Premise:

While the Cloud Computing market is still relatively young (active since 2009), some major trends have emerged that are dictating the new buying models and technology usage patterns of customers. As of now, no single vendor has a perfect Public Cloud + Private Cloud offering. Instead, most offerings have strengths and weaknesses in one of those two areas. To be successful, vendors need to understand where they can successfully compete and where they may need to alter their strategic plans to enhance their areas of weakness.

As the role of IT changes over the next decade, the ability for vendors to succeed in this market segment will have a significant impact on the overall success of their company. Failure to succeed in Hybrid Cloud will likely lead to the overall failure of those companies to transition from traditional IT to Digital Business Platforms.

NOTE: All Wikibon research on Hybrid Cloud – http://wikibon.com/?s=Hybrid+Cloud

Overall Market Dynamics:

The IT industry is undergoing a wave of significant change as customers transition from traditional IT applications to cloud-native platform applications. This transition is impacting applications, infrastructure and operations for both vendors and customers. As EMC’s CEO David Goulden stated in the Q4’15 earning call, “Customers are buying ‘just enough’ & ‘just in time’ for their traditional environments.” This transition signals that customers are beginning to reshape their thinking about IT to more closely align to the experiences and expectations of the Public Cloud, rather than traditional IT buying experiences. IT vendors need to be more aware of this shift and reshape how they will compete as the rules of the games are rapidly changing.

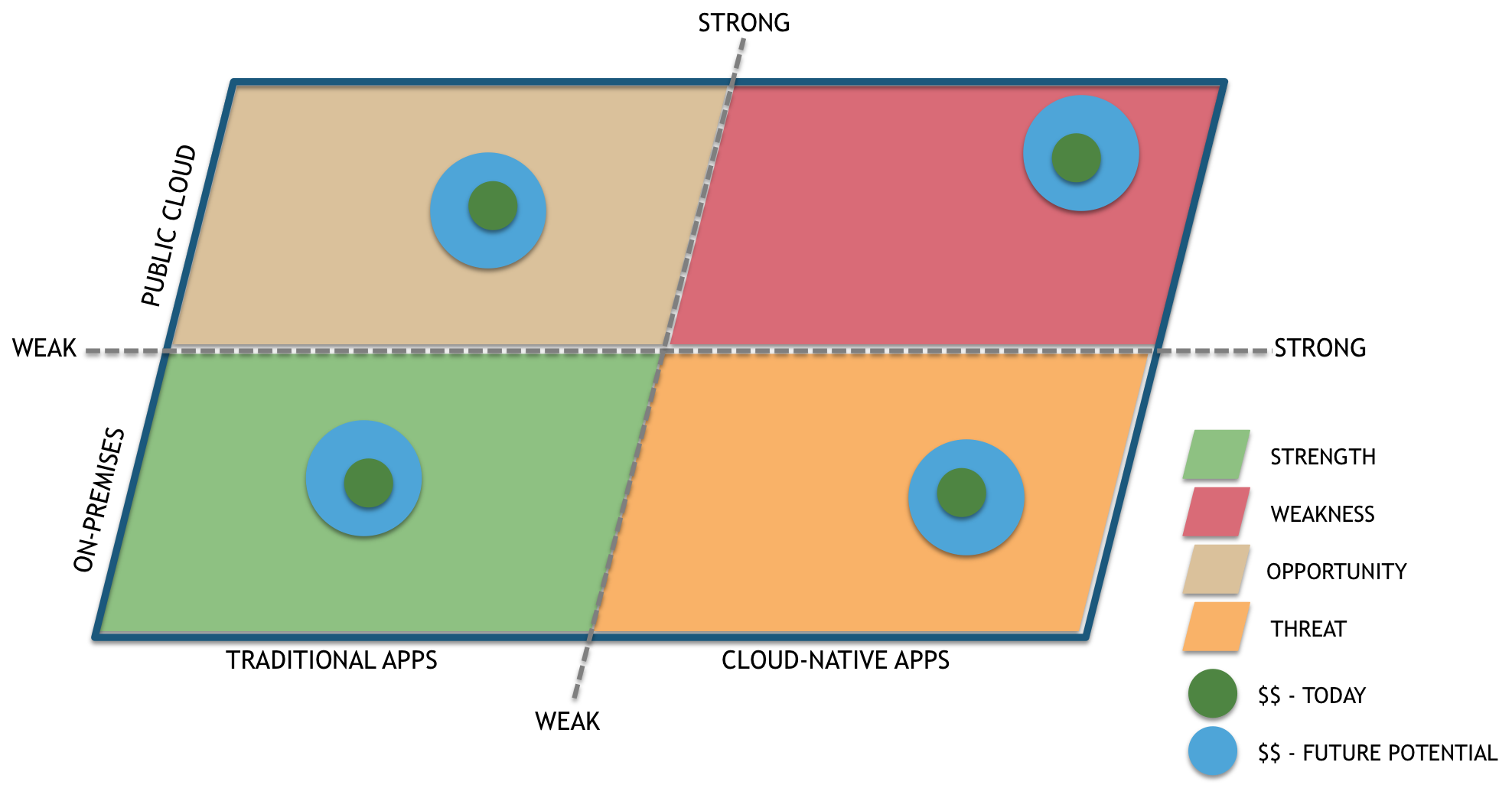

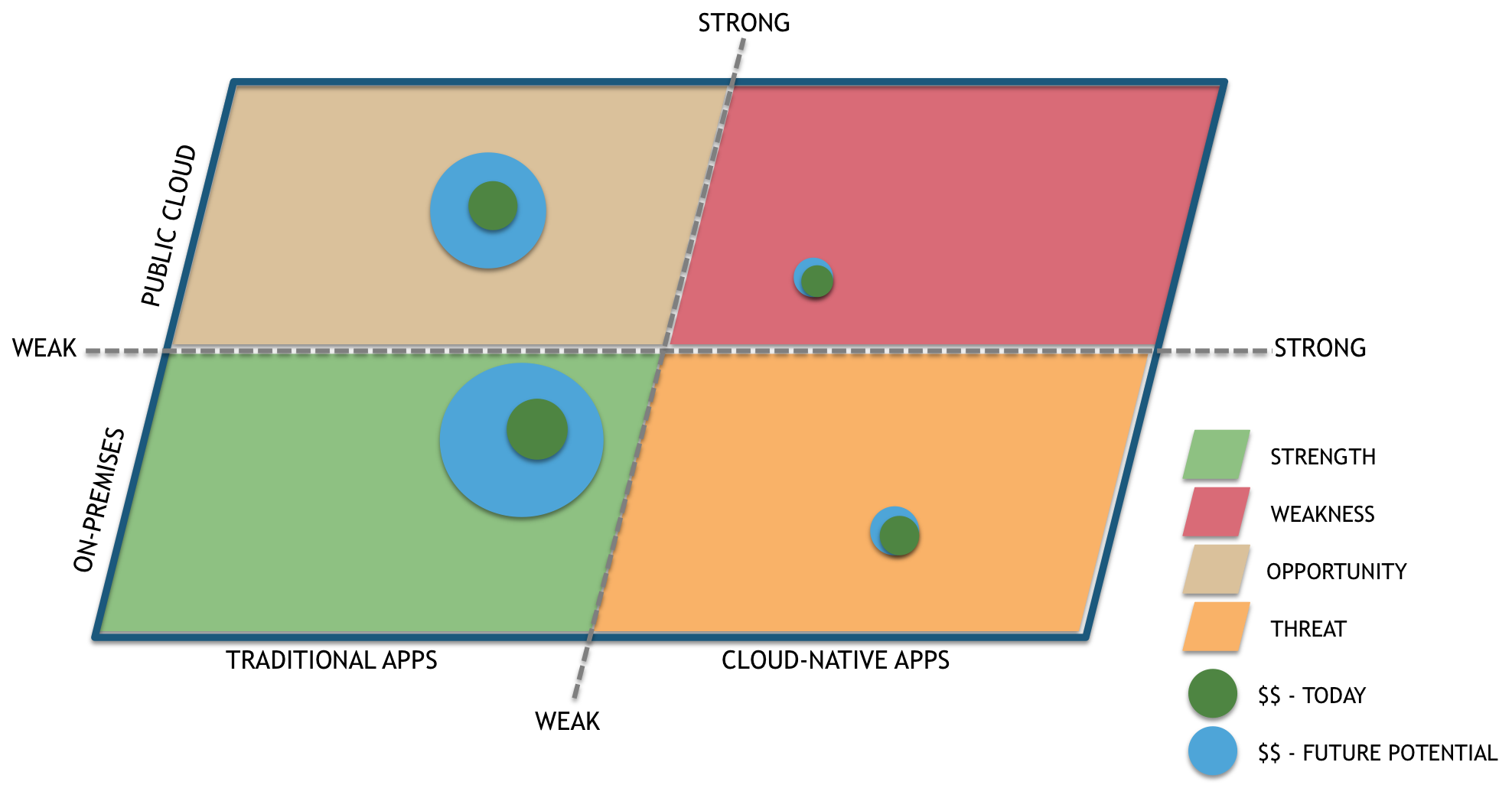

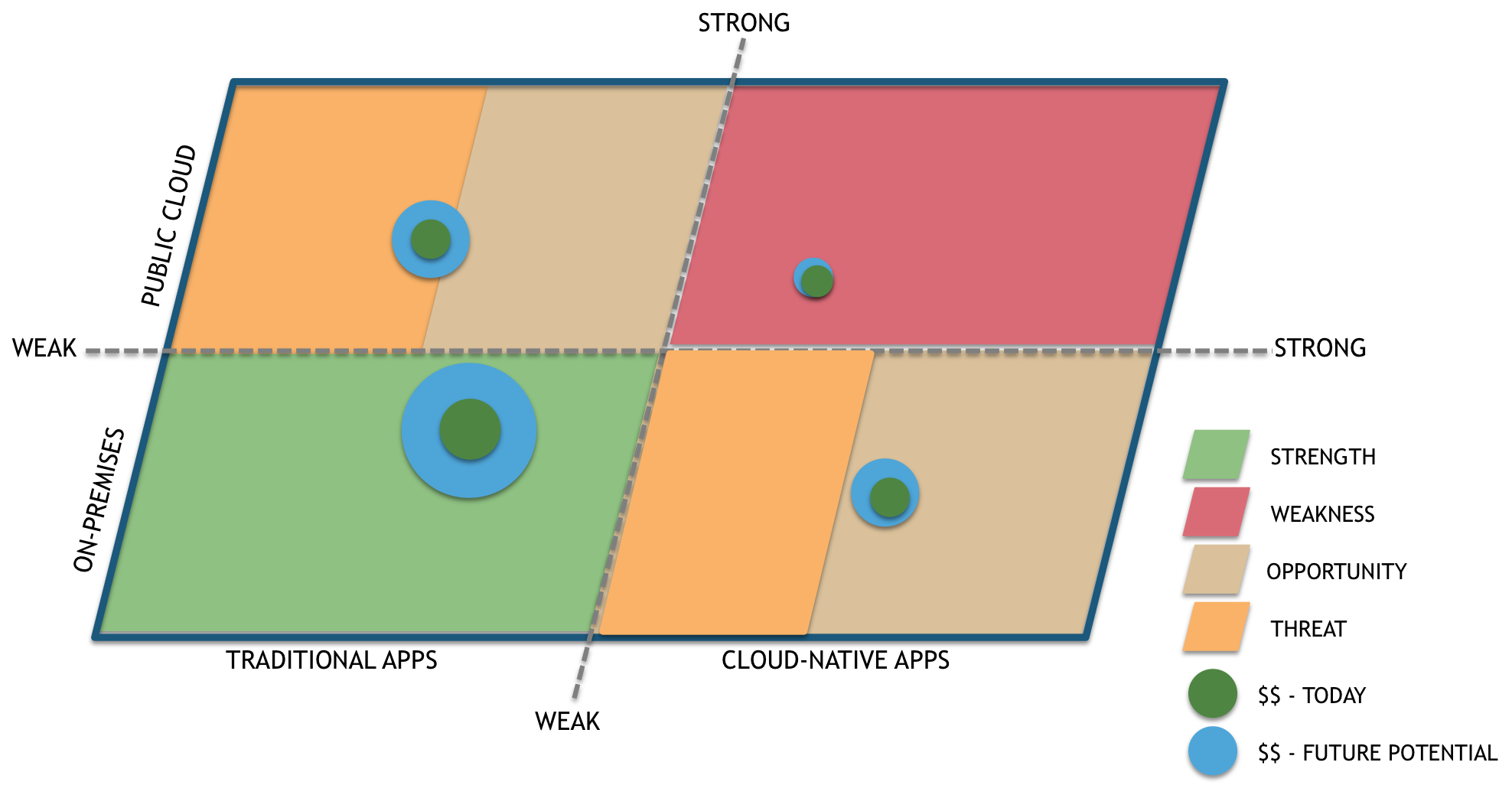

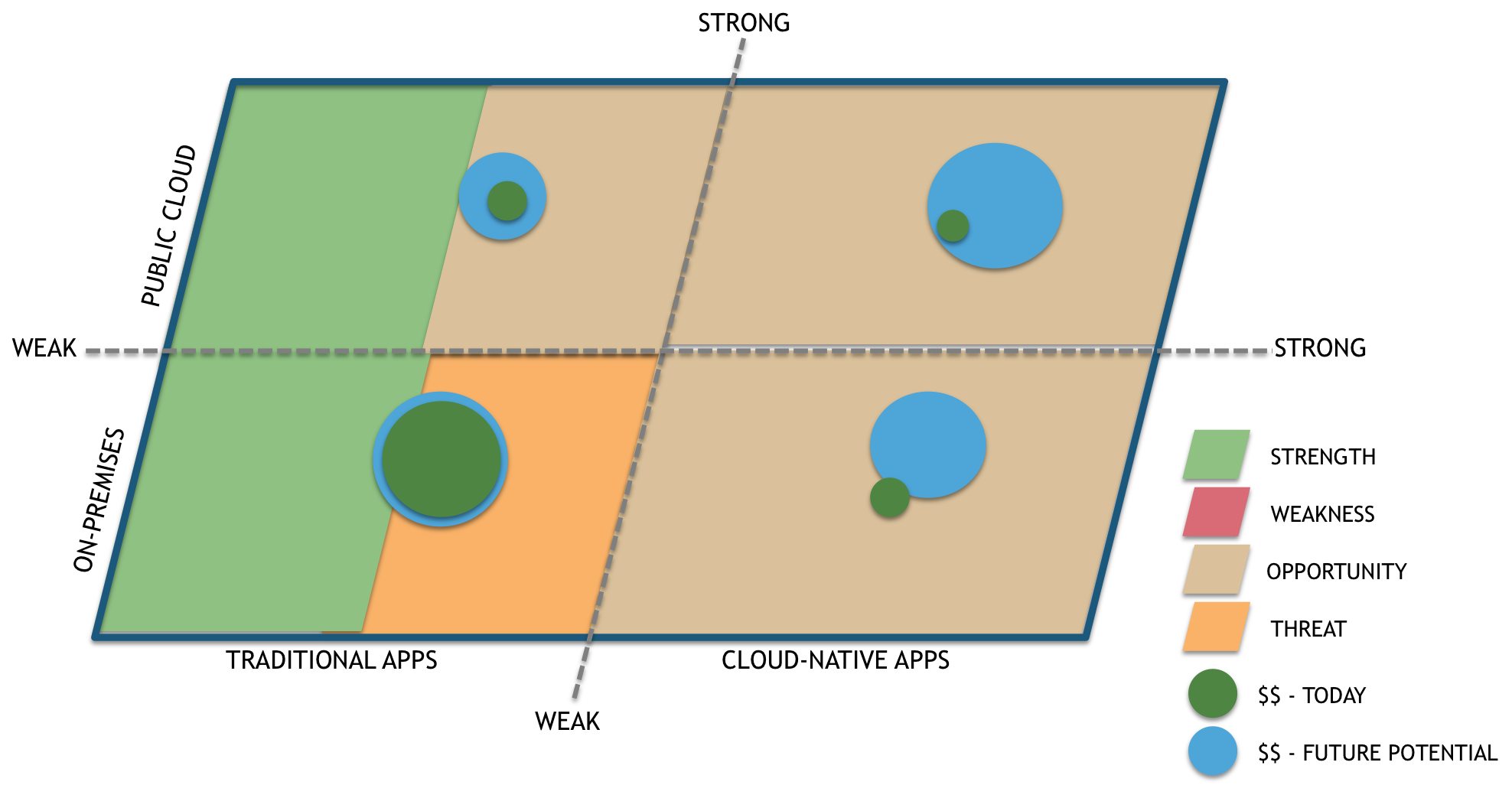

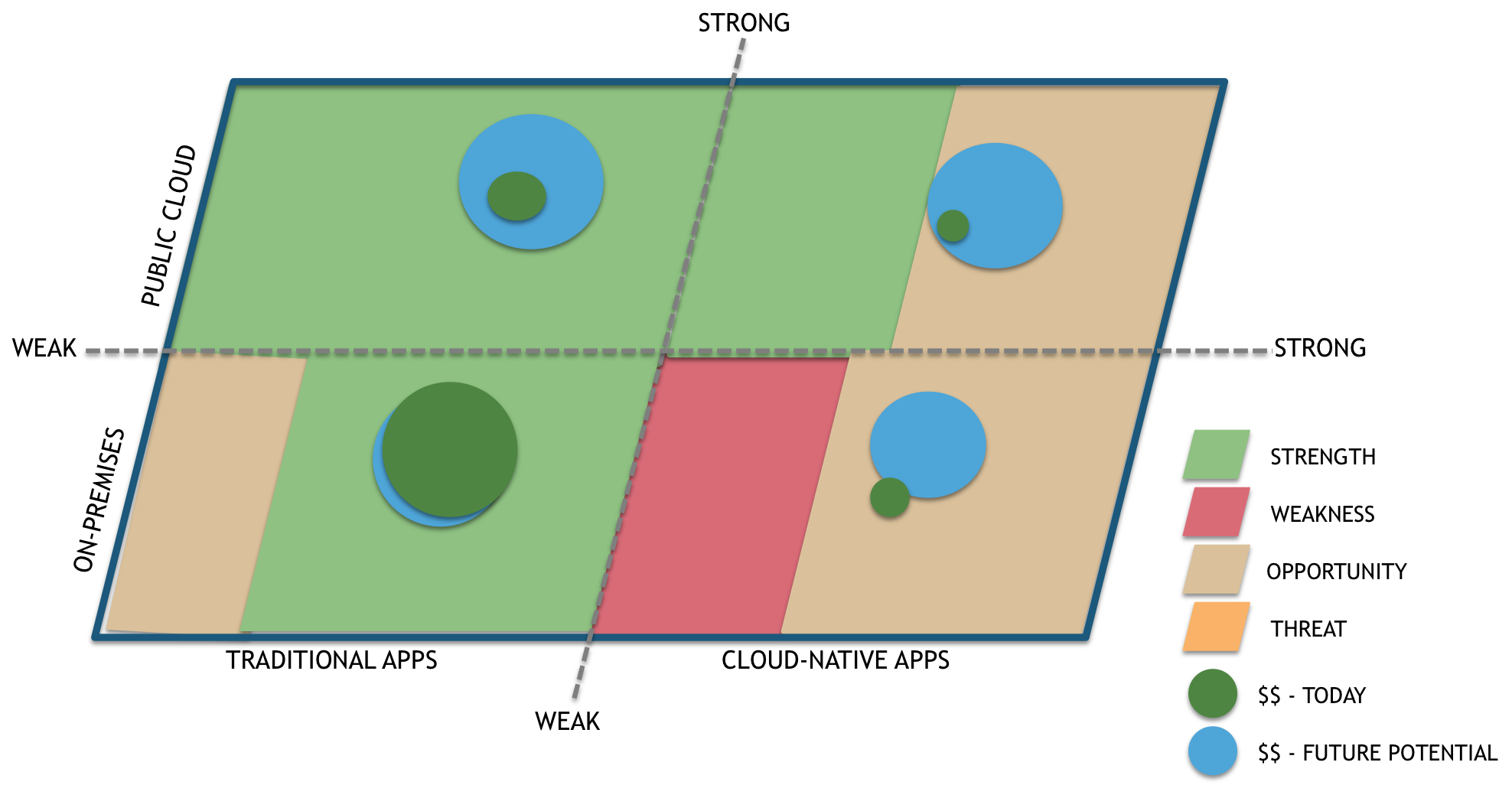

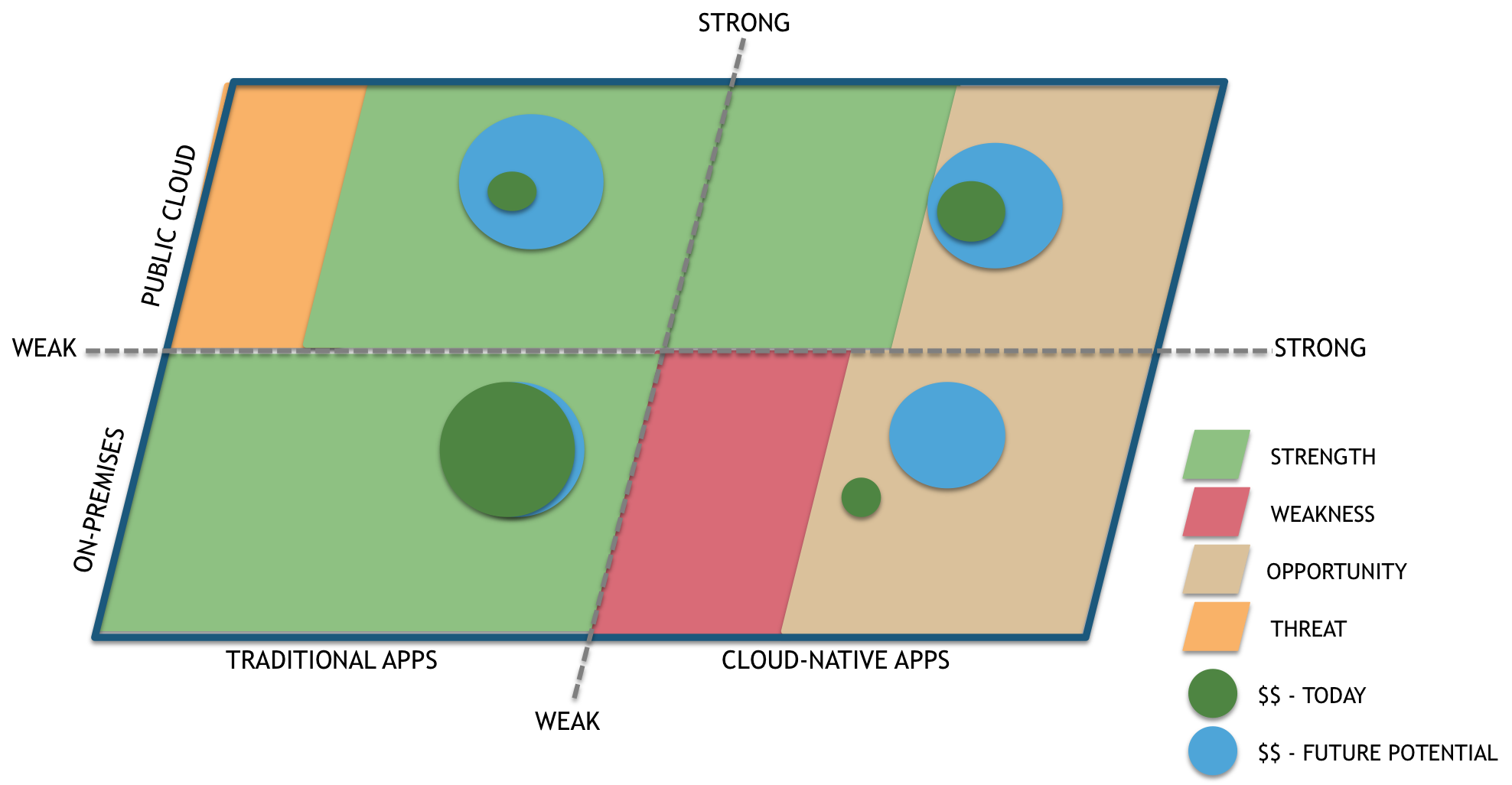

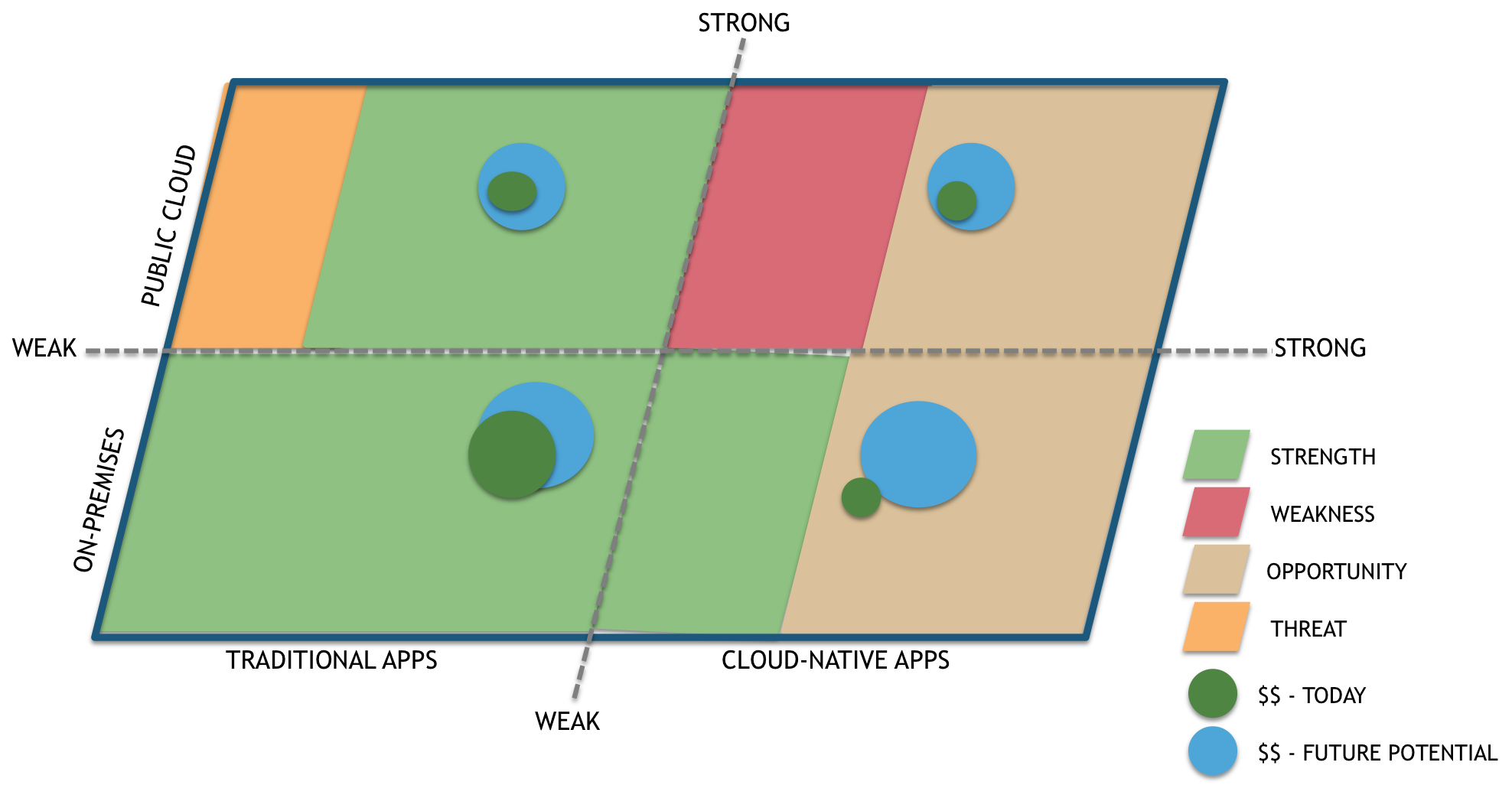

Wikibon Disruption Dimensions – Today’s Solution & Tomorrow’s Opportunities

Evaluating multi-dimensional offerings from the perspective of now and multiple years into the future can be a difficult task to visualize. To try and simplify that challenge, Wikibon introduces the “Disruption Dimensions”. This visual looks at a given vendor’s offerings across multiple dimensions:

- Traditional applications vs. Cloud-native applications

- On-premises offerings vs. Public Cloud offerings. NOTE: For on-premises offerings, Wikibon is primarily focused on solutions that align to the True Private Cloud definition.

- Across either of those dimension, a scale between “Strong” and “Weak” is plotted based on current market offerings and the potential of future offerings. NOTE: Future offerings are based on known roadmaps or Wikibon’s anticipated trajectory for the vendor given existing resources and capabilities.

- The size of the “$$” values are relative to the overall market, unless specifically identified within the vendor’s research section.

- The color-coding of the section aligns to Wikibon’s analysis if that area is primarily a Strength, Weakness, Opportunity or Threat. NOTE: It’s possible that some vendors may not have all SWOT aspects represented in the Dimension.

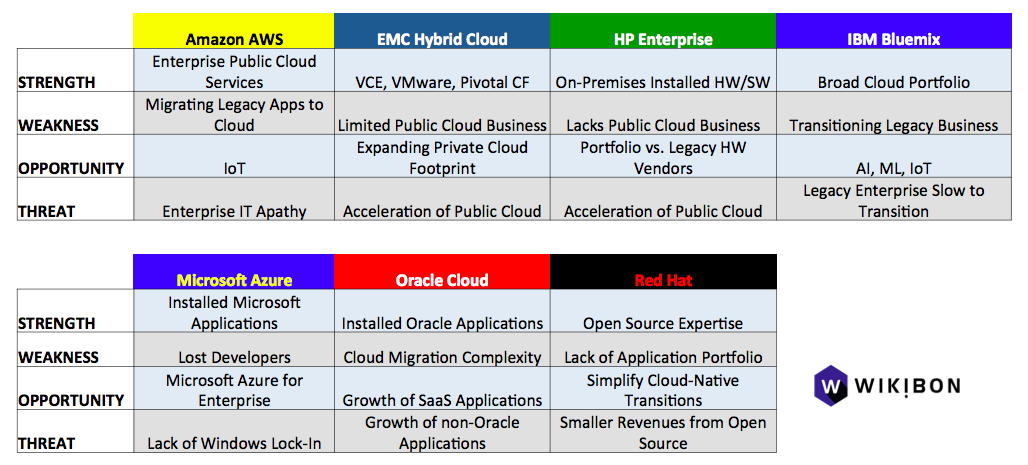

Hybrid Cloud Services and Solutions

Within this research, Wikibon created SWOT analysis of the follow Hybrid Cloud offerings.

- Amazon Web Services

- EMC Hybrid Cloud Solution

- Hewlett Packard Enterprise

- IBM Bluemix

- Microsoft Azure

- Oracle Cloud

- Red Hat

NOTE: Google Cloud Platform is not included in this research because at this time they do not have a stated Hybrid Cloud strategy.

Amazon Web Services

Solution: https://aws.amazon.com/enterprise/hybrid/

Overview of Solution: Amazon Web Services (AWS) is the leading global Public Cloud for IaaS and PaaS services. AWS delivers on-demand (OPEX), modular services that can be consumed individually or integrated together. AWS is currently #1 in Public Cloud IaaS/PaaS revenues.

Cloud Revenues: FY2015 – $7.9B

Solution Target: AWS services are targeted at companies that wish to have simpler access to scalable, IT resources that are globally available. AWS initially targeted startup companies, but has expanded to offer a set of services that appeal to Enterprise, Gov’t, Mid-Market and SMB customers. AWS focuses on customers that are trying to grow their business, rather than have a primary focus on cost-reduction in IT. They also seek to attract new developers targeting multi-language/multi-platform next-generation applications such as Mobile, Data Analytics, Machine Learning (ML), Artificial Intelligence (AI), and Internet of Things (IoT).

Target Audience: AWS primarily targets application developers, with the goal of disintermediating IT organizations or common IT operational functions. AWS targets organizations that are building new or updated applications.

Strengths:

- Largest Public Cloud provider in terms of revenue and scale of resources.

- Highly profitable business (28% Operating Margin, Q4’15) that has been expanding profitability as it expands and scales.

- Broadest portfolio of Public Cloud IaaS / PaaS / Data services in the market.

- Continues to rapidly innovate and add new services to their portfolio on a monthly or quarterly basis. Quickly filling in holes to attract Enterprise customers.

- Multiple pricing models from on-demand to reserved/spot pricing to longer-term contracts.

- Customers are not required to own any physical assets (equipment, data centers)

- AWS is able to offload the cost of human resources (IT staff) by 1/10th the price through automation of services (e.g. DBA or Storage Admin in their RDS service).

- Frequently reduces prices to drive new/additional demand.

- Extremely strong brand – all other Cloud experiences are compared to AWS.

Weaknesses

- AWS Compute and Network performance has frequently (here, here) been shown to be behind other leading Public Cloud providers. NOTE: Wikibon does not perform independent performance testing, so individual customer experience may vary.

- AWS list pricing is frequently higher than both Google Cloud Platform and Microsoft Azure for Compute and Storage services.

- AWS pricing can be complicated to understand (many services, different prices) and costs can grow unexpectedly if customers do not actively pay attention to usage.

- While they are very well documented, AWS APIs and Services are not open-source, so it can be complicated to move applications or data off of the AWS cloud.

- AWS ability to run Oracle and SAP applications/databases in the manner defined in their best practices often require many work-arounds for security, networking and licensing.

- Outside of VPC and Storage Gateway, AWS does not manage on-premises resources for customers. This creates a very different experience for AWS-managed resources and customer-managed resources.

Opportunities

- Shadow IT – As more companies are dissatisfied with internal IT organizations, AWS can capture more Enterprise business by being a better (faster, cheaper, more services) IT alternative.

- Wikibon forecasts that Public Cloud will be 1/3rd of all IT spending within 10 years.

- Many traditional IT vendors are struggling (EMC, Dell, Cisco, HPE, VMware, Oracle) with growth, margins, and re-organizations. Customers may seek alternative vendors for new projects.

- The IoT market is still nascent and no leaders have emerged. This is a huge opportunity for AWS to capture the next-generation of Internet growth.

Threats

- Growing in the Enterprise will be more difficult than with startups. Enterprise and government customers have different buying patterns, different buyers, different selling expectations, etc.

- There are increasing global concerns about data sovereignty (location of data) vs. the locations of AWS data centers. Does this limit the markets (in Europe, Asia, South America) that AWS can capture?

- The cost of building new data centers to expand capacity is very capital intensive, which could reduce margins.

- Lack of existing IT/customer skills for new tools/technologies. AWS does provide a wide range of training (directly and indirectly), but learning can take long periods of time.

- Oracle, Google, Microsoft have large cash reserves to compete with AWS, as well as existing application portfolios that can be leveraged to influence customer-buying decisions.

EMC Hybrid Cloud (EHC) Solution

http://www.emc.com/en-us/cloud/hybrid-cloud-computing/index.htm

Overview of Solution: EMC’s EHC brings together technology from across the EMC companies (EMC, VCE, VMware, Pivotal) into a single Hybrid Cloud solution. The solution is primarily focused on delivering a turn-key Private Cloud to enterprise customers, with the ability to broker services from multiple Public Clouds (AWS, Azure, vCloud Air, Virtustream).

NOTE: This research is focused on the EMC Enterprise Hybrid Cloud (EHC) solution. EMC announced the Native Hybrid Cloud (NHC) solution in May 2016. The NHC offering is not scheduled to be GA until the end of 2016, so it will not be covered in this research. Wikibon did provide initial coverage of the solution at the time of EMC World 2016.

Cloud Revenues: Not explicitly reported by EMC/VMware/Pivotal – Wikibon True Private Cloud forecast/estimates.

Solution Target: IT Leadership focused on transforming IT to a more cost-effective, more responsive organization for their business. Infrastructure-as-a-Service (IaaS) solution with integrated Data Services, with the ability to add additional services through PaaS (Native Hybrid Cloud) and Data Lake offerings.

Target Audience: Infrastructure and Operations Teams

Strengths

- Industry leading technologies: Converged Infrastructure (VCE), Storage (EMC), Virtualization (VMware) and Platform-as-a-Service (Pivotal Cloud Foundry)

- Large installed base of VMware customers – small learning curve to adopt Private Cloud technologies.Leading PaaS platform (Pivotal Cloud Foundry) with the largest level of Cloud Foundry contribution (65% – http://stackalytics.com/?project_type=cloudfoundry-group&release=all&metric=commits)

- Integrated Data Services for Backup and Disaster Recovery

- Solution is not application-dependent. Will support multiple types of traditional and cloud-native applications.

- Single Call for Technical Support across the entire EHC solution.

- EMC Adaptivity software allows customers to have a blueprint for application migrations and modernizations.

Weaknesses

- CAPEX-only solution. Does not have (readily available) options to consume the solution in an OPEX model. Pricing is not granular across any domain (compute, storage, services).

- Uncertainty about the EMC Public Cloud strategy with the changes in the VMware/Virtustream alignment. Virtustream has limited global footprint (data centers) and lacks the rich developer-centric services available in leading Public Cloud offerings.

- VMware has separate cloud partnerships with Google Cloud Platform and IBM Cloud.

- Pivotal has separate cloud partnerships with CenturyLink, Microsoft Azure and several other service providers.

- EHC’s Public Cloud portion of the solution is limited. VMware vCloud Air has limited functionality and AWS and Azure brokerage is limited and expensive (often requires EMC Professional Services engagements).

- VMware vRealize management software is not widely adopted by VMware customers (approximately 17% attachment rate to ESX licenses, per VMware financial reporting)

- Even with some application-specific services (Pivotal Cloud Foundry, VMware Codestream), the solution is primarily targeted at Infrastructure/Operations teams, not application or developer teams.

- EHC solution is marketed as a set of individual technologies and products, not “services” to be consumed by the customers. Lacks a focus on vertical markets or solutions at the application-layer.

- EHC solution is slow to add new functionality (6-12 months between releases) and does not have a way to add new functionality in a modular way.

Opportunities

- Target customers in industries that are highly regulated and prefer Private Cloud.

- Target the uncertainty surrounding Hewlett Packard Enterprise and lead with Converged Infrastructure transformation as a way to move towards Private/Hybrid Cloud.

- Focus on customers with existing VMware installations (HP, Dell, Cisco, Lenovo customers) where existing IT skills can drive decision-making.

- Continue to integrate the Virtustream public cloud platform to build hybrid cloud offerings.

- Highlight that EHC can work across a broad range of applications – against Oracle, Microsoft, SAP.

- Highlight that EHC requires the least amount of changes to applications (AWS, Azure) or Infrastructure (IBM/x86, Microsoft/Hyper-V, Oracle/OracleVM

- Use Pivotal Cloud Foundry as an entry point for “digital transformation” and cloud-native application development.

- Leverage EMC Adaptivity to reduce the risk/cost of IT Transformation.

Threats

- The market is uncertain about the pending EMC/Dell acquisition and may look to alternative solutions for longer-term stability.

- Customers still have to operate the Private Cloud. Limited cost reductions unless they adopt highlight automated operations (and reduced headcount)

- Application teams are beginning to hold greater levels of budget and choose to use Public Cloud (AWS, Azure) for new applications and digital transformation.

- Limited Public/Hybrid Cloud capabilities lead customers to go directly to Public Cloud (instead of via brokerage)

- Customer skip the Private Cloud transformation and focus on VPC between existing applications and Public Cloud

- Application teams may not want to adopt Cloud Foundry on Neutrino Nodes. This would introduce OpenStack, which is another operational unknown. Consider VMware technologies instead (VMware Integrated Containers; Photon Platform).

Hewlett Packard Enterprise (HPE) – HPE Helion

http://www8.hp.com/us/en/cloud/helion-hybrid.html

Overview of Solution: HPE current Private/Hybrid Cloud solution is based on a combination of HPE Helion (OpenStack + Cloud Foundry), HP Synergy Converged Infrastructure, and HP OneView management. HPE no longer operates a Public Cloud service (discontinued in 2015) and their strategy is now focused on brokering to Public Cloud services from AWS and Microsoft Azure, as well as HPE service providers.

Cloud Revenues: Not explicitly reported by HPE – Wikibon True Private Cloud forecast/estimates.

Solution Target: IT Leadership focused on transforming IT to a more cost-effective, more responsive organization for their business. Infrastructure-as-a-Service (IaaS) solution with integrated Data Services, with the ability to add additional services through PaaS.

Target Audience: Infrastructure and Operations Teams

Strengths:

- After restructuring, HPE is no longer burdened with the financial debts of HP.

- A complete set of infrastructure (hardware), cloud management, IaaS and PaaS offerings for on-premises solutions.

- Largest installed base of x86 servers and storage.

- Largest installed base of VMware.

- Strength of HPE Services to help customers manage transitions – highlighted in several Wikibon in-depth interviews with customers.

NOTE [Updated – May 24, 2016]: HPE announced a merger of the HPE Enterprise Services Business with CSC.

Weaknesses

- Corporate uncertainty and frequently changing strategy over last 5 years – Is HPE still a company to align longer-term IT strategy?

- HPE has lost many cloud-focused executives and technical leaders over the last 3-5 years (OpenStack, Public Cloud, etc.)

- HPE Helion solution is based on OpenStack, not VMware, so customers need to relearn infrastructure technologies.

- HPE’s Public Cloud strategy, via partners, is not always clear. Some messaging aligns with HPE Service Provider partners, other messaging aligns to HPE / Microsoft Azure partnership, and still other messaging is aligned to AWS / Eucalyptus technical capabilities. HPE does offer customers many choices, but it is not clear where the technical strategy is guiding customers and where engineering resources are focused to help customers integrate Public Cloud services into a HPE Helion solution.

- Cloud Foundry is based on Active State Stackato, which was a fork from original Cloud Foundry and lacks the depth of services of Pivotal Cloud Foundry (Pivotal is #1 contributor to CF) – http://stackalytics.com/?project_type=cloudfoundry-group&release=all&metric=commits

- HPE lacks Enterprise networking. Partners with Arista, Cumulus, and VMware NSX.

Opportunities

- Target customers in industries that are highly regulated and prefer Private Cloud

- Replace existing HP equipment with Helion/Synergy within existing installed base. Build on that momentum into expanded markets (Dell, Cisco, IBM customers).

- Build on existing Microsoft relationship to create deeper integration between Helion and Azure for Hybrid Cloud.

- Leverage the Eucalyptus technology to create deeper integration between Helion and AWS for Hybrid Cloud.

Threats

- Customers continue to be confused by frequent HPE strategy changes.

- Customers still have to operate the Private Cloud. Limited cost reductions unless they adopt highlight automated operations (and reduced headcount)

- Application teams hold greater levels of budget and choose to use Public Cloud (AWS, Azure) for new applications and digital transformation.

- Weak Public/Hybrid Cloud capabilities lead customers to go directly to Public Cloud (instead of via brokerage)

- Customer skip the Private Cloud transformation and focus on VPC between existing applications and Public Cloud

- Application teams may not want to adopt HPE Helion Cloud Foundry.

IBM Bluemix

http://www.ibm.com/cloud-computing/us/en/landing/hybrid.html

Overview of Solution: IBM’s Cloud Solutions are made up of three core elements:

- Softlayer – Provides the cloud data centers and IaaS services

- BlueBox – Providers managed Private Cloud (based on OpenStack) that resides within a Softlayer data center or on the customer’s premises.

- Bluemix – IBM’s version of Cloud Foundry for Platform-as-a-Service (PaaS), with linkage to Data Analytics, Mobile, IoT and other application services.

IBM’s message is heavily influenced by “open” as the core of their offerings, Docker, OpenStack, Cloud Foundry, OpenWhisk. This open messaging is intended to commoditize the elements of Infrastructure-centric competitors, with IBM’s value-add being at the application layers. It also allows IBM to more closely align to the trends around greater usage of open-source software across both development and infrastructure operations. IBM has long been a strong supporter and contributor to many open source projects.

IBM is able to offer Public Cloud and Private Cloud versions of their offering, with “Local” technology, that allows IBM to remotely manage/operate/update resources that reside on-premises. This allows IBM to augment or replace customer’s operations teams.

Cloud Revenues: FY2015 – $6-8B (Public Cloud + Private Infrastructure HW/SW + Services) – Wikibon True Private Cloud forecast

Solution Target: IBM traditionally markets to larger customers (Enterprise, Government), but with the additional of Softlayer and BlueBox, they are now able to reach down into the Mid-Market and larger SMB accounts. IBM traditionally sells fairly high up into an organization, with a mix of products and services, but the BlueBox/Softlayer elements are also allowing customers to go more directly to the services if desired.

Target Audience: IBM’s solution is attempting to reach every decision-maker within a company, from CEO/CIO down to Enterprise Architect, Application Developer and Infrastructure/Operations team.

Strengths:

- Broad set of existing customers that trust IBM to set their technical direction.

- Large, global data center footprint in United States, Europe and Asia.

- Deep expertise with application developers.

- Broad set of vertical market offerings – allows them to sell higher into an account.

- Industry leadership in Big Data (#1 Big Data vendor).

- Solution Areas (http://www.ibm.com/cloud-computing/solutions): Mobile, Analytics, Big Data, DevOps, Enterprise Apps, Business Solutions, HR, ITSM, Marketing, Security, Social/Collaboration, Federal, Retail.

- Growing mix of on-premises and Public Cloud offerings, linked together with managed “Local” operations.

Weaknesses

- Financially struggling; market perception is down over the past 5+ years.

- Softlayer was considered a Managed/Hosting Provider, not a True Public Cloud. Was never highly rated by Gartner MQ for IaaS.

- IBM Solutions displace the infrastructure teams to a large extent – how to interact between application teams and IBM?

- IBM Bluemix is not a significant contributor to Cloud Foundry, or they keep the majority of their development private (only 4% – http://stackalytics.com/?project_type=cloudfoundry-group&release=all&metric=commits)

- IBM or BlueBox are not a significant contributors to OpenStack, or they keep the majority of their development private (8% –http://stackalytics.com/?project_type=openstack&release=all&metric=commits)

- IBM is not a significant contributor to Docker, or they keep the majority of their development private (4% – http://stackalytics.com/?project_type=docker-group&release=all&metric=commits)

Opportunities

- Huge opportunity to move IBM customers back towards a mainframe-type model when they are more tightly aligned to all IBM services/technology.

- Move IBM customers from WebSphere to Bluemix for next-generation applications (Mobile, Analytics, Big Data, Cognitive, etc.)

- Through IBM Local, offer the broadest range of on-premises and off-premises resources, with consistent management that’s offloaded to IBM (reduce operations costs)

- Focus on application-level digital transformation, which brings in IBM services to dominate account control.

- Offer deep integration into existing IBM applications and middleware for next-generation, business applications. IBM brings the legacy application support that AWS or Azure can not.

Threats

- Enterprise businesses see the growth of AWS and look to them as an evolving trusted partner for digital transformation.

- Financial struggles prevent IBM from continuing to invest heavily in Cloud, in favor of other areas (e.g. Mobile, Analytics, Cognitive, etc.)

- IBM middleware gets displaced by Cloud Foundry, Spring (Java) or other application/middleware software, removing a $20B revenue stream and interconnection point into their applications.

- IBM does not grow it’s Public Cloud business and chooses to exit the business, similar to HPE.

- Private Cloud customers continue to want to buy hardware from vendors and place less consideration on IBM Servers, Storage and Networking.

Microsoft Azure

https://www.microsoft.com/en-us/server-cloud/solutions/hybrid-cloud.aspx

Overview of Solution: Microsoft’s Cloud strategy involves multiple elements, which are still under-going changes in 2016 and 2017:

- Microsoft Azure (Public Cloud) – offers on-demand IaaS, PaaS, Data and Developer services from global data centers. Azure is currently #2 in Public Cloud IaaS/PaaS revenues.

- Microsoft Azure Stack (Private/Hybrid Cloud) – released to early beta in Feb. 2016, Azure Stack allows Microsoft customers to install similar software to Azure on their on-premises servers. Microsoft will update the software to maintain compatibility with the Azure Public Cloud. GA is not expected until late-2016 or 2017.

- Cloud Platform System – the current offering to bring Azure-like capabilities to on-premises servers, but with limited scalability.

- Microsoft Office 365 / Dynamics CRM – SaaS versions of popular Microsoft productivity software

Cloud Revenues:

- Intelligent Cloud Division – $6.3B (includes Azure, Windows Server, SQL Server)

- Azure – $1.698M

- Dynamics Online – $178M

- Office 365 – $528M

Solution Target: Microsoft is targeting customers that desire to have consistent Cloud services both on-premises and from the Public Cloud. The primary target is Microsoft applications, but it is expanding to a broader set of open-source technologies and cloud-native application frameworks.

Target Audience: Microsoft targets both their installed base of .NET application developers and Windows Systems Administrators. They are also hoping to attract new developers targeting multi-language/multi-platform next-generation applications such as Mobile, Data Analytics, Machine Learning, AI, IoT.

Strengths:

- Massive installed base of Microsoft applications and developers.

- Shifting trends away from PCs to multiple devices (tablets, smartphones, gaming, etc.) that want a consistent, connected experience, which trend toward Cloud-based applications.

- Huge cash reserves and on-going profitability to invest in infrastructure and R&D to expand their Cloud business or grow through M&A.

- Massive global data center footprint for Microsoft Azure cloud services.

- Shifting DNA in Redmond to become less dependent on the Window OS and more open to a range of technologies that customers desire to use.

- Early announcement of Azure Stack will give existing Windows Server customers time to plan for Hybrid Cloud architectures.

- Deep integration of Visual Studio development tools.

Weaknesses:

- Azure is reportedly not profitable, http://www.businessinsider.com/why-microsofts-cloud-is-hugely-unprofitable-2016-2. Financial details are not yet broken out from on-premises Windows Server, SQL Server.

- Mobile Device strategy has struggled (smartphones, tablets), leading developers to move towards non-Microsoft frameworks for new applications.

- AWS and Google lead in Big Data and Analytics services

- Cloud Platform System partners HPE and Dell are either losing market-share in the Enterprise or have competing Hybrid Cloud offerings (Dell/EMC, HPE/Helion)

- Millennial generation does not look favorably on Microsoft technology.

- Hyper-V trails VMware in on-premises, Private Cloud environments.

Opportunities

- Support for open source and non-Windows technologies in Azure allow Microsoft to potentially capture new developers and next-generation applications.

- Microsoft is able to bundle Azure licensing between Azure and Azure Stack / Windows Server to incent more customers to link the on-premises and Public Cloud environments.

- Azure pricing and performance is frequently better than AWS. Opportunity to attract customers looking for multi-cloud strategy.

- Xamarin acquisitions and integrations offer Microsoft a strong opportunity to reclaim mobile developers on both iOS and Android platforms.

Threats

- If Azure Stack struggles to work properly and Microsoft loses the ability to leverage their existing on-premises customers to move to Azure.

- AWS creates services that attract Microsoft developers away from Azure.

Oracle Cloud

Overview of Solution: Oracle’s Cloud Solutions span SaaS, PaaS and IaaS services. Oracle delivers all of these services via their Public Cloud, and is beginning to deliver them on customer’s premises through Engineered Systems, Machines and Appliances. The core pillars of Oracle Cloud are Oracle Applications, Oracle Database and consistency of Oracle hardware and software in both Public and Private Cloud environments.

Cloud Revenues: Q2FY2016 – $649M; $165M IaaS, $484M SaaS/PaaS – Wikibon True Private Cloud forecast

Solution Target: Oracle Cloud solutions are targeted at extending and migrating existing and future Oracle Applications into the Oracle Cloud, through SaaS, PaaS and IaaS offerings. Oracle solutions are primarily attempting to capture all-Oracle technology stacks (“Red Stack”), although they do have some ability to work with 3rd-party technologies.

Target Audience: Oracle is targeting decision makers from the CIO to VP of Application, VP of Infrastructure/Operations and the many Lines of Business that use the Oracle Applications (ERP, CRM, HCM, SCM, Marketing, Sales, etc.)

Strengths:

- Strong financials that allow them to heavily invest in R&D, data center build-out and M&A.

- Large and loyal installed base of Oracle Applications and Oracle Database that run mission/business critical application and contain critical business data.

- An expanding hardware business that is a catalyst to drive transformation of customers from existing hardware platforms – promise of better performance, security, etc.

- Broad breadth of on-premises and public cloud (SaaS) applications for business, across many business functions.

- Strict software licensing model which can be used to reshape customer usage patterns to align to Oracle product strategies (e.g. Oracle Cloud credits included in ELAs)

- Quickly growing M&A portfolio to fill in Cloud-centric gaps in existing Oracle Cloud (Containers, OpenStack, Cloud Management, etc.)

- Customer business trends moving to mobile and new collaboration models, which works better with Cloud-based applications.

Weaknesses:

- Oracle applications are highly engineered and customized on customer’s premises. May be difficult to migrate them to public cloud.

- Oracle Cloud is made up of internal R&D + acquisitions. Will take time before overall cloud services can be tightly integrated instead of delivered as individual services.

- Customers have concerns about all-Oracle technology stack on-premises and Public Cloud. Concerns about technology lock-in, competitive pricing, and technology refresh cycles.

- Oracle tends to announce new Cloud technologies 12-18 months before they are generally available in the market, often with no pricing information. AWS and Azure are much faster at bringing services to market, with greater price transparency.

- How well will Oracle handle non-Oracle applications and technologies in the Oracle Cloud?

Opportunities:

- By delivering consistency on-premises and in the Oracle Cloud, they have the opportunity to displace on-premises hardware with Engineered Systems, Machines and Appliances, with the goal of creating Hybrid Cloud consistency.

- Oracle’s “Oracle Cloud Machine” has the opportunity to disrupt the traditional CAPEX model by making it on-demand pricing and offering the ability for Oracle to manage elements of the system – deliver a more Cloud-like experience.

- Oracle can manipulate pricing of ELA and Cloud credits to drive more usage towards areas they are trying to grow.

- Oracle has the potential to drive new application development for Enterprise customers if they can built integrations and connectors to existing applications – grow the Oracle SaaS and PaaS business.

Threats:

- Customer concerns about lock-in to the Oracle “Red Stack”.

- AWS and Azure continuing to grow quickly and draw developers to their platform instead of Oracle Cloud.

- Oracle not committing the capital to build out global data centers as overall revenues/profits have slowed.

Red Hat

https://www.redhat.com/en/technologies/cloud-computing

Overview of Solution: Red Hat’s cloud solutions span OS (RHEL), Automation (Ansible), Cloud Management (Cloud Forms), Containers, IaaS (OpenStack), PaaS (OpenShift) and Middleware (JBoss). Red Hat delivers these offerings through a mix of customer options, including free open-source software, paid Red hat software support, on-demand Red Hat software in various public cloud services (e.g. AWS, Azure, Google Cloud Platform), managed cloud providers hosting Red Hat software (e.g. Rackspace), and Red Hat OpenShift as a public cloud service.

Cloud Revenues: Not explicitly reported by Red Hat – Wikibon True Private Cloud forecast

Solution Target: Red Hat cloud solutions are targeted at a broad range of companies that are trying to modernize their infrastructure at either the infrastructure or application layers, and are looking for vendor partners that deliver complete solution stacks. Red Hat cloud solutions build upon their large installed base of Red Hat Linux and attempt to simplify the packaging and operations of modern open source projects (e.g. OpenStack, Docker, Kubernetes, etc.). Red Hat solutions provide customers with a variety of choices about how to acquire the software (free, paid support, managed services, public cloud), as well as independence from underlying hardware requirements.

Target Audience: Red Hat is targeting a mix of IT operations and application developers that feel comfortable using open-source technologies and working with open communities.

Strengths:

- Market leadership in developing, packaging and contributing to open source projects.

- Market leading OpenStack IaaS solution – leading contributor to OpenStack projects.

- Multiple customer options to deliver or consume OpenStack solutions (on-premises, managed services, public cloud).

- Market leadership in automation (Ansible).

- Evolving PaaS platform (OpenShift) based on leading open source projects (Docker, Kubernetes) – leading contributors to both open source projects.

- Multiple customer options to deliver or consume OpenShift solutions (on-premises, public cloud, dedicated public cloud resources)

- Strong Enterprise, Government and Mid-Market footprint of Red Hat Linux. Customers have strong trust of Red Hat for their open source solutions.

- Evolving partnerships with Amazon AWS, Microsoft Azure and Google Cloud Platform.

- Red Hat continues to grow at 15-20% YoY and is the only on-premises open source vendor that is consistently profitable.

Weaknesses:

- Red Hat business model generates the smallest level of revenues of all the Hybrid Cloud competitors.

- OpenStack is still an emerging technology and does not have wide adoption by customers. (see Wikibon analysis from OpenStack Summit 2016).

- Red Hat has limited public cloud offerings beyond Red Hat OpenShift (Dedicated, Online). Red Hat does not deliver an IaaS service, and the OpenShift offerings lack the advanced data services of AWS, Azure and Google Cloud Platform.

Opportunities:

- Emerging partnerships with Microsoft Azure and Google Cloud Platform allow Red Hat to leverage existing customer engagements and offer Hybrid Cloud architectures that span on-premises and public cloud.

- Being a leading contributor and distributor of complex open source technology afford Red Hat the opportunity to help customers that want to leverage the new technologies to build cloud-native applications and drive digital transformation in their business.

- If the technology sector experiences a downturn in 2016-2018, Red Hat is well positioned to acquire or hire top open source talent to help expand their offerings for IaaS, PaaS, automation, etc.

Threats:

- Emerging public cloud services are making the Linux operating system less visible to customers.

- The need for large amount of financial resources to invest in data centers (public cloud) or engineering talent is becoming more critical to all successful cloud vendors. Red Hat will be required to rely more on partnerships to deliver scalable options to customers.

- Red Hat is not part of the Cloud Foundry foundation, and more PaaS vendors (Apprenda, Apcera, CoreOS, Rancher Labs) are adding Kubernetes support to their platform. Differentiating in the PaaS market is becoming more complicated.

Action Item:

The breadth of Hybrid Cloud services and solutions in the market has continued to evolve and expand over the past 2-3 years. While no service or solution provides a consistent experience for both on-premises and public cloud applications, the ability to align a solution to business needs and technology skills is becoming much more viable. Vendors will need to continue to evolve their offerings, and make strategic decisions about how they will address the market – with a great focus on traditional applications or cloud-native applications.