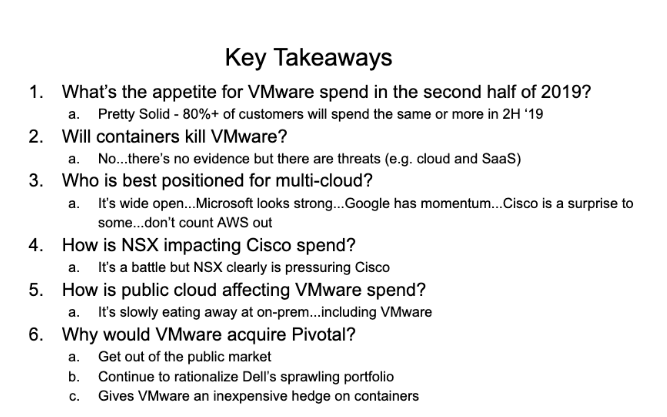

The VMworld 2019 IT spending survey data shows that while customers continue to invest heavily in VMware, organizations are doubling down on their public cloud commitments at the expense of incumbent on-prem infrastructure. As well, the battle for market share amongst enterprise tech companies is heating up as share gains are the most obvious way to offset tepid overall on-prem market growth. This dynamic is creating confusion in the marketplace as trends in cloud, containers, software-defined everything and so-called multi-cloud create both opportunities and risks for buyers.

Key Findings

- Spending on VMware remains strong. Forty-one percent (41%) of respondents said they intend to spend more on VMware technologies in the second half of 2019 than they did in the first six months of the year. Only 7% plan to spend less.

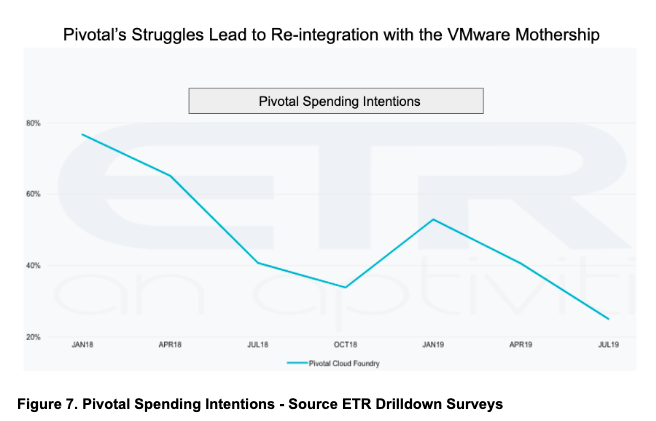

- There is little evidence that containers are hurting VMware. We see VMware’s acquisition of Pivotal as both opportunistic and a hedge against future threats…as well as a governance mandate from Michael Dell.

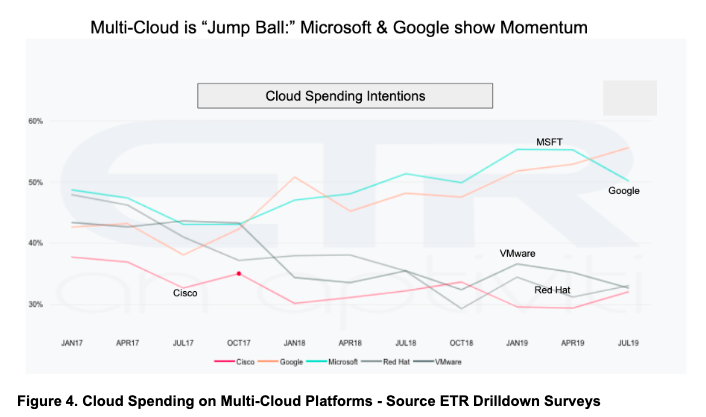

- The multi-cloud opportunity is wide open as the early market forms. However the data shows that Google and Microsoft have mindshare momentum in this space with customers, while VMware, IBM Red Hat and Cisco are well-positioned to compete. Although AWS marketing does not publicly acknowledge multi-cloud, we believe the company will be a major player in this space going forward.

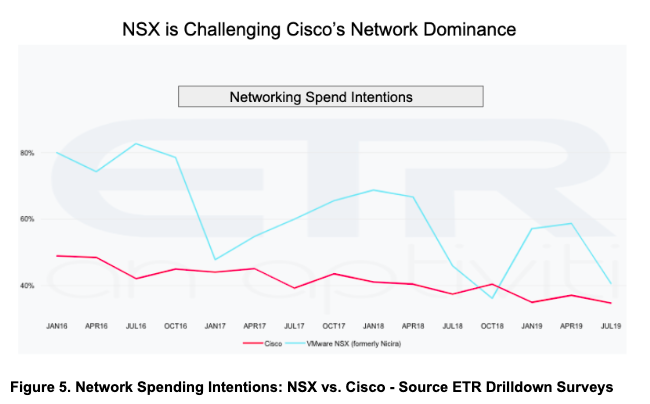

- Interest in NSX is strong and the data suggests this is negatively impacting Cisco. Fifteen survey data snapshots since January of 2016 show a gradual but steady downward slope in spending intentions on Cisco networking. Nonetheless, Cisco remains the dominant networking player with a majority of its installed base remaining loyal to the company’s networking products.

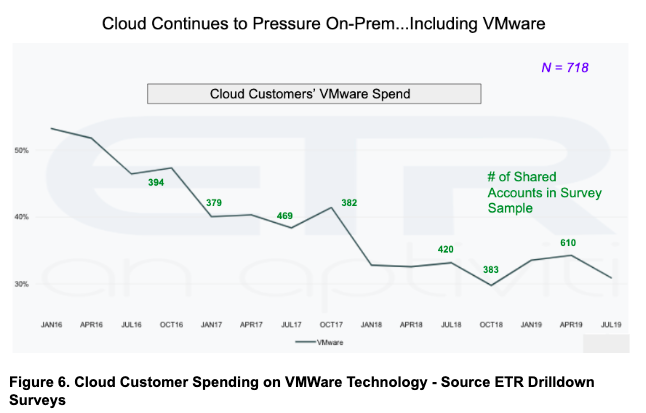

- Public cloud spending is impacting on-prem infrastructure and VMware is not immune. Customers continue to spend more on public cloud at the expense of on-prem deployments. VMware spend amongst cloud customers has been steadily declining since 2016 and vendor claims of widespread repatriation don’t appear to be meaningful.

- Pivotal spending patterns have been negative for eighteen months. Survey data shows that spending intentions for Pivotal technologies have been meaningfully in decline since the Jan 2018 survey. We believe that Dell, which controls Pivotal voting shares, is making moves to stop the negative momentum, eliminate public stock market scrutiny, consolidate some software assets and give VMware a future hedge against containers.

Background and Methodology

Enterprise Technology Research (ETR) is a primary technology market research firm. The company has ten years of history, capturing real-time spending intentions from a panel of more than 4,500 enterprise technology buyers, representing nearly one trillion dollars in spending power. ETR has provided SiliconANGLE access to its survey data and experts to help us better understand customer buying intentions. Our first collaboration related to IBM’s acquisition of Red Hat.

This current survey highlights key spending patterns within the VMware ecosystem. Ahead of VMworld 2019, and to mark theCUBE’s tenth year at VMworld, we partnered with ETR to provide data to critical questions on the minds’ of customers and technology players within our respective communities. We have analyzed ETR survey data over the past forty-two months comprising fifteen “Drilldown” surveys, each with many hundreds of respondents (e.g. 693 in the latest July survey), representing hundreds of billions of dollars in annual spending.

We explored the following six key questions for IT spending survey:

VMware Spending Intentions – 2H ‘19

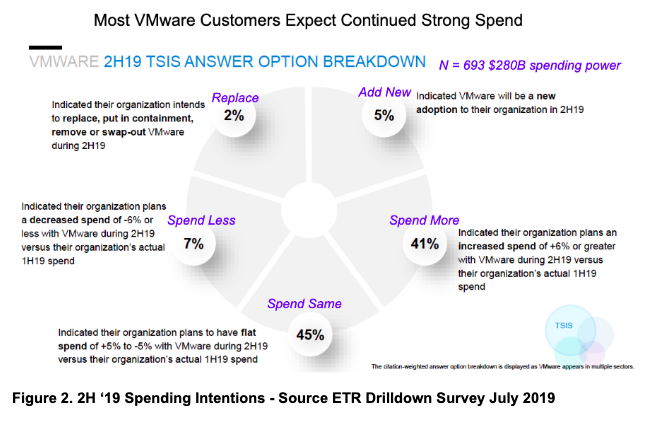

Figure 2 shows summary data from the VMworld 2019 IT spending survey for the second half of 2019. Respondents were asked if their 2H 2019 spending would increase decrease or stay flat, relative to the first half of 2019. The key takeaways are:

- 86% of customers said they expect to spend the same or more in 2H ‘19

- 41% plan to spend more than 6% relative to the first half

- Only 7% plan to cut spending by more than 6%

- Very few customers are replacing VMware

Note: This data is not unusual for an entrenched incumbent like VMware. Customers are familiar with an incumbent’s technologies and switching costs are rarely warranted for a leading platform such as VMware.

Will Containers Kill VMware?

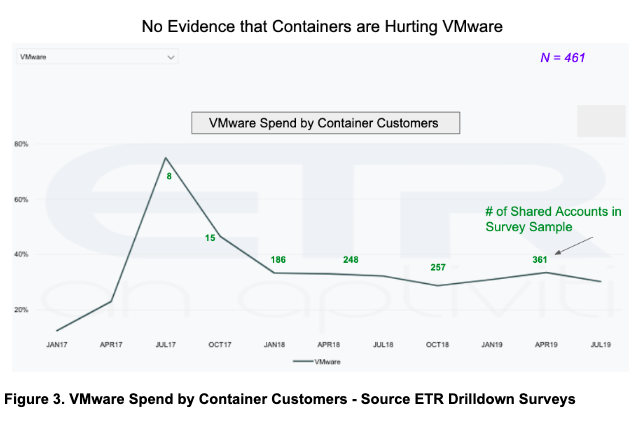

Figure 3 shows that customers with high container adoption continue to spend on VMware technologies across the board (i.e. compute, storage, networking, EUC, etc.). NSX and vSAN spending were particularly strong, affirming VMware’s public statements.

Of note in this data are the number of shared accounts between those heavily adopting containers and VMware buyers. Two years ago the number of shared accounts was minimal, however the more recent surveys allowed us to analyze several hundred shared accounts. The trendline shows that VMware spend remains strong despite predictions that containers will kill VMware.

Anecdotally, customers tell us that they deploy containers in a variety of use cases, some negative some positive for VMware – e.g. both in bare metal deployments and on top of VMs. The acquisition of Pivotal gives VMware a strong incentive to further drive synergies with enterprise Kubernetes (PKS) in support of VMware’s multi-cloud intentions.

One caveat. As shown later in Figure 6, cloud is a major threat to on-prem suppliers, including VMware. As containers are deployed in the cloud and used in SaaS offerings, the impact to VMware could be downward pressure. Why? Because the leading SaaS players are generally not building on top of VMware and increasingly they’re moving to the public cloud.

Who Will Lead Multi-Cloud?

Note: Figure 4 is nuanced. We chose the five companies for the VMworld 2019 IT spending survey that we considered to be potential leaders in so-called multi-cloud. We then cut the data by assessing cloud-related spending on those top platforms as a proxy for multi-cloud.

Both Microsoft and Google show strength here. We attribute this to Microsoft’s strong position in both public cloud, on-prem and software apps. Increased interest generally in Google Cloud as an alternative hedge to AWS is likely providing momentum for Google along with Google Anthos, the company’s recently announced multi-cloud offering.

Notably, VMware (data center OS), IBM Red Hat (OpenShift + IBM Global Services) and Cisco (strength in networking and security) are bunching up as the on-prem leaders. We did not include AWS in this analysis as they don’t publicly acknowledge intentions to compete in multi-cloud. However we believe at some point, if the market asks for it, AWS will be a major player in this space.

Based on the approach we took we have to be careful about the conclusions we draw. After all…what is multi-cloud? We believe that the term really is aspirational today and reflects the state of bespoke multi-cloud choices (multi-vendor) rather than a coherent customer strategy. In other words, customers have chosen multiple clouds for different use cases and different reasons (e.g. shadow IT, different corporate divisions, developer preference, etc.). These clouds are disaggregated and loosely coupled at best, each with its own homegrown orchestration and automation software often born of an open source fork that is now proprietary. Today, integration with on-prem systems is lightweight or non-existent.

The vision of true multi-cloud implies a massively scalable distributed system comprised of multiple public clouds and on-prem applications. These systems have tightly integrated control and data planes. Wikibon (SiliconANGLE’s sister firm) asserts that to conform to the vision of true multi-cloud, the system must incorporate hybrid architectures and: “any application or application service can run on any node of the hybrid cloud without re-writing, re-compiling or re-testing. True Hybrid Cloud architectures have a consistent set of hardware, software, services, APIs, with integrated network, security data, and control planes that are native to and display the characteristics of public cloud infrastructure-as-a-service. These attributes can be identically resident on other hybrid nodes independent of location (e.g. including public clouds, on premises or at the edge).”

It’s safe to say that this strict definition of multi-cloud doesn’t exist today and perhaps may never become a reality. To achieve this vision, buyers are more likely in the near term to deploy a highly homogenous infrastructure stack (e.g. AWS Outposts, Azure Stack, Oracle Cloud at Customer), however this will not really comprise multiple public clouds and be highly proprietary in nature.

We do believe that managing and orchestrating a consistent set of services across multiple cloud and on-prem domains will be a requirement; particularly with regard to security, compliance and infrastructure deployment. The reality is that this will be a journey for customers and will take many years to achieve.

Networking: The Battles of the NSXes

ETR survey data shows that on balance, the networking sector is being pressured by public cloud, which accounts for some of the downtrend shown in Figure 5. Nonetheless, the data shows that VMware’s Nicira acquisition and its strong SDDC marketing are having an effect on the spending intentions of Cisco’s customers. VMware has stated that it wants to do to networking (and storage) what it has done to compute. And we don’t think that’s good news for Cisco and other infrastructure providers. This shows up in that data above as since early 2016, spending intentions on Cisco networking gear has steadily waned, while interest in NSX has bounced above the trendline.

Cisco of course has countered with its own software-defined vision and has aggressively launched efforts to make its infrastructure programmable with the DevNet group. ETR data shows that Cisco customers continue to be loyal and spend heavily on Cisco infrastructure.

How will Public Cloud Spending Impact VMware?

Figure 6 shows the three plus year trend on VMware spending intentions over fifteen drilldown surveys. The data clearly shows that cloud customers are shifting their priorities and despite the strength of VMware, public cloud continues to grow at the expense of on-prem infrastructure. VMware is not shielded from this mega-wave.

To counter this effect, VMware has cut deals with all the major cloud players with AWS being the most prominent. But we believe VMware sees multi-cloud management and orchestration as a way to offset this pressure and create new TAM opportunities. Hence its aggressive acquisition posture and moves to create a leading multi-cloud offering in the marketplace.

Pivotal Pivots and VMware’s Container Hedge

VMware announced last week that it would acquire Pivotal in a deal valued at $2.7B. Figure 7 shows the 18 month trendline for spending intentions on Pivotal technologies. The downward trajectory is meaningful and mirrors Pivotal’s struggling stock price since its IPO. We believe this deal is driven by three primary factors:

- Pivotal’s poor stock performance.

- Dell’s dominant ownership structure and VMware’s cash allows Pivotal to expediently get out from under Wall Street scrutiny.

- It gives VMware an integrated container play and a hedge by picking up an asset valued at $4B for only $900M in cash.

For a detailed analysis of the deal structure and its implications see this video.

Along with Pivotal, VMware is acquiring Carbon Black, a Waltham, MA based security company with a large portion of its revenue derived from SaaS (almost 40%). Currently VMware’s SaaS business represents around 12% of company revenues. The acquisitions of Pivotal and Carbon Black are expected to add roughly $1B in SaaS revenue in the first year and $3B by year two.

Combined with several other acquisitions in the security and hybrid cloud space, we believe VMware has a sense of urgency to stem the cloud threat shown in Figure 6 and break out from the multi-cloud pack.

Many thanks to our friends at ETR. This summary barely scratches the surface and there are many more powerful cuts on the data. As always please don’t hesitate to get in touch if you have questions or comments.

We’ll be covering these and many other issues celebrating our 10th year at VMworld with theCUBE. We’re in the lobby of Moscone North so please stop by and see us.

Here’s a video we did this week with a cliplist summarizing the VMworld 2019 IT spending survey and the key questions addressed above…Thanks for watching.