Analysts

David Floyer

Stu Miniman

Premise

With the introduction of 3D NAND flash technologies driving flash costs down, the introduction of new protocols such as NVMe and parallel I/O, the introduction of fast system interconnect technologies such as RoCE, and proven performance proof points, Wikibon projects that storage is moving inexorably from traditional storage arrays to Server SAN in a server rack, both for public (hyperscale) and private (enterprise).

Overall Server SAN Results in 2015

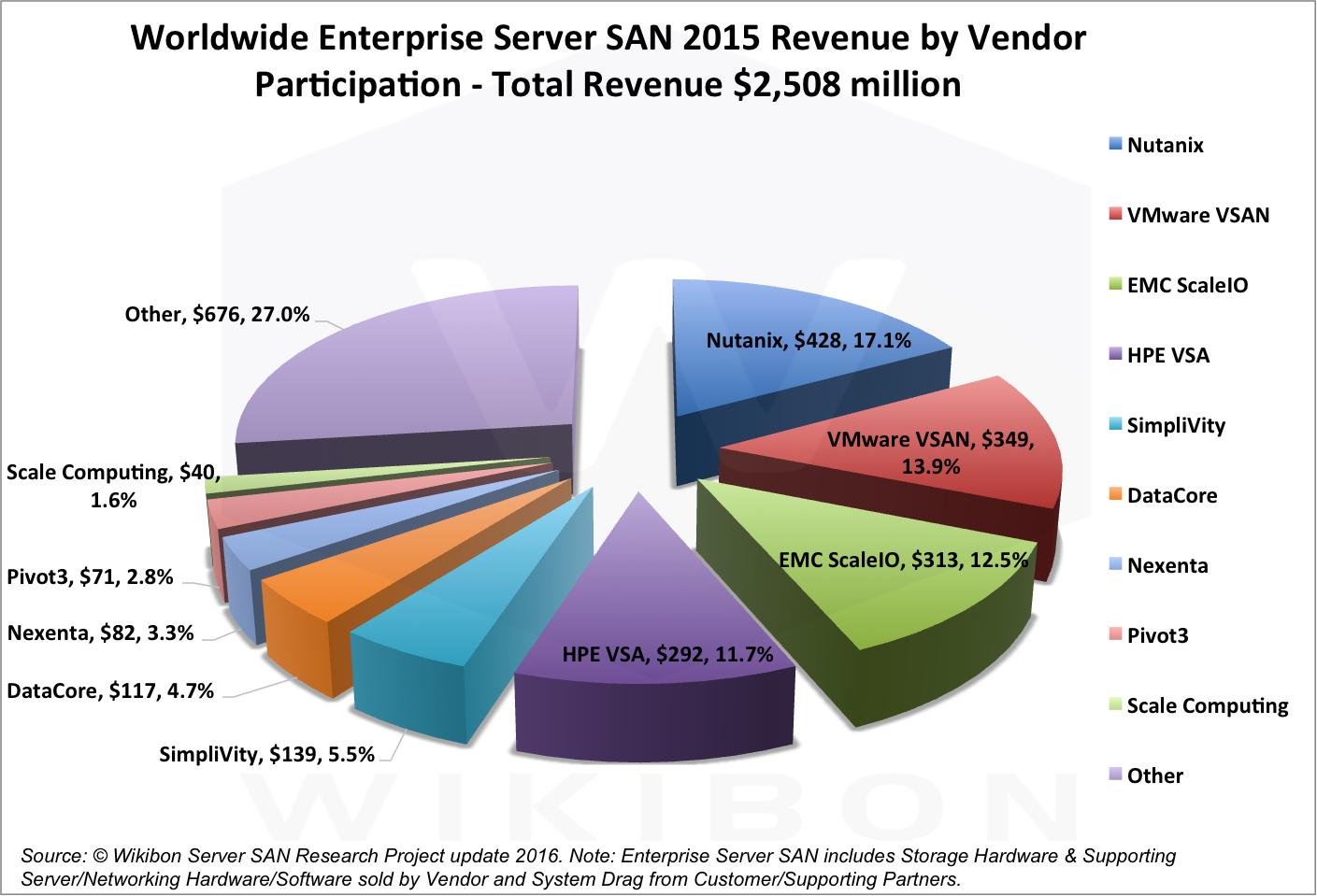

Server SAN (see Footnote1 below for definition) added a $1.25 Billion dollars in 2015, and grew strongly from worldwide revenues of $1.25 Billion in 2014 to $2.50 Billion in 2015. The overall growth was 99%. Figure 1 shows the revenue by vendor. The top three vendors were Nutanix (17%), VMware VSAN (14%) and EMC’s ScaleIO (12%) by a nose from HPE VSA (12%). The top three account for 43% of the market. EMC ScaleIO had the most explosive growth of over three and half times (3.5x) from 2014 to 2015. SimpliVity and DataCore also have passed the $100M mark with the inclusion of System Drag. “Other” include other Server SAN US-based vendors: as the entry to delivering Server SAN solutions is not high, “Other” also includes an estimate of revenues from Server SAN products in other countries that have not make it to the USA (particularly from China, Japan, India and and Europe).

Source: © Wikibon 2016

Detailed Review of Server SAN Vendors and Products

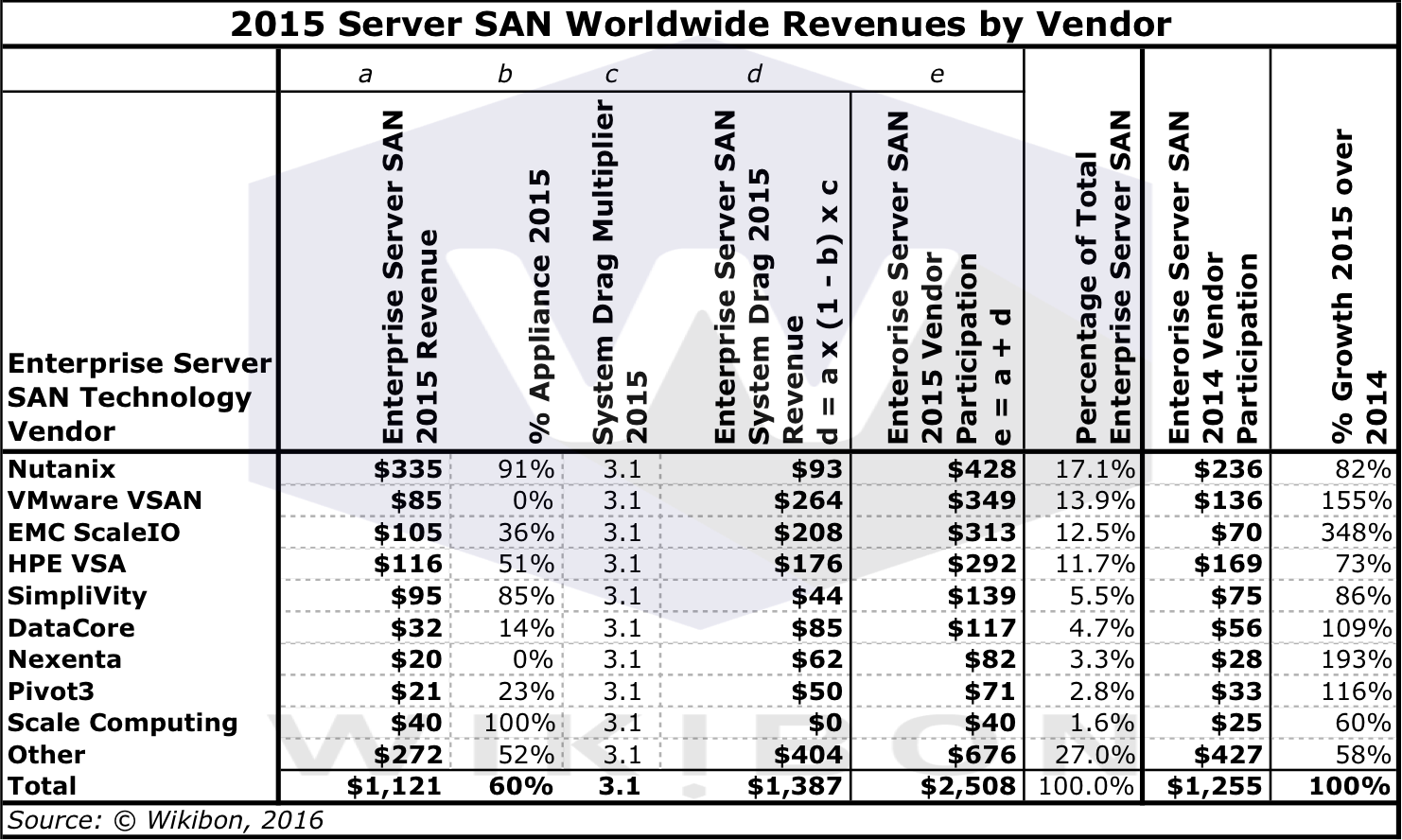

Table 1 looks in more detail at the composition of the figures. The first column shows the direct worldwide revenue by vendor for 2015 from Server SAN software and hardware. The second column (b) shows the percentage of the revenue in column (a) that is shipped as an appliance by the vendor.

The normal practice in defining market segments is to define revenue as purchases by the final users. In the case of Server SAN, this would be the major companies such as Lenovo, Dell, HPE and others that integrate the Server SAN software into their own converged solutions and sell to enterprises of service providers. As Server SAN is an emerging market, Wikibon has chosen for the time being to allocate this revenue to the technology vendor who sells the underlying technology software and hardware. The reason for this choice is to track what technologies and technological functions are growing. Column (c) in Table 1 shows the uplift for “System Drag”, which has increased from 1.8 in 2014 to 3.1 in 2015. The same figure is used for all vendors. Column (d) is the calculation of this uplift from columns a, b & c (see Table 1 for detailed calculations). Column (e) in Table 1 is the sum of columns (a) and (d).

Source: © Wikibon 2016

- Nutanix remains the revenue leader and has continued strong growth despite the entrance of many competitors, including the attention of the sales forces of large storage players. Nutanix has expanded and enhanced its offering to include a SMB solution and an increased focus on software. Nutanix’s software includes a native “free” (open-source based) hypervisor and expanded management tools. Growth is also coming from reseller agreement with Dell, Lenovo and others.

- VMware is core to the Server SAN market, both through its dominant position in the hypervisor market (used on most appliances), and the strong growth of VMware VSAN. The majority of VSAN deployments in 2015 were VSAN Ready Nodes, which are solutions built primarily by server vendors following basic guidelines from VMware. The single SKU VSAN option EVO:RAIL was less popular, phased out, and has been replaced by the VxRail product which is created by EMC and VMware (and is expected to leveraged Dell servers once the Dell/EMC acquisition is completed). With over 5,000 customers (only 1% of VMware’s customer based), the solution can claim to be the most widely deployed in this category.

VMware has an opportunity for very rapid growth in Server SAN. VMware has a large installed base for which the friction for selling VSAN is low. However, VMware is/will be managed by EMC/Dell, and EMC has previously prioritized VMware storage investments that have helped EMC storage sales to sell traditional storage arrays with much higher margins. As a result, VMware VSAN has been slow in coming out. If that strategy is continued, there is significant risk that VSAN functionality will fall behind other Server SAN competitors, and the opportunity to add storage virtualization and dominate the VMware ecosystem will be lost. Performance is a critical component which will be under scrutiny.

- EMC ScaleIO The most outstanding growth came from the EMC ScaleIO platform, which has grown 385% in the past year. ScaleIO has been successful with very large deals, particularly in the telecommunication market. The integration into VCE’s VxRack as a converged solution for large-scale block implementations has also been very successful. ScaleIO is the most functionally rich Server SAN product in the market. Wikibon has the same concerns that EMC/Dell may not prioritize technical and marketing investments in this new areas that conflicts with current traditional array products. Server SAN platforms will take all the top spots in performance benchmarks in the later part of 2016 and beyond, and Datacore (see below) is number 1 in SPC-1. Wikibon believes that ScaleIO should and will outperform all array-based architectures, including EMC’s VMAX and ell’s range of storage arrays. The opportunity to gain market share with ScaleIO is a one-time opportunity.

- HPE StoreVirtual VSA continues to do well in the Server SAN market as a result of being packaged and sold by HPE’s server division. HPE also does well in selling other Server SAN products, but at the moment Wikibon recognizes this revenue under the core technology.

- SimpliVity has developed extremely sophisticated and efficient file-system that enable backup and recovery to be completely integrated at the application level. This allows applications to be deployed at levels of availability only matched by Oracle, at a fraction of the cost. However, finding ways to sell this concept to enterprise IT is proving difficult for SympliVity. When sold, SympliVity achieves very high marks from its customers.

- Microsoft Storage Spaces has had a slow ramp, but is expected to ramp up in 2016 and onwards. Server and storage vendors are expected in develop integrated solutions, such as Dell Storage with Microsoft Storage Spaces.

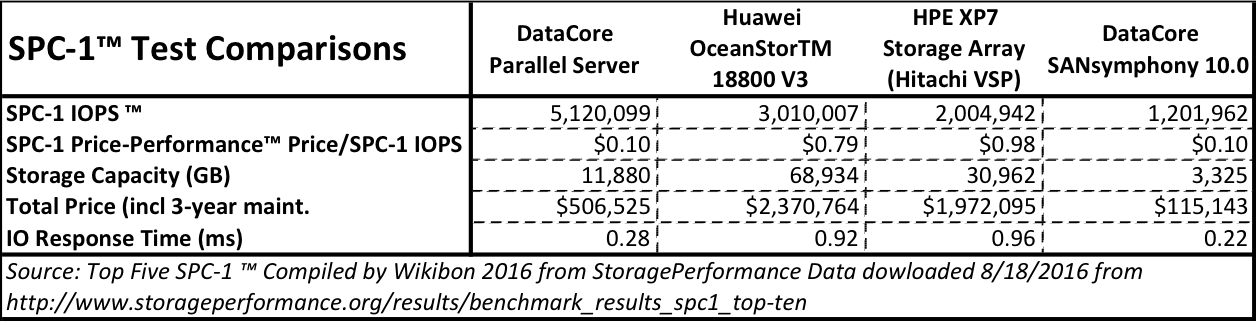

- DataCore created a world record in 2016 for the SPC-1 benchmark of 5.1 million SPC-1 IOPS, beating Huawei with 3.0 million, and Hitachi/HPE with 2.0 million (see Table 2 below). Even more impressive is the price performance (1/8th of nearest competitor) and the IO response time (280 microseconds average). This was built on Datcaore’s parallel I/O technology, which exploits the bandwidth and cores of the latest Intel chips. This type of parallel performance innovation of the IO code is the first of many in the pipeline, and is the result of tighter integration between the server and storage layers. This is a good illustration of the new levels of performance that is being achieved by moving the storage much closer to the server. Wikibon expects that Server SAN platforms will dominate all storage benchmarks from late 2016 and onwards.

- Pivot3 is a major player in the digital surveillance market, but is now achieving about 50% of its revenue from integrated systems which include Server SAN. It has brought over its expertise in storage handling for the cost sensitive surveillance marketplace (using highly efficient erasure coding) into Server SAN.

Source: © Wikibon. Top Five SPC-1 ™ Compiled by Wikibon 2016 from StoragePerformance Data dowloaded 8/18/2016 from http://www.storageperformance.org/results/benchmark_results_spc1_top-ten

- Permabit is the leading supplier of compression, deduplication and thin provisioning technologies to storage array vendors to include in their proprietary controller stacks. Permabit has now made available this same code in a software package (VDO 6) for Linux, expanding availability beyond the OEM marketplace.

- Mellanox is the leading supplier of RoCE (pronounced “rocky”, RDMA over Converged Ethernet), which is a remote memory management capability allowing server to server data movement directly between application memory without any CPU involvement. RoCE provides this efficient data transfer with very low latencies on lossless Ethernet networks using 10GbE, 25GbE, 40GbE, 56GbE and 100GbE. The Mellanox NICs include hardware offload, and enables sub-2 microsecond ultra-low and ultra-consistent latency. This capability and performance brings Server SAN vendors a completely new sets of tools for high performance and high availability applications. The resultant database environment allows faster processing times for end-users or contingent processes, and the ability to process two orders of magnitude (100 times+) more data in the same time. This means that modern applications can give far greater productivity to consumers and enterprise users from faster consistent response times and vastly improved applications.

Reason’s for Server SAN Growth

Server SAN leads to improved application design, improved application operation, a wider range of application performance options and lower infrastructure costs. The major reason is that instead of the operating system for storage management being held in proprietary code in storage array controllers, the code is now part of the Linux ecosystem, and there is incentive and a much larger market for innovation. The three examples above from Server SAN in 2016 illustrate the opportunities and potential for the Server SAN ecosystem to provide new functionality at much lower costs.

Server SAN can serve both the high performance and the high capacity marketplaces, both scale-out and scale-up). One fundamental architectural problem of traditional storage arrays is that storage management is built into the array stack. Software-led Storage architectures such as Server SAN separate the storage from storage management, and allows both markets to flourish independently.

Server SAN will also integrate into other software-led infrastructure initiatives such as the orchestration layer of OpenStack, allowing greater choice and lower software costs. The use of Server SAN in open hardware stacks such as the Open Compute Project, especially together with software stacks like OpenStack, will enable enterprise data centers to be cost-competitive with hyperscale vendors and cloud service providers such as AWS.

ISVs now has every incentive to write applications for Server SAN, knowing that this technology can be brought to bear to solve many performance problems. They will be able to focus on creating more value within their applications for the cloud and for on premise systems, rather than constraining design to meet old storage array architectures.

The simplification of storage with Server SAN will lead to higher levels of convergence and automation, and enable much more productive, flexible organizational structures such as Dev/Ops and Cloud/Ops to deliver application value to the business.

Server SAN Projections

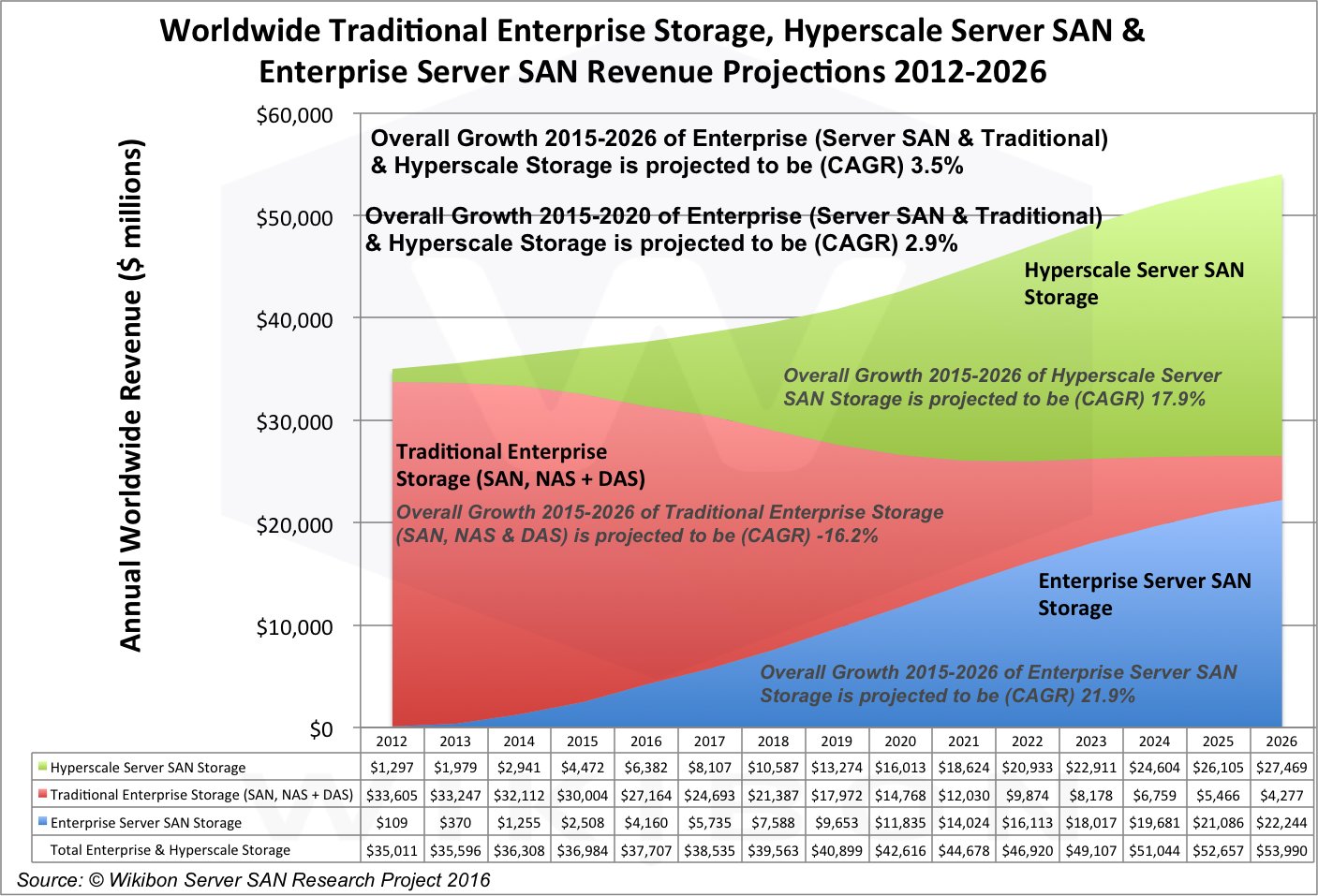

Wikibon has updated its Server SAN Projections in Figure 2 below from the last update in July 2015. The overall worldwide market for enterprise storage consists of three sectors:

- Enterprise Server SAN is projected to grow worldwide revenue at 22% CAGR from 2015-2026, from $2.5 Billion in 2015 to $22 Billion in 2026.

- Hyperscale Server SAN (developed initially by cloud service providers, moving to mainly volume storage vendors by 2026). This is projected to grow worldwide revenue at 18% CAGR from 2015-2026.

- Traditional Enterprise Storage (SAN Storage Arrays, NAS Filers and DAS). This market is projected to decline worldwide revenue by -16% CAGR from 2015-2026.

The overall storage market is projected to grow at 3.5% overall, the increase being driven by the higher value to users of storage because of rapid advances in performance and functionality driven by Server SAN and flash volumes.

The overall Server SAN market (Hyperscale + Enterprise) is projected to grow worldwide revenue at 22% CAGR between 2015 and 2026, from $7 Billion to $50 Billion. This will increasing become one market, as technologies cross-pollinate functionality, performance and cost reduction.

Wikibon now expects the hyperscale cloud market and the enterprise storage market (Enterprise Server SAN and Traditional Storage) to be roughly similar by 2026 at $27 Billion each. This has been updated in line with the Wikibon 2016 Public Cloud Forecast, and the storage figures extracted from the projections using the same methodology described in the Wikibon July 2015 Server SAN update. Other relevant research is Server SAN: Hyperconvergence into the Majority.

Wikibon expects that distributed edge Server SAN will become a significant portion of Enterprise Server SAN, to support the adoption at the edge of the Internet of Things. These will interconnect to mega-datacenters that are using an increasing amount of Hyperscale Server SAN and colocated enterprise Server SAN. These mega-datacenters will connect cloud services and collocated Enterprise Server SAN with fast secure hyper-networks. In turn, the mega-data centers will connect to Enterprise private/hybrid/edge clouds to support local enterprise storage and processing.

Source: © Wikibon 2016 Server SAN Project

Action item

Wikibon strongly recommends senior enterprise executives make strategic partnerships with vendors who can provide and support complete converged infrastructure server and Server SAN hardware, Server SAN software, and services, with a single hand to shake and a single throat to choke. 2016 should be the year Server SAN initiatives are installed for evaluation and production.

Footnotes

Footnote1 – Server SAN Definition

Wikibon has previously defined Server SAN as a combined compute and pooled storage resource comprising more than one storage device directly attached to separate multiple servers (more than one). Communications between the direct attached storage (DAS) occurs via a high speed interconnect (such as InfiniBand or RoCE on Low Latency Ethernet), where data coherency is managed by the software of the solution. Server SAN multi-protocol storage can utilize both spinning disk and flash storage. Server SAN is configured in enterprise applications to ensure high availability.

Footnote2 – Minor changes made to text and data 9/9:2016 and text on 11/1/2016. df