big Data and Analytics – The Internet of Things (IOT) and in-line analytics will provide significant opportunities for Public Cloud – especially when cloud-based data is part of the input for a Big Data Analytic application. Enterprises are moving to Systems of Intelligence (see Wikibon’s Big Data research on this topic) which build and extend key business applications by mining customer engagement in real-time to anticipate and optimize their experiences. A single vendor data solution for building, integrating, testing, delivering, and operating this platform will bring it close to the target business service to optimize speed and value.

- Identity and Access Management – While this is likely to be a more significant problem for Hybrid Cloud, to the extent to which Public and Private Cloud live together under a Hybrid Cloud umbrella, this will be an issue.

- Consumer Public Cloud applications are being adopted by enterprise users. Facebook and Twitter marketing is beginning to penetrate enterprises. DropBox is another tool that enterprise users are adopting for their use.

- Service providers are drawing on complete solutions from arms merchants (Cisco, HP, etc.) who are offering mature cloud infrastructure offerings for service providers to deliver a mature level of Public Cloud service to enterprises and SaaS providers – especially for SMBs and specialized applications.

- Governance, regulatory compliance, and security will also be considerations for users. To the extent to which these problems are solved by providers will provide a boost to market growth.

- Other Cloud approaches will compete with Public Cloud as a delivery method. These clouds can be deployed on premise, or increasingly in mega-datacenters, so that they can be physically close (and use much cheaper internal communication rather than telecommunication suppliers) to other cloud services.

- Private Cloud – Private Cloud is often the cloud deployment method of choice, especially for enterprises with skills and capabilities to handle the requirements for effective deployment and management. Orchestration and automation are key characteristics of private clouds, enabling them to become an internal service to enterprises. Private Cloud makes sense, then, for enterprises especially with large scale and high performance workloads. It enables users to get many of the benefits of Public Cloud, while limiting their risk exposure and providing a gentler path to Public Cloud adoption for some of their workloads. To the extent to which private cloud offerings can deliver significant value and a similar cost structure, the pressure to look at public cloud will ease.

- Hybrid Cloud – Hybrid cloud is in its infancy today, but gaining significant traction. In the long term it is likely to become the cloud approach of choice as enterprises will be able to deploy workloads to the optimal cloud platform based on requirements. Orchestration, automation and cross-cloud management and compliance will be complex and needs to be handled carefully, but the flexibility and scalability potential of Hybrid Cloud approaches will be highly appealing in the long run.

- Market Direction and leadership – A market growing at 30%+ in the past few years has been “lifting all the boats” – including to some extent those of the traditional IT providers who continue to struggle with their Public Cloud strategies and offerings. One important factor in product or service acceptance by users is market leadership – where the leaders establish themselves as the bell-weathers and set market direction and standards for enterprises to follow. Outside of Microsoft, the Public Cloud market is being led today by pure play Public Cloud providers who are disrupting traditional methods of delivering IT services and solutions to users. Since it is unclear today which providers will win, enterprises are uncertain about who to follow. This is a constraint for users considering making large budget commitments today. With Public Cloud likely to comprise 33% of all replaceable IT spend by 2026, this uncertainty will be resolved in the next few years.

Software-as-a-Service Market

Application software is the primary driver of the business value delivered by information technology today. As a result, the Public Cloud SaaS market will grow from $39.4B in 2014 to $298.4B by 2026, 18% compounded annually. The trend for more Public Cloud SaaS spending is underscored by the rush to develop Public Cloud offerings for core ERP and cross industry products on the part of the leading software licensing vendors in that space (especially Oracle and SAP) to complement and significantly extend their acquired ERP SaaS offerings. Growth will remain steady and strong through 2026 – but SaaS will begin to near its asymptote of overall application software growth by the end of the period. The SaaS market is likely to remain highly fragmented – like the Application Software (license and cloud) is today.

The Public Cloud SaaS market today is very fragmented with 100s of participants in most segments of the application software market (See Figure 5 for a general breakout of the main segments). Cross Industry applications (Customer Relationship Management, Sales, Marketing, Human Capital Management, Supply Chain, Service Management, and Financial), productivity applications (Office, Content Management, Collaboration), and some Industry-specific industry offerings (Health Care, Manufacturing, Insurance, Transportation and Hospitality) are all growing dramatically. Even more than the Cross-Industry application software market today, the Industry-specific segment will always have a high degree of fragmentation. As a result, Cross-industry and Productivity applications will continue to be the leading segments of SaaS going forward, but we expect in-line analytics for business operations in the public cloud, including vertical solutions, to become more important in the 2020s.

Infrastructure-as-a-Service Market

The Public Cloud IaaS market will grow from $15.1B in 2014 to $126.2B by 2026, 19% compounded annually. In the latter part of the forecast period, a significant minority of IaaS will be absorbed into PaaS usages. Like the infrastructure hardware, software, and services markets today, the Public Cloud IaaS market will be less fragmented than SaaS. AWS, Microsoft Azure, IBM Cloud, and Google are the leaders today. However, infrastructure hosters and outsourcers like CenturyLink (Savvis), Equinix, Verizon Terremark, etc. are likely to migrate more of their offerings to Public Cloud-based models. Offerings from Cloud arms merchants like HP and Cisco will enable enterprises and their partners to furnish cloud-ready offerings to SMBs and industry-specific solution providers.

Platform-as-a-Service Market

The Public Cloud PaaS market will grow from $1.7B in 2014 to $68.3B by 2026, 36% compounded annually. This market is still in its formative stage and includes 3 classes of providers – all with different perspectives and market entry points.

- PaaS from an IaaS provider – Amazon Elastic Beanstalk, components of Microsoft Azure, components of Google App Engine are examples here. This approach offers excellent integration with the underlying IaaS platform, rapid migration from test to production, and good vendor support. On the other hand it enables platform lock-in, has limited extensibility, may not support hybrid clouds, and skills may not be very portable.

- PaaS from a SaaS provider – Salesforce.com Sales Force1, ServiceNow Service Automation Platform, SAP HANA Cloud Platform are examples of these. This approach (of course) offers excellent integration with the underlying SaaS platform, a rich set of platform-specific tools, rapid deployment, and good vendor support. However, performance can be problematic, and these tools may not be appropriate for general purpose use. Platform lock-in may be a risk. Skills may not be portable.

- PaaS from a Development Environment provider – IBM’s Bluemix, HP’s Helion Development Platform, Pivotal Software’s Cloud Foundry are examples of these. As shown in Figure 2 above, this approach supports a DevOp IT structure and This approach is characterized by flexibility to deploy easily on a supported infrastructure platform and supports a wide range of languages and management tools. There is a risk of platform lock-in and does encourage good skills portability. This approach may be a good one for hybrid clouds.

Action item

Public Cloud is a rapidly growing technology that will continue to disrupt nearly every traditional IT market and deliver significant value for many workloads. Line of Business Executives will control more of their IT-driven business processes. IT Executives will continue to offload as many routine IT functions as practicable to the Public Cloud. Application Developers will use the public cloud to rapidly extend current apps and create new ones that will impact business processes and value. Enterprise actors – both business and IT – need to be actively engaging in leveraging the Public Cloud today and planning a strategy for a technology that could make up 33% of their external technology spending budget by 2026.

At the same time, enterprises should be wary of over-commitment to any one Public Cloud vendor. Rather they should establish an adaptive strategy that exploits the best of today’s Public Cloud offerings while hedging their bets to leave open the space to move to alternative platforms as their needs and the market itself continues to develop.

Appendix A: Cloud Definition

Users and vendors have varying definitions of what they mean by “Cloud”. For consistency, we have mapped our Public Cloud definition to conform to the NIST definition (from Wikipedia). The National Institute of Standards and Technology‘s definition of cloud computing identifies “five essential characteristics” which Wikibon adheres to in this study:

- On-demand self-service – A consumer can unilaterally provision computing capabilities, such as server time and network storage, as needed automatically without requiring human interaction with each service provider.

- Broad network access – Capabilities are available over the network and accessed through standard mechanisms that promote use by heterogeneous thin or thick client platforms (e.g., mobile phones, tablets, laptops, and workstations).

- Resource pooling – The provider’s computing resources are pooled to serve multiple consumers using a multi-tenant model, with different physical and virtual resources dynamically assigned and reassigned according to consumer demand.

- Rapid elasticity – Capabilities can be elastically provisioned and released, in some cases automatically, to scale rapidly outward and inward commensurate with demand. To the consumer, the capabilities available for provisioning often appear unlimited and can be appropriated in any quantity at any time.

- Measured service – Cloud systems automatically control and optimize resource use by leveraging a metering capability at some level of abstraction appropriate to the type of service (e.g., storage, processing, bandwidth, and active user accounts). Resource usage can be monitored, controlled, and reported, providing transparency for both the provider and consumer of the utilized service.

Of course, users and vendors may not be so exacting in their internal definitions of what “cloud” means to them. However, we are confident that our data closely correlate to the definitional framework above.

Appendix B: What We’re Counting

Wikibon counts Public Cloud revenue in the following manner:

- Public Cloud only – Professional services, advertising-related, and other spending is excluded from this report. Advertising revenue may indeed become a factor in public cloud spending in the future, and Wikibon will consider including advertising revenue if and when it becomes a factor in how Public Cloud services are paid for.

- Enterprise and Consumer Spending – The overwhelming proportion of Public Cloud spending today is by enterprises. Wikibon expects that consumer-related cloud services – i.e., productivity, collaboration, content management, marketing-related from vendors like Facebook and Twitter – will need to be enterprise standard, and will be included in Public Cloud in the future. Wikibon will monitor this trend closely.

Appendix C: Public Cloud Sizing and Forecast Methodology

This forecast is based on a variety of interlocking inputs and points of calibration and can be updated quarterly to reflect changing market conditions, Wikibon has drawn on a wide variety of sources to establish this Public Cloud Sizing, Segmentation, and Forecast.

- Worldwide Cloud Spending Sizing and Forecast – Our growth and penetration rates for Cloud for each segment are built up from reported revenue of ~100 lines of business for cloud providers. In some cases, Wikibon analysts have applied intelligent estimates where the vendor is important and the published data is ambiguous. This approach has been made easier over the past year as many more of the largest vendors are reporting Cloud revenue.

- Sizing Cloud Segment Revenue – Wikibon has conducted surveys of Cloud users to gauge the applications and use cases. We have applied this data to our working revenue models to calibrate the segments where spending is strong today and where users are intending to expand their cloud use cases and spending in the future.

- Wikibon Expert Analysis – Most importantly, Wikibon has drawn on its expert analysts to calibrate the near term data and to create a vision of where the cloud market is heading based on their knowledge of users, vendors, and the technology evolution that will continue to press Cloud into more and more varied usage scenarios.

- Underlying Worldwide IT Spending Forecast – Lastly, our growth and penetration rates are calibrated against a WW IT Spending market model that is based on publicly reported quarterly financial data and a protocol of statistical trend analyses to estimate the likeliest revenue outcomes for the forecast period for each of ~ 150 vendors and reported business units (in the aggregate covering 45% of all WW IT spending). The approach assumes that — in the aggregate — leading vendor financial reports provide good guidance for the market’s overall growth rate. The data is weighted and aggregated for each IT industry segment within which Cloud spending occurs so as to ensure our growth rates make sense in terms of rates and degree of penetration vs. available spending.

Appendix D: Wikibon Public Cloud Forecast Philosophy

A famous economist once said, “If you don’t forecast well, then you should forecast often.” Given the turbulence that Cloud is creating in the IT Market today, the Wikibon methodology takes this advice seriously. Wikibon will be tracking Public Cloud trends on a quarterly basis and will provide a formal semiannual report update as well as research notes quarterly that will comment on significant changes as they unfold.

This approach enables our forecasts to incorporate up-to-the-minute, auditable data to maintain running forecasts that can be recalibrated to reflect new information and real market trends.