The public cloud market remains strong, attracting both new enterprise customers and suppliers. This report updates Wikibon’s July 2016 public cloud forecast.

Wikibon’s market research, including guidance from numerous providers, concludes that public cloud will grow 32.3% in 2017 to $135.1B and that strong growth will be sustained over the forecast period to $530.8B by 2027 (14.7% CAGR from 2017 to 2017). SaaS CAGR for 2017-2027 will be 14.4%; PaaS CAGR (31.3%), and IaaS (12.3%). Wikibon believes that public cloud will represent 28% of typical traditional enterprise IT budgets by 2027.

Key factors driving our forecast model include:

- SMB customers remain central to public cloud growth. Public cloud adoption has been led by SMB in the US. The SMB influence will remain strong in 2017 – and will be augmented in non-US markets where cloud penetration is more nascent.

- Large enterprise growth is accelerating. While migration and complexity considerations have constrained public cloud in large enterprises, exceptions gradually are being chipped away with better offerings and a recognition that public cloud must be part of their digital transformation efforts – outright or as component of hybrid approaches.

- PaaS is attracting more developers. Digital transformation efforts are pushing more developers to public cloud PaaS, which biases subsequent IaaS and SaaS choices. We expect this dynamic to continue.

- Public cloud market structures are solidifying – in the US, at least. Public cloud leadership is consolidating which provides the market with credibility and direction. Leaders are on a growth – make that market share grab – phase of development. We expect that offerings and prices will be increasingly attractive and competitive for enterprises of all sizes. Various factors ensure the non-US cloud market remains more fluid including local regulations on data ownership and jurisdiction, security, and impact on national economic infrastructures.

- Big data is embracing public cloud. Analytics (especially big data) has found a home in the public cloud, which is helping to increase success rates for big data projects – and reshaping the big data software ecosystem. In part because of the growing tie between big data and public cloud, “Consider Cloud First” increasingly is the attitude for enterprise decision makers.

Public Cloud Trends and Dynamics Point to Strong Growth

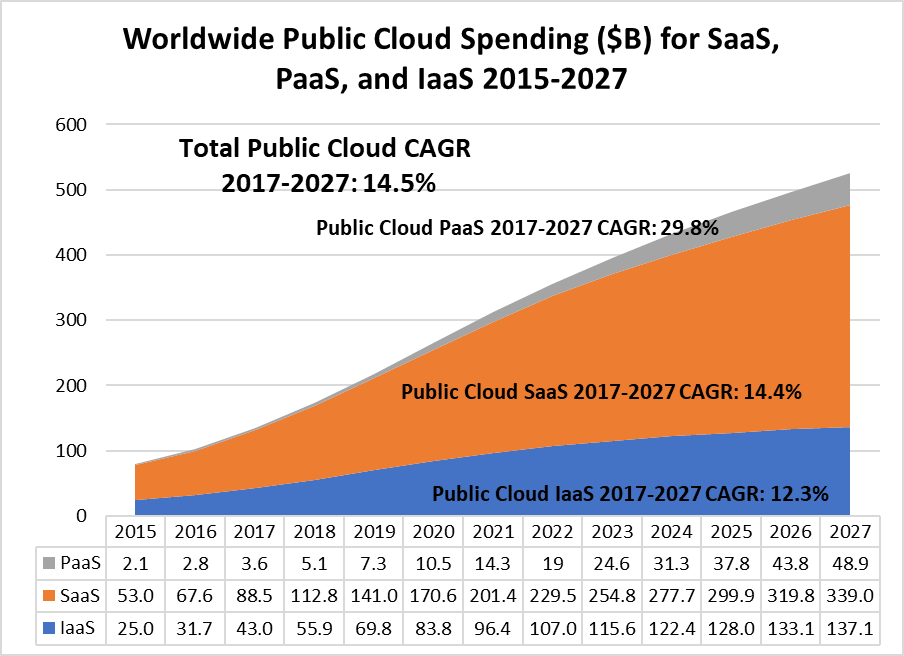

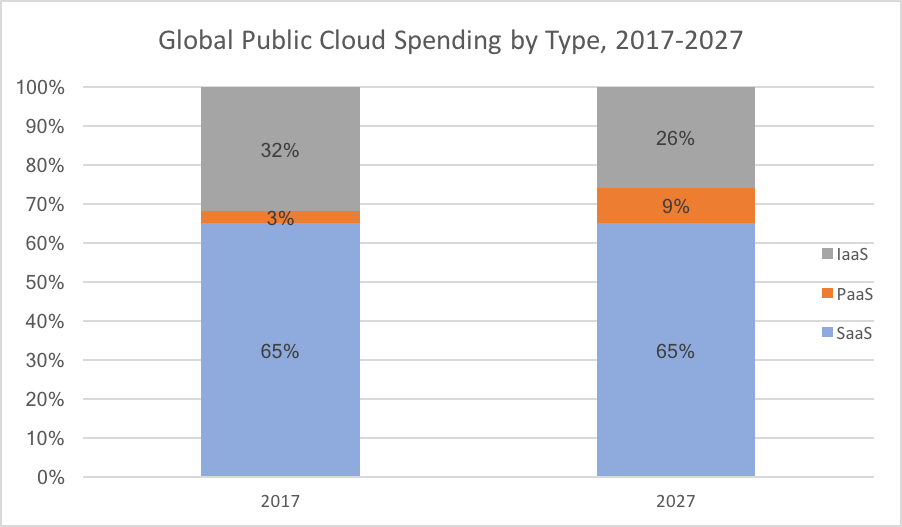

As we see in Figure 1, public cloud revenue will grow by 14.5% compounded annually, from $102.1B in 2016 to $525.0B by 2027. Each public cloud segment will grow by double digits in the 2017 to 2027 period, including SaaS 14.4%, PaaS 29.8%, and IaaS 12.3%. However, the mix will differ as public cloud increasingly becomes the destination for digital transformation and mission critical workloads (see Figure 2). By 2027 SaaS will account for 65% of public cloud spending. Despite slower growth, IaaS, at 26%, also will be significant. The growth of PaaS will be strong (including the IaaS portion of its use), but still only account for 9% of the public cloud market by 2027.

Figure 1: Worldwide Public Cloud Revenue ($B) 2015-2017 for PaaS, SaaS, and IaaS

Figure 2: Share of Public Cloud by Type 2017

Public Cloud Adoption Differs Depending on Enterprise Size and Region

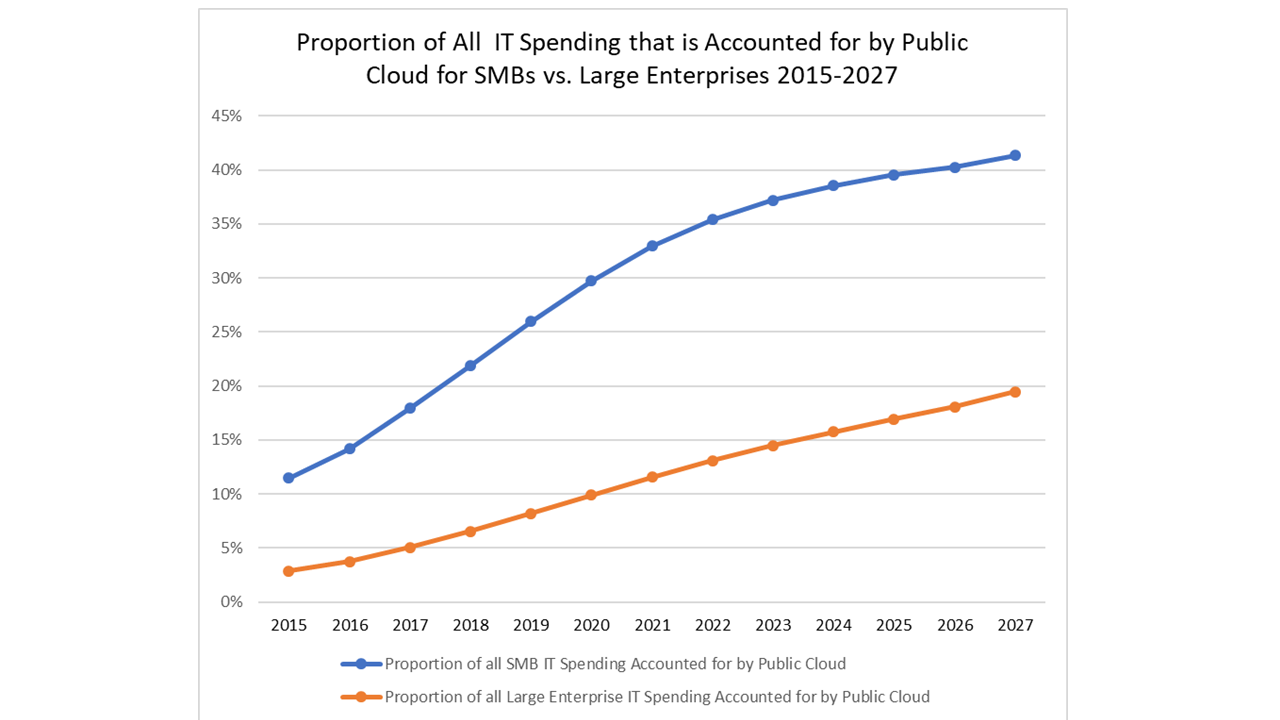

Public cloud spending growth will be strong for both SMBs and Large Enterprises thru 2027 (see Figure 3), albeit with different starting points and end points. We expect start-ups and SMBs to continue to be strong buyers of public cloud services. Microsoft Azure, Amazon Web Services (AWS), Google GCP, and Alibaba Aliyun are especially strong in the SMB customer segment. SMB public cloud spending is 18% in 2017 and will grow to 41% by 2027. We see large enterprises accelerating their public cloud spending from 5% of all their IT spend in 2017 to 20% of all their IT spending by 2027.

Figure 3: Proportion of all IT Spending that is Accounted for by Public Cloud for SMBs and Large Enterprise

AWS, IBM, Microsoft Azure and Oracle will lead the public cloud market in the large enterprise segment. Large enterprises will demand a mix of public, hosted, and on-premises true private cloud options to satisfy their more complex environments and business processes. Public cloud will gain an increasing share of this mix, however, as the leading vendors solve the complexity and compatibility challenges. Ultimately, our research points out the following enterprise size and regional trends.

- Public cloud is exploding in the start-up segment. Public cloud (especially in the form of SaaS) has emerged as the default option for start-ups. While there is a lot of growth potential here, the spend is relatively modest compared to SMBs and Large Enterprises because start-ups have reduced needs for infrastructure scale. With high rates of penetration today, this will continue to be a public cloud stronghold – but won’t produce surging growth itself.

- SMBs have many reasons to adopt SaaS offerings. SMBs are already on board with public cloud – so they will continue to be a solid source of growth – especially from EMEA and APAC SMBs. Accounting for roughly half of all global IT spend, SMBs can draw the most value today from pubic cloud SaaS offerings – avoiding costly infrastructure and often benefitting from a rich development environment offered by the SaaS provider for application extension and customization. Moreover, SMBs can attain world class digital transformation performance (e.g., omnichannel capabilities in retail) that were only available to large scale competitors, until recently. This ability to “flatten the learning curve” allows SMBs to extend their capabilities to adjacent applications.

- Large Enterprises will be deliberate and cautious buyers of public cloud. Large enterprises face difficult decisions about how and where to embrace public cloud. First, enterprises typically employ competent IT staffs that currently are delivering working IT services. Second, large enterprise needs can be very specific, with workloads reflecting the complexity of enterprises businesses along customer segment, offering portfolio, region, and partnership lines. Third, enterprises typically are not “greenfield” customers; most enterprises have deployed large portfolios of complex applications over the years, almost all of which do not easily or cheaply migrate to public cloud platforms. We expect complexity to be a barrier in the early years of the forecast period for large enterprises. However, large enterprises will be considering public cloud solutions as replacements (or at least augmentation) for aging legacy applications. Hybrid models seem to be a logical next step to effect this transition. We expect large enterprises to decide that more public cloud workloads from both incumbent and cloud native public cloud providers will be suitable for deployment.

- International markets are only now beginning to heat up. Wikibon expects that public cloud providers will evolve to serve the unique needs of international markets. Concerns include local regulations on data ownership and jurisdiction, security, and impact on national economic infrastructures. International markets in general are weighted more towards SMBs than is the case of the US, which is helping to catalyze international adoption of public cloud. In places like China (and across the Asia/Pacific regions generally), which features a continuous stream of start-ups, we expect rapid and significant uptake of SaaS. US-based SaaS vendors already are reporting more significant growth from their international markets. Markets in EMEA are especially sensitive to regulatory, security, and business infrastructure issues as mature businesses evolve to accommodate less mature data privacy regulations. Our expectation is that EMEA will solve its issues and will more rapidly expand public cloud use in the early part of the forecast period.

Public Cloud Remains Part of Enterprise IT Spending

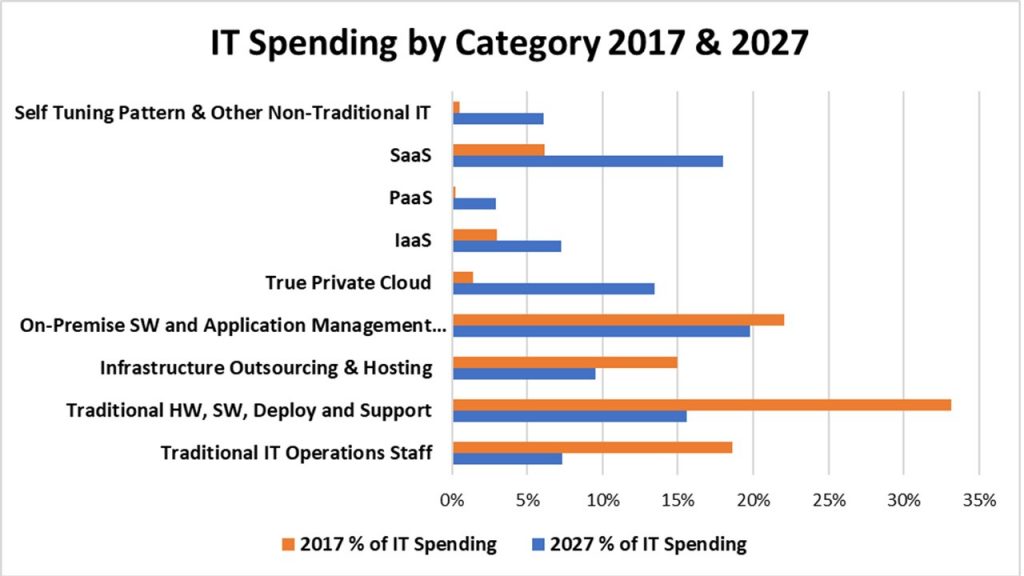

Public cloud spending does not live in a vacuum. In creating our long term forecast we have considered the envelope of spending within which public cloud resides (See Figure 4). In addition to public cloud, IT and LOBs technology-related business challenges can be met by True Private Cloud (https://wikibon.com/wikibon-2017-true-private-cloud-forecast-and-market-shares/), traditional data center infrastructure hardware, software, and services, traditional applications (on-prem software and application management services), infrastructure services (hosted clouds as well as traditional infrastructure outsourcing), as well as the basic costs of operations (not development) staff. As such, public cloud deployment and spending will compete with these alternatives.

Figure 4: IT Spending by Category 2017-2027

Overall, Wikibon forecasts that IT spending (including non-traditional IT workloads – e.g., IIoT) will grow at about 2.7% compounded annually from 2017 to 2027. As can be seen in 4, Public Cloud will have a marked impact on IT spending over the next decade growing from 9% in 2017 to 28% in 2027. This will come primarily at the expense of traditional HW, SW, outsourcing, and operations staffing. Wikibon expects the vendors of these products will be significant participants in the emerging segments we’ve identified. So public cloud will not dominate IT strategy and spending, but will be a much more vital component than its position today.

At this time, we have not included BPO or enterprise development personnel costs in this model.

SaaS: It Just Keeps on Growing

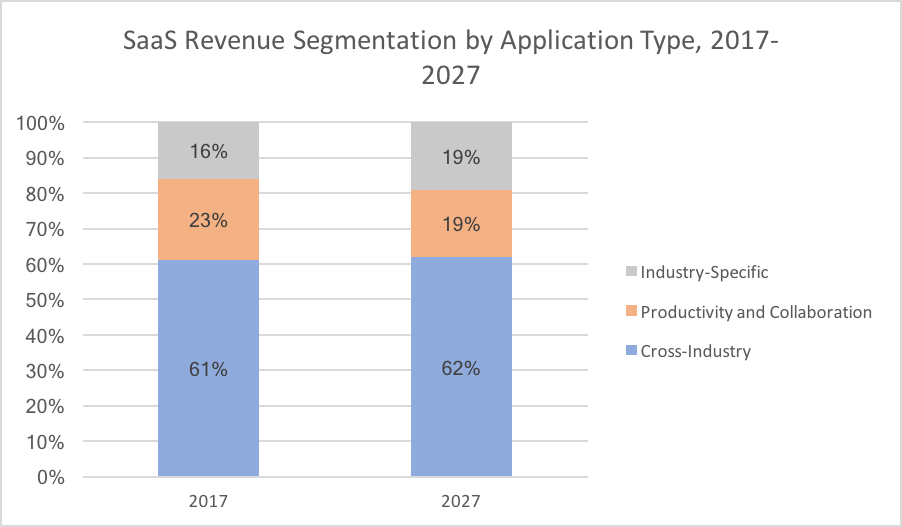

SaaS will evolve in response to continuing SMB demand, entrance of new application forms (including many from non-technology companies), and methodical conversion of legacy applications to public cloud by large enterprises. The SaaS market was $67.6B in 2016 and will grow to $88.5B in 2017. The SaaS market will grow to $339B by 2027, a CAGR of 14.4%. SaaS will be the largest cloud market; indeed, SaaS will account for 18% of total IT spending in 2027. While SaaS growth will be universally strong, it will differ by solution segment (see Figure 5):

- “Low-hanging fruit” growth slows. Personal productivity, collaboration, social media, and content delivery were the earliest SaaS applications. SaaS is the generally accepted preferred method for deployment for these use cases. With the current high degree of penetration and product acceptance, this segment will have a relatively slower growth rate in the forecast period. Capabilities in security, admin, and compliance will be enhanced – but the room for growth of these core capabilities is limited by relative saturation.

- Cross Industry Applications remain the largest SaaS markets. Cross industry applications (marketing, sales, CRM, and HCM especially) are a good fit for public cloud since the models for these applications are common across all industries and company sizes. There is still a lot of runway here for spending growth – especially among SMB customers. Wikibon includes infrastructure performance management SaaS tools as Cross-Industry Applications.

- Industry-specific applications have been slower to materialize due to narrow niches and specialized requirements. There have been a few noteworthy areas of public cloud beachheads in vertical markets – notably healthcare and government which are characterized by many small businesses operating in a heavily regulated environment. In some cases, these industry apps are specialized versions of general Cross Industry apps. However, inherently smaller revenue opportunity of vertical markets makes investments in SaaS technology less attractive and more risky. Salesforce and other leading SaaS vendors such as ServiceNow are turning their attentions to these types of solutions so there will be a mix of leading SaaS vendors and specialists as the market unfolds. Other industry-specific workloads may not be so suitable for the public cloud (i.e., manufacturing execution systems, industrial internet of things) due to data movement and the requirements of rapid response time for interactive apps (i.e. interactive engineering and simulation applications).

Figure 5. SaaS Revenue Segmentation by Application Type, 2017-2027

IaaS

SMB demand assures strong public cloud IaaS growth. Enterprise migration of legacy apps and transforming outsourcing relationships to public cloud services will expand demand among large enterprises, albeit at a slower rate due to the complexity of the infrastructure environment. The IaaS market was $31.7B in 2016 and will grow by 36% to $43.0B in 2017 with a 12.3% CAGR though 2027. While growth will still be in double digits through 2027, we believe that IaaS growth will be the slowest of the three segments for a number of reasons.

Second, and perhaps most importantly, both traditional and new infrastructure vendors are bringing compelling, advanced, on-premises architectures like True Private Clouds (i.e., based on hyperconverged and ServerSAN architectures) (https://wikibon.com/wikibon-2017-true-private-cloud-forecast-and-market-shares/ that deliver public cloud benefits to the data center. Later in the forecast period, new classes of systems that combine compute, storage, and networking into a uniform and universal package (we’re calling Unigrid). Unigrid will offer universal access to systems for any application, uniform developer environments, and unitary systems administration. These alternatives will enable data centers to counter “public cloud first” for IaaS with comparable in-house offerings of their own versions of cloud. At this point in the market, traditional SAP and Oracle enterprise apps may be the first go to these types of platforms where they may settle for the duration – or provide a migration step towards public cloud offerings.

The surge of on-premises true private cloud offerings ensures that the move to hybrid cloud will impact IaaS – in some cases providing a viable alternative to public cloud and in other cases providing a potential on-ramp to public cloud. In the latter case, many workloads will require highly compatible underlying infrastructure compatibility between the on-prem and public cloud version of the systems upon which they depend. Oracle, for one, increasingly is moving in that direction, so their installed base won’t be “forced to select public over private” and perhaps look elsewhere to get their business workloads done. This may play out to actually be a facilitator for public cloud in the long run. However, distributed computing is never easy to effectively deploy, so this will hinder hybrid solutions overall at least through 2020 as vendors like Oracle architect methods for making hybrid cloud solutions truly transparently identical – wherever the workload resides. Microsoft has similar challenges. IBM is working this problem in even more complex environments.

Platform-as-a-Service Market: Nascent Market Has Significant Upside

The public cloud PaaS market will grow from $2.8B in 2016 to $3.6B in 2017 and $48.9B by 2027, a CAGR of 29.8%. This market overall is still in its early formative stage, both in its public and private cloud manifestations. So its robust public cloud growth rate is a function, in part, of the overall adoption of this approach to development.

To begin with, our definition of PaaS is narrowly drawn – see Appendix C. Much of the development work we see today doesn’t meet our criteria for full application life-cycle cloud service, including initial development, testing, deployment, operations, and maintenance to suit modern continuous integration and delivery development models. We expect this to change over the forecast period with development projects increasingly encompassing the full life cycle as opposed to today’s limited approaches.

PaaS growth will be facilitated by these drivers:

- PaaS makes the development cycle much more efficient. The key value of PaaS is that it enablesThe trade-off to efficiency and rapid deployment, of course, is that for specialized requirements, this sort of generalized solution may not be appropriate. But for most workloads, faster time to value and ease of execution will have the highest value.

- Public cloud PaaS will grow fast because of greenfield opportunities. Public cloud PaaS is most often deployed for new applications and start-up situations that don’t feature legacy code that must be emulated or migrated. PaaS in the traditional data center will have tougher road to travel — since today’s operational workloads (and developer skills) have not often been built in a manner that is conducive to PaaS tools and practices — and rip and replace is not an appealing option. However, we expect that enterprises will leverage the new generation of augmented programming tools to accelerate refactoring, containerization, orchestration, migration, and optimization of legacy enterprise applications for public and hybrid cloud PaaS environments.

- Considerable VC investment into this space bolsters growth. Established public cloud vendors like AWS, Salesforce, Oracle, IBM, Microsoft, Google, ServiceNow, et alia are leading the PaaS market. Moreover, start-up providers of augmented programming tools are having an important impact on the PaaS market, including Outsystems, Mendix, Kony, Caspio, BettyBlocks and Kintone. Which way developers go will have a major impact on all aspects of public cloud, but an especially important impact on PaaS. Today, developers are getting their cloud development done by adding augmented programming tools to their portfolios of offerings for developing PaaS and IaaS capabilities for public, private, and hybrid cloud deployments. For the purposes of this forecast, we are counting IaaS revenue under the control of PaaS as PaaS.

- Developers are gaining more influence in platform decision-making. The incumbent SaaS and IaaS vendor, of course, has an advantage in terms of tool selection, but developers themselves are gaining more influence on how to attack increasingly complex workloads in areas like AI and machine learning. Their influence in platform and tool choices will grow throughout the forecast period as applications extend into new areas.

- PaaS is beginning to turn out commercial SaaS products. One example of this is the recent GE Ventures and ServiceNow partnership to commercialize Nuvolo’s mobile-centric cloud-based asset management system for clinical assets in health care. The ability to bring solid solutions based on well supported development platforms will make PaaS all the more attractive to developers.

Action Item

Enterprise actors – both business and IT – need to be actively engaging in bringing the public cloud into their business today and planning a strategy for a technology that is likely to make up as much as 28% of their IT spending budget by 2027. Ultimately, practitioners need to consider their enterprise’s unique business and digital transformation requirements to properly architect and deploy workloads where they can obtain the best business value for their enterprise.

To accomplish this, enterprises should establish an adaptive strategy that exploits the best of today’s public cloud offerings while hedging their bets to leave open the space to move to alternative platforms such as True Private Cloud and hybrid options as their needs and the market itself continues to develop.

Appendices

Appendix A: What We’re Counting

Wikibon counts public cloud revenue in the following manner:

- Public cloud only – Professional services, advertising-related, and other spending is excluded from this report. Advertising revenue may indeed become a factor in public cloud spending in the future, and Wikibon will consider including advertising revenue if and when it becomes a factor in how public cloud services are paid for.

- Enterprise vs. consumer spending – The public cloud spending covered in our model is by enterprises. Wikibon expects that consumer-related cloud services – i.e., productivity, collaboration, content management, marketing-related from vendors like Facebook and Twitter – will need to be enterprise standard. Wikibon will monitor this trend closely. We continue to include business-centric social networks like LinkedIn in this study,

- Public cloud revenue reports caveat – Wikibon acknowledges that provider reporting of “public cloud” revenue seems to be in the eye of the beholder. Salesforce and AWS are pretty much pure public cloud plays, as are many start-up software vendors all of whom report public cloud revenue fairly clearly. However, the definition of “public cloud” becomes a bit murkier for non-pure-plays. As such, Wikibon has developed company-specific models that reflect historical guidance and other pointers and indicators to establish revenue levels for public cloud offerings for some vendors.

- Microsoft guides the growth rates for Azure, Dynamics Online, O365 Commercial, and O365 Consumer) but does divulge the actual size of each public cloud business. Wikibon has developed a detailed model that we believe closely represents their public cloud revenue splits.

- Oracle’s SaaS (organic growth vs. acquisition?) vs. PaaS (given Wikibon’s definition) vs. IaaS are challenging to unravel. Oracle recently provided additional revenue segmentations that make the picture a bit clearer.

- SAP’s “Cloud” designation – and it’s reporting of Ariba and other acquisitions makes the revenue allocation challenging.

- IBM’s very broad array of public and private cloud services span hardware, software, professional services, hosting, outsourcing services, analytics, as well as public cloud. We’ve modeled what we believe their public cloud (but our definition) revenue to be.

However, in our view, the definitional unclarity just indicates that public cloud is being leveraged from many different angles and is building significant momentum as it encompasses both product and service delivery mechanisms, pretty much penetrating into all aspects of information technology.

Appendix B: Public Cloud Sizing and Forecast Methodology

This forecast is based on a variety of interlocking inputs and points of calibration and can be updated quarterly to reflect changing market conditions, Wikibon has drawn on a wide variety of sources to establish this public cloud sizing, segmentation, and forecast.

- Worldwide cloud spending sizing and forecast – Our growth and penetration rates for cloud for each segment are built up from reported revenue of ~100 lines of business for cloud providers. In some cases, Wikibon analysts have applied intelligent estimates where the vendor is important and the published data is ambiguous. This approach has been made easier over the past year as many more of the largest vendors are reporting cloud revenue.

- Sizing cloud segment revenue – Wikibon has conducted surveys of cloud users to gauge the applications and use cases. We have applied this data to our working revenue models to calibrate the segments where spending is strong today and where users are intending to expand their cloud use cases and spending in the future.

- Wikibon expert analysis – Most importantly, Wikibon has drawn on its expert analysts to calibrate the near term data and to create a vision of where the cloud market is heading based on their knowledge of users, vendors, and the technology evolution that will continue to press cloud into more and more varied usage scenarios.

- Underlying worldwide IT spending forecast – Lastly, our growth and penetration rates are calibrated against a WW IT Spending market model that is based on publicly reported quarterly financial data and a protocol of statistical trend analyses to estimate the likeliest revenue outcomes for the forecast period for each of ~ 150 vendors and reported business units (in the aggregate covering 45% of all WW IT spending). The approach assumes that — in the aggregate — leading vendor financial reports provide good guidance for the market’s overall growth rate. The data is weighted and aggregated for each IT industry segment within which cloud spending occurs so as to ensure our growth rates make sense in terms of rates and degree of penetration vs. available spending.

Appendix C: Special Consideration: Platform-as-a-Service Market

Wikibon’s definition of PaaS (see http://wikibon.com/2016-wikibon-public-cloud-definitions/) requires that to qualify as PaaS revenue, the usage must encompass a full application life-cycle cloud service, including initial development, testing, deployment, operations, and maintenance to suit modern continuous integration and delivery development models. As such, over time PaaS will incorporate portions of IaaS and SaaS. In our definition, individual components of development, per se, which are not used in a total life cycle platform are not counted here, but rather they are counted in the IaaS segment.

PaaS includes three classes of providers – all with different perspectives and market entry points.

- PaaS from an IaaS provider. – Amazon Elastic Beanstalk, components of Microsoft Azure, components of Google App Engine are examples here. This approach offers excellent integration with the underlying IaaS platform, rapid migration from test to production, and good vendor support. On the other hand it enables platform lock-in, has limited extensibility, may not support hybrid clouds, and skills may not be very portable.

- PaaS from a SaaS provider. – Salesforce.com Sales Force1, ServiceNow Service Automation Platform, SAP HANA Cloud Platform are examples of these. This approach (of course) offers excellent integration with the underlying SaaS platform, a rich set of platform-specific tools, rapid deployment, and good vendor support. However, performance can be problematic, and these tools may not be appropriate for general purpose use. Platform lock-in may be a risk and the skills required for the environment may not be portable to other PaaS approaches.

- PaaS from a development environment provider. – IBM’s Bluemix, HP’s Helion Development Platform, Pivotal Software’s Cloud Foundry are examples of these. This approach supports a DevOp IT structure and is characterized by flexibility to deploy easily on a supported infrastructure platform and supports a wide range of languages and management tools. There is less risk of platform lock-in and the approach does encourage good skills portability. This approach may be a good one for hybrid clouds.

Appendix D: Wikibon Public Cloud Forecast Philosophy

A famous economist once said, “If you don’t forecast well, then you should forecast often.” Given the turbulence that cloud is creating in the IT market today, the Wikibon methodology takes this advice seriously. Wikibon tracks public cloud revenue trends on a quarterly basis with the goal to provide a formal semiannual report update. This approach enables our forecasts to incorporate up-to-the-minute, auditable data to maintain running forecasts that can be recalibrated to reflect new information and real market trends.