Contributing Analysts

Ralph Finos

David Floyer

Brian Gracely

Stu Miniman

Premise:

Wikibon believes that Public Cloud represents a quantum level of disruption to the manner in which IT Services are delivered to enterprises and users. As such, in order for in-house IT organizations to remain valuable and relevant to the business functions and processes they support, enterprises should consider delivering Private Cloud in the same light – that it should emulate the pricing, agility, low operational staffing and breadth of services of Public Cloud to the maximum degree possible.

Public Cloud has redefined the service levels and nature of the interaction between provider & user in a manner that will become the standard requirements for any enterprise that seeks to take advantage of “cloud” technology in their own data center. While virtualization and the deployment of incremental, “cloud-like” measures may be effective in the short term to reduce IT costs, Wikibon believes that enterprises considering deploying clouds within their data centers should leapfrog to a complete solution having the characteristics of Public Cloud as soon as possible in order to keep pace with the accelerating value proposition and agility that is Public Cloud. We’re naming this enhanced form of private cloud, True Private Cloud.

Wikibon believes that True Private Cloud will start delivering in greater volumes in 2016 as complete solutions with a single point of purchase, support, maintenance, and upgrades. These solutions will move almost all maintenance work to a vendor or systems-integrator.

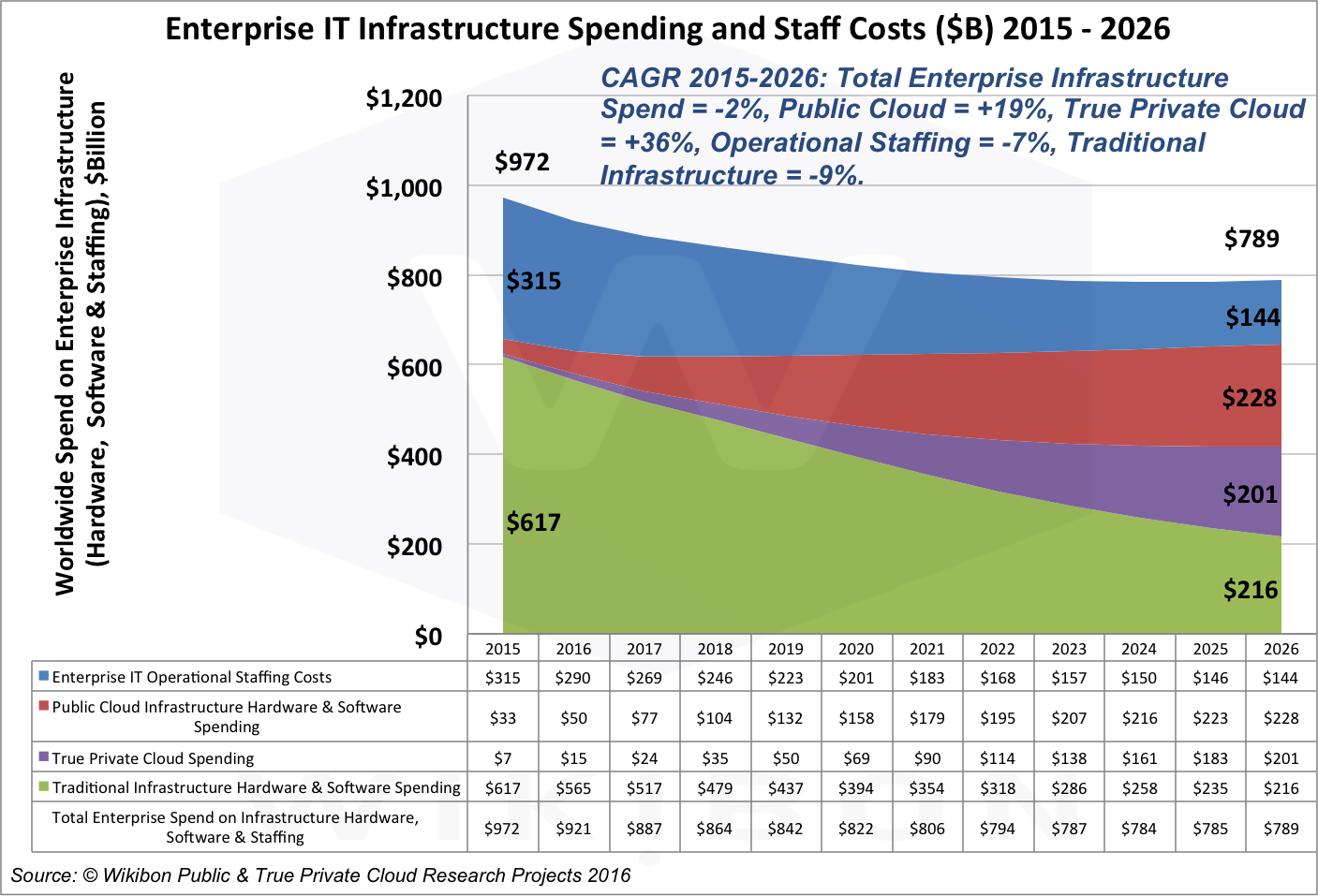

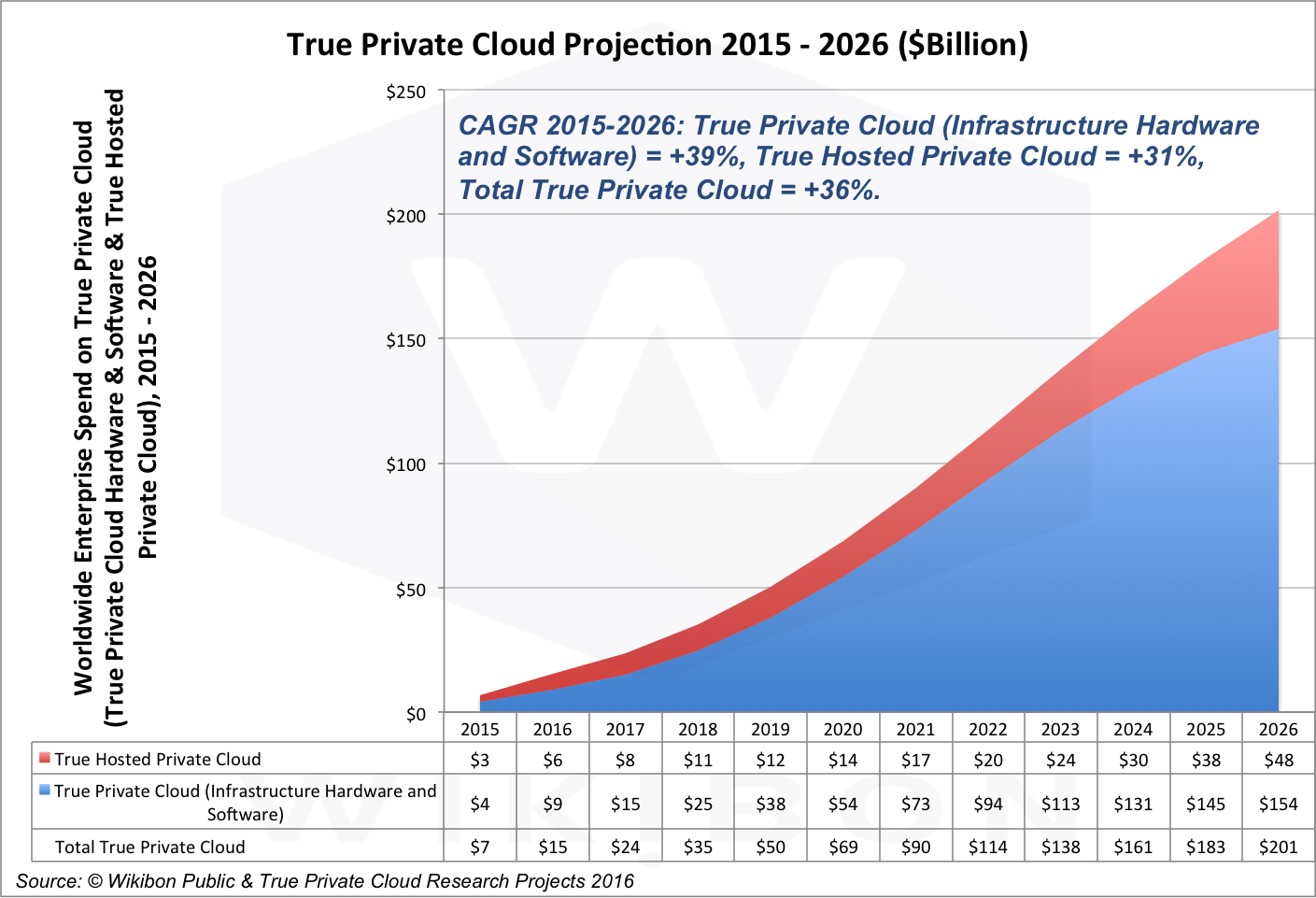

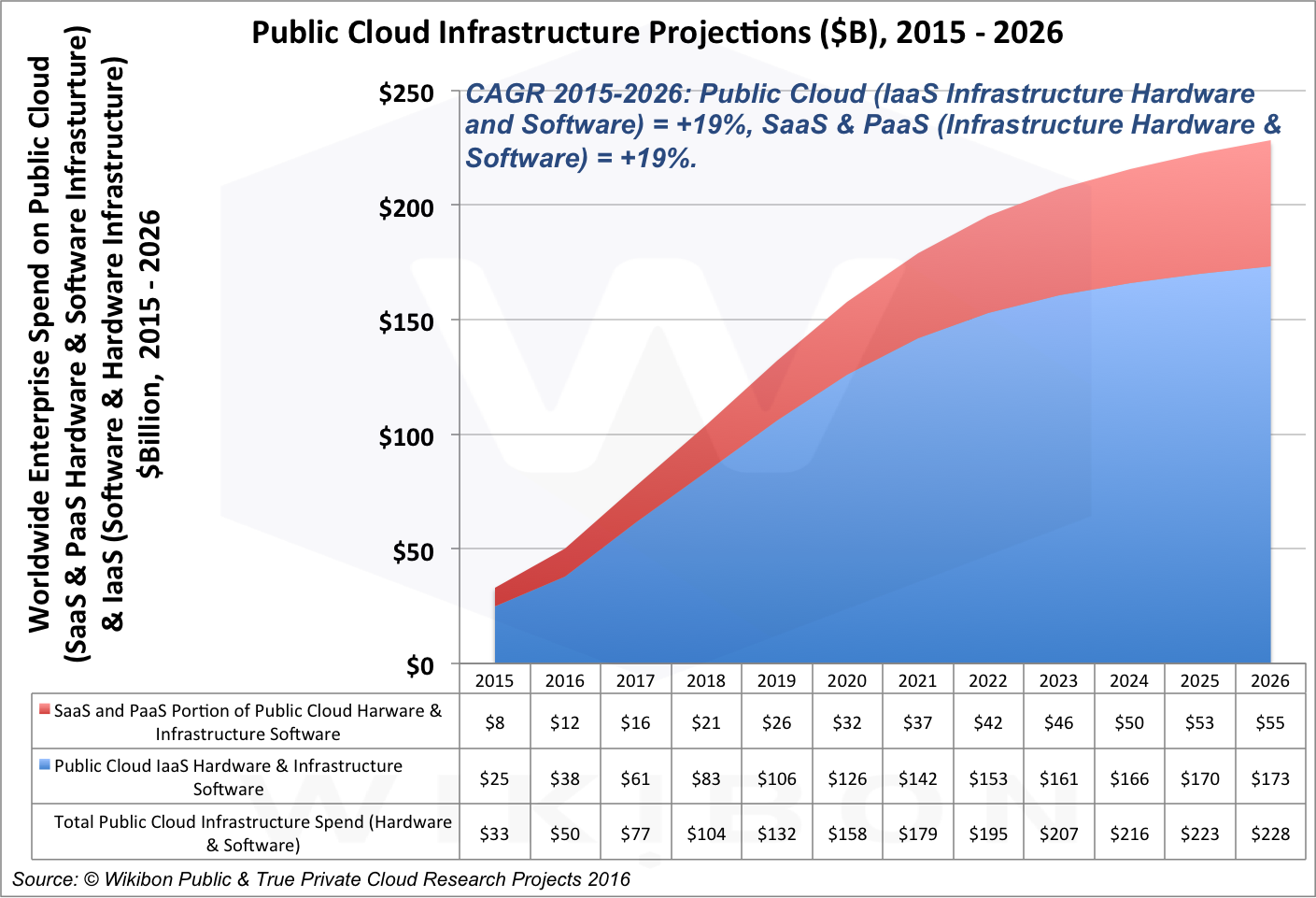

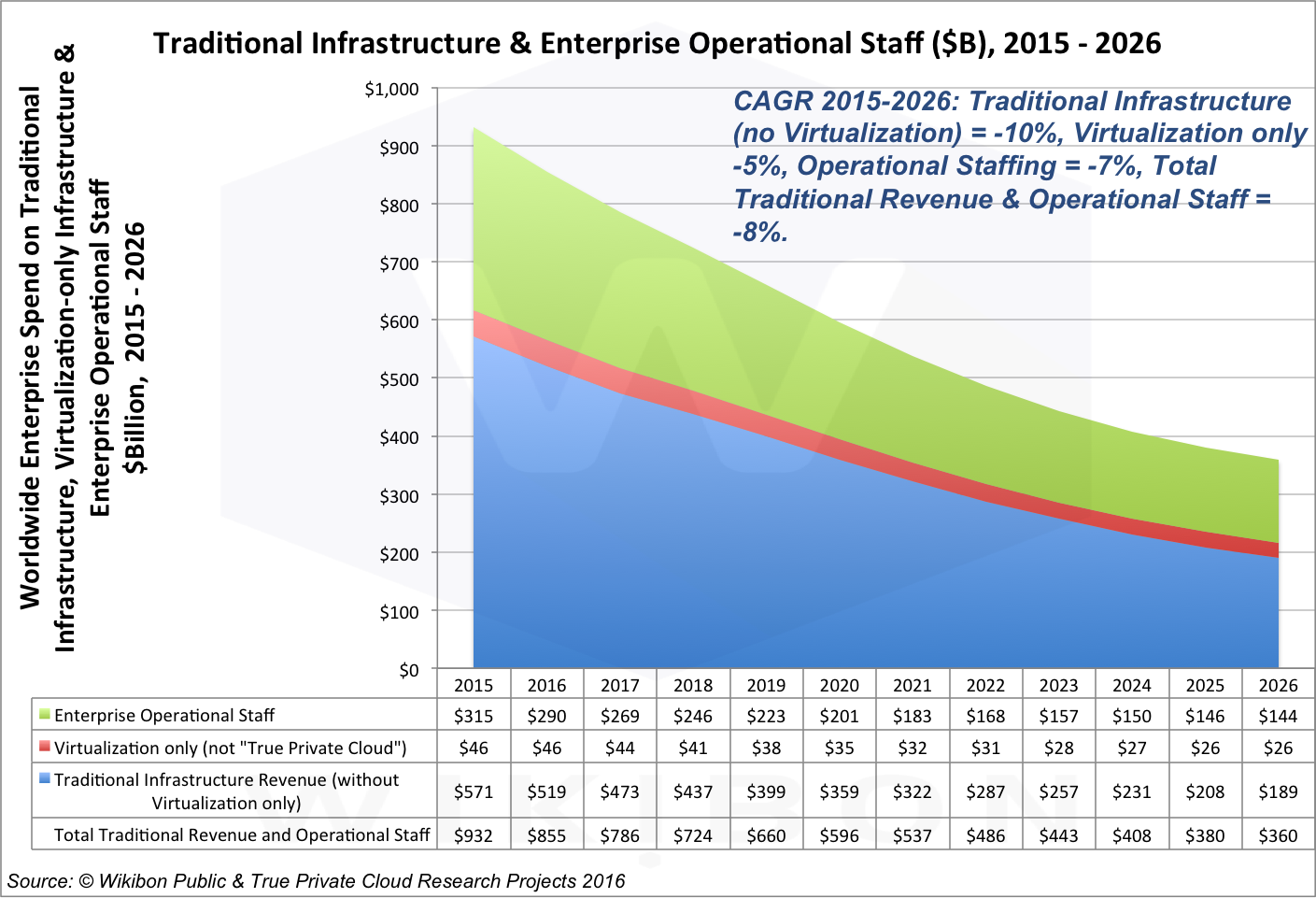

True Private Cloud (On-Premise and Hosted together) is expected to grow from $7B in 2015 to $201B in 2026 (36% CAGR), and be 31% of infrastructure spend. True Private Cloud is tracking 2-3 years behind Public Cloud. Public Cloud Infrastructure (IaaS and about 15% of PaaS and SaaS) is projected to become the leading method of providing infrastructure by that time (36%). Traditional Infrastructure Spending will decline from 96% of the total in 2015 to 33% in 2026.

NOTE: While Wikibon believes that the elements of a True Private Cloud will be available to the mainstream market in 2016, it is important to remember that many on-premises offerings do not include any elements of day-to-day Cloud Computing operations. If IT organizations are not able to accelerate the evolution of their skills or transition a larger percentage of their workloads to external Managed Private Cloud Providers, these forecasts could be significantly impacted in a negative manner. If IT organizations cannot evolve, the % of technology spending that uses Public Cloud resources will be grow at a rate that is much faster than current Wikibon projections. Wikibon expects that Public Cloud providers will deliver enhancements over the next 12-24 months that will significantly help reduce the current inhibitors to Public Cloud usage (e.g., Security, Performance, and Compliance/Regulatory). As this functionality improves, this will put greater pressure on IT organizations to deliver True Private Cloud services, or be bypassed by businesses looking for new solutions and reducing the cost of operations.

Source: © Wikibon Public & True Private Cloud Research, 2016.

Private Clouds and True Private Clouds

True Private Clouds are distinguished from “private cloud” in its current usage by the completeness of the integration of all aspects of the offering – including the performance characteristics (price, agility, service breadth), but more importantly the nature of the relationship with the Cloud supplier – single point of purchase, support, maintenance, and upgrades. While aspects of the performance characteristics (i.e., virtualization) are broadly available today and characterized as “private cloud”, True Private Clouds are only beginning to emerge as a distinct sector – primarily out of the Converged Infrastructure offerings (e.g., Cisco/NetApp Flexpod, EMC Vblock & Vscale, HPE Synergy, Microsoft Partner ECI, Nutanix, Oracle Engineered Systems, SimpliVity, etc).

While these products generally do not offer the totality of services today that we characterize as True Private Cloud, they are advanced building blocks along that path that Wikibon expects to rapidly evolve along that path over the next few years. For an example and discussion of the benefits of True Private Cloud, see a Wikibon case study of the business value of converged infrastructure.

Wikibon did hundreds of confidential in-depth interviews, and the Cube recorded hundreds of video interviews with senior executives from IT vendors and enterprise IT. More details of the methodology used are give in the appendix.

Wikibon True Private Cloud Definition

As such, True Private Cloud should incorporate the following characteristics of public cloud:

- True Private Cloud should significantly simplify the relationship between the user and the provider. That is, the user should have a relationship/transaction with a single provider, as is the case with public cloud. This can be realized in one or more ways:

- Through a foundation of converged (or hyper-converged) systems (i.e., VCE, Exadata, Flexpod, et alia) that are highly automated and managed as local pools of compute, storage, and network resources optimized to integrate the infrastructure (and ultimately applications) as a Single Managed entity where the user has a relationship with one provider, a “single throat to choke” as it were. We would include cases where the system is converged but where Level 2 software support may reside with another provider.

- Hosted managed private cloud (CenturyLink Private Cloud, CSC BixCloud, Cisco Metapod, Expedient Private Cloud, IBM BlueBox, Platform9, Rackspace Private Cloud, CenturyLink Private Cloud, et alia) would also be included in our definition. The chief characteristic of True Private Cloud in this case is its matching the customer relationship with the provider with similar efficiencies as provided by Public Clouds.

- True Private Cloud should allow users the flexibility to choose how IT resources are consumed – either “by the drink” or in a long term commitment. Whichever method they chose to pay their bills, the per-transaction cost of True Private Cloud should be transparent to the user.

- True Private Cloud should be designed to accommodate existing or future Hybrid Cloud application use cases.

- A True Private Cloud should be available on a self-service basis. Of course, the user can elect to pay for support from a provider if it useful, but there should be no requirement for permissions or provider intervention in order to use the service. Enterprises may impose rules of use of their own (say for access to hosted private cloud resources), and choose alternative charging practices (e.g., chargeback, show-back), but these would not affect how the user could interact with the True Private Cloud if they had license to.

In terms of levels of convergence to qualify as True Private Cloud, Wikibon prefers to see automation and orchestration including:

- Cluster management

- Network automation and management

- VM/container automation and management

- Storage automation and management

- Application templates and deployment tooling

- Operations dashboard

- Workload analytics

- Capacity optimization

- Log management

- Root cause analysis

- Remediation tools

- Configuration monitoring

- Proactive alerts

- Backup and replication services on premise or hybrid to other cloud services

- Snapshot management & catalog services

Managed/Hosted True Private Cloud

Managed/Hosted True Private Cloud includes offerings such as Cisco MetaCloud, Verizon Private Cloud, Rackspace Private Cloud, CenturyLink Cloud Managed Services, IBM Softlayer Private Cloud, IBM BlueBox, Internap Dedicated Private Cloud, Dell Managed Cloud Services, Platform9, et alia. These offerings, as far as the user is concerned, look and behave like a Public Cloud services except that under the covers, the resources are not shared across enterprises.

What our Definition Does not Include

Wikibon is taking a long term, disruptive perspective on the optimal end state that True Private Clouds should be reaching in the next decade to realize the full value of “cloud” if they elect to own their own cloud in their data center or via providers. As such the following are not included in our sizing or forecast of True Private Cloud.

- Converged Systems with limited orchestration and automation, i.e. not meeting the True Private Cloud convergence criteria above.

- Self-integrated private cloud or convergence involving numerous vendors. For example, Wikibon would regard the installation of VMware vSphere (or Microsoft HyperV) on new Dell or HP Servers, EMC storage, and Cisco networking along with packaged orchestration and automation as “virtualization” but not True Private Cloud. Virtualization is a useful step, but ultimately falls short in terms of costs and supportability to the quantum gains that True Private Cloud can deliver. This extends to situations where users deploy VMware tools such as vSphere, vCloud Suite, etc. or Microsoft Cloud Platform System – but not as part of a single entity managed converged solution. VMware, Microsoft, and other software providers, of course, participate in this market significantly as OEM providers to hosters of private clouds who take full responsibility for a True Private Cloud converged systems with infrastructure management and automation.

- Spending by service providers (AWS, Azure, Softlayer etc.) for their public cloud infrastructure whether self-built or acquired via a converged system. While these are advanced deployments and there is considerable activity in the Service Provider sector to build their own clouds to offer as a public cloud service, Wikibon’s perspective for this report is on what enterprises should be doing to duplicate Public Cloud experience, costs and efficiencies.

- Spending for cloud consulting, support and deployment, general data center outsourcing, co-location, and similar services – unless the service is to maintain and manage a Private Cloud for an enterprise.

- Virtual private cloud (Amazon VPC, Azure Virtual Network, CSC Virtual Private Cloud et alia). These revenues are included in our Public Cloud figures at this time.

True Private Cloud Market Projection

Our projection begins with total infrastructure spending. Wikibon’s definition of infrastructure spending, the envelope for the market within which True Private Cloud will compete in the next decade, includes Public and True Private Cloud spending, as well as the hardware, software, and services that are purchased to support the infrastructure needs of enterprises. We have also provided an estimate of enterprise IT Operation staff spending to show where the largest impact on total infrastructure spending will be realized. As such the total available market serving the infrastructure needs of enterprises includes:

-

True Private Cloud

- Systems, Infrastructure Software, and related Support services – The Converged Systems and Support segment of True Private Cloud is expected to grow from $7B in 2015 to $201B in 2026, at a CAGR of 39%. This extraordinary level of growth is a function of the rapid growth of Converged Systems platforms coupled with the transformation of these offerings from the virtualization-centric convergence of today to True Private Cloud through 2020. We expect that the Converged Infrastructure segment (including bundled software offerings meeting the definition) will become a more attractive solution in the latter part of the forecast period – especially as it embraces sensitive mission-critical systems of record workloads that enterprises will probably prefer to keep on premise or operate in a hybrid manner. When the performance of Converged Systems begin to approximate that of Public Cloud we expect that more workloads will migrate from Traditional spending – enabling enterprises to bring the value to an increasing number of workloads – especially those that are latency dependent. True Private Cloud also includes Enterprise Server SAN (see Wikibon’s: Industry Shifts to Catch the Server SAN Wave, and Server San 2012-2026).

- Hosted Services – Today the Cloud Hosting segment is a key method of delivering True Private Cloud services ($3B in 2015 growing to $48B in 2026 for a CAGR of 31%).

Source: © Wikibon Public & True Private Cloud Research, 2016.

-

Public Cloud

- Public Cloud IaaS – Wikibon’s IaaS Public Cloud forecast is $25B in 2015 growing to $173B in 2026. This includes a slight upwards revision of our IaaS forecast of earlier in 2015. The Public Cloud segment will continue on its high growth trajectory throughout the decade (Reference: Public Cloud 2015-2026 forecast). However, Wikibon projects that the low hanging workloads will be exhausted by the end of the decade, and conversion costs and other factors are likely to restrict the movement of complex business processes and applications (including edge computing) that are not such a good fit for the Public Cloud. At the same time, True Private Cloud will offer a much easier transition for these workloads. Hyperscale Server SAN is included within our Public Cloud definition.

- IaaS portion of SaaS and PaaS – From a purely infrastructure perspective, Wikibon estimates that some portion of SaaS and PaaS should be attributed to Infrastructure. For the purpose of capturing IT industry infrastructure spending in this report, we have included 15% of our SaaS and Paas forecasts in these figures, or $8B in 2015 growing to $55B in 2026 (19% CAGR). This estimate is based on a slightly higher base than our previous Public Cloud Projections, which will be updated soon.

Source: © Wikibon Public & True Private Cloud Research, 2016.

-

Traditional Infrastructure Spending and Staffing

- Virtualization – While this makes up the majority of what is typically referred to as “Private Cloud” today, we expect that this method of delivering infrastructure services will be supplanted over time with True Private Cloud implementations – declining from $46B in 2015 to $26B in 2026 (-5% CAGR). However, many mid to late technology adopters will get on the journey to True Private Cloud via virtualization as a starting point which will continue to provide value (albeit not as much as true Private Cloud) on the basis of an enterprise’s technology readiness.

- Traditional IT Operations spending – “Traditional” infrastructure spending is the difference between the prior categories and all spending for infrastructure – including hardware and related maintenance, systems software, outsourcing, infrastructure hosting, and deploy and support services. This category will decline at a -10% CAGR from $571B in 2015 to $189B in 2026. That spending will include workloads that are best left to traditional computing methods or that are sensitive (custom built vertical business processes, high performance computing, highly sensitive data-based workloads, very high transaction rate environments, et alia or where the scale and importance of key workloads requires a more cautious step by step transformational approach. Our definition of Traditional Infrastructure expressly excludes Application Middleware, Database, and Application Software as well as consulting, system integration, application maintenance and hosting. PCs, smartphones, and peripherals are also excluded.

- Enterprise IT Operations Staffing – In order to capture the total value of True Private Cloud for IT is automation and efficiency we have added an IT Operations Staffing line item to our forecast. We believe that True Private Cloud will dramatically impact enterprise operations staffing during the forecast period. IT Depts will reduce some staff, but more importantly deploy more staff to produce business process value. In addition, Public Cloud providers, True Private Cloud vendors and Private Cloud hosters will absorb some of the operations staff (removing them from the direct IT budget) – albeit much more efficiently as their service offerings grow in volume and scope. Enterprise staff is projected to decline from $315B in 2015 to $144B in 2026, at a CAGR of -7%. This reduction of resources is projected to be a major factor in driving vendor R&D and cost reductions for customers to enable the migration to True Private and Public Clouds from very inefficient traditional infrastructure.

Source: © Wikibon Public & True Private Cloud Research, 2016.

True Private Cloud Market Shares

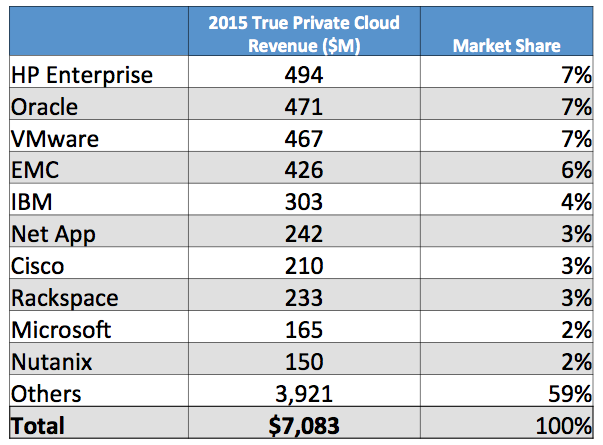

Below is a table of revenue by vendor; today the percentage of revenue that qualifies under Wikibon’s True Private Cloud is a small piece of the overall revenue of most of these companies. As discussed earlier in this research, converged (and hyperconverged) infrastructure companies, software companies and service providers all have opportunities to assist users with transforming operations and become more responsive to the needs of the business.

[Update: A previous version of the report failed to include Oracle revenue in the chart above]

For the software vendor, there is significant hardware and services drag (2-5 times) from other vendors that are not reflected in Table 1 above.

Conclusions and Action Items:

Enterprises should seek True Private Cloud solutions that duplicate most closely the user relationships, performance, and practices of Public Cloud providers. While virtualization and other measures are a step on the path, the best practice will be to incorporate as much of the Public Cloud profile to your data center initiatives as possible. If building a True Private Cloud – seek out converged infrastructure solutions with the highest levels of orchestration and automation as possible as a starting point, and where the provider of the True Private Cloud is happy to be the single throat to choke for maintenance and upgrades. Another approach to take is to engage with Private Cloud Service providers who have the skills and ability to provide Public Cloud levels of service, maintenance and performance. At least a basic Hybrid Cloud service should be included initially, with a roadmap to include more expansive services.

Product Vendors serving the True Private Cloud market should be cognizant that the premium product is one that is converged and highly integrated throughout as many levels of the stack as possible. Support should include coordinated upgrade cycles.

Appendix – Methodology and Sources

Wikibon drew on many sources to construct this picture of the future of infrastructure and True Private Cloud. Our sources included:

- Wikibon held and recorded confidential in-depth interviews (IDIs) with over 50 senior management and practitioners who were early adopters of Public Cloud, Public Cloud providers, converged infrastructure users, Server SAN users and other users of systems with components of True Private Cloud. These interviews looked in detail at the configuration before and after the changes, the business case for installation, and the results of the installation. These interviews were at the heart of our estimates of the friction in the adoption of True Private Cloud, the business case for adoption, and the cost and difficulty of making changes. We also had presentations from very many vendors and startups on software and hardware that is in development and is likely to be brought to market. The Cube also interviewed thousands of leading vendors and practitioners about the core IT issues that they were trying to provide solutions or implement solutions for. The IDIs and cube interviews enabled us to project the likely technology directions of vendors and the benefit of these technology introductions to enterprises.

- Total infrastructure envelope and growth – Wikibon’s own Standard Business Model (based on revenues of $1 Billion dollars, 4,000 employees, and an IT budget of $40 million) and publicly available from Forrester and other companies from 2012 served as a starting point for the allocation of infrastructure spending across segments. Wikibon applied its own IT segment growth models to forecast each of the infrastructure spending segments to create a baseline and the spending envelope for growth from 2014-2026.

- Public Cloud data. We increased our IaaS forecast based on more recent data – especially for Amazon and Microsoft. This forecast will be formally updated in our Public Cloud Forecast update later in the Q2 2016.

- Virtualization Traditional Spending – Wikibon drew on its own research to build this model.

- 2014 True Private Cloud Converged Systems – Wikibon drew on publicly available IDC data about the Converged Systems markets to size those for 2014. We used Wikibon assumptions and research to calibrate the True Private Cloud Content of each for 2014 through 2026.

- 2014 True Hosted Private Cloud – Wikibon drew on publicly available IDC data about True Hosted private Cloud to size that market for 2014. We applied its own analysis of the portion that was True Private Cloud. Wikibon used its own assumptions and research to calibrate the growth rate from 2015 through 2026.