Alex Karp’s recent broadside against the frontier model vendors put a knife to the throat of the central enterprise AI debate. Karp’s argument is that frontier model vendors (he didn’t mention Anthropic and OpenAI by name) intend to suck the knowledge out of enterprises and destroy the “alpha” companies enjoy through their proprietary data, processes and underlying business advantage. In our last Breaking Analysis, we called this approach “Data Communism,” where every firm gains access to the same intelligence.

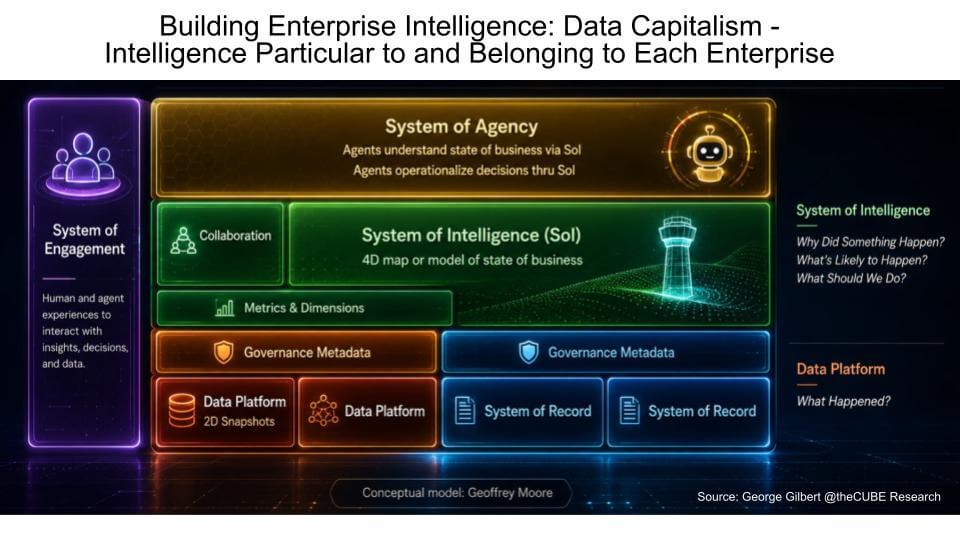

Our counter to data communism is data capitalism, where proprietary advantage remains exclusive to an organization and its broader ecosystem. The familiar graphic below describes how we see the AI software stack evolving. The most important pieces of this stack, in our view, are the System of Intelligence (SoI) and the System of Engagement (the new user/client surface). We believe competitive advantage accrues to firms that can make these two puzzle pieces interact and learn from the reasoning traces of humans. Critical is how they capture tacit enterprise knowledge to take governed and trusted actions both with and without humans.

The key issue we explore in this Breaking Analysis is who will own the operating intelligence of the enterprise?

On the surface, the argument is about closed models versus open models, OpenAI and Anthropic versus Nvidia’s Nemotron (as an example), and whether enterprises should trust frontier labs with their most sensitive data and workflows. But as Jensen Huang said at GTC 2026, “proprietary versus open is not a thing. It’s proprietary and open.”

The deeper issue is not model choice. It is control.

This question goes to the heart of the debate inside theCUBE Research and across the industry. Here are the two ends of the spectrum, with two scenarios from theCUBE Research:

- Frontier Model Leadership – One camp believes the frontier model vendors will dominate the stack because their utility, cost curves, research velocity, volume and compute access will outpace everything else.

- Dispersed Intelligence – The alternative argument is the frontier players lack the mindset, DNA, process knowledge and trust. This camp agrees that the highest-value layer is not the model itself, but the System of Intelligence – the enterprise-specific context layer that captures business rules, policies, processes, state and tacit knowledge as governed assets. And the argument is that other players (e.g., Palantir, Databricks, Microsoft, Google, Celonis and new startups) will cement a more critical position in the AI stack than the frontier model players.

Both views can be true. And both acknowledge that: 1) the System of Intelligence and the client surface must be part of the winning vendor’s stack; and 2) trust and proprietary knowledge must be the exclusive property of the customer. But the Karp conversation unveils the tension between them and, we believe, will define the future enterprise AI industry power structure. In either case, it’s highly likely that silos of intelligence will emerge over the next decade, and the industry will remain heterogeneous and fragmented.

To put a finer point on the topic, Karp’s statements imply that OpenAI and Anthropic are stealing data from their customers and overcharging them. He positions his company, Palantir, as a critical “application layer” to protect businesses and governments from those newbies and their bad intentions. He is on a mission to convince businesses they need a more trusted partner than Anthropic or OpenAI. Rather than dealing directly with the two AI firms, he’s arguing Palantir (by proxy) should be that intermediary.

The frontier model dominance case

We’ve not published extensively on this point of view, and it’s worth taking a moment to do so here. Much of the following is based on scenario and cost modeling work done by theCUBE Research Analyst Emeritus David Floyer. The methodology and framework are detailed below and draw extensively on Wright’s Law, as applied to software. Wright’s Law says that as cumulative production rises, costs fall in a predictable way. In AI, the equivalent is not just cumulative production but cumulative usage, cumulative tokens, cumulative feedback, cumulative training experience, cumulative inference optimization and cumulative compute deployment.

While some of the AI data forecasts in the methodology need updating, the principles of the forecasting approach still apply.

Here’s the argument.

Think of the frontier model as a “cognitive surface,” the heart of intelligence and the sole source of tokens. It performs reasoning, planning, synthesis and learning. It is built and runs on the most advanced hardware available and continues to improve rapidly. It is capital-intensive, power-dense and scarce by design. Only a small number of organizations can develop and operate frontier models at scale, and enterprises should not attempt to replicate this function.

Directly coupled to the frontier model is a new layer that does not exist in traditional enterprise architectures: The System of Intelligence (SoI). This layer manages all inputs to and outputs from the LLMs. It shapes intent, context, constraints and semantic grounding before intelligence is invoked. It expresses intelligence into actions, system interactions and multimodal outputs after tokens are produced. It hosts security, policy enforcement, compliance, auditability, latency control and integration with enterprise systems. It evolves in lockstep with the frontier model while remaining external to it, preserving both control and adaptability.

While frontier model developers must own their cognitive surface architecturally and evolutionarily, they will almost certainly want to own the SoI and also allow the controlled distribution of both. A fundamental assumption in this scenario must be made explicit: Large enterprises will be permitted by the LLM license terms to operate instances of the cognitive surface locally or within sovereign environments to meet latency, security and regulatory requirements. However, this distribution will occur under strict contractual and technical control. Enterprises will not be able to modify the LLM itself; they will only be able to configure, utilize and integrate it within defined boundaries. But those configurations and associated data, process logic and underlying enterprise knowledge remain the sole property of the customer. Semantic grounding, safety constraints, interface definitions and evolutionary alignment will remain under frontier model governance. This arrangement preserves enterprise control over data, latency and policy while preventing intelligence fragmentation or semantic drift.

The LLM is also the place where a small number of early and strategically positioned SaaS vendors will negotiate with frontier model providers to license access to semantic definitions, interfaces and selected process and execution logic. Likely candidates are SAP, Oracle, Salesforce, ServiceNow and other leading SaaS providers. Vendors of platform services and middleware may also seek certified integration points within the cognitive surface. For example, a platform provider such as Oracle is well-positioned to operate a minimal, authoritative RAG capability within the cognitive surface, in conjunction with a frontier model provider such as OpenAI. Open-source applications may also be integrated, subject to the same semantic, security and governance constraints.

Frontier leaders as this era’s disruptors

This scenario recognizes frontier players have the world’s top AI researchers. They have access to the largest pools of compute. They have massive user volume. They have consumer products and/or consumer-like volumes that act as high-frequency learning loops. They have brand affinity, developer adoption and enterprise pull. And they have the capital to run far ahead of companies that are trying to compete from narrower positions, all while being rewarded and still losing money.

As such, this point of view assumes model players will have the lowest cost, highest volume and most functional product. The outlook projects that companies will scale with less labor and achieve 10X productivity relative to current best practice metrics. This economic advantage, the argument says, will overwhelm Karp’s concerns about trust because a winner-take-most dynamic and software-like marginal economics will accrue to firms that lead in AI adoption.

If the frontier models keep improving at a faster rate than alternatives, and if inference costs keep falling, enterprises will continue to route more work to them. Smaller models and open models will absolutely have a role. They will be used for cost-sensitive tasks, domain-specific workloads, sovereignty requirements, edge deployments and latency-sensitive use cases. But in many workflows, they may be most effective as part of a broader ensemble led by frontier-class models.

The most aggressive version of this thesis says that token costs will fall so dramatically that today’s budget concerns will look temporary. Enterprises may complain about LLM bills now, but the real comparison is not token cost versus token cost. It is token cost versus headcount.

If a company can grow revenue 10x without scaling labor proportionally, tokens become relatively cheap. If agents allow enterprises to compress support, engineering, finance, operations, compliance, analytics and fieldwork into software-driven workflows, the marginal cost of tokens becomes much lower than the marginal cost of people. In that world, the winning providers are the ones that deliver the highest utility per unit of work – not necessarily the lowest nominal token price.

That is the frontier model bull case.

OpenAI, Anthropic and Google may become the lowest-cost providers of high-utility intelligence because they operate at the largest scale. Their compute purchasing power, model optimization, inference infrastructure and usage volume may give them better marginal economics than alternatives. If that happens, model routing becomes less about avoiding frontier models and more about using them intelligently where their incremental utility justifies the cost.

Karp’s argument is really about enterprise sovereignty

Karp’s comments are in large part a fear campaign against OpenAI and Anthropic. His language was purposefully fiery, and the reported suggestion that frontier model providers could “take the alpha” of a customer’s business and transfer it into their weights is attention-getting. Notably, there is no public evidence cited that Anthropic or OpenAI trains on customer data in violation of their terms; OpenAI has publicly said it does not train on customer data.

But whether the literal accusation is proven is not the main point.

The enterprise fear is real.

Karp nailed the sentiment. Customers are asking: If our most sensitive workflows, data, decisions, policies and proprietary operating knowledge flow through a frontier model vendor, are we building our future on a supplier that could one day intermediate us, compete with us or extract too much margin from us?

Palantir’s answer is self-serving but thought-provoking – i.e., don’t let the model vendor own the enterprise brain. Let Palantir sit between the customer and the model, govern the interaction, route workloads to the best model, preserve sovereignty and make the model interchangeable.

That is a classic platform move and the one we’ve been putting forth based on George Gilbert’s work. Palantir wants to own the System of Intelligence and treat models as pluggable engines. Its message is the model is important, but the enterprise operating layer is strategic.

This aligns with our Enterprise AGI thesis. We have argued that the real enterprise prize is not generalized intelligence in the abstract, but intelligence that is unique to and owned by each enterprise – data, processes, policies, business logic and tacit knowledge turned into governed assets that agents can reason over and act through.

The System of Intelligence counterargument

The counterargument is that model utility is necessary, but not sufficient for enterprise AI excellence.

Enterprises do not run on intelligence alone. They run on rules, policies, exceptions, permissions, workflows, systems of record, regulatory constraints, domain knowledge, organizational structures and tacit human judgment.

A frontier model can reason brilliantly and still not know what the enterprise is allowed to do.

It may not know which revenue definition is authoritative. It may not know which customer data can be used in which jurisdiction. It may not know which approval is required before changing payment terms. It may not know whether a support escalation should trigger a field dispatch, a credit memo, a legal review or an executive notification. It may not know the difference between what employees usually do and what policy requires them to do.

That is a System of Intelligence problem.

The System of Intelligence is the live enterprise map – ontology, digital twin, semantic layer, business-process model, policy fabric and operational context layer. It is where enterprise data, process logic, business rules, skills and tacit knowledge become assets. It is what allows agents to act safely and confidently.

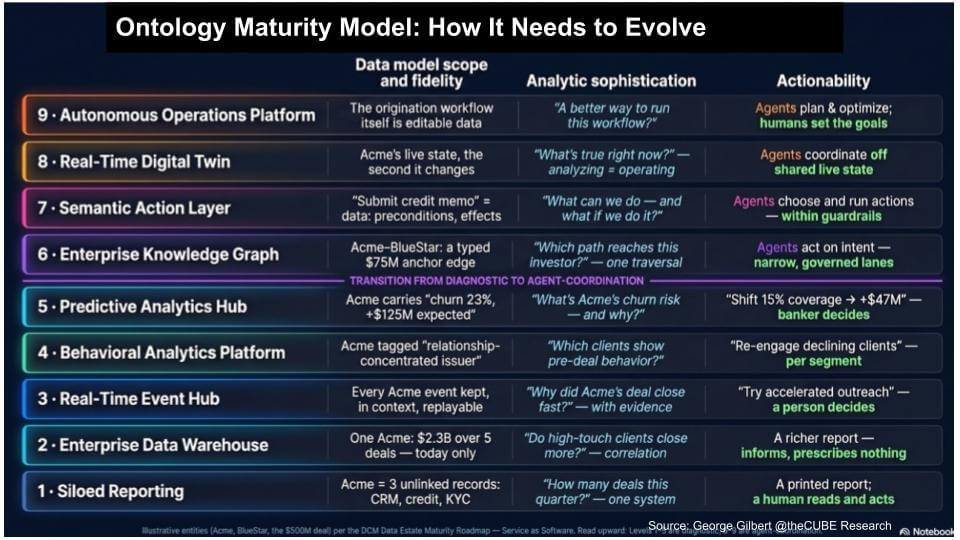

This is where Palantir has a strong argument. Palantir has spent years building ontology-driven operational systems for complex institutions. It understands that the application layer is not just a UX layer. It is where data, decisions, workflow and governance meet.

Databricks is attacking a related problem from the data platform side. Genie, Genie Ontology, Agent Bricks, Unity Catalog, Unity AI Gateway and Omnigent represent an effort to move from governed data infrastructure into engagement, intelligence and agency. In our research, we described this as Databricks moving up the enterprise intelligence stack – from data platform toward a System of Intelligence.

But there is a difference. Palantir is closer to an executable ontology and operational decision layer (see graphic below). Databricks is building from governed data, semantic context and agent governance and is currently between levels five and six in the diagram below based on our current assessment. Both approaches are important. Palantir has a far more mature ontology story, and Karp took a swipe at firms like Databricks, alluding to the fact that everyone is now talking about ontology. Regardless, the leaders are converging on the same control point – the SoI.

Open models are a wedge, not the whole story

Karp’s emphasis on Nvidia’s Nemotron and U.S.-made open models is clever. For government, defense and regulated industries, model sovereignty is vital. Customers may prefer open or domestic models where security, auditability, deployment control or geopolitical concerns outweigh absolute benchmark performance.

But open versus closed is not the real dichotomy.

Jensen Huang’s position that “proprietary and open, not proprietary versus open” is probably closer to how the market develops. Enterprises will use a mix of products. They will route workloads across frontier models, open models, specialized models, small models and internal models. The model router becomes an important economic and governance control point.

Palantir’s Evolve and Databricks’ Unity AI Gateway both point in this direction. Each is trying to help customers decide which model to use for which workload based on cost, performance, security, governance and policy. That is the most pragmatic enterprise answer.

The ideological open-source debate is important, but the operational reality is model optionality.

Still, Karp’s argument has special force in government. If an American open model becomes “good enough” for a classified battlefield workflow, and if Palantir can tune, govern and deploy it securely through its platform, then the closed frontier model may not be necessary for that use case. Good enough plus sovereign plus governed can beat best model plus external dependency.

But that will not apply universally. For the hardest reasoning tasks, frontier models may continue to lead. The market will not standardize on one model class.

Can the frontier labs build the System of Intelligence?

This is the crux of the debate.

One side says the frontier vendors will inevitably move into the System of Intelligence because they must. Consumer AI gives them volume, learning and brand, but enterprise productivity is the obvious TAM. If they stop at model APIs, they risk becoming suppliers to the platforms that actually capture enterprise value. That is not a sustainable end state for companies spending tens or hundreds of billions on compute and research.

From this perspective, the frontier labs will build, partner and acquire their way up the stack. They will create enterprise memory, shared skills, workflow engines, governance layers, agent orchestration, model routers, data connectors, domain packages and forward-deployed implementation capabilities. Consumer volumes are a feature, not a drawback. Personal memory becomes workgroup memory. Skills become business logic. Agent traces become process intelligence. Over time, they develop or buy the missing System of Intelligence.

The other side says this is not in their DNA.

The frontier labs are research and model-scaling organizations. Enterprise software is a different muscle. It requires long-cycle implementation, governance, domain modeling, integration, change management, procurement patience, compliance, auditability and trust. Building a durable System of Intelligence means encoding how enterprises actually operate – and that is deeply messy.

This camp believes Palantir, Microsoft, SAP, Salesforce, Databricks, Snowflake, ServiceNow, Celonis, Oracle and others have better starting positions because they already sit closer to enterprise data, workflow, identity, systems of record, governance or business process.

But even skeptics of the frontier labs must concede that if OpenAI and Anthropic decide the System of Intelligence is existential, they have the capital, distribution, model utility and talent magnetism to pursue it aggressively through M&A and partnerships.

The question is whether they can absorb enterprise complexity without losing the qualities that made them successful.

The likely market structure

Our view is that the industry will not resolve cleanly.

History suggests the market will fragment across several control points:

| Control point | Likely competitors |

|---|---|

| Model utility and inference economics | OpenAI, Anthropic, Google, Meta, xAI, Nvidia, open model ecosystems |

| Engagement layer | Microsoft Copilot, ChatGPT, Claude, Gemini, Databricks Genie, Snowflake CoWork, SaaS copilots |

| System of Intelligence | Palantir, Databricks, Snowflake, Microsoft Fabric, Salesforce, SAP, ServiceNow, Celonis, RelationalAI |

| Agent governance and routing | Databricks Unity AI Gateway, Palantir Evolve, hyperscaler platforms, model routers |

| Managed outcomes | Palantir, AI-native services firms, vertical operators, GSIs under pressure |

The leaders will capture multiple layers. The most valuable companies will combine model intelligence, enterprise context, governance and permission to act.

That is why the Karp-versus-frontier-lab debate is so interesting. Karp is arguing that Palantir owns the enterprise context and can commoditize the model. The frontier model bull case argues that model utility and economics will become so overwhelming that frontier vendors will eventually own or absorb the context layer.

The truth may be that both sides need each other until they no longer do.

Action item

For CIOs, CTOs and business technology executives, the takeaway is not to choose a religious position on open versus closed models. It is to avoid architectural dependency.

Enterprises should assume a multi-model future. They should use model routers. They should preserve optionality across frontier, open, domestic, specialized and small models. They should separate model choice from enterprise context. Most importantly, they should begin building their own System of Intelligence.

That means capturing:

- Authoritative metrics

- Business definitions

- Policies and permissions

- Process logic

- Decision rights

- Workflow state

- Human skills and tacit knowledge

- Agent traces and feedback loops

The model market will change quickly. The enterprise operating model should not be trapped inside any one model provider.

Bottom line

Karp is right that enterprises need an intermediary layer between raw models and mission-critical operations. The model alone is not the enterprise brain.

The frontier model advocates are right that scale, volume, compute and learning curves are powerful. The best models may become dramatically more capable and cheaper faster than many expect. Tokens may prove far cheaper than labor, and frontier vendors may enable companies to scale revenue without scaling headcount.

The unresolved question is who captures the resulting value.

If the System of Intelligence remains outside the frontier labs, companies like Palantir, Databricks, Microsoft, SAP, Salesforce and ServiceNow will have the opportunity to make models interchangeable and capture the enterprise control point.

If the frontier labs use their scale to build, buy or partner into the System of Intelligence, they could dominate far more of the enterprise stack than today’s skeptics expect.

This is the strategic debate the industry will wrestle with:

Will enterprise AI value accrue to the providers of the most powerful intelligence?

Or to the platforms that understand how each enterprise actually works?

Our answer, for now, is that Enterprise AGI requires both. But the vendor that combines frontier utility with governed enterprise context will win the biggest prize.