Premise

Server SAN continues to grow fast, and is projected to replace most traditional storage arrays by 2026. Wikibon projects Enterprise Hyperscale Server SAN will migrate to True Private Cloud (TPC) Server SAN. Wikibon also projects that True Private Cloud Server SAN will make some headway together with Hyperscale Server SAN in public cloud storage.

Definitions for the Wikibon Server SAN classifications are provided in the Appendix at the end of this research report.

With contributing authors Ralph Finos, Stu Miniman, and Peter Burris.

Executive Summary

The Age of SAN Storage

Prior to storage area networks (SANs), storage was directly attached to servers. This led to high costs for stranded storage and under-utilized servers, as well as high costs for moving data around between servers to meet growth and performance challenges.

SANs are now the backbone of most IT installations. Almost all traditional storage arrays in SANs have proprietary storage controllers running proprietary software to manage storage attached to those controllers. Servers attach to the storage controllers, usually through a storage switch. The storage controllers run the majority of the storage management software.

Why Server SAN

Server SAN is cheaper to install, maintain and upgrade that traditional storage SAN arrays. Server SAN has storage software running on system servers, managing directly attached storage or JBOD/JBOF. Both the storage and storage management software runs on a network of system servers, allowing storage and servers to be scaled independently.

Server SAN offers much higher performance that storage arrays. It enables point-to-point communication with consistent low-latency high-bandwidth connection between any application and any data source. This is the UniGrid architecture, and is a focal point for Wikibon research. Wikibon believes that performance potential is the single most important strategic reason for migrating to Server SAN, and will be a prerequisite for real-time analytic systems and AI supporting systems of record.

Server SAN Projections

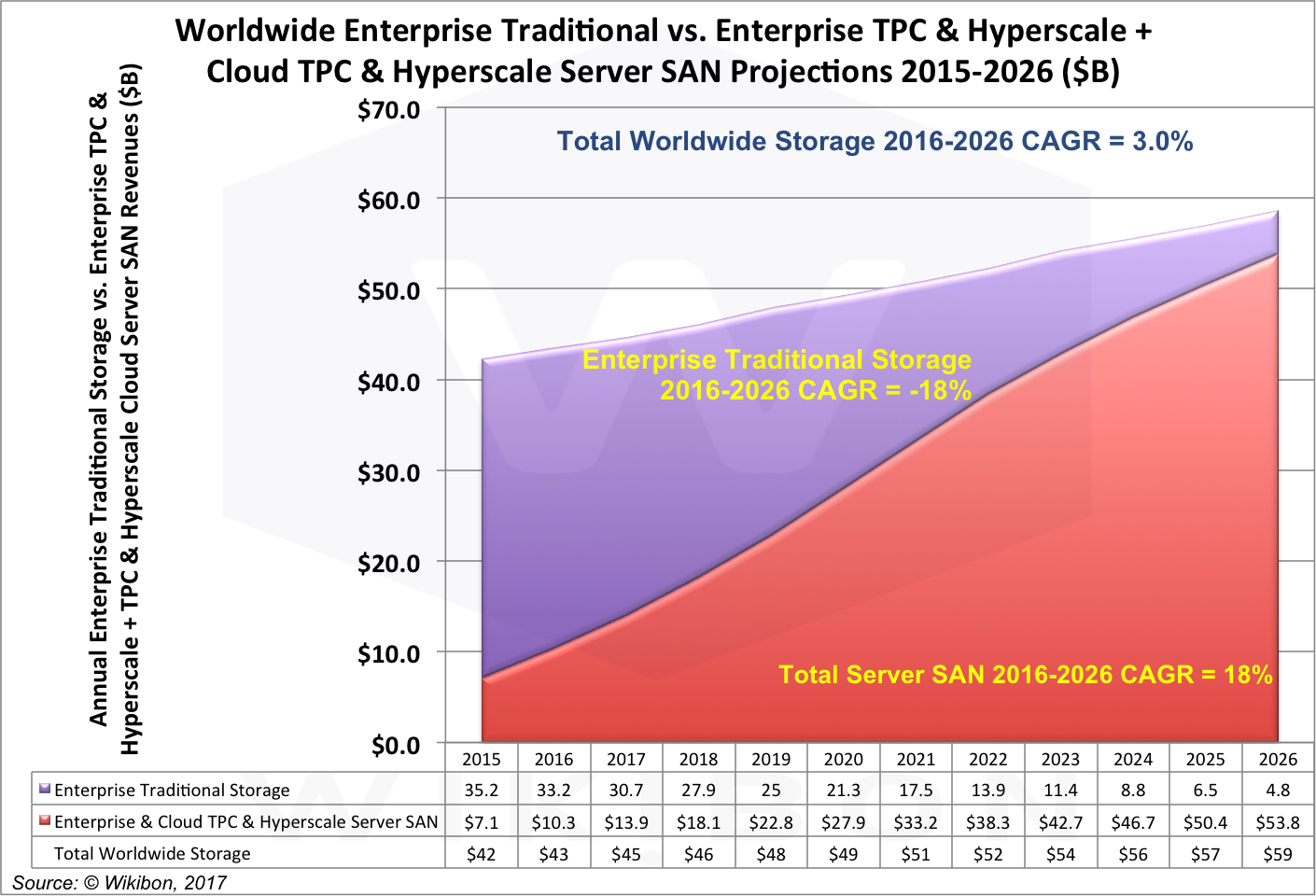

Figure 1 below shows the the Wikibon projections for traditional storage (mainly SAN and NAS) declining at about -18% CAGR. In contrast, the combination of enterprise Server SAN (including Server SAN on Enterprise True Private Cloud and Enterprise Hyperscale Server SAN) and Cloud Hyperscale Server SAN is projected to grow at 18%. The overall growth in storage is projected to be about 3%.

The main reasons for this migration to Server SAN are cost and performance. This is especially true as flash storage takes an increasing percentage of the spend both in enterprises and in the cloud.

The main inhibitors to the growth of Server SAN are software functionality and the cost of migration from storage arrays. These are areas of significant investment by platform vendors and many new entrants. Wikibon is keeping a close eye on potential developments in this area. Wikibon sees the Server SAN software functionality growing rapidly, with a trend to offload this functionality to ARM processors within both SSDs and networking fabric. There will also be a trend to move basic software to firmware in both the storage and networking fabric, which will allow easier integration into hyperconverged and hyperscale environments.

Source: © Wikibon 2017

Server SAN and True Private Cloud

Cloud Server SANs have been implemented mainly in hyperscale configurations for public cloud deployments. However, Wikibon projects that enterprise systems, at both the Edge and on-premises, will migrate to True Private Cloud (TPC) as the main topology. The major reasons driving this are the reduced cost of managing, securing, recovering and updating on-premises systems, as well as the emergence of new system architectures such as UniGrid with tremendous performance advantages. See Figure 3 in a later section for details.

Wikibon also sees that TPC will be chosen for some public cloud deployments, growing from 3% of revenue in 2015 to 17% in 2026. See Figure 4 in the sections ahead for details of this change.

Note. The definitions of converged, hyper-converged, traditional enterprise storage, enterprise hyperscale, True Private Cloud, and cloud hyperscale classifications of storage are provided in the Appendix at the end of this research report.

Server SAN in 2016

Server SAN Revenues

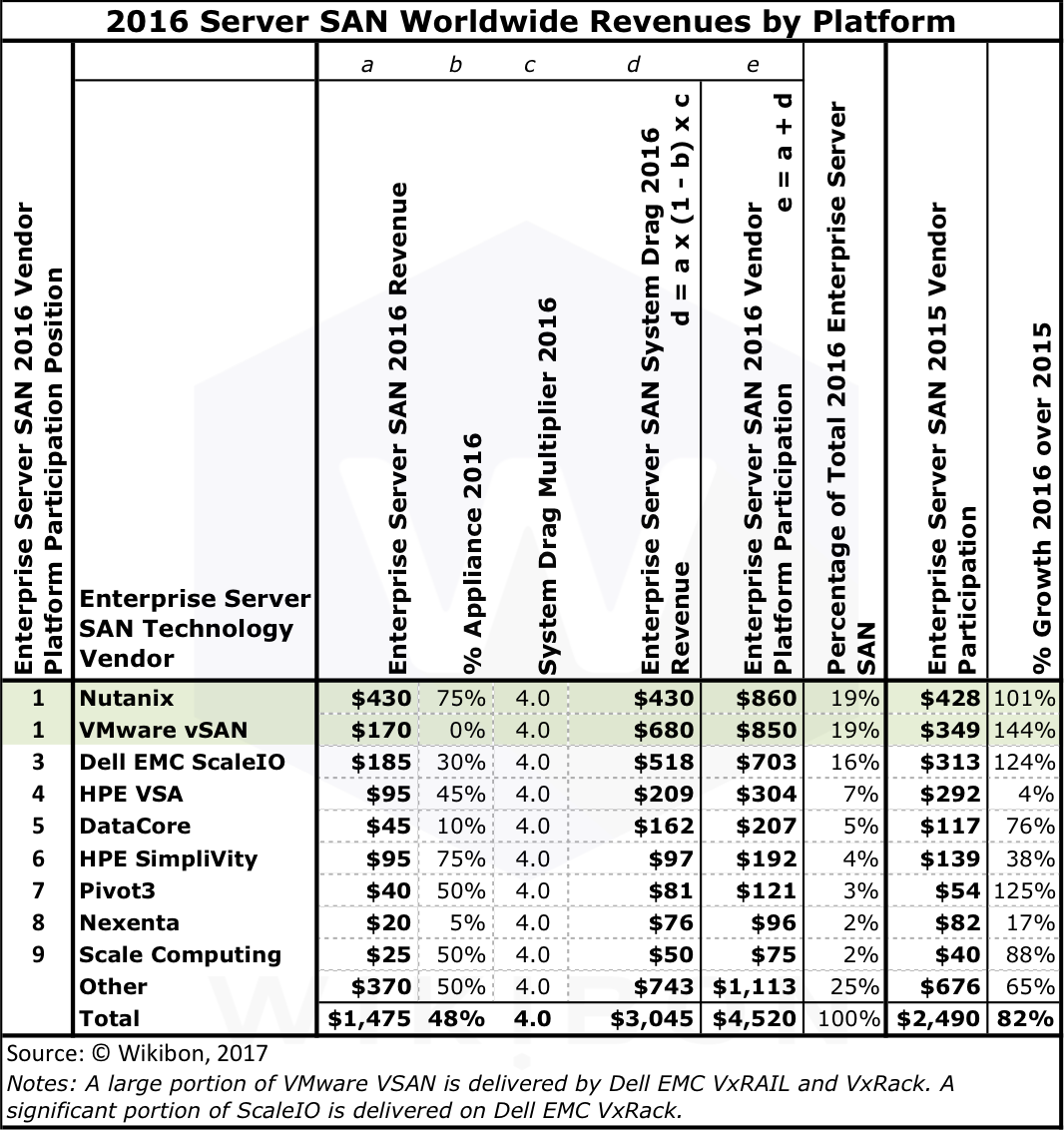

Table 1 below is a summary of the major platforms supporting Server SAN. The 2015 numbers in the last Wikibon report are slightly lowered in a restatement of 2015 figures in the penultimate Table 1 column. 2016 showed a healthy increase of 82% (see last column) in revenue, from $2.5 Billion in 2015 to $4.5 Billion (column e) in 2016.

Column a in Table 1 shows the direct software and hardware revenue for each vendor. Column b shows the percentage of this revenue from appliances. The software only component of revenue is multiplied by the system drag coefficient in Column c and the resulting system drag is shown in Column d. The drag includes the server, networking and other software costs for implementing the storage Server SAN software that is not realized by the Platform Vendor. It does not include the application software or server costs which is not direct revenue that is realized by the Platform Vendor.

One factor in the overall increase is the general lowering of software prices for Server SAN. This factor, together with larger implementations, results in the drag (discussed above) being higher. Column c of Table 1 shows an estimated 4x in 2016 compared with 3.1x in 2015.

The Server SAN Vendor Platform Participation Revenue in Column d is the sum of the vendor revenue (Column a) and the system drag (Column d). The drag revenue is shared across many other hardware and software vendors and cloud service providers. These vendors are not listed as Platform vendors. For example, Nutanix has agreements with system vendors such as Dell EMC, Lenovo, and others. The software component is include the Platform Vendor revenue (column a), and the system vendor portion (from Dell EMC, Lenovo and others) of the revenue is included in the drag.

Source: © Wikibon 2017

Wikibon will take a look at the system vendors revenues within the system drag in more detail in the 2017 Server SAN Report.

Major Server SAN Platforms

Nutanix and VMware were in a statistical tie as the leading vendor Server SAN platforms in 2016, as shown in green shading in figure 1 above.

Nutanix continued strongly in 2016, doubling platform revenue to $0.9 Billion. Deals were struck with Dell, Lenovo and other vendors, which lowered the % of appliances sold directly in 2016. The Nutanix platform is a prime example of a True Private Cloud (TPC) platform, with Nutanix being responsible for all the undifferentiated management costs, including hardware, firmware and system software.

The largest increase in platform revenue comes from VMware’s strong push of vSAN. VMware partnered with Dell EMC and others, which has driven a 126% increase in platform revenue. VMware is moving towards TPC with Dell EMC VxRail and VxRack implementations.

EMC’s ScaleIO software has been deployed in very large configurations, because of its consistent performance at scale. EMC is building a strong enterprise hyperscale Server SAN and TPC Server SAN implementations with its VxRack implementations of ScaleIO.

Other Server SAN Platforms

SimpliVity has an advanced architecture, particularly in regard to keeping consistent copies of data at distance with very low data transport cost and low latency to consistency. If well managed, its acquisition by HPE should allow significantly higher sales in 2018 and beyond.

DataCore has the highest performance benchmarks, because of its unique very low overhead parallel IO implementation. Practitioners should include DataCore in RFPs for performance challenged workloads.

Pivot3 has the highest growth of all Server SAN vendors of 249%. The platform, born from enabling efficient digital capture of video surveillance, is highly efficient in storage costs, and is a well-integrated True Private Cloud.

The “Other” segment shrank slightly from 27% in 2015 to 25% in 2016. Wikibon warns that this may be under-recorded, given the increase in software implementations of file and object storage, and the likely growth of Server SAN solutions in the EU and China.

One vendor in “Other” that deserves special mention is Micron. Micron, together with Excelero and Mellanox, has integrated a version of UniGrid. This platform allows very-low latency any-to-any between hundreds or thousands of servers and flash storage, using NVMe over Fabric (NVMe-oF) technology. Watch a discussion of the business value potential from this technology when CIOs Trevor Schulze & Don Duet sit down with Dave Vellante & David Floyer at the Micron Summit 2017 in New York City, NY.

There are a number of other vendors in the file, object and block spaces that are bringing new ideas and software technologies to the storage marketplace. Datrium, Infinidat, and NetApp are three that Wikibon will cover in the 2017 review.

Breaking out the Server SAN Market

Cloud vs. Enterprise Server SAN

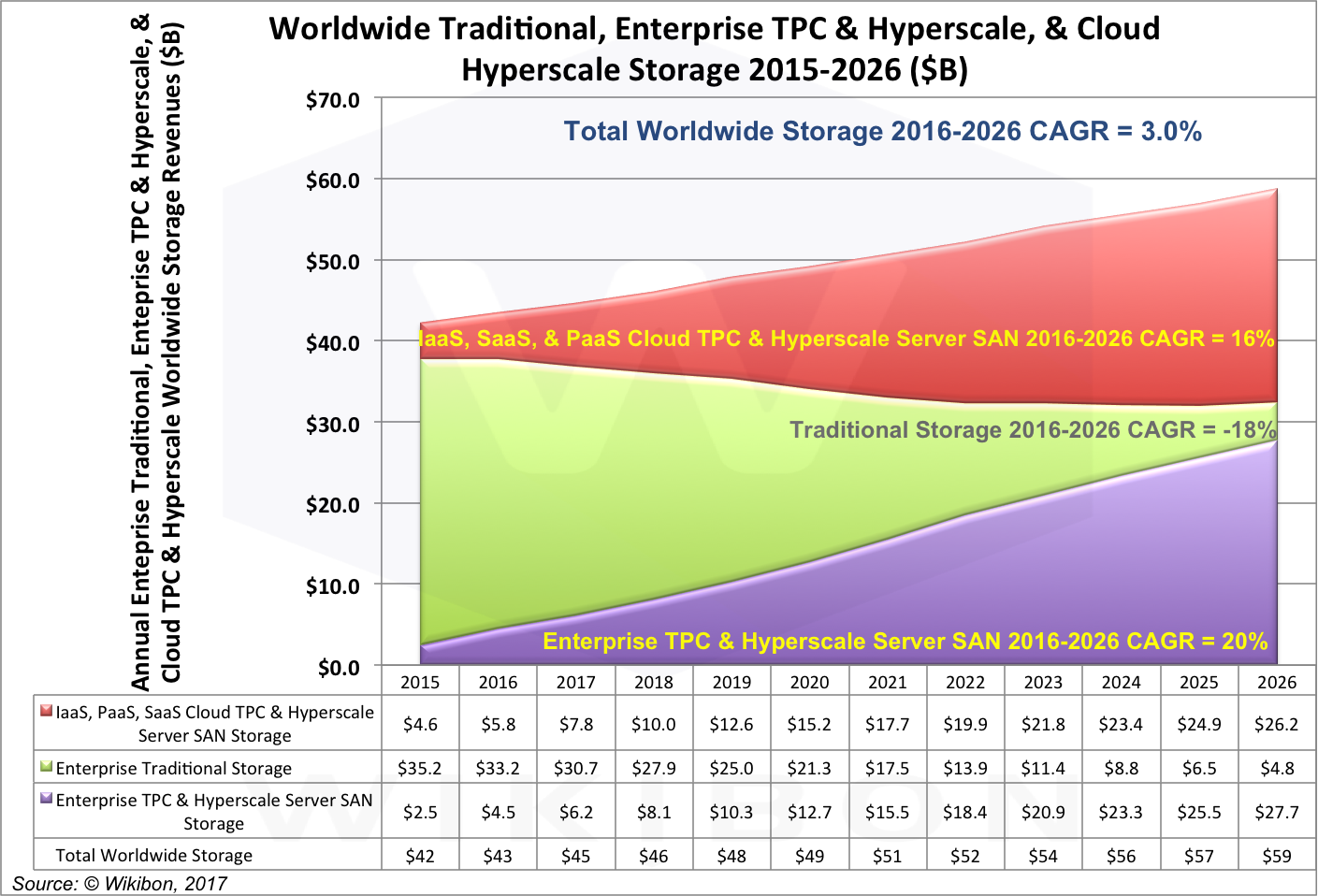

Figure 2 below breaks the “Enterprise & Cloud TPC & Hyperscale Server SAN” line in Figure 1 into two components, Cloud and Enterprise. The “Enterprise TPC & Hyperscale Server SAN Storage” line is at the bottom purple area of Figure 3, and the “IaaS, SaaS, & PaaS Cloud Server SAN Storage” is the top red area. Together, they are squeezing traditional storage shown in green in the middle.

Source: © Wikibon 2017

Enterprise Hyperscale vs. TPC

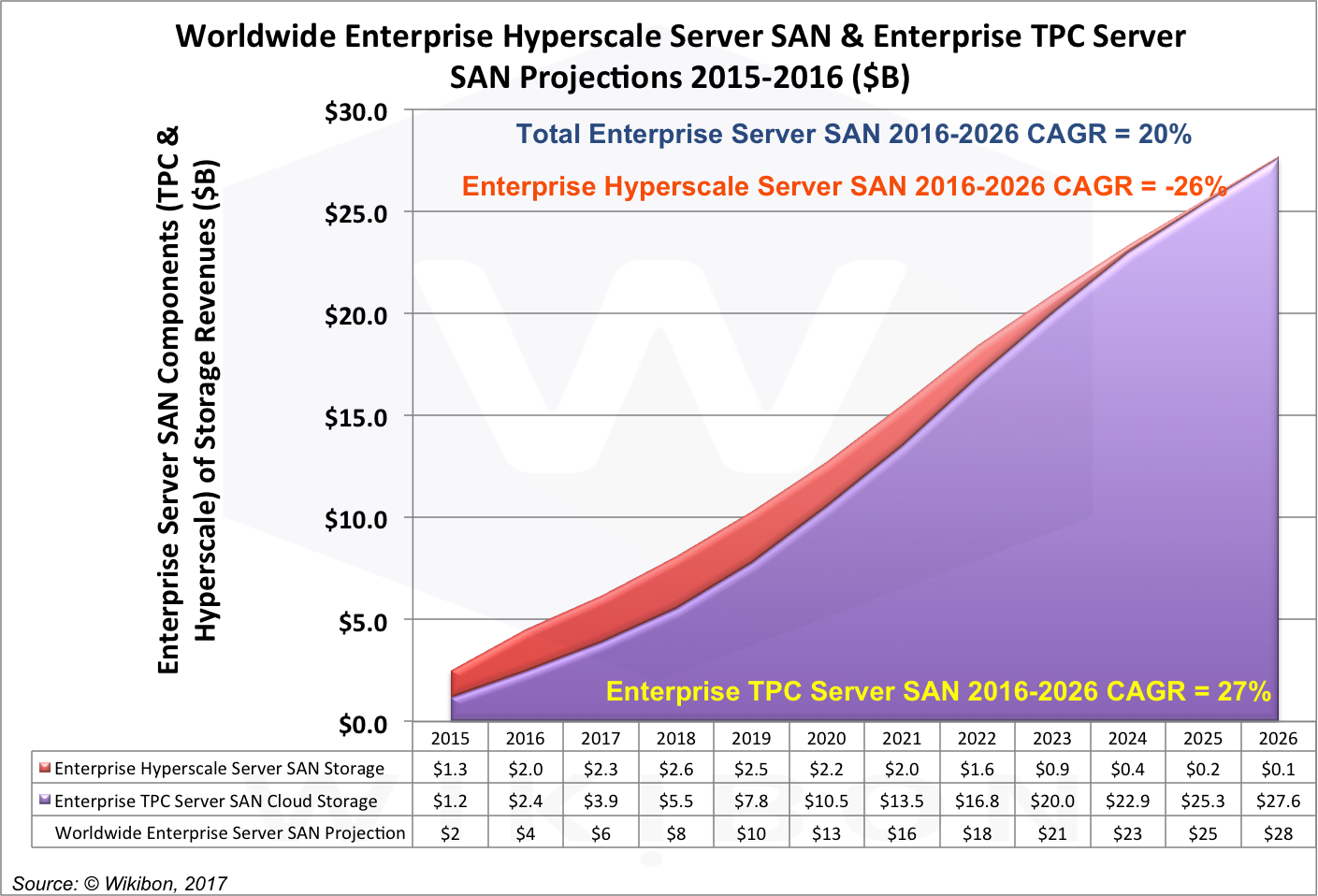

Figure 3 below takes the “Enterprise TPC Cloud Storage & Hyperscale Server SAN Storage” line from Figure 2 and breaks it into two components, Enterprise TPC Server SAN Storage and Enterprise Hyperscale Server SAN Storage. In 2015 and 2016 the emerging enterprise Server SAN market is equally divided between TPC (shown in purple) and hyperscale (shown in red). Wikibon believes that the cost benefits and time-to-value from software benefits of TPC will drive the enterprise on-premises market strongly towards TPC, as is shown in Figure 3 out-years.

Source: © Wikibon 2017

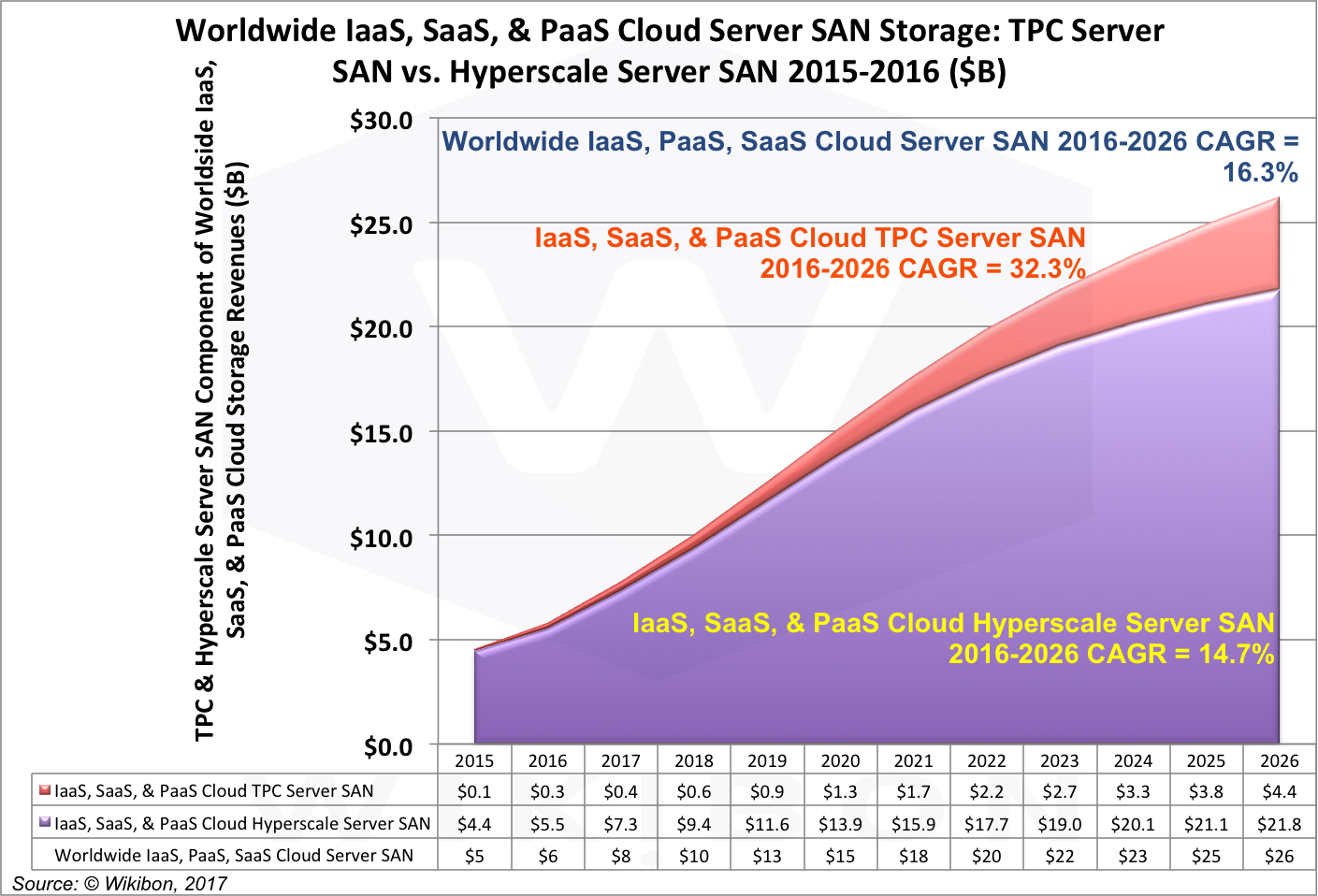

Cloud Hyperscale vs. TPC

Figure 4 takes the “IaaS, SaaS, & PaaS Cloud Server SAN Storage” line from Figure 2 and breaks it into two components, TPC and hyperscale. Hyperscale is very well established in cloud storage, especially in the major cloud vendors such as AWS, Microsoft, Google and IBM. The first three take piece parts directly from manufacturers and have all implemented their own Server SAN hyperscale software and integrated it into their cloud stack. Wikibon does not think this approach will change soon for the major players.

However, there is definitely room in other parts of the cloud market for users to take advantage of TPC economics without developing their own storage solution. Smaller cloud service providers, and in particular SaaS ISVs, are looking to buy solutions using a TPC architecture, and will include Server SAN as part of that TPC stack. Wikibon expects that TPC Server SAN shipments will grow from 3% in 2015 to 17% of a much larger market by 2026. The overall growth rate is projected to be a high CAGR of about 32%.

Source: © Wikibon 2017

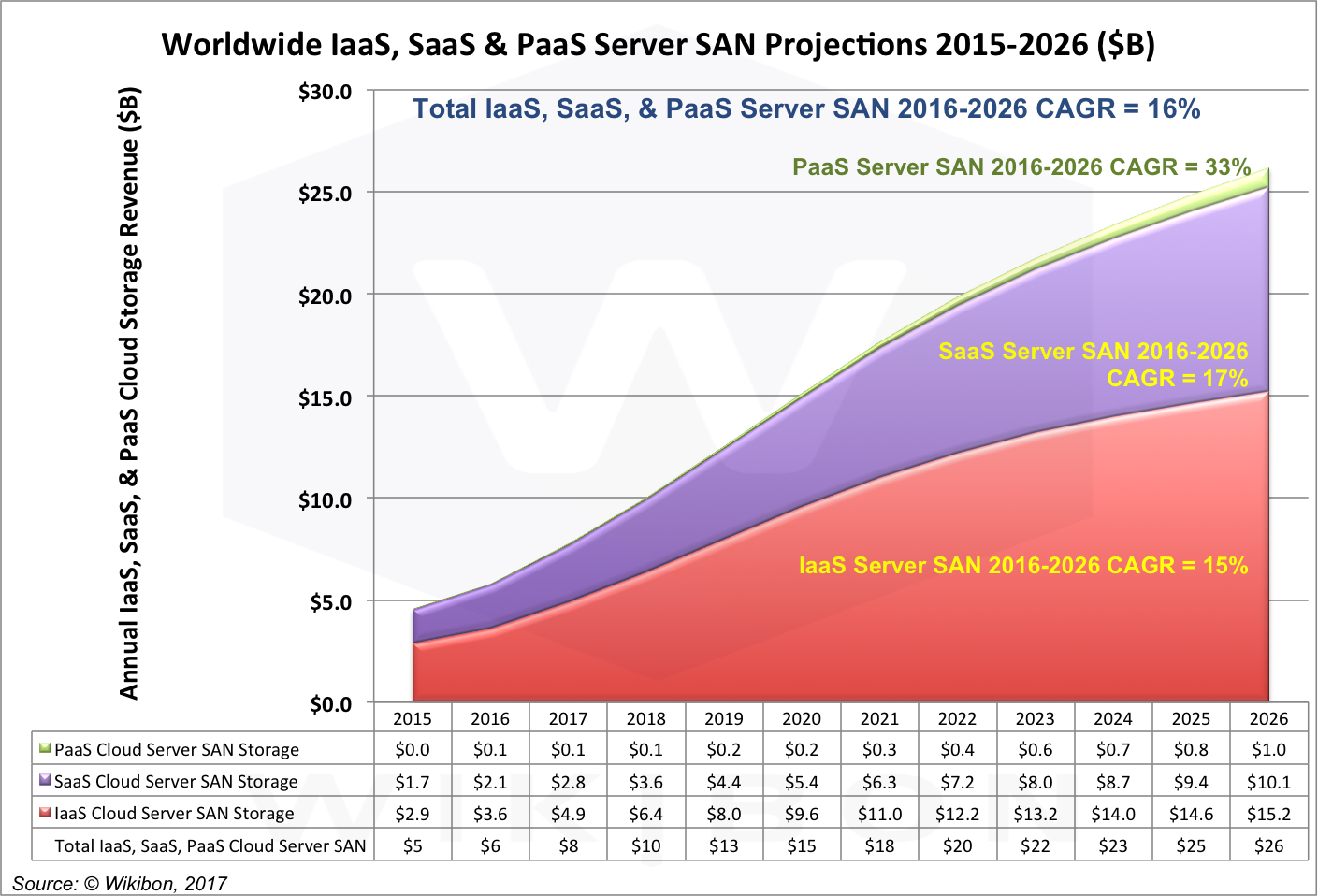

Cloud Storage for IaaS, SaaS, and PaaS

Figure 5 takes the same “IaaS, SaaS, & PaaS Cloud Server SAN Storage” line from Figure 2 and breaks it into the three different cloud components, Infrastructure-as-a-Service (IaaS), Software-as-a-Service (SaaS), and Platform-as-a-Service (PaaS). It shows IaaS in Red, SaaS in Purple, and PaaS in Green.

Source: © Wikibon 2017

Source: © Wikibon 2017

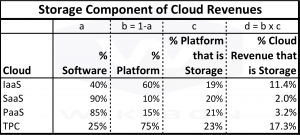

The cloud storage revenues in Figure 5 are derived from Wikibon’s Public Cloud Forecast and True Private Cloud Projections., Table 2 column d is used to calculate the proportion of cloud revenue that is storage.

Figure 5 shows that the largest cloud storage market is IaaS. However, this is also the portion of the market that is least available to vendors other than component vendors, direct storage vendors and ODC vendors. However the SaaS and PaaS markets have a much higher number of ISVs who may need high performance systems tuned to their software. Wikibon expects TPC to be implemented in these types of environment, as well as IaaS service providers for specific high-value market-places (e.g., Oracle Database).

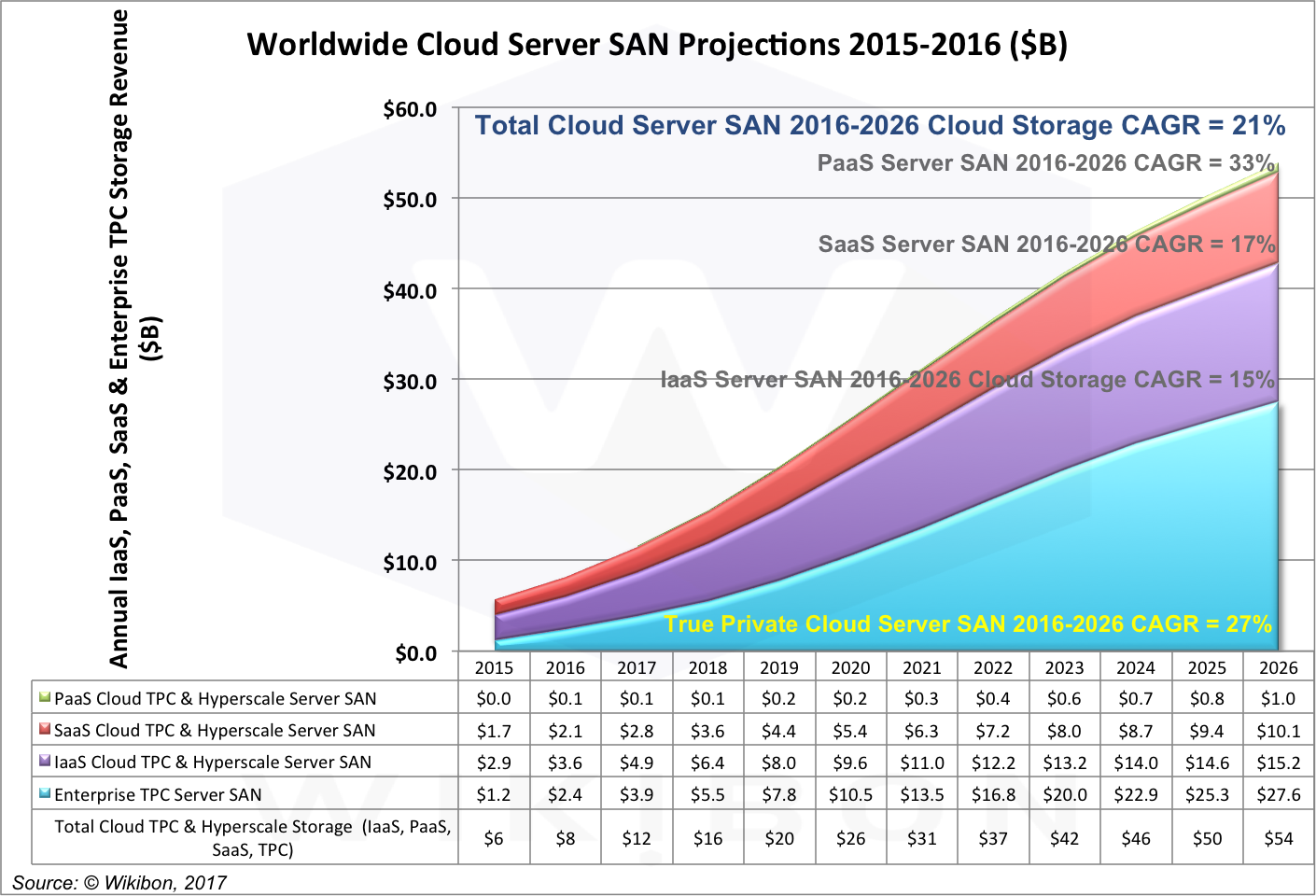

Cloud Storage for IaaS, SaaS, PaaS & TPC

Figure 6 takes the same “Enterprise and Cloud TPC & Hyperscale Server SAN” line from Figure 1 and breaks it into the four different cloud components. These are Infrastructure-as-a-Service (IaaS), Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), and True Private Cloud (TPC). Figure 6 shows IaaS Server SAN in Purple, SaaS in Red, PaaS in Green, and TPC in Blue. This projection shows that TPC will become about the same size as the IaaS, PaaS and SaaS markets by the middle of the next decade.

Source: © Wikibon 2017

Conclusions

Server SAN is projected to replace most of traditional storage arrays by 2026. Wikibon projects that most enterprise Server SAN will be deployed within True Private Cloud platforms. Hyperscale Server SAN will be the predominant public cloud deployments, although True Private Cloud Server SAN will also make some headway.

The main reasons for migration to Server SAN are cost and performance. This is especially true as flash storage takes an increasing percentage of the spend both in enterprises and in the cloud. It is cheaper to install, maintain and upgrade than traditional storage SAN arrays and offers much higher performance. Wikibon believes that the performance potential will be the single most important strategic reason for migrating to Server SAN. It will be an important prerequisite for real-time analytic systems and AI supporting systems of record without rewriting or migrating systems of record.

The main inhibitors to the growth of Server SAN are software functionality and the cost of migration from traditional storage arrays.

Action Item

CIOs and CTOs should define a Server SAN strategy for their on-premises infrastructure, and consider implementing it as part of an in-house True Private Cloud and multi-cloud strategy. In the meantime, CIOs and CTOs should plan to minimize migration costs from current storage platforms.

Appendix: Server SAN Classification Definitions

Wikibon’s definitions for converged, hyper-converged, traditional enterprise storage, enterprise hyperscale, True Private Cloud, & cloud hyperscale are:

- Converged – Originally systems like EMC’s VBlock, which was delivered as a single unit consisting of system/storage array mix. Other examples include NetApps FlexPod with Cisco. The piece parts and system software are maintained by IT. Initially this market grew rapidly, but has recently topped out.

- Hyper-converged – Systems with pre-tested and usually virtualized piece-parts. This system type is growing very rapidly. This term is often mis-used by vendors who sometimes label “converged systems” erroneously as “hyperconverged”.

- Traditional Enterprise Storage – This includes separately defined SAN storage, File Storage, Object Storage. It also includes traditional SAN-based Converged and Hyper-converged Storage.

- Enterprise Hyperscale – Systems with virtualized and software-defined compute, Server SAN software-defined storage, networking, with a common management. Examples include Nutanix, Dell EMC’s VxRAIL, Dell EMC’s ScaleIO, and Pivot3 offerings.

- True Private Cloud – Hyperscale Enterprise Systems where a vendor takes responsibility for delivering, maintaining and upgrading infrastructure, and manages an OEM relationship with hardware, system software and ISVs. Automation and orchestration features are provided. One example is Oracle’s Cloud Machine.

- Cloud Hyperscale – Separated compute, storage and network services, full set of API-driven services delivered in the public cloud. AWS, Microsoft Azure, Google, AliBaba, etc. are prime examples.

Orthogonal to the above is UniGrid – a new system architecture where the storage and network layers are separated out from the the compute layer and operate independently from compute (and in the future, compute and DRAM). Unigrid opens the door to ultra-low latency systems with multiple different architectures across hundreds and thousands of heterogenous processor nodes. UniGrid can be used as an architectural foundation for True Private Cloud, Enterprise Hyperscale and Cloud Hyperscale.